It’s a tough spot to be in. You need cash, and your 401(k) balance is staring you in the face. But everyone knows the big rule: touch that money before age 59½ and the IRS hits you with a painful 10% penalty.

But what if you didn’t have to pay it? Think of 401(k) withdrawal exceptions as special passes the IRS hands out for certain life events. These passes let you take out your own savings without that extra 10% hit.

The Big Difference Between Penalties and Taxes

Before we start, let's clear up the most confusing part. Getting an exception only saves you from the 10% early withdrawal penalty. It does not get you out of paying your regular income tax.

Think of it like this:

- The 10% penalty is an extra fee for breaking the age rule.

- The income tax is what you were always going to owe when you took money out of your traditional 401(k).

Key Takeaway: Avoiding the penalty is great, but the money you pull out will still be added to your income for the year and taxed like a paycheck.

Understanding the Basics of 401(k) Withdrawals

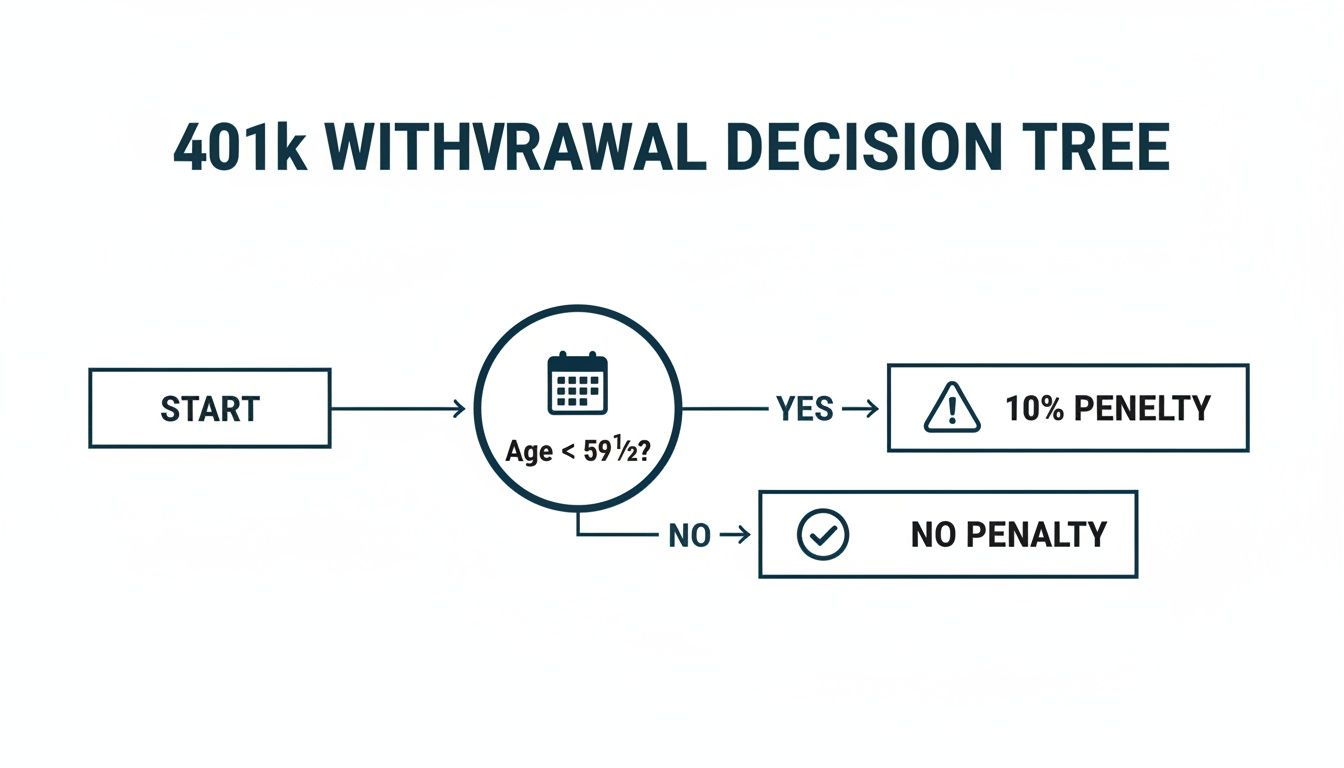

Your 401(k) is built for retirement. That’s why the government made rules to help you leave that money alone until you're older. The magic age is 59½. Once you hit that birthday, you can take money out for any reason, and you'll only pay income tax on it.

Before that age, though, the IRS adds the 10% penalty on top of the income tax. This simple picture shows the basic rule.

As you can see, taking money out early usually leads to a penalty. That’s why finding an exception is so important. The good news is, there are more than a dozen situations where you might get a pass.

Here's a quick look at common reasons the 10% penalty might not apply. Remember, you'll still owe regular income tax in most cases.

| Reason for Withdrawal | Condition to Avoid 10% Penalty | Is It Still Taxable as Income? |

|---|---|---|

| Separation from Service | You leave your job in or after the year you turn 55. | Yes |

| Total & Permanent Disability | A doctor says you are unable to work. | Yes |

| Medical Expenses | The costs are more than 7.5% of your yearly income. | Yes |

| QDRO (Divorce) | A court order gives part of it to your ex-spouse. | No, if rolled over. Yes, if taken as cash. |

| Death of Participant | Your beneficiary inherits the 401(k) funds. | Yes |

| IRS Levy | The IRS takes funds to pay your federal tax debt. | Yes |

This table just gives you an idea of the kinds of major life events the IRS makes allowances for.

What Situations Qualify for an Exception?

The IRS knows that life doesn’t always go as planned. You might lose your job, face a huge medical bill, or need to split up money in a divorce. Because of this, they've made a list of exceptions.

These cover a wide range of situations, including:

- You become totally and permanently disabled

- You have medical bills that are more than 7.5% of your income for the year

- You leave your job in or after the year you turn 55

- A court orders you to share the money in a divorce (this is called a QDRO)

- You have or adopt a child (up to $5,000)

It's also important to know about new laws. For instance, the SECURE Act 2.0 recently added new exceptions and changed some old ones. These rules are there to help you through tough times without making things worse.

For business owners, understanding these rules is a key part of financial planning for business owners, both for yourself and for your team.

Common Exceptions for Job Loss and Medical Bills

Some of the most common reasons people need their 401(k) early are because of big, unexpected life changes. Losing a job or getting overwhelming medical bills are two of the biggest. The IRS has specific rules that can help you avoid that painful 10% penalty in these situations.

Let's look at what qualifies when your career or health takes a turn.

The Rule of 55 for Job Loss

Losing your job is stressful enough. Thankfully, the IRS made a rule that can help, often called the “Rule of 55.” It's pretty simple.

If you leave your job—whether you quit, get laid off, or retire—during or after the calendar year you turn 55, you can take penalty-free withdrawals from that company's 401(k).

For example, say your birthday is in October. If you turn 55 this year and leave your job next March, you've met the age rule. You could start taking money from that 401(k) without the 10% penalty.

Important Note: This is a key detail. The exception only applies to the 401(k) of the company you just left. If you have money in an old 401(k) from a past job or in an IRA, this rule doesn’t help you.

When You Are Totally and Permanently Disabled

Another big exception is for a total and permanent disability. This isn't for a short-term injury; it’s for when a condition leaves you unable to do any kind of paid work.

To qualify, you'll need to give proof to your 401(k) company. This usually means getting a doctor to sign a form saying your condition is expected to be long-lasting or even life-threatening. If you meet this strict definition, you can take money from your 401(k) without the 10% penalty, no matter how old you are.

Paying for Large Medical Bills

Big medical bills can wreck anyone's budget. The IRS gets this and lets you take a penalty-free withdrawal to cover them, but there's a catch.

You can only withdraw the amount that is more than 7.5% of your adjusted gross income (AGI) for the year. Your AGI is your total income minus some deductions, and you can find it on your tax return.

Let’s see a real example:

- Sarah's Income: Sarah has an AGI of $80,000.

- Her Threshold: 7.5% of her AGI is $6,000 ($80,000 x 0.075). She has to cover this amount herself before the exception helps.

- Her Bill: She has a $15,000 medical bill that insurance didn't pay for.

- The Math: She can withdraw the amount over her $6,000 threshold. So, $15,000 (total bill) – $6,000 (her part) = $9,000.

- The Result: Sarah can take $9,000 out of her 401(k) without the 10% penalty. She will still owe regular income tax on that $9,000.

Dividing Assets in a Divorce (QDRO)

Divorce often means splitting up everything, including retirement accounts. To divide a 401(k) without causing taxes and penalties, you need a special court order called a Qualified Domestic Relations Order, or QDRO.

A QDRO is a legal paper that tells the 401(k) company how to split the account between the employee and their ex-spouse.

When the money is paid to the ex-spouse under a QDRO, they can take it as cash without the 10% penalty. They will still owe income tax on it.

Or, the ex-spouse can do something smarter: they can roll the money directly into their own IRA or another retirement plan. This move avoids both the penalty and the immediate income tax, saving the money for their own retirement.

Navigating Hardship Withdrawals and Emergencies

Life happens. Sometimes it throws you a real curveball. The IRS gets this and created a special category for true emergencies, called a hardship withdrawal. This isn't for a tight month or a vacation; it’s for what the IRS calls an “immediate and heavy financial need.”

Think of it as a last-resort safety net. These rules can help you handle a crisis without the extra sting of the 10% penalty. But there's a catch: your employer's 401(k) plan must allow hardship withdrawals—and not all of them do.

What Counts as a True Hardship

The IRS has a clear list of situations that it considers an "immediate and heavy" financial need. To keep things simple, most 401(k) plans follow this list. If your plan allows it, you may be able to take a hardship withdrawal for one of these reasons:

- Medical Care: Paying for medical bills for yourself or your family that insurance won't cover.

- Buying a Home: Covering costs to buy your main home. This doesn't include making mortgage payments.

- Education Costs: Paying tuition and fees for the next 12 months of college for you, your spouse, or your kids.

- Preventing Eviction or Foreclosure: Making payments to stop you from being kicked out of your rental or losing your main home.

- Funeral Expenses: Paying for the funeral of a close family member.

- Home Repairs: Paying to fix damage to your main home, like after a storm.

Before you can take a hardship withdrawal, you usually have to confirm you don't have other money available. This means you’ve already checked your savings or tried to get a loan.

Tapping retirement funds for emergencies is becoming more common. One friend of mine had to do this last year when his furnace died in the middle of winter and he didn't have the cash to replace it. It wasn't ideal, but it kept his family warm. You can read more about the dramatic rise in 401(k) hardship withdrawals and what it means for long-term savings.

The SECURE 2.0 Act Added New Protections

Recent law changes, like the SECURE 2.0 Act, have added a few more important exceptions for difficult personal situations. These are a huge help for people facing crises that weren't covered before.

Key Update: The SECURE 2.0 Act added new, penalty-free withdrawal options for people diagnosed with a terminal illness and for victims of domestic abuse. This provides a financial lifeline in very bad situations.

Let’s look at how these newer exceptions work.

Withdrawals for Terminal Illness

If a doctor diagnoses you with a terminal illness, you can now get your 401(k) funds without the 10% penalty. A doctor must certify that your illness is expected to result in death within 84 months (that’s 7 years).

This is a big deal. It lets someone facing a life-limiting diagnosis use their own money to pay for care or get their affairs in order without an extra penalty.

Withdrawals for Domestic Abuse Victims

Another new exception is for survivors of domestic abuse. If you have been abused by a spouse or partner, you can now withdraw a certain amount penalty-free.

Here’s what you need to know:

- Withdrawal Limit: You can take out the lesser of $10,000 or 50% of your 401(k) balance.

- Timeframe: You have to make the withdrawal within one year of when the abuse happened.

- No Proof Needed: You don't have to provide proof of the abuse to your 401(k) company. You just have to self-certify that you qualify.

This is a major change designed to help survivors get money quickly to escape a dangerous situation or find new housing.

Life is full of big moments—some happy, some very hard—and they almost always cost money. The IRS understands that when you're welcoming a new baby or cleaning up after a natural disaster, the last thing you need is a 10% penalty.

That’s why they’ve built several 401(k) withdrawal exceptions for these exact moments. Think of it as a financial relief valve, letting you access your own savings when you truly need it most.

Let's walk through how your retirement funds can help during some of life's biggest events.

Welcoming a New Child to Your Family

Having a baby or adopting a child is wonderful, but the costs can be huge. From hospital bills to setting up a nursery, the expenses add up. To help new parents, there’s a specific penalty-free withdrawal option.

You can take out up to $5,000 from your 401(k) for each qualified birth or adoption. This isn't a loan; it's money to help you cover costs for your new family member.

Here’s a real-world example:

- The Limit: My friends just had a baby. The $5,000 limit is per person, per child. Since both of them have a 401(k), they could each withdraw $5,000 for a total of $10,000.

- The Deadline: You have one year from the date of birth or the date the adoption is final to take the money out.

- The Catch: Remember, this only avoids the 10% penalty. The money is still taxed as regular income, so you will owe income tax on it.

This is just one of more than a dozen exceptions the IRS allows. Recent rules have expanded this list, including up to $22,000 for disaster recovery and even a new rule for domestic abuse survivors to withdraw up to $10,000. You can see the full list in the IRS guidelines on early distribution exceptions.

Getting Relief After a Natural Disaster

When a hurricane or wildfire hits your community, money penalties are the last thing on your mind. If you live in a federally declared disaster area, you might be able to take a “qualified disaster distribution” from your 401(k).

This exception lets you withdraw a large amount to help you get back on your feet. For recent major disasters, this limit has been as high as $22,000.

This money can cover almost any financial loss you’ve had from the disaster, from rebuilding your home to replacing your car. A cool feature here is that you can choose to spread the income tax hit over three years, which makes the tax bill much easier to handle.

When Military Reservists Are Called to Duty

If you're a military reservist, getting called to active duty can put a sudden strain on your family’s finances. To help with that, the IRS created an exception for qualified reservist distributions.

This rule allows you to take penalty-free withdrawals from your 401(k) or IRA if you are called to active duty for more than 179 days.

This isn't for just any expense; it's meant to help replace lost income while you are deployed. It’s a small way of recognizing the financial sacrifice military families make. Even better, once your active duty ends, you usually have two years to repay the funds to your retirement account. If you do, you can avoid paying income tax on the withdrawal.

How to Actually Take a Withdrawal The Right Way

Knowing you might qualify for a 401(k) withdrawal exception is one thing. Actually getting the money is another. It’s a process with paperwork, specific rules, and some big decisions.

So, let's walk through the real-world steps. This isn’t about calling the IRS; it’s about working with the people who manage your company’s retirement plan.

Your First Step: Contact Your Plan Administrator

Your first call shouldn't be to your boss, but to your 401(k) plan administrator. This is the financial company—like Fidelity, Vanguard, or Charles Schwab—that holds the money for your employer.

If you don't know who it is, your HR department can tell you. The administrator has the forms you'll need and knows the exact rules for your company's plan. Remember, while the IRS sets the main rules, every 401(k) plan is a little different.

Get Your Paperwork in Order

The plan administrator needs proof that you qualify for an exception. They won't just take your word for it. Think of it like applying for a loan; the more organized your papers are, the faster it will go.

Depending on why you need the money, you'll need to gather specific documents.

- Medical Bills: You'll need itemized bills from your doctor or hospital showing what your insurance didn't cover.

- Court Orders: If it's for a divorce, you absolutely need a signed Qualified Domestic Relations Order (QDRO).

- Eviction Notices: To stop an eviction, you’ll need the official, dated letters from your landlord.

- Home Purchase Agreement: For a down payment, you'll need the signed contract for your new home.

Once you submit your application and papers, the administrator reviews everything. They have the final say on whether your request is approved, based on both IRS rules and your company's plan rules.

You might have to decide whether to take a loan from your 401(k) or a permanent withdrawal. These are two very different choices with big financial results.

The Big Decision: 401(k) Loan vs. Withdrawal

Think of a 401(k) loan as borrowing from your future self. You take money out now, but you have to pay it back into your own account, usually with interest. A withdrawal, on the other hand, is permanent. That money is gone from your retirement savings for good.

If your plan allows loans, it’s often the smarter first choice. Here’s why:

- No Taxes or Penalties: Because you're paying it back, a loan isn't taxed. You won't owe income tax or the 10% penalty.

- You Pay Yourself Back: The interest you pay on the loan goes right back into your own 401(k) account.

- Your Money Stays Invested: The rest of your 401(k) stays in the market, continuing to grow for your retirement.

But loans come with a big risk. If you leave your job, you may have to repay the entire loan balance very quickly, sometimes right away. If you can’t, the rest of the loan is treated as a taxable withdrawal, hitting you with both income tax and the 10% penalty. Understanding these details is a key part of our guide on how to prepare for tax season.

Permanently cashing out retirement money is a huge issue. A shocking amount of this happens when people change jobs, not for real emergencies. Before you pull the trigger, make sure you explore every other option, like understanding what to do with your 401k after leaving a job, to avoid a costly mistake. You can find more details in this analysis of retirement account leakage from EBRI.

Common Questions About 401k Withdrawals

Even when you think you have the rules straight, taking money from your 401(k) can be scary. It’s a big financial move, and it's normal to have lots of questions.

To help you out, we’ve answered some of the most common questions we hear about 401(k) withdrawal exceptions.

If I Qualify for an Exception, Do I Still Pay Taxes?

Yes. This is the most important thing to remember. An exception only saves you from the 10% early withdrawal penalty. That’s it.

The money you take out is still considered income by the IRS. That means you will owe federal income tax on the full amount, and probably state income tax too.

For example, if you're in the 22% federal tax bracket and take a $10,000 withdrawal, you’ll still owe $2,200 in federal taxes. Your 401(k) company will likely withhold 20% for federal taxes right away, but you might owe more or less depending on your total income for the year.

What Is the Difference Between a Hardship Withdrawal and a Loan?

Think of it this way: a 401(k) loan is borrowing from yourself, while a hardship withdrawal is taking money out for good.

Here’s a quick breakdown:

- A 401(k) Loan: You borrow from your own account and must pay it back with interest. As long as you repay it, you won’t owe any taxes or penalties. It's a temporary fix.

- A Hardship Withdrawal: This is permanent. You take the money out, and you don’t pay it back. You will definitely owe income taxes on the entire amount.

A loan is almost always the better first choice because it keeps your retirement savings intact. The biggest risk with a loan is if you leave your job—you might have to repay the whole thing right away. If you can't, it becomes a taxable withdrawal.

Key Insight: A loan keeps your retirement plan on track, but a withdrawal permanently shrinks your nest egg. Always consider a loan first if your plan allows it.

How Do I Prove I Need a Hardship Withdrawal?

You can’t just tell your 401(k) provider you’re having a hard time; you have to prove it with paperwork. The IRS requires you to show proof of an "immediate and heavy financial need."

So, what kind of proof do you need?

- Copies of medical bills for you or your family

- An official eviction notice from your landlord

- Foreclosure letters from your bank

- Tuition bills for college

- A signed contract to buy your main home

You'll also likely have to sign a paper saying you don't have any other money to cover the cost. Your plan administrator looks at everything and has the final say.

Can My Employer Stop Me From Taking a Withdrawal?

Yes, they can. This surprises a lot of people. Just because the IRS allows an exception, it doesn't mean your company’s 401(k) plan has to offer it.

For example, a plan might allow hardship withdrawals for medical bills but not for buying a first home. Or it might not allow withdrawals for having a baby. The specific rules for your account are in a document called the Summary Plan Description (SPD).

You have the right to ask your 401(k) provider for a copy of the SPD. This document is your rulebook. It will tell you exactly which types of withdrawals your plan allows and what steps to take. As a small business owner, it’s important to know the details in your own plan, not just for yourself but for guiding your employees. These details are part of a larger financial picture, which you can explore further in our guide on the essential list of small business tax deductions.

Navigating your business's finances—from payroll and bookkeeping to making smart decisions about benefits like a 401(k) plan—can be a lot to handle. At MyOfficeOps, we provide the financial clarity and expert guidance you need to not only manage your daily operations but also build long-term value. Schedule a discovery call with our team today to learn how we can help you grow your business with confidence.