Is the interest you pay on business loans tax deductible? The short answer is yes, almost always. But, like everything with the IRS, it’s not quite that simple. If you borrow money to run your business, you can usually subtract the interest you pay from your income. This lowers your taxable income and, in the end, your tax bill.

Getting this right is a key part of managing your company's money, so let's break down what this means for you.

What Is Deductible Interest Anyway?

Think of interest as the fee you pay for “renting” money. When you take out a loan, you’re not just paying back the amount you borrowed; you're also paying a fee for the privilege of using those funds.

The good news is that the government sees this fee as a normal cost of doing business. Because of that, they let you subtract most types of business interest from your income before you calculate your tax bill. That subtraction is called a tax deduction, and it’s one of the best tools you have for reducing what you owe.

Why does the IRS allow this? It’s to encourage people to start and grow businesses. The government wants business owners like you to invest, expand, and hire people—all things that help the economy. Making interest deductible lowers the cost of borrowing, making it easier for you to fund those big moves.

Why This Matters for Your Business

Knowing which interest payments you can deduct isn't just for your accountant. It directly impacts your company’s cash flow. Every dollar of interest you can legally deduct is a dollar that stays in your business, ready to be used for something else.

Imagine you own a small construction company and take out a loan for a new excavator. The interest you pay on that loan is a business expense. Deducting it means you pay less in taxes, which frees up cash you can use for other things, like paying your employees or starting a marketing campaign.

The main idea is that the cost of borrowing money to make money is a business expense. As long as the loan is for a clear business purpose, the interest is usually deductible.

What Is a Business Purpose?

This brings us to the most important rule: the loan must be for ordinary and necessary business activities. The IRS needs to see a clear link connecting the borrowed money to your business.

Here's a quick look at the kinds of interest your business might pay and if you can typically deduct them.

Common Types of Business Interest

| Type of Interest | Common Use Case | Generally Deductible for Business? |

|---|---|---|

| Business Loan | Funding operations, buying equipment, expansion projects. | Yes, as long as the loan is from a real lender and you're legally responsible for the debt. |

| Credit Card Interest | Paying for everyday business expenses like supplies, software, or travel. | Yes, but only for the part related to business purchases. This is why you must keep business and personal spending separate. |

| Mortgage Interest | Purchasing commercial property like an office, warehouse, or storefront. | Yes, interest on a mortgage for property used in your business is deductible. |

| Vehicle Loan Interest | Financing a car, truck, or van used for business activities. | Yes, based on the percentage of business use. If the vehicle is used 50% for business, you can only deduct 50% of the interest. |

| Line of Credit | Managing short-term cash flow gaps, covering payroll, or buying inventory. | Yes, the interest paid on funds you draw from the line of credit for business use is deductible. |

The key takeaway is that you must be able to prove the money was used for your business, not for personal things like a family vacation or a down payment on your personal home. This is where good bookkeeping becomes your best friend—it creates the paper trail you need to back up your deductions.

We’ll dig into the different types of interest and how to handle them later, but you can also explore our complete guide to small business tax deductions for a bigger-picture view.

The Main Types of Interest You Can Deduct

Once you know that deducting interest is possible, the next question is, "Which interest counts?" When you look at your company’s books, you’ll see interest popping up in a few different places. The IRS has different rules for each, so telling them apart is the first step to getting every deduction you're allowed.

Think of it like sorting tools in a workshop. You have wrenches, screwdrivers, and saws—they all help you build something, but you can't use a saw to turn a bolt. You have to use the right tool for the job. The same goes for interest deductions.

Let's break down the most common types of interest you'll see.

Business Loans for Equipment and Operations

This is the most common type for most business owners. When you take out a loan to buy something for your business—like a new server for your IT firm or a delivery van for your catering company—the interest on that loan is a business expense.

This also covers loans you take out just to run the business day-to-day. Maybe you needed a line of credit to cover payroll during a slow month or a loan to fund a marketing campaign. As long as the money was used for ordinary and necessary business activities, the interest you pay is usually 100% deductible.

For example, I know a contractor who took out a $75,000 loan to buy a new excavator. The interest he pays on that loan is a clear business deduction because that machine is critical for his company to make money.

Real Estate and Mortgage Interest

Many businesses eventually decide to buy their own property instead of renting. If your medical practice bought its own clinic or your manufacturing company owns its warehouse, you’re likely paying a commercial mortgage.

The interest on that mortgage is a big deduction. For any business with a physical location, this lowers the cost of owning your commercial property.

Just like with any other loan, the deduction depends on business use. If you own a mixed-use building where you live upstairs and run your shop downstairs, you can only deduct the part of the mortgage interest that matches the space used for the business.

Business Credit Card Interest

It's very common to use a business credit card for everyday expenses. Software, office supplies, client lunches, travel—these cards are a simple way to manage cash flow. The good news is the interest that adds up on your business card balance is also deductible.

But this is where things can get messy. It is very important that you do not mix personal and business expenses on the same card. If you charge a family dinner and a new office printer to the same card, you can only deduct the interest connected to the printer. Trying to separate that later is a headache. This is why having a separate business credit card isn't just a good idea; it's a must.

Vehicle Loan Interest

Whether it's one car for a consultant or a whole fleet for a construction company, vehicles are essential for many businesses. The interest on a loan for a business vehicle is deductible, but there’s a catch: you can only deduct the part that reflects business use.

- 100% Business Use: If a work truck is used only for job sites and never for personal errands, you can deduct 100% of the loan interest.

- Mixed Use: If you use your personal car for business trips 60% of the time, you can only deduct 60% of the interest you paid on your car loan for that year.

This is where keeping good records is mandatory. You’ll need a detailed mileage log to prove that business-use percentage to the IRS. It's a small habit that protects a valuable deduction.

Understanding the Business Interest Limitation

Alright, let's get into a slightly more complicated topic. Don't worry, I'll keep it simple and focus on what this means for your business.

The government has a rule, officially called Section 163(j), that puts a cap on how much interest bigger businesses can deduct. Think of it as a speed limit on your deductions. Once your business gets big enough, you can’t just write off every single dollar of interest you pay.

Now, this rule is really aimed at larger companies, and we’ll cover how most small businesses don't have to worry about it in the next section. But it's smart to know how it works, especially if your business is growing fast.

What Is the Interest Limitation Rule?

For businesses that fall under this rule, the amount of business interest expense they can deduct is generally limited to 30% of their adjusted taxable income (ATI), plus their business interest income.

So, what is “adjusted taxable income”? It’s a special formula for figuring out your business's profit for just this one rule. To get to ATI, the IRS asks you to add certain expenses—like depreciation—back into your income.

The way ATI is figured out has a huge impact on your deduction. A higher ATI means you can deduct more interest, which is what you want.

How Is Adjusted Taxable Income (ATI) Calculated?

This is where things got a little confusing for a few years because the formula changed. Let’s look at the two versions.

EBITDA-Based Calculation: This is the better formula for businesses. EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. Using this method, you get to add back your depreciation and amortization expenses to your income. This makes your ATI higher, which raises your deduction limit.

EBIT-Based Calculation: This is the stricter formula. EBIT stands for Earnings Before Interest and Taxes. With this method, you can't add back depreciation and amortization. This leads to a lower ATI and a lower limit on your interest deduction.

For a few years, businesses were stuck with the stricter EBIT formula. It was tough on companies with a lot of equipment or buildings, like manufacturers or doctors' offices, because their large depreciation expenses couldn't be used to increase their deduction limit.

A Big Upcoming Change That Helps Businesses

Here’s the good news. A recent law is bringing a major positive change. Starting in 2026, the rule will go back to the more generous 30% of EBITDA calculation.

This is a big deal. The experts at Grant Thornton estimate this change could unlock $500 billion in deductions for U.S. firms by 2030. For a growing business—say, a local healthcare clinic looking to finance new facilities—this change means much better cash flow.

What This Means for You: Starting in 2026, the "speed limit" on your interest deduction will be based on a higher number. This gives businesses more room to deduct the interest they pay on loans for equipment, property, and growth.

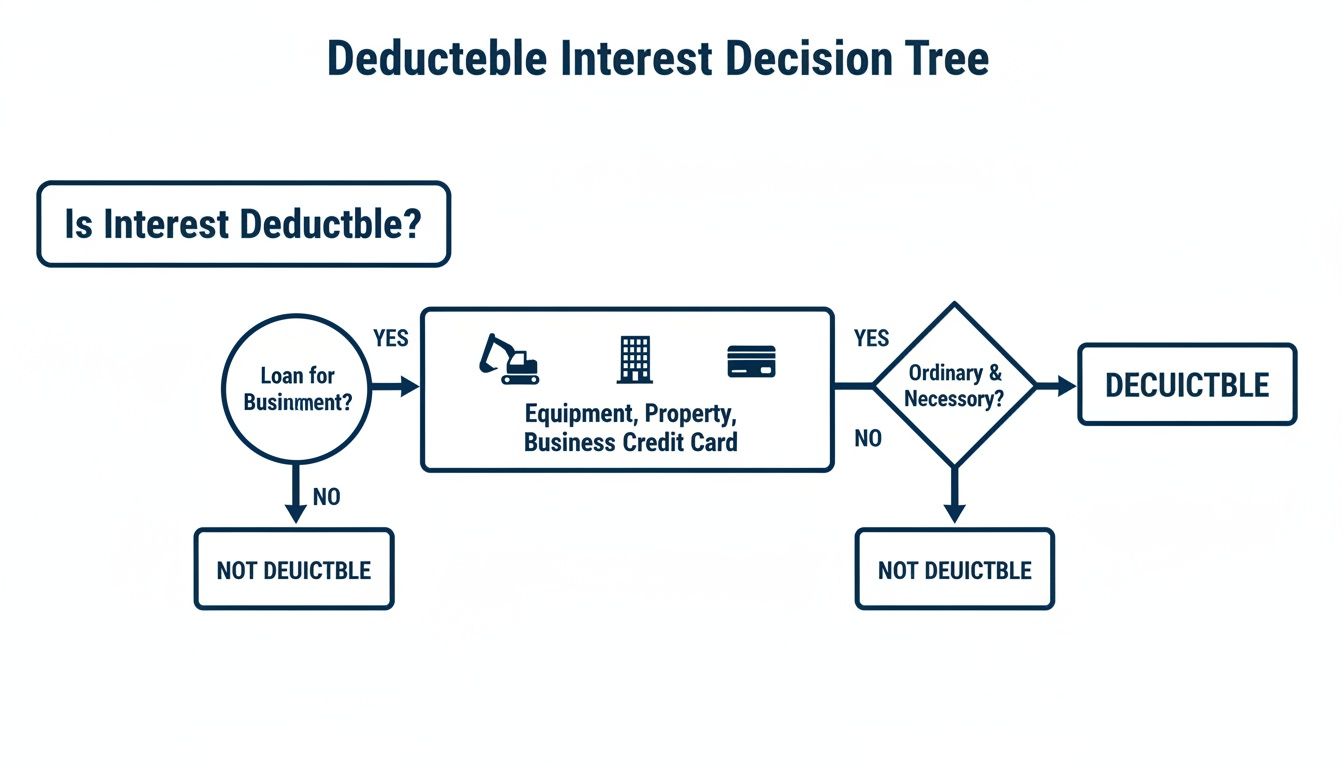

This decision tree gives you a simple visual for how to think through whether an interest expense is deductible.

As you can see, the main idea is simple. If you took out a loan for a clear business purpose—to buy equipment, property, or even use a company credit card—the interest is usually a valid expense.

The key takeaway is that even with these rules, the main point holds true. The question isn't usually if you can deduct your business interest, but simply how much you can deduct in a given year.

How Small Businesses Can Avoid the Interest Limit

That 30% interest limit we just covered can sound scary. But I've got good news: most small and mid-sized businesses I work with never have to worry about it.

The IRS created something called the small business exemption for this exact reason—to take this burden off your plate. If your business qualifies, you can usually ignore the 30% limit and deduct all of your normal and necessary business interest.

This is a huge benefit for the companies we see every day, from local contractors to medical practices. Let’s walk through how to know if you qualify.

Checking If You Qualify for the Exemption

To qualify for this exemption, your business must have average annual gross receipts below a certain dollar amount. Think of "gross receipts" as your total sales for the year, before you subtract any expenses. It's your top-line revenue number.

The IRS adjusts this number for inflation each year. For the 2023 tax year, that number was $29 million. If your average annual gross receipts for the three prior tax years are below this amount, you are likely exempt from the interest limitation.

It’s a simple calculation:

- Add up your total gross receipts for the last three tax years.

- Divide that total by three.

- If the result is less than the annual limit, you qualify.

And if you have a newer business that hasn't been around for three years? You just average the years you've been in business. It’s a simple test designed to help most business owners avoid a complex tax headache.

This exemption is a clear signal from the government that they don't want to get in the way of small business growth. The goal of the 30% limit is to control certain actions at huge corporations, not to penalize a local contractor for buying a new truck.

Special Exceptions for Certain Industries

On top of the general small business exemption, the tax code also allows a couple of key industries to opt out of the rule. These are typically businesses that have to spend a ton of money on physical things just to open their doors.

The two main industries with these special choices are:

- Real Property Trades or Businesses: This includes companies in real estate development, construction, management, or sales. If they choose to opt out of the interest limit, there's a big string attached: they must use a different, less helpful depreciation method for their properties. It's a big trade-off to consider.

- Farming Businesses: Like real estate, some farming businesses can also choose to opt out. They face a similar trade-off, requiring them to use a specific depreciation system for certain farm assets.

For most companies I work with, the gross receipts test is the cleanest and simplest way to avoid the limit. These industry-specific choices involve much more complex tax planning and should be discussed with a financial advisor. You need to run the numbers to see if the trade-offs make sense for your situation.

Navigating rules like this is crucial, but it's just one piece of your overall financial strategy. To see how this fits into the bigger picture, check out our complete guide to small business tax deductions.

Good Records Are Your Key to Tax Savings

After all the talk about rules and limits, everything comes down to one simple truth: you can only deduct what you can prove. Knowing all about interest deductions is worthless if you don't have the paperwork to back it up.

Think of it this way. If an IRS agent questions a deduction, you can't just say, "Oh yeah, that was for the business." You need to show them the proof. Your financial records are the evidence that turns a potential deduction into real tax savings.

This is where so many business owners stumble. It's not because they’re dishonest. It's because the daily work takes over, and bookkeeping gets pushed to the bottom of the to-do list. But clean, organized books aren't just 'good practice'—they are the only way to guarantee you get every single dollar you're owed for the tax deductibility of interest.

The High Cost of Messy Books

Let me give you a real-world example. I’ve seen business owners who use a single checking account for everything. They pay for a new laptop, software, and client dinners. But they also pay their personal car loan and buy groceries from that same account.

At tax time, this creates a huge mess. Untangling the business interest from the personal interest becomes nearly impossible. Your accountant will have to spend hours sorting through transactions, and you'll be paying for every minute. Worse, if the records are too jumbled, you could lose the deduction entirely or, even worse, trigger an IRS audit.

Good bookkeeping takes this entire headache off your plate. It creates a clear paper trail that makes tax season feel normal, not scary.

A Simple Checklist for Tracking Interest

Keeping good records doesn't have to be a second job. The secret is doing it consistently. If you track a few key items correctly from the start, you build a solid foundation that makes claiming your interest deductions easy.

Here’s what you absolutely need to keep:

- Loan Agreements: Keep a digital copy of every loan agreement. This is the legal document that proves you owe the debt.

- Loan Statements: Your monthly or quarterly statements are key. They clearly show the principal and interest parts of your payments, which is the main proof of the interest you paid.

- Bank and Credit Card Statements: These statements show the money leaving your business account to pay the loans. They connect the payment to your business.

- Receipts for Purchases: This is crucial for credit card interest. Keep the receipts for the items you bought. This proves the original expense was for a real business purpose.

The goal of great record-keeping is to tell a clear story. The documents should show that a business loan was taken out, payments were made from a business account, and a specific amount of interest was paid.

To get the most out of your deductions, organization is everything. This Tax Season Survival Guide offers great advice to help you get organized and make sure every deductible expense is properly recorded.

Setting Up Your Books for Success

The easiest way to keep your records clean is to set up your accounting system correctly from day one. Trust me, it’s far simpler to build good habits now than to fix a year's worth of bad ones later.

1. Separate Bank Accounts are a Must: Get a dedicated business checking account and at least one business credit card. Never mix personal and business spending. This is the single most important step you can take to protect your deductions.

2. Label Everything Clearly: Inside your accounting software (like QuickBooks), be specific. Don’t just create a generic "Loan Payment" expense. Instead, use accounts like "Interest Expense – Equipment Loan" and "Interest Expense – Vehicle Loan."

3. Check Your Accounts Monthly: At the end of every month, sit down and match your bank statements to the transactions in your accounting software. This 30-minute task can save you from a year-end disaster by catching errors before they get out of hand. For more on this, check out our guide on how to categorize business expenses.

When you follow these simple steps, you're not just doing bookkeeping; you're building a fortress around your deductions. You’ll have the peace of mind that comes from knowing that if the IRS ever comes knocking, you have a perfect, easy-to-read record proving every claim you’ve made about the tax deductibility of interest.

Understanding the rules around interest deductibility is one thing. Actually using them to save your business real money is another. This is where having a partner, not just a bookkeeper, changes everything.

At MyOfficeOps, we don't just talk about rules; we help business owners like you build a real financial plan out of them. We put systems in place that make these complex rules work for you.

From Clean Books to a Clear Plan

It all starts with clean, accurate books. There's no way around it. Our Core Accounting services make sure every interest payment is tracked correctly from day one. We set up your accounts so that interest from an equipment loan is never mixed up with a credit card payment, giving you the solid ground you need for any tax deduction.

This isn't just about organizing data. It’s about building a financial picture of your business that you can trust. When your books are solid, you can be sure you’re capturing every single dollar of interest you can deduct.

Think of it like this: You wouldn't build a house on a shaky foundation. In the same way, you can't build a smart tax strategy on messy books. We make sure your financial foundation is rock-solid.

Turning Tax Rules into Action

Once your day-to-day accounting is running smoothly, we can start looking at the bigger picture. This is where our Profit Optimization services come in. We don't just record what happened last month; we help you map out what's coming next.

For example, we’ll take a look at your company’s loans. We can analyze them and help you see how the business interest limit might—or might not—impact you as you grow.

Let's say you’re a business owner planning to expand your office. Our team can help you look at different financing options. We can show you how taking on a new commercial mortgage will affect your tax bill and cash flow, helping you pick the smartest path forward before you sign any papers.

Or, maybe you’re a contractor who needs to buy a new piece of heavy equipment. We can walk you through the long-term impact of that loan, factoring in both the interest payments and the tax savings you'll get from the deduction.

A Partner for Your Business Growth

Look, our goal isn't just to do your taxes or clean up your books. It's to give you the financial clarity you need to build a stronger, more profitable business. We handle the details on topics like the tax deductibility of interest so you can stay focused on what you do best—running your company.

We believe that good financial management should feel simple for the business owner. That's why we deliver:

- Clear, simple reports that you can actually understand.

- A team that answers when you have a question.

- Proactive advice to help you make smarter decisions about growth, hiring, and profit.

By turning confusing tax rules into a simple, actionable plan, we help you stop losing sleep over taxes and start focusing on your next big opportunity.

Common Questions About Deducting Interest

Even when you have a good handle on the basics, a few specific questions about interest deductions always seem to pop up. We've heard them all from business owners over the years. Let's tackle a few of the most common ones with some simple answers.

Can I Deduct Interest on a Loan from My Parents?

This question comes up all the time. The short answer is yes, you can, but you have to treat it like a real business transaction. You can’t just take cash from a family member and call it a loan.

The IRS needs to see that it’s a real debt. This is a requirement. You must:

- Sign a formal loan agreement. This document needs to state the loan amount, the interest rate, and a repayment schedule.

- Charge a fair interest rate. You can't just pick a number. The rate must be at least the minimum set by the IRS, known as the Applicable Federal Rate (AFR). Using this rate proves it’s a real loan, not a hidden gift.

- Actually make the payments. You need a clear paper trail showing you're making regular principal and interest payments, just like you would to a bank.

If you do all this, the interest you pay is a valid business deduction. If you don't, the IRS will likely call the money a gift and deny your deduction.

What Happens to Interest I Can’t Deduct This Year?

This is a common worry for businesses getting close to the interest limit. The good news is that any business interest you can't deduct in one year isn't lost forever.

The IRS allows you to carry it forward to future tax years. Think of it like rolling over unused cell phone data. You can apply that disallowed interest to reduce your taxable income in a later year when you have more room under the deduction limit. This carryforward can become a valuable asset down the road.

Is the Interest on My Business Credit Card Deductible?

Absolutely. The interest that builds up on your business credit card balance is deductible, as long as the card was used only for legitimate business purchases.

However, this is where so many business owners trip up. If you use your business card for a client lunch and then for your family’s groceries, you can only deduct the interest tied to the business spending. Untangling that mess is a nightmare.

The rule is simple: One card for business, one card for personal. Mixing them is one of the easiest ways to lose out on valuable deductions and create major red flags for the IRS.

Keeping these rules in mind is a big part of getting your finances in order. For more tips, check out our guide on how to prepare for tax season to make the process as smooth as possible.

Feeling overwhelmed by the rules? You don't have to manage it all alone. MyOfficeOps provides the financial clarity you need to stop worrying about compliance and start focusing on growth. We turn confusing regulations into a clear, actionable plan for your business. Get in touch today to see how we can help.