A lot of owners don’t ask what their business is worth until something forces the question.

A partner wants out. A bank asks for more than a tax return and a handshake. A family transition gets real. Or someone casually says, “If you ever want to sell, call me,” and suddenly the number matters.

That’s why business valuation methods for small business matter long before a sale. Value isn’t just a sale price. It’s a report card on how clean your books are, how dependable your profit is, and how much risk a buyer sees when they look under the hood.

What Is Your Business Actually Worth and Why It Matters Now

A West Chester business owner once described it to me like this: “I’m not selling, so why would I pay attention to valuation?” Fair question. Then his partner started talking about stepping back, and the conversation changed fast.

When you need a number, you usually need it quickly. That’s a bad time to discover your books are messy, your owner pay runs through five different accounts, and nobody has a clean answer for what the business earns without you in the middle of everything.

Valuation is not just for a sale

Think about a few common situations:

- A partner buyout: One owner leaves. The other stays. You need a fair number both people can live with.

- A loan or financing request: Lenders want to understand the strength of the business, not just the top line.

- Succession planning: If family is involved, guessing creates tension. A grounded valuation gives everyone something concrete.

- Day-to-day decision making: If you know what drives value, you can make better calls on pricing, hiring, and spending.

A lot of owners treat valuation like a home appraisal done right before listing the house. I think it works better as an annual physical. It tells you where you stand today and what needs work before a buyer, lender, or partner starts asking harder questions.

Your business value is not just a price tag. It’s a summary of profit, risk, and how transferable the company is without you.

The number is only part of the story

Two businesses can have similar revenue and very different value. One has clean books, repeat clients, and a team that runs without the owner. The other depends on the owner for every major relationship and has a profit and loss statement full of personal expenses. Same industry. Very different outcomes.

That’s why I tell owners to stop asking only, “What could I sell for?” Ask, “What would a buyer worry about?” That question usually gets you to the right work faster.

If you want a practical overview of how owners start this process, this guide on how to value a small business for sale is a useful starting point.

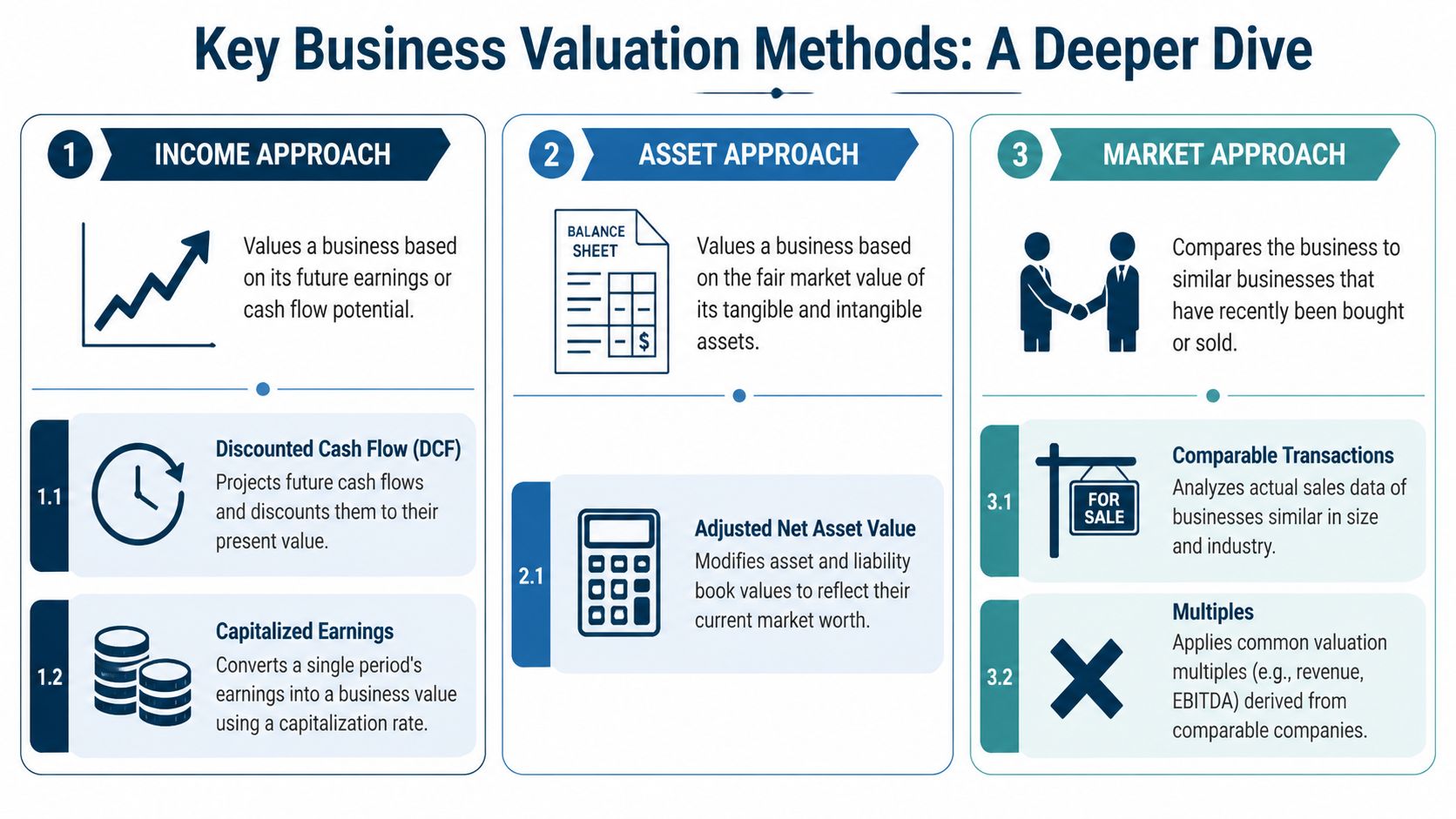

The Three Main Ways to Price a Business Explained Simply

Most valuation talk sounds more complicated than it needs to be. Strip away the jargon, and there are really three main ways to price a business.

Asset approach

This is the “what is all your stuff worth?” method.

If you were selling a used truck for parts, you’d look at the engine, tires, body, and anything else that has resale value. Businesses work the same way under the asset-based approach. You add up assets, subtract liabilities, and see what’s left.

This method tends to fit businesses where the assets matter a lot. Think equipment-heavy operations, real estate related firms, or companies in distress where the buyer cares more about what can be sold than what the future profit looks like.

Where it works well

- Asset-heavy companies: Equipment, vehicles, inventory, or property play a big role.

- Distressed situations: If earnings are weak, future income is less persuasive.

- Floor value checks: It can show the minimum value support under the business.

Where it falls short

- Service businesses: A bookkeeping firm, law office, or agency usually isn’t worth much based on desks and laptops alone.

- Businesses with strong cash flow: Asset value can miss the actual earning power.

Market approach

This is the Zillow version of valuation.

You price a house by looking at what similar houses nearby sold for. The market approach does the same thing with businesses. You compare your company to similar companies that recently sold and apply the kinds of multiples buyers paid.

This approach makes sense because buyers don’t value your business in a vacuum. They compare it with other deals.

Income approach

This is the rental property way of thinking.

When someone buys a rental, they care about the cash it will produce. Same with the income approach. A buyer asks, “What will this business earn for me, and how risky is that income?”

This method usually fits profitable businesses with stable cash flow. It’s common for professional services, healthcare practices, and owner-operated firms where the earnings tell the clearest story.

Practical rule: If your business makes money consistently, income usually matters more than furniture, fixtures, and old equipment.

Which one should you trust

Here’s the simple answer. None of these methods should stand alone without context.

A smart valuation usually uses more than one lens. Asset value can provide a baseline. Market data can show what buyers are paying. Income can show what the company is worth based on profit. When those methods tell a similar story, your confidence goes up. When they don’t, that gap usually points to a problem worth investigating.

A Deeper Look at Key Business Valuation Methods

Most owners hear terms like revenue multiple, SDE multiple, DCF, and capitalization rate and feel like they need a translator. You don’t. The math is not the hard part. The hard part is knowing when a method fits the business in front of you.

Market multiples in plain English

The market method uses actual sale patterns as a guide. According to BizBuySell, the average American small business sells for 0.6 times annual revenue, and for businesses with under $5 million in revenue, the average SDE multiple is 2.5x according to Lendio’s summary of business valuation methods.

That gives you two different lenses already. One is based on revenue. The other is based on owner benefit, which is often more useful for small owner-operated companies.

Here’s a simple whiteboard example taken from the same source. If comparable businesses in a relevant field sell for 2 times annual revenue, then a business with $500,000 in revenue could be valued at $1 million. That doesn’t mean every business with that revenue gets that number. It means the market method starts with comparable deals, then adjusts for quality, risk, and fit.

Why multiples are useful and dangerous

Multiples are useful because they’re fast and tied to real transactions. They’re dangerous because owners grab a number off the internet and use it like gospel.

A multiple only means something if the comparison is close. Same size. Same kind of customer. Similar margins. Similar owner involvement. Similar location and risk.

Here’s a quick way to think about it:

| Method | What it asks | Good fit | Main weakness |

|---|---|---|---|

| Revenue multiple | What do similar businesses sell for based on sales? | Simple benchmark for small businesses | Ignores profit differences |

| SDE multiple | What cash benefit does an owner get from the business? | Owner-operated companies | Depends on clean add-backs |

| Comparable transactions | What did businesses like this actually sell for? | Markets with good deal data | Weak if there are few true comps |

If you want a practical reference point, this resource on business valuation multiples by industry helps show why one multiple rarely fits every business.

Capitalization of earnings

This method sits under the income approach. It works best when a business has steady earnings and a buyer can reasonably expect that pattern to continue.

The idea is simple. You take normalized annual earnings and divide them by a capitalization rate, which reflects risk and expected return. Grifco gives a clean example: $100,000 in normalized annual profit divided by a 10% capitalization rate equals a value of $1 million in its overview of small business valuation methods.

Write it on a napkin and it looks like this:

- Normalized profit: $100,000

- Cap rate: 0.10

- Value: $100,000 ÷ 0.10 = $1,000,000

The logic is straightforward. Lower perceived risk supports a lower cap rate, which produces a higher value. Higher risk pushes the cap rate up and value down.

Discounted cash flow

DCF sounds intimidating, but the concept is basic. Money you receive later is worth less than money you receive today. So you project future cash flow and discount it back to today’s dollars.

Grifco’s example uses $100,000 annual profit over five years with a 10% discount rate, which produces a present value of about $380,000. That’s useful for a growing business where future earnings matter, but it depends heavily on assumptions. If your forecast is shaky, the answer will be shaky too.

A DCF is only as believable as the forecast behind it. If the projections are optimistic fiction, the valuation is too.

Asset-based valuation

This one is often the easiest to explain and the easiest to misuse.

If your business owns meaningful hard assets, this approach matters. If you run a professional service firm with modest equipment and most of the value sits in client relationships and recurring profit, asset value will usually understate the story.

That’s why no serious buyer should rely on just one method. In practice, the strongest valuations pull from market evidence, income logic, and asset reality, then ask which one best matches the stage of the business and the reason for the valuation.

SDE versus EBITDA What Each Reveals About Your Business

These two terms get tossed around like they mean the same thing. They don’t.

If you own a small business and you still work in it every day, SDE often tells the more useful story. If the business has a real management layer and the owner is less central to day-to-day operations, EBITDA usually becomes more relevant.

What SDE is trying to show

Seller’s Discretionary Earnings is built for owner-operated businesses.

It starts with profit and adjusts for expenses that wouldn’t continue the same way under a new owner. That can include the owner’s compensation, certain perks run through the business, and one-time items. The goal is to show the total financial benefit available to one working owner.

This is why SDE often matters in local service businesses. Think contractor, clinic, bookkeeping practice, or small law office. A buyer isn’t just asking, “What is the company profit?” They’re asking, “What does this business generate for the person who buys and runs it?”

What EBITDA is trying to show

EBITDA strips out interest, taxes, depreciation, and amortization to focus on operating earnings.

It’s a cleaner operating measure for businesses where the owner is not the whole engine. Buyers and investors use it because it helps compare one company to another without getting bogged down in capital structure or tax differences.

According to Entrepreneurs Forever’s explanation of small business valuation, a business with a $125,000 two-year average EBITDA and a 4x multiplier would be valued at $500,000. The same source notes that multiples vary a lot by industry, with high-growth professional services potentially seeing 5x to 10x, while more cyclical industries might see 2x to 4x.

Side by side comparison

| Measure | Best for | What it highlights | Common issue |

|---|---|---|---|

| SDE | Owner-operated small businesses | Total owner benefit | Bad bookkeeping can hide real add-backs |

| EBITDA | Larger or more structured businesses | Core operating earnings | Can miss the reality of owner dependence |

Which one should you care about

If the business can’t run without you, start with SDE. If you have managers, cleaner departmental reporting, and the business functions more like a stand-alone company, EBITDA becomes more meaningful.

A lot of owners make the mistake of jumping to EBITDA because it sounds more complex. Complexity is not the goal. Accurate is the goal.

If a buyer is replacing you with themselves, SDE usually tells the truth better. If a buyer is keeping the company structure and evaluating operating performance, EBITDA often tells the truth better.

Your Checklist for Normalizing Earnings and Adjusting Value

A good valuation often determines whether it wins or loses credibility.

Your tax return and your internal profit and loss statement are not the same thing as normalized earnings. Buyers want to know what the business earns on a repeatable basis. That means cleaning out noise.

What normalizing earnings means

Normalizing means adjusting your financials so they reflect the business’s true ongoing earning power.

That matters because value is tied to earnings and risk. As noted earlier in the income-based example from Grifco, $100,000 in normalized annual profit at a 10% capitalization rate points to $1 million in value. If your earnings aren’t normalized correctly, the number built on top of them won’t be reliable.

A practical add-back checklist

Here are common areas to review before anyone talks multiples.

- Owner compensation: If your pay is above or below what the market would require for someone doing your job, adjust it. Buyers want a realistic operating picture.

- Personal expenses through the business: Travel, meals, vehicles, or subscriptions that mainly benefit the owner should be separated from real business costs.

- One-time legal or professional fees: If the expense was unusual and not part of normal operations, flag it.

- Non-recurring repairs or disruptions: A strange equipment failure or unusual cleanup cost may not reflect ongoing earnings.

- Related-party rent: If the business pays rent to a building you also own, the amount may need to be adjusted to a market rate.

- Owner-specific perks: Health costs, family payroll, or discretionary spending need a close look when they won’t continue for the next owner.

What buyers will ask

Buyers usually don’t reject add-backs because the category is wrong. They reject them because the proof is weak.

Keep support for each adjustment:

- General ledger detail

- Invoices or statements

- Clear explanation of why the cost is non-recurring or discretionary

- A bridge from reported profit to normalized earnings

A good quality of earnings report helps organize this story in a way buyers, lenders, and advisors can follow.

The trap to avoid

Owners sometimes treat add-backs like wish lists. That backfires.

If the expense will keep happening after a sale, it probably doesn’t belong as an add-back. If the explanation takes ten minutes and still sounds fuzzy, it likely won’t survive diligence. The goal is not to inflate profit. The goal is to present honest earnings clearly enough that a buyer believes them.

Common Valuation Mistakes That Cost Owners Real Money

The most expensive mistake is simple. Owners wait too long.

They don’t value the business while they still have time to improve it. They wait until a sale, health event, partner issue, or family transition forces action. By then, the number is what it is.

Mistake one is bad timing

A major gap in valuation advice is timing. Most guides explain how to value a business but not when valuation is most useful. Clearly Acquired points out that many owners miss opportunities to improve value because they don’t address valuation timing and lifecycle in its article on the three core methods of valuing a small business.

That’s exactly right. A valuation done early gives you options. A valuation done late gives you consequences.

Mistake two is using the wrong shortcut

Owners love rules of thumb because they’re fast. The problem is that shortcuts often skip the details that move value up or down.

A multiple without context is just a rumor. If your business has customer concentration, weak documentation, owner dependence, or spotty margins, the “standard industry multiple” you found online may have nothing to do with your actual business.

Mistake three is messy books

This one isn’t glamorous, but it matters.

If your books are behind, inconsistent, or full of personal spending mixed with business spending, buyers start distrusting everything. They’ll question the earnings. They’ll question the add-backs. They’ll question whether the business can survive due diligence. Once trust drops, value usually follows.

Buyers can handle bad news faster than they can handle unclear numbers.

Mistake four is ignoring intangible value and transfer risk

Some owners focus only on hard assets. Others do the opposite and talk only about brand and “potential.” Both can miss the mark.

A buyer wants transferable value. That can come from systems, recurring clients, trained staff, and clean reporting. If the goodwill lives only in your head or in your personal relationships, it’s fragile. Fragile businesses trade differently than transferable ones.

The fix is not complicated. Start earlier. Match the method to the business stage. Keep the books clean. Build a company that can function without you in every decision.

Your Next Steps to Prepare for a Business Valuation

If you’re thinking about valuation today, start with your books. Not next quarter. Not after tax season. Today.

No valuation method can rescue bad records. If your financial statements are late, inconsistent, or hard to explain, every later step gets harder.

If a sale is not close

When a sale is still years away, the focus should be on building value, not guessing value.

That means improving the parts of the business a buyer cares about most:

- Cleaner financial reporting: Monthly statements should be timely and understandable.

- Stronger profit visibility: Know which customers, jobs, or services are profitable.

- Less owner dependence: If every major decision lands on you, the business is harder to transfer.

- Documented processes: Buyers pay more comfortably when the operation can be learned and repeated.

For owners who want a broader perspective on appraisal work, resources like Nanak Accountants and Associates’ business appraisal solutions can help show how formal valuation support is framed in practice.

If a transaction may happen sooner

The closer you get to a sale, buyout, or succession event, the more the work shifts from growth to de-risking.

Focus on:

- Reconciling the books cleanly

- Separating personal and business expenses

- Documenting add-backs with support

- Summarizing key contracts, customers, and vendor relationships

- Showing that the business can function without daily owner heroics

This is also where an outside advisor can help pressure-test the story. MyOfficeOps is one option for owners who need bookkeeping, financial analytics, and valuation-related advisory tied to exit readiness. The practical value is not a magic formula. It’s getting the financial picture organized well enough that a buyer, lender, or partner can trust it.

A simple timeline to work from

Here’s the plain version.

| Timing | What to do now |

|---|---|

| Today | Clean up bookkeeping, separate personal expenses, and make sure reporting is current |

| Next year | Track profitability by service line, customer, or job and reduce owner dependence |

| Longer term | Build systems, document processes, and make the business easier to transfer |

The best time to understand value is before you need it. That gives you room to improve it.

If you want a clearer picture of what your business is worth and what’s getting in the way of a stronger valuation, MyOfficeOps helps small and midsize business owners get their books clean, normalize earnings, and prepare for valuation, transition, or sale with practical CFO-style support.