If you're like most owners I talk to, you have a rough number in your head for what your business is worth. Maybe it's based on revenue. Maybe it's based on profit. Maybe it's based on how hard you've worked for years to build it.

The problem is that buyers don't pay for effort. They pay for a business they can take over, run, and grow.

That's why enterprise value calculation matters. It gives you a more complete view of what someone is really buying. For a small business owner, that matters long before a sale. It affects lending conversations, partner buy-ins, succession planning, and the choices you make now that shape your exit later.

What Is Enterprise Value and Why It Matters

A lot of owners start with the wrong question. They ask, "What did I make last year?" or "What's my revenue?" Those numbers matter, but they don't tell the full story.

Enterprise value is closer to the actual price tag of your business. Think about buying a car from a private seller. You don't just look at the sticker price. You also look at whether there's a loan on the car. And if the seller leaves cash in the glove box, that lowers what the buyer is really out of pocket. Business value works in a similar way.

The simple way to think about it

A buyer isn't only buying your profit stream. They're also taking on certain obligations and gaining access to certain assets.

That is why enterprise value is more useful than a quick revenue multiple pulled from a conversation at an industry event. It tries to answer a practical question:

If someone bought the whole company, what would they really be paying for the operating business?

For public companies, the standard foundation is EV = Market Capitalization + Total Debt – Cash and Cash Equivalents, with more complete versions also adding preferred stock and noncontrolling interest for accuracy, as explained in Sage's overview of enterprise value.

For a small private company, you usually won't have a public stock price. But the logic still holds. The buyer cares about the business itself, not just the equity on paper.

Why owners should care before a sale

Enterprise value matters because it changes how you run the company.

If you pile on debt, that affects value. If the business sits on excess cash, that affects value differently. If your books are messy, buyers will question every adjustment. If your earnings are clean and repeatable, the company becomes easier to value and easier to sell.

A lot of owners also discover that their internal numbers aren't organized in a way that helps with valuation. If you're cleaning up records ahead of planning work, a practical reference like Snyp for UK company accounts can help you think through how financial reporting should be prepared before anyone starts talking about value.

For a broader look at how EV fits with other approaches, it's also worth reviewing these small business valuation methods. Enterprise value is one lens, but it's one of the most useful because it forces you to think like a buyer.

What EV does better than a gut estimate

Here is where owners usually get tripped up:

- Revenue can flatter a weak business. A company can sell a lot and still be hard to transfer.

- Net income can be distorted. Owner pay, one-time expenses, and tax choices can muddy the picture.

- Bank balance isn't business value. Cash in the company helps, but it isn't the same thing as sustainable earnings.

Practical rule: Buyers pay for future earning power, then adjust for debt, cash, and anything else that changes what they're actually getting.

Once you see enterprise value this way, the next step gets easier. You stop asking, "What number do I want?" and start asking, "What would a rational buyer adjust?"

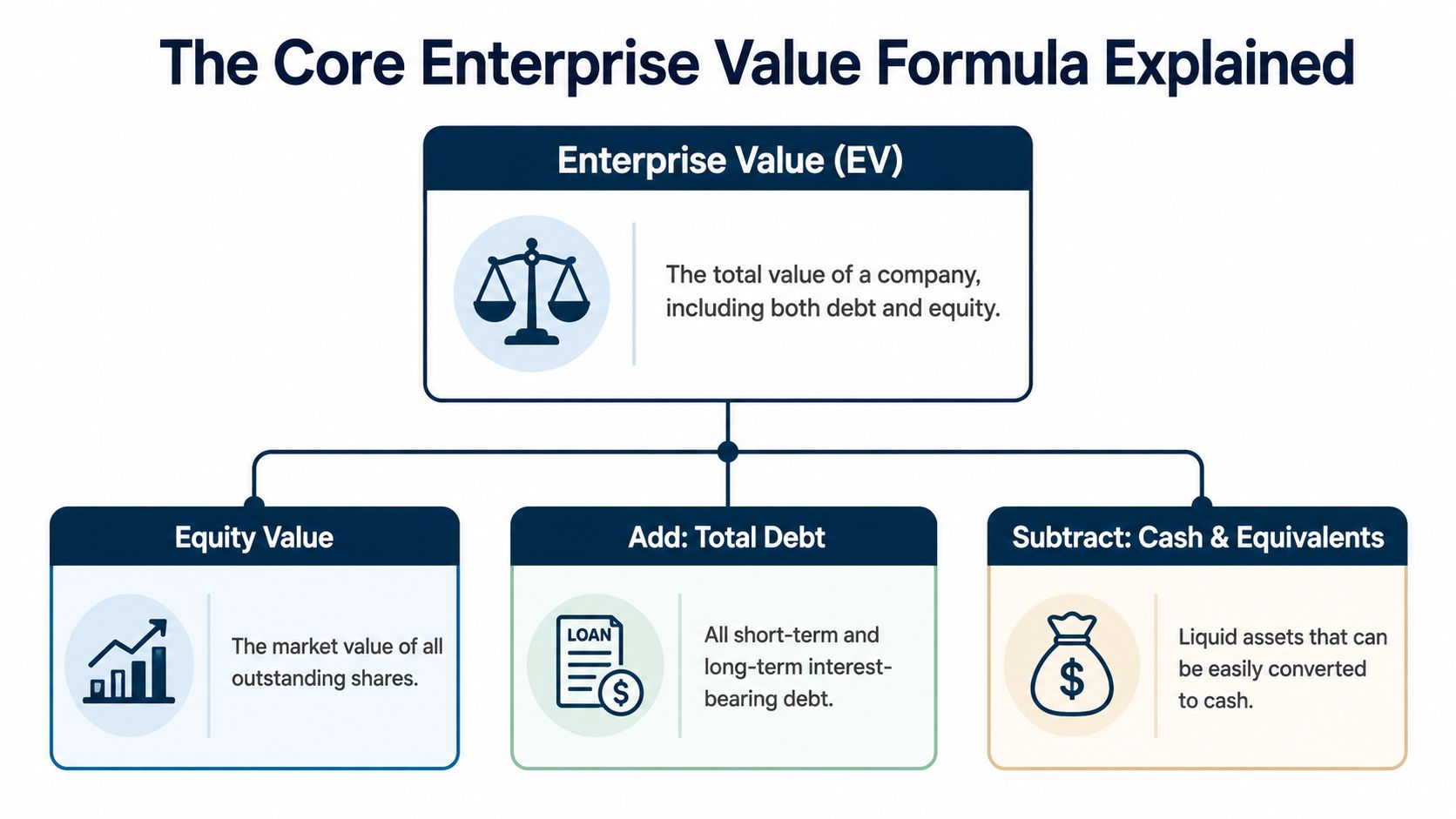

The Core Enterprise Value Formula Explained

An owner gets excited about a valuation number, then the buyer starts adjusting for debt, cash, and financing obligations buried in the balance sheet. The headline value drops fast. That usually happens because the formula looked simple, but the inputs were treated too casually.

The formula is simple. Enterprise Value = Equity Value + Total Debt – Cash and Cash Equivalents. In more complex capital structures, preferred stock and noncontrolling interest can also be added because they represent claims on the business that affect what a buyer is really paying for.

For a public company, equity value usually starts with market capitalization. As NetSuite explains, market capitalization is the current share price multiplied by outstanding shares.

Most small business owners do not have a quoted share price. So for a privately held company, equity value is usually an estimate based on earnings, cash flow, or revenue multiples. That is the practical difference that matters. Public companies can look up equity value. Private owners have to build it.

How private companies estimate equity value

In real deals, owners usually start with a rough valuation multiple, then test whether the underlying numbers would survive buyer diligence. A profitable services firm may be valued off adjusted EBITDA or seller's discretionary earnings. A smaller distributor might be discussed in terms of EBITDA. A software business may get more attention on recurring revenue quality than on current profit.

The method matters less than the discipline behind it. If the earnings figure is inflated by personal expenses, one-time costs, or inconsistent bookkeeping, the equity estimate will be off before debt and cash are even added in. If your books need cleanup before you can separate financing items from operating items, Allied Tax Advisors' guide for startups is a useful reference for what a clear balance sheet should include.

What counts as debt and cash

In this regard, privately held businesses often get messy.

Debt usually includes more than the obvious bank loan. Buyers often review lines of credit, equipment notes, seller-financed obligations, and sometimes lease-related liabilities depending on the deal structure. The practical question is straightforward: what obligations must be repaid, assumed, or reflected in price at closing?

Cash also needs judgment. A buyer may not give full credit for every dollar sitting in the account because some of that cash is required to run the business normally. Payroll, vendor timing, tax payments, and working capital swings all affect how much cash is excess.

A simple mechanics example

The math itself is not complicated. If a company has equity value of $10 million, debt of $2 million, and cash of $500,000, enterprise value is $11.5 million.

For a private company, the challenge is rarely the arithmetic. The challenge is deciding whether the equity estimate is realistic, whether all financing obligations were captured, and whether the cash balance includes money the business needs to operate. Those judgment calls directly affect what an owner can expect to receive in a sale.

A practical first pass

Use this sequence for a first draft:

- Estimate equity value. Use a valuation method that fits your type of business and your size.

- Add interest-bearing debt. Include obligations a buyer would inherit or require you to clear.

- Subtract cash and equivalents. Separate excess cash from the operating cash the business needs.

- Review other claims. Preferred equity, minority interests, or unusual financing terms can change the result.

The formula is easy to memorize. The sale price depends on how accurately you classify each line item.

That is why two companies with similar revenue can produce very different enterprise values. One owner has organized records, manageable debt, and earnings a buyer can trust. The other has unclear liabilities, cash that is tied up in operations, and an equity estimate built on numbers that will not hold up in diligence.

Important Adjustments Beyond the Basic Formula

A deal can feel on track right up until the buyer starts marking up your balance sheet. The headline value looks fine in the first conversation. Then questions about debt, cash, and off-book economics start pulling that number apart.

That is normal in a private company sale.

Buyers are not just checking the formula. They are testing whether the business will transfer with the same earning power, working capital, and risk profile they believed they were buying. For an owner, these adjustments matter because they change what ends up in your pocket at closing, not just what appears in a valuation summary.

A small firm example

Take a consulting firm with recurring clients, solid margins, and a healthy bank balance. The owner assumes the cash adds value dollar for dollar.

A buyer looks closer.

Part of that cash covers uneven collections and payroll timing. The company also has a line of credit that gets used during slow months. On top of that, it holds an investment account that has nothing to do with serving clients. Those items do not belong in one bucket, and treating them as if they do can distort value fast.

Net debt is where many sale proceeds change

In private deals, net debt is less of a textbook concept and more of a closing reality. Buyers care about what they are taking on, what cash stays in the business, and what obligations reduce the seller's proceeds.

That means the review usually goes beyond the obvious term loan. It can include shareholder loans, equipment notes, capital leases, overdue taxes, earnout-related obligations, and any interest-bearing balance that a buyer expects to assume or have cleared before closing.

Cash requires the same discipline. A buyer may let you keep excess cash, but not the amount required to run the company normally. If your business needs cash to bridge receivables, fund inventory, or cover payroll swings, that portion is operating cash, not a bonus sitting on top of value.

This is one reason owners are often surprised late in a process. They hear an attractive offer, then learn the equity check depends on debt-like items and a working capital target that were never analyzed carefully at the start.

Operating assets versus non-operating assets

Enterprise value is meant to reflect the value of the operating business. If an asset does not help produce the core earnings a buyer is paying for, it may need separate treatment.

Common examples include:

- Investment accounts or marketable securities not used in operations

- Excess real estate that could be sold or leased separately

- Idle equipment or vehicles no longer supporting current revenue

- Personal or owner-related assets parked on the company balance sheet

For small business owners, practical judgment comes into play. A warehouse used every day is part of operations. A parcel of land the company has held for years with no operating purpose is a different asset with a different buyer pool and often a different valuation method.

Working capital is often the toughest adjustment

Many owners focus on price and overlook working capital until the letter of intent is signed. That is risky.

Most buyers expect a business to be delivered with a normal level of working capital so they can operate it on day one without injecting cash. If receivables, payables, and inventory are below normal at closing, the buyer may reduce the purchase price or require a post-close adjustment.

A simple analogy helps. Selling a business without enough working capital is like selling a truck without enough fuel to leave the lot. The truck still has value, but the buyer will not want to pay full price and then stop immediately to fund basic operation.

The practical move is to calculate what "normal" looks like before going to market. Monthly averages usually tell a better story than a single year-end balance sheet, especially in seasonal businesses. Owners who prepare this analysis early tend to have fewer surprises in diligence and more control over the negotiation.

If your financials are messy or buyer questions are getting more detailed, a quality of earnings report can help separate operating performance from balance-sheet noise.

Buyers pay for a company that can keep running after closing. If cash, liabilities, or side assets change that reality, they will change the price.

That is the practical lesson. The basic formula gets you started. The adjustments determine whether your valuation holds up when a buyer, lender, or diligence team starts testing the details.

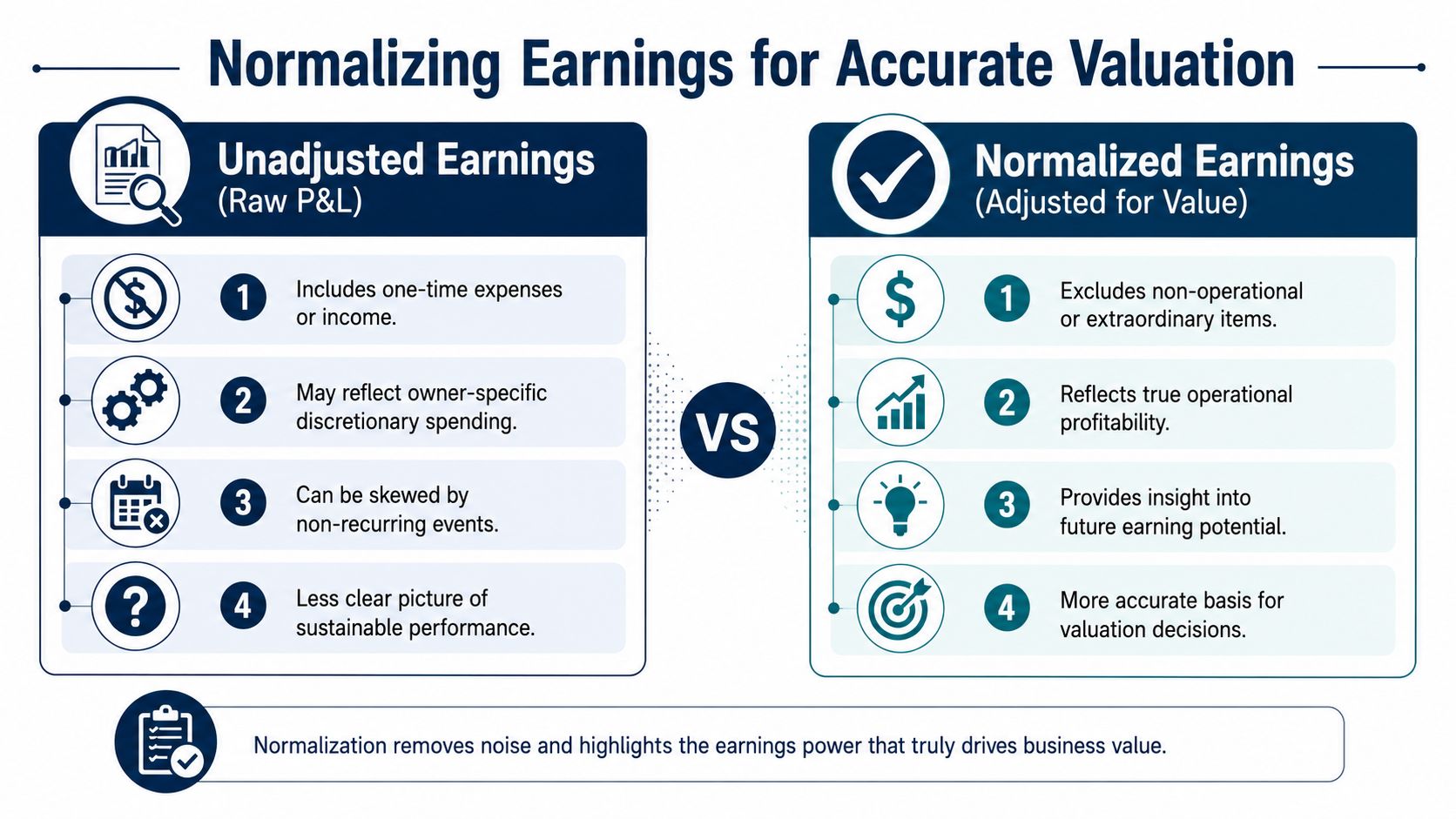

How to Normalize Earnings for an Accurate Value

A common seller mistake looks like this. The owner applies a market multiple to last year's profit, likes the answer, and goes to market. Then buyer diligence starts, half the add-backs get challenged, and the value drops because the earnings number was never clean in the first place.

That is why normalized earnings matter for a privately held business. Buyers are trying to answer a practical question: what will this company earn after the current owner is gone and normal operations continue?

What normalization actually means

Normalization is the process of adjusting your profit and loss statement so it reflects ongoing operating performance, not owner preferences, tax strategy, or unusual events.

For small business owners, this is less about finance theory and more about credibility. A buyer will usually accept a lower number they can trust before they accept a higher number they cannot verify.

EBITDA often becomes the starting point because it strips out interest, taxes, depreciation, and amortization. That makes it easier to compare one business to another. But the key work is in the adjustments below that line and around it.

Where private company earnings usually need cleanup

Small business books are often built to run the company efficiently, reduce taxes, or both. That creates distortions in valuation.

Typical normalization items include:

- Owner pay that is above or below market. If a buyer needs to replace the owner with a GM or operator, compensation has to reflect that real cost.

- Personal or discretionary spending in the business. Cars, travel, meals, cell phones, and family expenses are common examples.

- One-time professional fees. Litigation, transaction prep, restructuring, or unusual consulting projects may not continue after closing.

- Non-recurring revenue or expenses. Insurance proceeds, disaster cleanup, relocation costs, and other unusual events can distort one year of results.

- Related-party arrangements. Rent, management fees, or services provided by a family entity may need to be reset to market terms.

One clean rule helps. If the expense or income item is likely to continue under a new owner, it usually stays.

The trade-off owners need to understand

Aggressive add-backs can make the headline valuation look better. They also create friction in diligence.

I have seen owners lose bargaining power by pushing adjustments that were technically possible but poorly supported. A buyer sees that and starts questioning everything else in the file. On the other hand, a disciplined normalization schedule with invoices, payroll records, and a short explanation for each adjustment usually speeds the process up and protects value.

That trade-off matters more than many owners expect. In private company sales, buyers are not just buying earnings. They are buying confidence in those earnings.

A simple way to judge an add-back

Use this test: Would a reasonable buyer have to spend this money again after closing?

If the answer is yes, it is probably not a valid add-back.

If the answer is no, document why, tie it to the general ledger, and show the amount clearly. The strongest schedules are boring in a good way. They are easy to follow, easy to prove, and hard to argue with.

| Earnings view | What it includes | What it tells a buyer |

|---|---|---|

| Unadjusted earnings | Owner-specific spending, unusual costs, mixed classifications | "I still need to figure out what this business really earns." |

| Normalized earnings | Recurring operations, supportable add-backs, market-based adjustments | "I can underwrite this and move faster." |

What works in practice

Start with the last three years, then review monthly detail, not just annual totals. Seasonal swings, owner bonuses, and one-time events are easier to spot that way.

Next, build an add-back schedule with backup for every line. Keep each adjustment specific. "Excess owner auto expense" is stronger than "miscellaneous discretionary costs."

If your records are complicated or buyer questions are getting sharper, review how a quality of earnings report tests earnings adjustments. That process shows why some add-backs survive buyer review and others get cut late in the deal.

Large public-company stories can make valuation sound abstract. That is one reason owners get distracted by headline numbers in articles about understanding Anthropic's IPO. In a small business sale, the practical issue is simpler. The cleaner and more believable your earnings, the more defensible your value.

Applying Valuation Multiples and Industry Context

You clean up the books, normalize earnings, and then hear three different valuation ranges from three different buyers. That is the moment many owners realize the multiple is not a fixed rule. It is a judgment about risk.

For a private company, that judgment often matters as much as the math.

Why one multiple doesn't fit every business

A multiple is a shortcut buyers use to price your future earnings power. If a buyer says five times EBITDA, they are saying those earnings are valuable enough, durable enough, and transferable enough to pay that price today.

The key word is transferable.

Two companies can post similar earnings and still get very different multiples. A software business with recurring subscriptions, low churn, and a management team that runs the operation without the founder will usually trade differently from a construction company that rebids work every season and depends on the owner's relationships to win jobs. Both may be healthy businesses. One gives a buyer more confidence that earnings will continue after the sale.

Industry context matters, but your business model matters more

Industry averages are a starting point, not a conclusion.

Owners often hear that "companies in my industry sell for X times earnings" and treat that number like a market price. Buyers do not. They look at the version of the industry you built.

A consulting firm with retainer revenue, documented processes, and several rainmakers is easier to underwrite than a consulting firm where the owner closes every deal and one client represents too much of total revenue. Both sit in the same category. They do not carry the same risk.

Buyers usually pressure-test a few recurring questions:

- How predictable is revenue? Contracted or repeat business usually supports a stronger valuation discussion than one-off project work.

- How concentrated is the customer base? Heavy reliance on a handful of clients can pull the multiple down fast.

- How dependent is the company on the owner? If the owner is the brand, lead seller, and technical expert, transfer risk goes up.

- How steady are margins? Consistent performance is easier to trust than a business with sharp swings.

- How credible is the growth path? Buyers pay more comfortably when they can see how growth happens after closing.

Use public-company headlines carefully

Public markets can help you understand how investors think about growth, risk, and business quality. They are less useful as direct valuation evidence for a small private company.

That is why broad market stories need context. Reading about understanding Anthropic's IPO can be useful if you want to see how investors price narrative, scale, and future expectations. It will not tell you what a buyer should pay for a privately held services firm, distributor, or local manufacturer.

Private company valuation is narrower and more practical. Size matters. Deal structure matters. Revenue quality matters. The buyer asking whether your top customer will stay after a change in ownership is not using the same lens as a public market investor chasing future category dominance.

Where owners should do their homework

Start with comparable businesses that look like yours in the ways a buyer cares about. Similar size. Similar margins. Similar customer mix. Similar dependence on the owner. Similar level of recurring revenue.

That is why a broad industry label is rarely enough.

A useful reference point is this guide to business valuation multiples by industry for private companies. Use it to frame the conversation and test whether your expectations are realistic. Do not use it as a shortcut to claim a number your business has not earned.

The practical takeaway is simple. Owners get higher multiples by reducing buyer risk before the sale process starts. Cleaner revenue, lower concentration, stronger management depth, and better reporting usually do more for value than arguing over half a turn of EBITDA in the final meeting.

Your Checklist to Increase Enterprise Value

Most owners can't change their enterprise value overnight. They can improve the drivers behind it over time.

That is good news. It means value creation is not random. It comes from a set of decisions that make the business easier to understand, easier to run, and easier to buy.

The practical owner checklist

Clean up financial reporting. Monthly close discipline matters. Buyers trust numbers that tie out, reconcile, and tell the same story across the P and L, balance sheet, and tax returns.

Reduce unnecessary debt. If debt doesn't directly support productive growth, it can drag on value and reduce flexibility in a sale process.

Separate business and personal spending. This helps with normalized earnings and removes doubt during diligence.

Protect working capital. Know what the business needs to operate normally. That keeps you from being surprised in closing negotiations.

Build recurring revenue where you can. Service agreements, retainers, maintenance plans, and repeatable contracts make earnings easier to underwrite.

Lower customer concentration. A business that can survive the loss of one client is safer in a buyer's eyes.

Document the way work gets done. SOPs, pricing logic, job workflows, CRM discipline, and team accountability all reduce dependence on the owner.

What buyers notice fast

Some value drivers show up quickly in a review:

| Buyer sees | Buyer thinks |

|---|---|

| Clean books and consistent reporting | "This owner runs a disciplined business." |

| Heavy owner dependence | "Transition risk is high." |

| Repeatable contracts and stable clients | "Cash flow looks more durable." |

| Mixed expenses and unclear adjustments | "I need to discount for uncertainty." |

Focus on transferability

The best growth move isn't always the one that adds the most sales next quarter. Sometimes it's the move that makes the company more transferable.

That could mean training a second layer of managers. It could mean locking in stronger client contracts. It could mean getting job costing right so margins are visible by service line. Those aren't glamorous projects, but they often matter more than owners expect when a buyer starts asking hard questions.

The point of enterprise value calculation isn't to produce one magic number. It's to show you which levers deserve your attention now, while you still have time to improve them.

If you want help turning messy books, unclear margins, and owner-dependent operations into a business that's easier to value and easier to sell, MyOfficeOps can help. Their team supports small and midsize businesses with bookkeeping, reporting, CFO-level guidance, and exit planning so you can improve financial clarity now and build a stronger enterprise value over time.