So you’ve hired someone to help out at home—a nanny for the kids, a caregiver for an older parent, or a housekeeper who comes every week. It's a huge help, and you pay them for their time. Seems simple, right?

Well, not exactly. How you pay them and the way you work together matters a lot to the government. Many families think paying in cash or with an app makes it a casual deal. But the IRS sees it more formally, and getting this wrong can cause real headaches down the road.

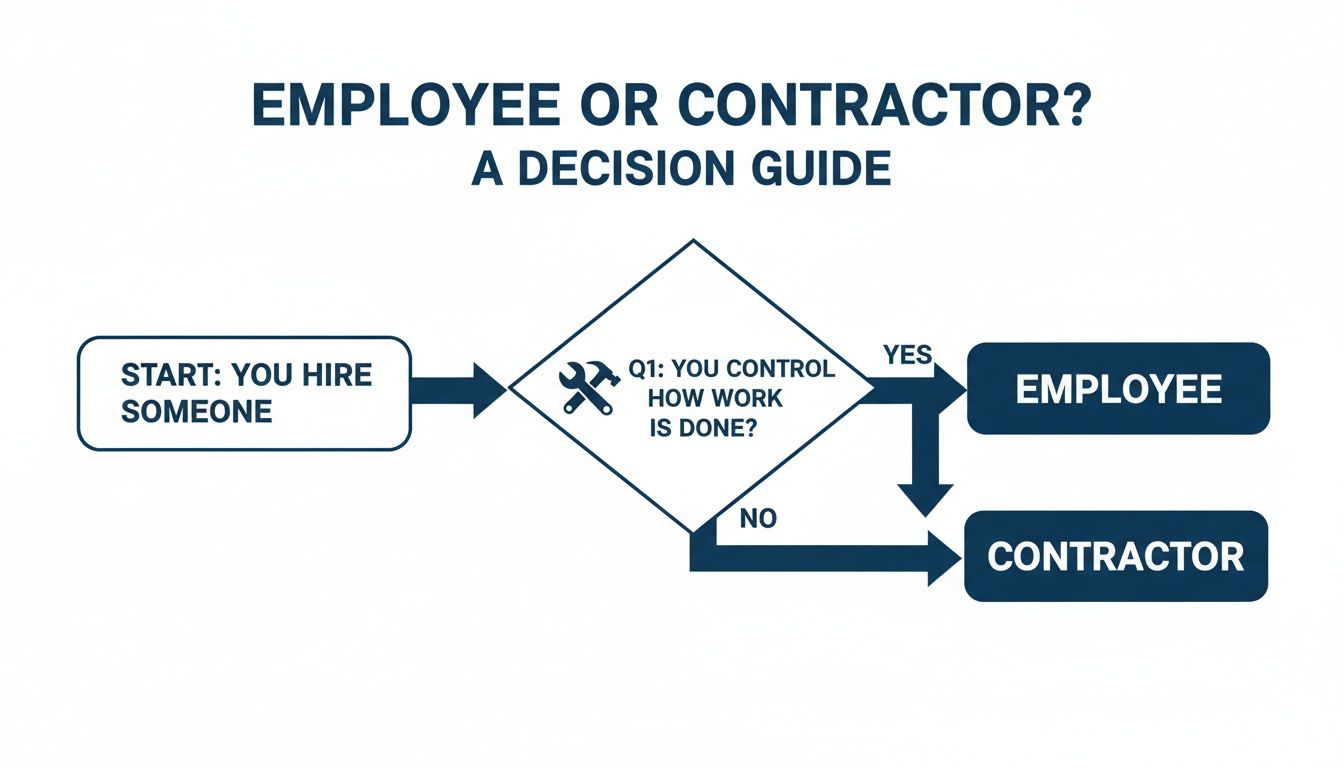

Let's clear this up, because it trips up a lot of people. The main question isn't what you call the person—it’s about who is in control.

Imagine you hire someone to clean your house. You give them a to-do list, provide the vacuum and cleaning sprays, and tell them which rooms to tackle first. In that case, you control how and what they do. That person is your employee.

Now, let's flip it. You hire a professional cleaning company. A team shows up with their own supplies and uses their own methods to make your house sparkle. You're paying for the result (a clean house), but you don't manage how they do it. In that case, they’re an independent contractor.

This difference is everything.

Employee vs. Contractor: The All-Important Control Test

The IRS uses a "control test" to figure out if someone is an employee or an independent contractor. It's the most important factor in knowing what you need to do.

This guide helps break it down.

As you can see, it all comes down to whether you have the right to direct and control how the work is done.

This isn't just a small detail; it's a legal line with real financial outcomes. The moment you pay a household employee $2,700 or more in one year (for 2026), you become an employer. That means you're responsible for handling certain taxes.

You can read the official IRS guidelines for household employees for all the details, but understanding this employee vs. contractor difference is the first—and most important—step.

Employee vs Contractor Quick Comparison

Use this quick table to see if the person you hire is an employee or a contractor.

| Factor | This Looks Like an Employee | This Looks Like a Contractor |

|---|---|---|

| Tools & Supplies | You provide the vacuum, computer, or other needed tools. | They bring their own equipment and supplies. |

| Instructions | You set the schedule and give step-by-step instructions. | They set their own hours and use their own methods. |

| Training | You train them on how to do the job your way. | They are already trained and work on their own. |

| Other Clients | They work only for you or mostly for you. | They have their own business and work for other clients. |

| Payment Method | You pay them a regular wage (hourly, weekly, etc.). | You pay them a flat fee for the whole job. |

This table should give you a good feel for it. If your situation points to the "employee" column and you pay them more than the yearly limit, it's time to start thinking like an employer.

Common Examples of Household Employees

The term “household employee” might sound formal, like you need a mansion with a full staff. But the truth is, millions of regular families have them and might not even know it.

It all goes back to that simple question of control. Let’s look at a few real-world examples.

Caregivers for Children and Seniors

Nannies are the clearest example. When you hire a nanny, you’re the one who sets the schedule, explains the house rules, and provides the home where they work. They are working for your family and following your lead, which makes them an employee. When you look for help, it’s smart to find qualified nannies who already understand this setup.

Senior caregivers work the same way. If you hire someone to help your mom or dad with meals, errands, or personal care in their own home, you become the employer. You're the one telling them what needs to be done each day.

Did You Know? This isn't a small part of the economy. Over 2.2 million people work as domestic workers, mostly in childcare, house cleaning, and home care. And it's a field dominated by women, who hold 91.5% of these jobs, according to this report from the Economic Policy Institute.

Helpers Around the House

What about the people who help keep your home and yard in order? This is another big area where you might accidentally become an employer.

- Housekeepers: If someone comes on a regular schedule, uses your cleaning supplies, and follows your to-do list, they’re your employee. They are working under your direction, not as their own separate business.

- Gardeners: The person you pay by the hour to mow your lawn, pull weeds, and plant flowers where you tell them is usually an employee. This is different from hiring a big landscaping company for a one-time project with its own crew and equipment.

- Personal Chefs: If you have a chef come a few times a week to cook meals based on your family's diet and tastes, that also creates an employer-employee relationship.

See the common theme? In all these cases, you’re in charge. You’re not just paying for a finished product; you’re controlling how the work gets done. That control is the bright line that makes you an employer in the eyes of the law.

This is where the casual deal with your nanny or housekeeper gets serious. Most people think being an “employer” means having a formal business and a team of people. But for household help, it's much simpler—and the rules kick in after just a few thousand dollars.

It’s not a choice you get to make; it’s a line you cross. The IRS has specific payment amounts that, once you hit them, automatically turn you into a household employer with legal and tax duties. Let’s break down exactly what those lines are.

The First Line: Social Security and Medicare Taxes

The biggest number to watch is the yearly pay limit for FICA taxes—that’s Social Security and Medicare.

For 2026, if you pay any single household employee $2,700 or more in cash for the year, you are responsible for these taxes. This isn't just paperwork; these payments help your employee build credit for their future benefits. You can learn more about this directly from the Social Security Administration.

Think about how fast that adds up. Paying a housekeeper just $60 a week will put you over the $2,700 line before the year is over. It’s a much lower bar than most people think.

The Second Line: Federal Unemployment Taxes

Next is federal unemployment tax, or FUTA. This tax pays for unemployment benefits for workers who lose their jobs for reasons that aren't their fault.

The rule here is different. You owe FUTA taxes if you pay a total of $1,000 or more in cash wages to all your household employees combined in any three-month period (called a "calendar quarter").

Here’s the catch: once you hit that $1,000 mark in any quarter, you are responsible for FUTA for the whole year. It applies back to January 1 and continues through December 31.

For example, let's say you hire a nanny and pay her $2,000 in January and February. Because you paid over $1,000 in the first quarter, you now owe FUTA tax on every dollar you pay her for the entire year, not just for those first few months. This is a detail that trips up a lot of people.

Putting It All Together

So, when do you need to start acting like an employer? The second you realize you're going to cross either of these two lines:

- The FICA Line: Paying one employee $2,700 or more in a year.

- The FUTA Line: Paying all employees a combined $1,000 or more in any quarter.

If you're on track to meet either of those, it’s time to start the paperwork. Your casual helper has officially become a formal employee, and that means you need to step up and handle your duties as an employer.

Okay, you've hired someone to help at home, and now you're wondering, "Am I an employer now?" The answer is almost always yes.

Don't panic. This doesn't mean you need to rent an office or become an accounting expert overnight. Just think of it as a simple, step-by-step plan. Let’s walk through exactly what you need to do to handle this right.

First, you need an Employer Identification Number (EIN). It’s like a Social Security number for you as an employer. Getting one is free and fast on the IRS website. You'll use this number on all your tax forms.

Next, you need to check that your employee is legally allowed to work in the United States. This is done with Form I-9, Employment Eligibility Verification. You and your employee fill it out together, and you check their documents to confirm their identity and work status. You keep this form for your records; you don’t send it to the government.

Understanding the Taxes

Now for the part that sounds much scarier than it is: taxes. There are a few different types, but they’re manageable once you know what they are.

FICA Taxes (Social Security & Medicare): This is the main one. As the employer, you have to make sure these taxes get paid. The total FICA tax is 15.3% of your employee’s pay. You can either pay the full amount yourself or split it. The common way is to take 7.65% from their pay and then you pay the other 7.65% yourself.

FUTA Taxes (Federal Unemployment): This tax is all on you, the employer. It's a small percentage on the first $7,000 you pay your employee each year. It’s a small cost, but an important part of doing things correctly.

Income Taxes: Here’s a key difference. You are not required to hold back federal income tax from your employee's pay. However, your employee might ask you to. It can be a big help for them so they don't get a huge tax bill at the end of the year. If they ask, they’ll fill out a Form W-4, and you can agree to do it for them.

Remember, your state might have its own rules, like state unemployment taxes or paid family leave. For example, some states have local taxes you need to handle. Our guide on paid time off and sick leave can also help you figure out common benefits.

Paperwork at the End of the Year

At the end of the year, it all comes down to two key forms. Don't let the form numbers scare you; they're pretty simple.

The Two Forms You Can't Forget: Your whole year as a household employer really just boils down to these two documents. Getting them right is the key to staying legal and making tax time easy for both you and your employee.

First is Form W-2, Wage and Tax Statement. You must give this to your employee by January 31st of the next year. It shows everything you paid them and all the taxes you took out. They need this to file their own tax return.

Second is Schedule H, Household Employment Taxes. This is your report card to the IRS. You attach this form to your own personal tax return (like Form 1040). It’s where you report the wages you paid and figure out the total FICA and FUTA taxes you owe for the year. This is how you pay the government what you owe.

Paying Your Household Employee the Right Way

Once you've accepted you're an employer, the next big question is how to handle payday. It's tempting to just pay in cash or send money through an app. But paying "under the table" is one of the biggest mistakes you can make.

Paying legally isn’t just about avoiding trouble with the IRS. It’s about doing right by the person who helps you. When you handle payroll correctly, your employee gets the protections they deserve, like building a history for Social Security and being able to get unemployment benefits if they ever need them.

The Pay Rules You Can't Ignore

Most household employees, like nannies, caregivers, and housekeepers, are protected by a federal law called the Fair Labor Standards Act (FLSA). This law sets some firm rules you have to follow.

- Minimum Wage: You must pay at least the federal minimum wage. But here’s the catch: many states and even cities have higher minimum wage laws. You have to pay whichever rate is the highest.

- Overtime Pay: This is a big one that surprises many families. For any hours your employee works over 40 in a single workweek, you must pay them 1.5 times their regular hourly rate. This "time-and-a-half" pay is not optional.

For example, say your nanny’s regular rate is $20 per hour. If they work a 45-hour week, you pay them the normal rate for the first 40 hours. But for those extra 5 hours, you have to pay them $30 per hour ($20 x 1.5).

Why Keeping Good Records Is Your Best Friend

I know, tracking hours and creating pay stubs sounds like a huge pain. But good records are your best protection. This isn’t just about paperwork; it’s what protects you from any arguments later about hours or pay.

Think of it this way: A clear record is your proof that you're being fair and following the rules. A simple timesheet and a pay stub for each payday create a clean history that protects everyone. It gets rid of any guesswork or "he said, she said" fights.

A pay stub is easy to make. It just needs to list the total hours worked, the pay rate, any overtime, and any taxes you took out. This builds trust and shows your employee that you are professional.

And if you pay them back for using their car for work, writing that down separately is important. You can find all the details in our guide on managing company mileage rates. Good records just make everything smoother.

Making Household Payroll Simple with a Partner

If you've made it this far, your head might be spinning with checklists, tax forms, and new things to do. That’s totally normal. The rules for hiring someone at home can feel like a full-time job on their own.

But here’s the good news: you don't have to become a payroll expert. There’s a way to get this all done right without getting lost in paperwork.

Bringing in an Expert

Think about hiring a partner to handle all the boring, behind-the-scenes work for you. For many families, this is the smartest thing to do. To make sure your employee is paid right and on time, many people use dedicated payroll services.

This is like having a affordable expert on your team who deals with this stuff all day. They manage the whole process, so you never have to worry about missing a deadline or making a costly mistake.

A good payroll partner does more than just cut checks. They protect you from headaches. They figure out the taxes, manage direct deposits, and file all the right federal and state forms for you, on time, every time.

The value for a busy family is huge. Instead of spending your nights and weekends trying to understand tax rules, you get that time back for what really matters. It frees you from the paperwork and gives you peace of mind that everything is being handled correctly.

This isn’t just about making life easier; it’s about getting it right. A payroll partner removes the guesswork—and the risk of penalties—from your plate. They can set up your payroll, figure out your employee's withholding, and keep you on the right side of all the rules.

If you'd like to see how this works, learn more about our simple, effective accounting and payroll services.

Frequently Asked Questions About Household Help

Once you've found the perfect person to help at home, the last thing you want to think about is taxes. But a few common questions always come up, and getting the answers wrong can be a costly mistake.

Let’s clear up some of the most common mix-ups we see.

Does My Teenage Babysitter Count?

This is the question we get most often. For the occasional date night sitter, the answer is usually no. The IRS made a special exception for this, so you can relax.

The “nanny tax” rules don’t apply if your babysitter is under 18 and babysitting isn’t their main job. Plus, you only have to worry about Social Security and Medicare taxes once you pay someone more than the yearly limit, which is $2,700 for 2026. Your casual sitter will almost never reach that amount.

Can I Just Give My Nanny a 1099 Form?

No, definitely not. This is probably the most common—and most expensive—mistake a household employer can make. A Form 1099 is for an independent contractor, but the person watching your kids is almost always your employee. Why? Because you control their schedule, what they do, and how they do it.

Trying to call them a contractor is a huge red flag for the IRS. It looks like you're trying to avoid paying taxes, and that can lead to big trouble with back taxes, interest, and fines. Your nanny needs a W-2 at the end of the year, plain and simple.

What Happens If I Never Paid These Nanny Taxes?

First, don't panic. But don't ignore it, either. Hoping the problem goes away is a bad idea, because the IRS bill for unpaid taxes, penalties, and interest just gets bigger over time.

The best thing to do is to come forward and get caught up. It shows you're trying to do the right thing. Working with a tax expert or a payroll service can help you file the old tax forms and try to get those penalties reduced or even removed.

Do I Need Workers' Compensation Insurance?

This one is tricky because the answer depends on where you live. Every state has its own rules for workers' comp, and they are all different. Some states require you to have it if you have even one employee, while others have different rules.

It's very important to check your state’s specific rules. This insurance is your safety net—it protects you from lawsuits and covers your employee’s medical bills and lost pay if they get hurt on the job. It's a non-negotiable part of being a responsible employer.

Feeling overwhelmed? MyOfficeOps can manage your household payroll from start to finish, ensuring you stay compliant without the stress. Learn how we make it simple at myofficeops.com.