You’re probably not looking for “a bank.” You’re looking for a place to put money, move money, borrow money, and not have your week blown up by clunky logins, missing wires, bad loan fit, or a branch that treats your business like a side hobby.

That’s the issue with searching for banks in west chester. Most lists tell you where the branch is and whether there’s a drive-thru. Fine. But if you run a law firm, clinic, contractor, agency, or real estate business, your bank should work like part of your back office. It should fit your bookkeeping process, support payroll, make cash flow easier to read, and help you make smarter calls when it’s time to hire, buy equipment, or clean up the books before a sale.

West Chester has deep banking roots. The Bank of Chester County, established in 1814, was the first bank chartered in Chester County and later reorganized as the National Bank of Chester County on October 25, 1864, before the historic building was added to the National Register of Historic Places on June 5, 1972. That history matters because local business owners still need the same thing they needed then. Stability, access, and good financial judgment.

If cash is tight and timing feels off, this guide to managing cash flow for small business is worth reading alongside your bank search.

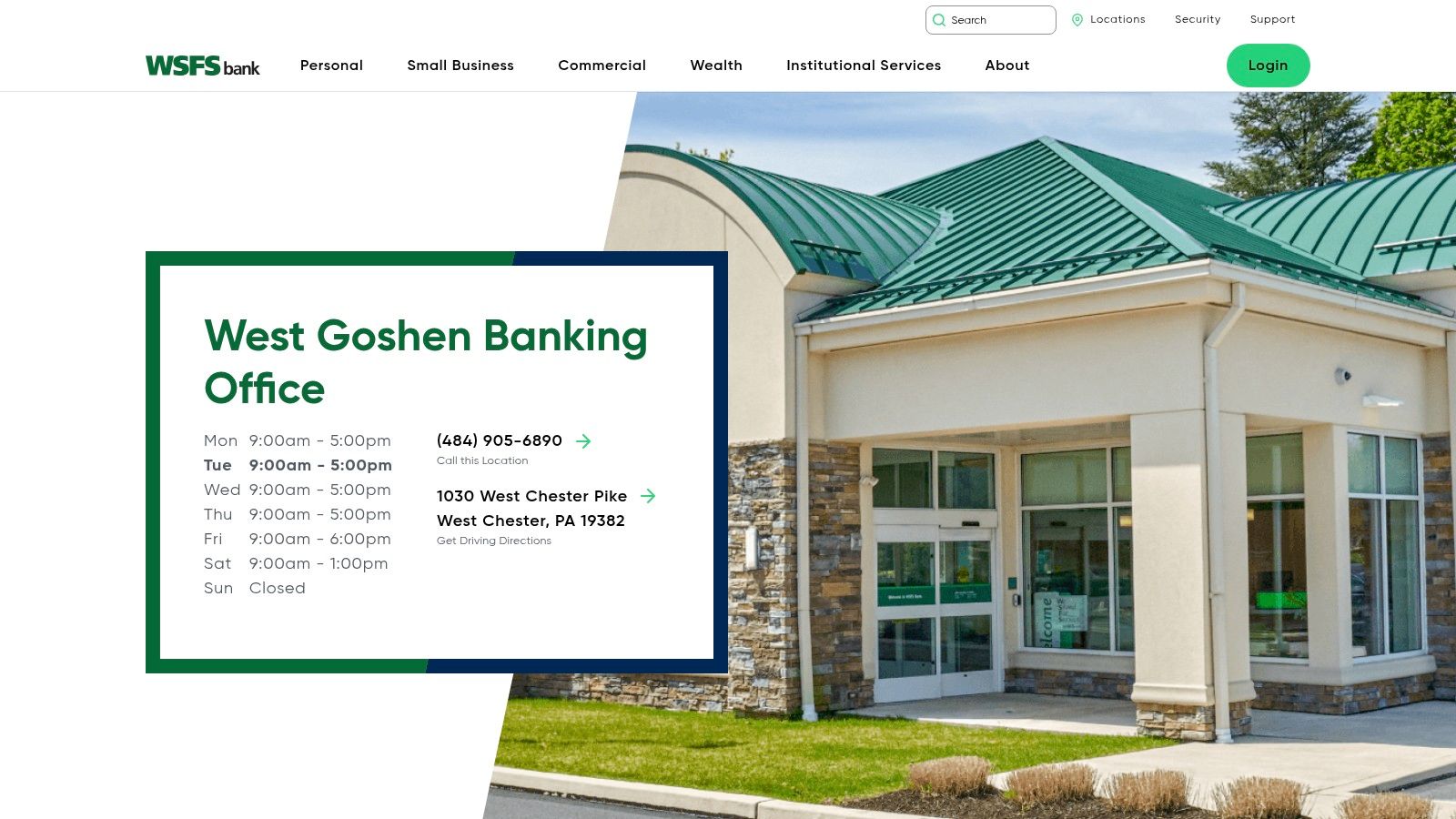

1. WSFS Bank – West Goshen

WSFS is a good fit when you want a regional bank that still feels reachable. For a lot of owner-led companies, that matters more than a flashy app. If you need a person who understands your accounts, your cash cycle, and why one bad month doesn’t tell the whole story, WSFS usually sits in the right lane.

Best for owners who want a real banker

This is the kind of bank I’d put in front of a service firm that wants day-to-day banking plus room to grow into better treasury habits. Think law firms, agencies, medical practices, and local operators with a few moving parts but not a full finance department.

What tends to work well:

- Relationship banking: You’re more likely to value WSFS if you want direct banker access instead of bouncing between a branch, a hotline, and a generic inbox.

- Core business services: Checking, lending, cash management, and treasury tools cover the basics most small and midsize firms use.

- Useful local presence: If your team still deposits checks, needs branch help, or wants local conversations around credit, that’s a plus.

The trade-off is simple. WSFS isn’t the bank you pick for nationwide convenience first. You pick it for proximity, context, and service.

Practical rule: If your bank knows your revenue but not your billing cycle, they don’t know your business yet.

If you’re comparing local options and want a more finance-first lens, this breakdown of West Chester business banking support is a useful companion.

Direct website: WSFS Bank West Goshen

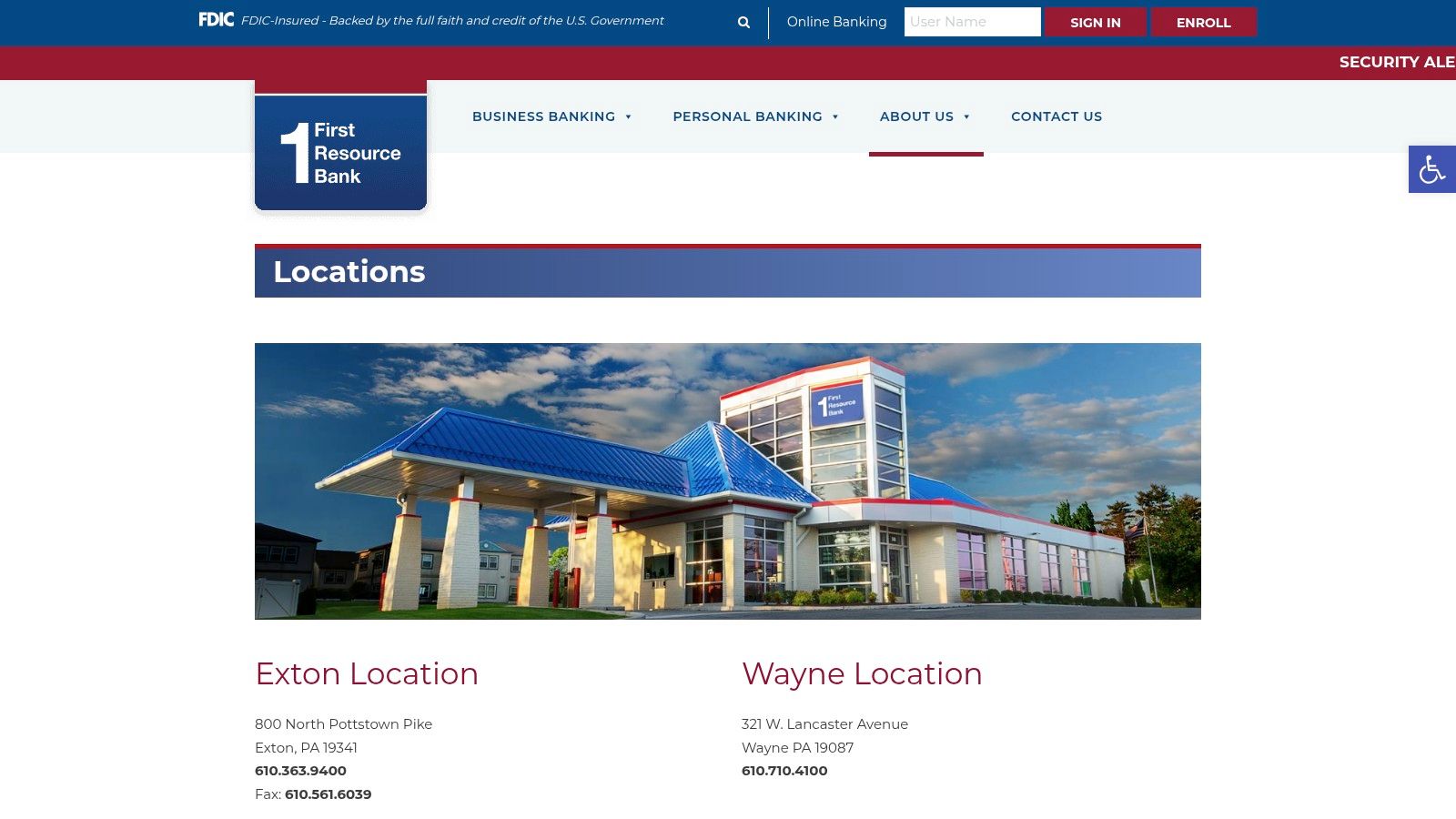

2. First Resource Bank – West Chester

A lot of owners hit the same wall at some point. Sales are fine, but cash still feels tight because bookkeeping lags, payroll hits before receivables clear, and the bank only shows balances instead of helping you set up a better system.

That is where First Resource can make sense.

The appeal here is not rate shopping or branch scale. It is clarity. For a business owner who wants to tie banking closer to how money moves through the company, a smaller local bank can be easier to work into weekly operations. You can keep operating cash, savings, and borrowing under one roof, then build simple routines around them for payroll timing, owner draws, tax reserves, and basic cash forecasting.

Best for owners who want banking that supports the back office

First Resource fits best for companies that have outgrown personal-bank habits but do not need a giant institution. I usually see the best fit with firms that want straightforward business checking, access to a loan or line, and local conversations about real estate or working capital without getting pushed through five departments first.

What stands out in practice:

- Cleaner decision-making: Fewer account options can be a benefit if you want your team to use the setup correctly instead of guessing which product does what.

- Local credit conversations: If your numbers need context, such as seasonality, uneven project billing, or a temporary dip tied to hiring, direct access matters.

- Good fit for process-minded owners: This bank works better when you use it as part of your operating system, not just a place to park money.

That last point matters. A bank relationship starts paying off when it connects to bookkeeping and payroll, not when it sits off to the side. If your reconciliations are late or payroll pulls from the wrong account, even a good bank setup gets wasted. Owners who need help tightening that side of the operation should also review Pennsylvania accounting firms that support bookkeeping and finance workflows.

The trade-off is straightforward. First Resource is less likely to be the right choice if you need a large branch footprint, specialized treasury features, or national-bank depth for a more complex finance stack.

For businesses trying to connect banking to the rest of the money picture, this guide on how to manage business finances helps tie the pieces together.

Direct website: First Resource Bank community locations

3. Fulton Bank – West Chester (Downtown & West Goshen)

Fulton usually lands in the middle ground. That’s not a criticism. It’s often the sweet spot. Bigger than a small community bank, more local-feeling than a giant national chain.

For growing companies, that can be a smart setup. You get treasury tools, multiple checking paths, merchant support, and lending options without feeling like you’ve entered a maze.

Better for growing firms than brand-new ones

If you’re still very small, Fulton can feel like more bank than you need. But once you’re juggling ACH runs, merchant deposits, wires, and separate accounts for taxes or projects, it starts to make more sense.

I’d pay special attention here if you run a construction business. Existing local content around banks in west chester usually skips contractor-specific financing needs, even though that’s often where the stress lives. The gap is real enough that recent discussion around the topic points out the lack of useful local guidance for builders trying to connect lending, treasury services, and bookkeeping workflows in West Chester, PA, especially as financing gets harder for construction firms (Commerce Bank reference discussing the content gap).

Contractors don’t fail because they’re busy. They fail because cash arrives late, costs move fast, and nobody sees the whole picture soon enough.

That’s why a bank like Fulton only works if you pair it with tight reporting. Treasury tools are helpful. They are not a substitute for job costing or good books.

If you need outside finance support while sorting bank fit, this directory of accounting firms in Pennsylvania can help you find the right support layer.

Direct website: Fulton Bank

4. First Bank (NJ) – West Chester

A lot of owners hit the same point. Payroll is due, bookkeeping is behind, a client payment is late, and the last thing you need is a bank that treats every question like a ticket number. First Bank tends to work better for companies that want direct access to a banker who can help connect the dots.

That matters more than many owners expect. A bank is not just where you park cash. It should fit the way money moves through your business, from deposits and bill pay to payroll timing and monthly close. If your accounting team needs clean account separation and quick answers from the bank, relationship banking starts to carry real operational value.

The West Chester branch at 849 Paoli Pike adds a practical advantage. First Bank’s West Chester branch page shows local branch details, including Saturday availability. For an owner who spends weekdays buried in jobs, patients, clients, or staff issues, that convenience can save real time.

A practical fit for owner-led firms

First Bank makes the most sense for businesses that want a banker who knows the company and can respond without layers of handoffs.

That often includes:

- Professional service firms: Law firms, agencies, consultancies, and accounting practices usually care about responsiveness, clean cash management, and fewer banking headaches for the back office.

- Real estate businesses: Landlords, investors, and small operators often benefit from local lending conversations and straightforward deposit relationships.

- Companies tightening operations: If you’re trying to align bank accounts with bookkeeping, payroll runs, and cash reserves, a more personal bank relationship can make setup and maintenance easier.

The trade-off is scale. If your business needs advanced treasury integrations, broad national coverage, or complex structures across multiple entities, you may outgrow this setup.

For a local company that values access, speed, and a bank that can support day-to-day financial operations without unnecessary complexity, First Bank sits in a useful middle ground.

Direct website: First Bank West Chester branch

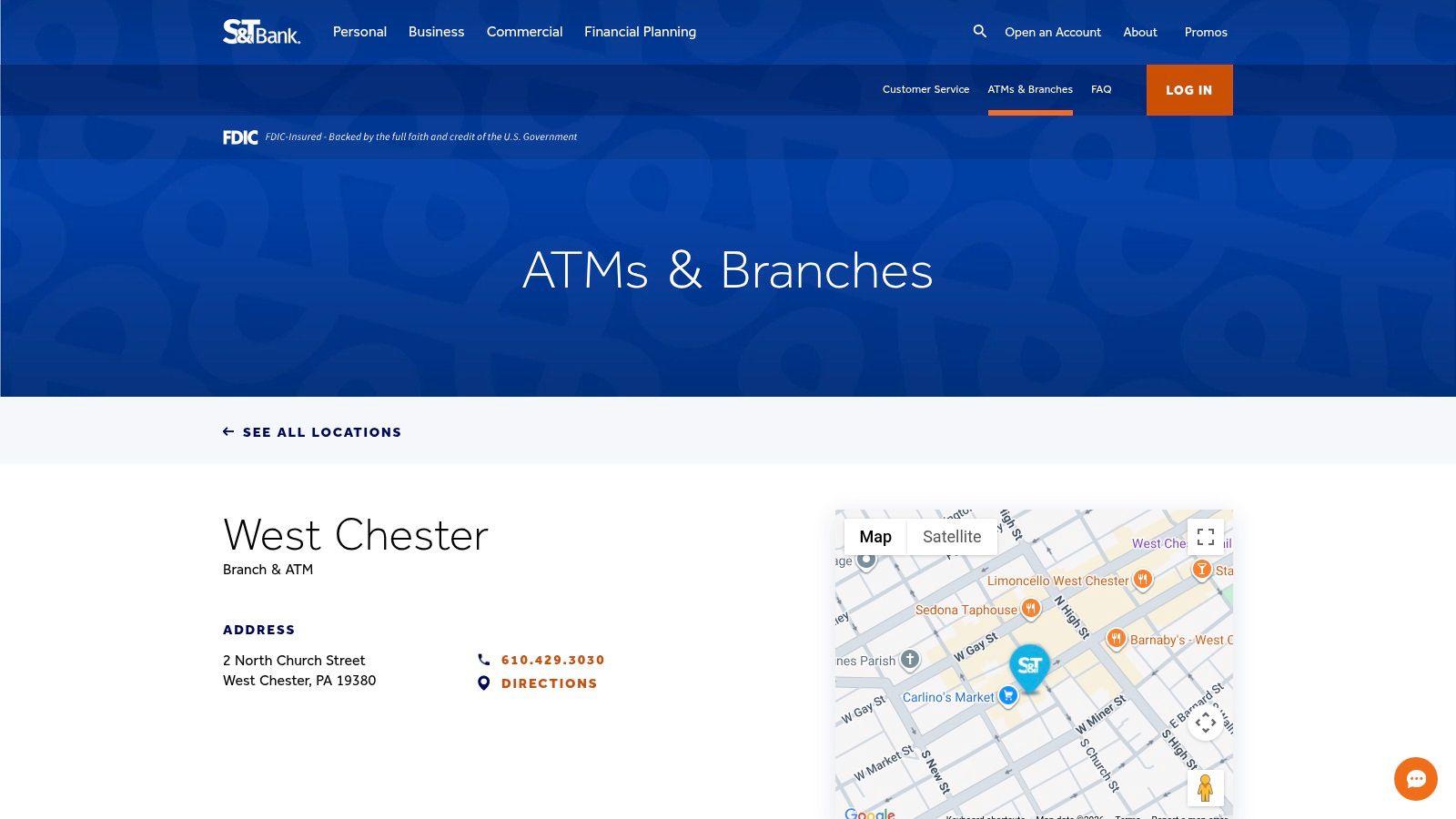

5. S&T Bank – West Chester

Payroll clears Friday. Vendor payments hit Monday. A tax transfer is coming next week. If that rhythm sounds familiar, S&T Bank can make sense for a business that wants steady banking operations more than flashy features.

S&T tends to work best for owners who run on predictable financial habits and want a bank that supports them with the basics done right. That usually means deposit accounts, lending, cash management tools, and branch access that help keep bookkeeping and daily cash movement under control. If your office manager is still chasing deposits, matching ACH activity by hand, or sorting through avoidable account clutter, your bank is part of the problem.

A practical match for firms that want control over cash flow

I’d look at S&T for businesses that need their bank to fit into operations, not sit off to the side as a place where money parks. Contractors, medical practices, and other owner-led firms often fall into that camp because their cash flow has a pattern, even when balances move around.

A few strengths stand out:

- Conventional business lending: Useful for equipment purchases, working capital needs, real estate, and other financing tied to normal operations.

- Cash management fundamentals: ACH and remote deposit services matter if you want fewer manual steps between collections, payroll, and reconciliations.

- Branch-backed banking: Some owners still want a local contact when a payment issue, account change, or loan question needs attention.

The trade-off is straightforward. S&T is usually a better fit for businesses that value consistency and banker access than for companies chasing advanced treasury tech, complex integrations, or a highly polished digital stack.

That doesn’t make it a lesser option. It makes it a more specific one.

A good banking relationship should help your bookkeeper close the month faster, help payroll run cleanly, and give you a clearer view of operating cash before you make the next hiring or equipment decision.

Direct website: S&T Bank West Chester locations

6. Truist – West Chester

Truist is usually worth a look if you want a larger platform without going all the way to the biggest national banks. It can work well for businesses that need merchant services, lending options, and a more modern digital experience in one place.

This is often where companies land once they’ve outgrown simple checking but still want local branch access.

Stronger when banking and payments need to talk to each other

If your business takes card payments, runs payroll through outside software, and wants fewer manual steps between revenue and reporting, Truist can be a reasonable fit.

Best use cases include:

- Retail and service businesses: Merchant services matter if card acceptance is a daily part of your operation.

- Growing firms needing lending plus treasury: SBA and industry-focused lending can matter as you expand.

- Owners who want digital tools with branch backup: Not every issue should require a branch visit, but some still do.

The trade-off is process friction. Bigger institutions often have stricter setup, verification, and policy requirements. That’s not always bad. It just means less flexibility when your paperwork is messy or your ownership structure is unusual.

I usually tell owners this: if you choose a bank like Truist, get your internal records clean before opening or changing accounts. Good books make account opening, loan review, and ongoing treasury setup much easier.

Direct website: Truist West Chester branch

7. TD Bank – West Chester

TD Bank wins on convenience more than strategy. That’s not a knock. Convenience solves real problems.

If you’re an owner-operator who leaves the office late, needs branch access outside the narrow banker window, or wants business banking that’s easy to understand, TD can be a solid choice.

Best when time is the real shortage

Plenty of business owners don’t need a complicated treasury stack. They need an account that works, branch hours that fit real life, and merchant services that don’t take a month to understand.

TD tends to be useful for:

- Busy local operators: Think restaurants, storefronts, solo owners, and small practices.

- People who want easy account choices: Straightforward account lineups help when you don’t want to study fee logic.

- Businesses with frequent branch needs: Extended and weekend access is the main draw.

The caution is fees. A simple account can stop being simple if you miss waiver rules or let old account settings sit untouched.

This isn’t usually my first pick for a company planning deeper financial complexity. It is a practical pick for owners who need banking to be available when they are.

Direct website: TD Bank West Chester branch

8. PNC Bank – East Bradford (West Chester area)

Your bookkeeper is reconciling three accounts, payroll is due tomorrow, and two managers still have more account access than they should. That is usually the point where a bigger bank starts to make sense.

PNC fits businesses that are outgrowing basic checking. If you have multiple entities, separate operating and tax accounts, or staff members involved in payments, stronger controls matter because they prevent expensive cleanup later.

Better for companies building process

The value here is operational discipline. A bank like PNC can support approval layers, account segmentation, and payment oversight in a way that lines up better with bookkeeping and payroll once your company gets past the owner-does-everything stage.

That makes PNC a practical option for:

- Businesses with more moving parts: Multiple accounts, locations, departments, or legal entities

- Teams that need tighter controls: Better fit when you want to limit who can move money and who can only view balances

- Owners cleaning up back office workflows: Useful if you want banking to connect more cleanly with accounting routines instead of creating month-end surprises

There is a trade-off. Large banks often give you more process, but less flexibility. If your business needs quick exceptions, highly personal service, or a banker who knows your operation without explanation, a smaller local institution may feel easier to work with.

I usually tell owners not to ask one bank to do every job. PNC can be a strong operating bank while reserve cash sits elsewhere and your accounting system ties the full picture together. That setup treats the bank as part of your financial operation, not just a place to park money.

Direct website: PNC Bank

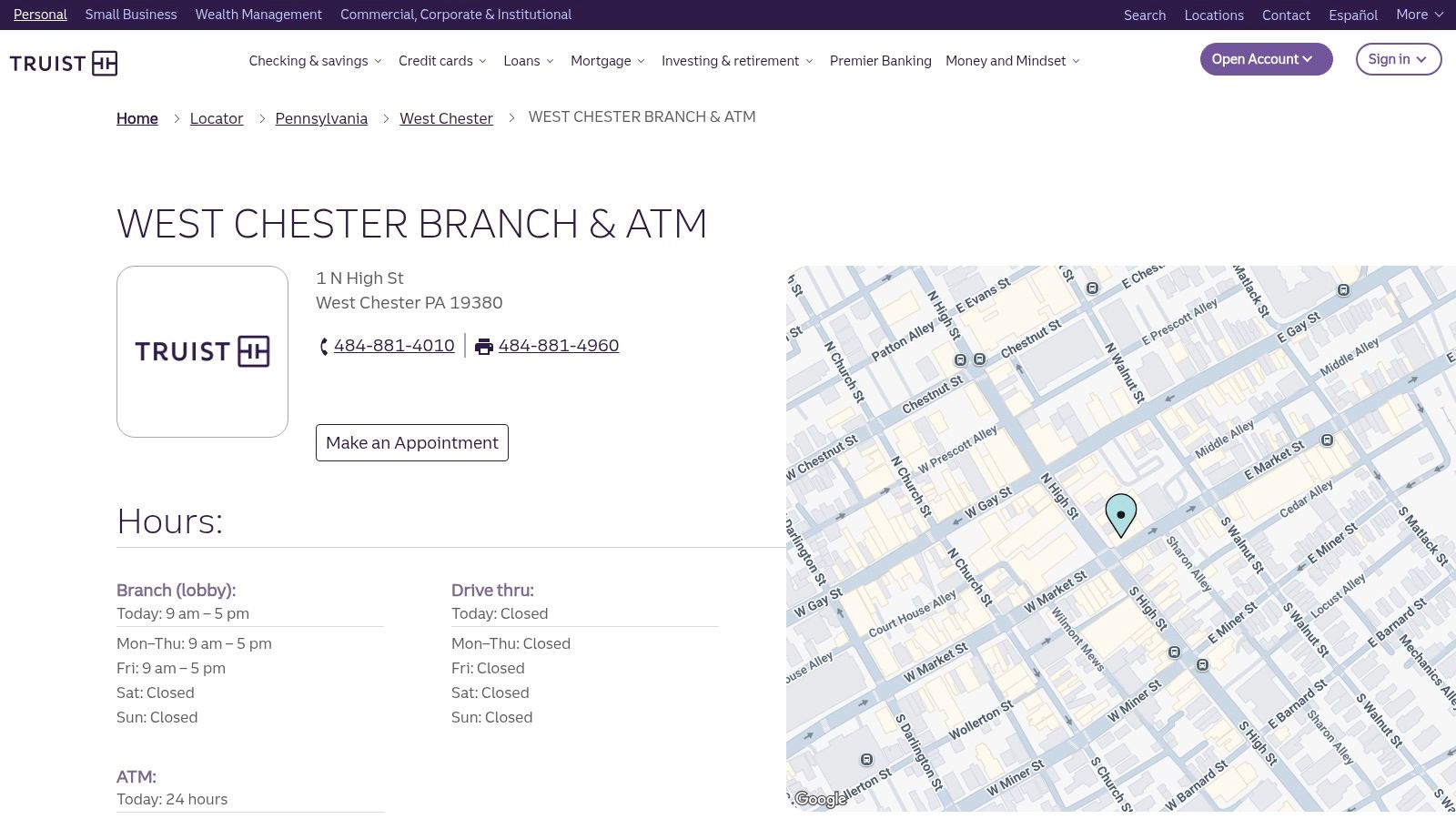

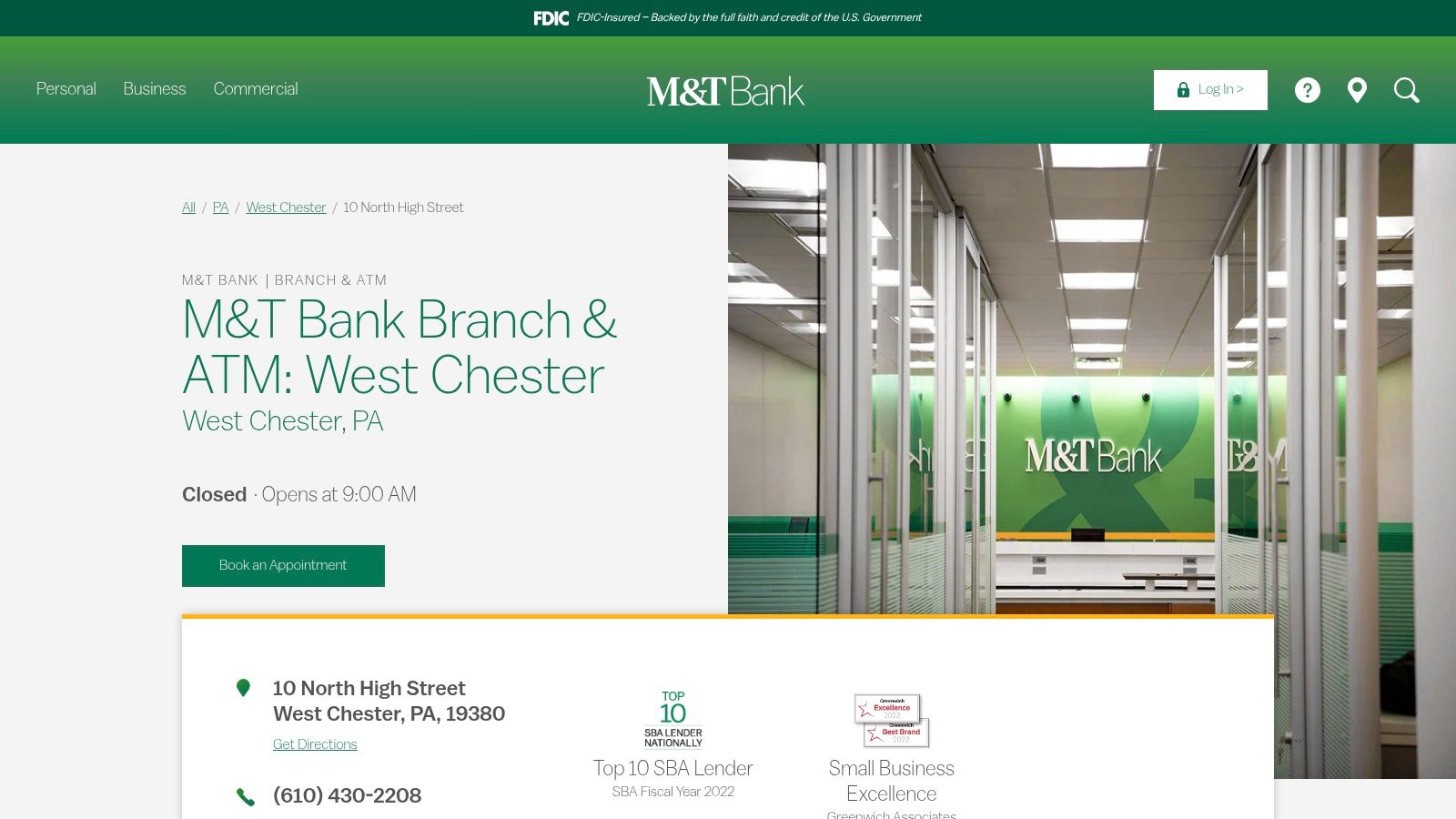

9. M&T Bank – West Chester

You feel the difference with a bank like M&T when the problem is not opening an account. It is getting payroll out on a tight week, covering a timing gap from slow receivables, or keeping a practice's cash flow predictable enough that your bookkeeper is not cleaning up avoidable mess every month.

M&T tends to fit established firms that want a regional bank with business banking depth and a branch team that still feels reachable. I see it work best for medical offices, law firms, accounting firms, and other local operators that need steady support, lending access, and a banker who understands that cash flow rarely moves in a straight line.

Where M&T fits best

The value here is not flashy technology. It is having a bank that can sit inside your operating system and support how money moves through the business.

That usually looks like this:

- Stable operating accounts: Good fit for businesses that need dependable daily banking, deposits, and basic cash management.

- Support for established service firms: Useful for practices and professional offices that care about credit access, steady account management, and fewer surprises.

- A workable middle ground: More business-focused than a very small local bank, but often easier to work with than a giant national institution.

That middle ground matters. If your controller, office manager, or outsourced bookkeeper needs clear account structure for payroll, taxes, and operating cash, the bank should help create that discipline. A good setup can reduce miscoding, make reconciliations cleaner, and give you better visibility into what is free to spend.

There is a trade-off. If your company depends on advanced integrations, heavy automation, or a very software-first treasury setup, you may find stronger digital options elsewhere. If your business wants consistent people, local access, and a bank that can handle normal lending and cash flow conversations without turning everything into a support ticket, M&T stays on the shortlist.

I usually tell owners to judge a bank by how well it fits the back office after the account is opened. If it helps bookkeeping stay clean, payroll stay protected, and reserve cash stay separate from spending cash, it is doing more than holding deposits.

Direct website: M&T Bank West Chester branch

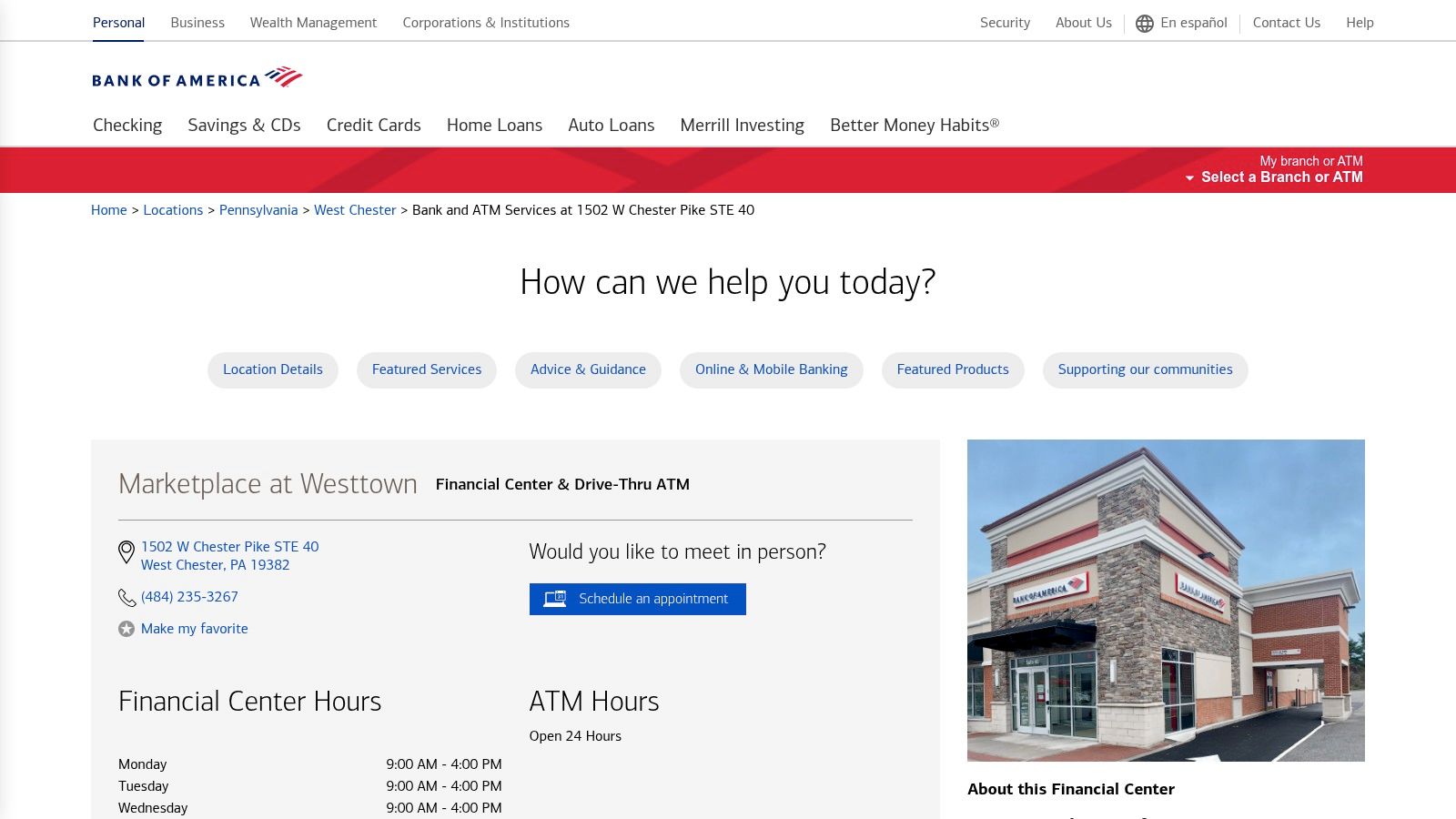

10. Bank of America – Marketplace at Westtown

If your business wants scale, Bank of America is hard to ignore. This is the bank for owners who care about broad product depth, national reach, strong payments, and systems that can plug into a bigger reporting setup.

It’s not the most personal option for very small firms. But for some businesses, that trade is worth it.

Best for businesses that need reach and structure

A professional service firm with remote staff, multiple payment flows, and outside software tools may find this setup useful. A larger operator with wires, card activity, and more layered reporting probably will too.

There’s also a broader trend behind that. Recent discussion of small business banking points out that fee structure and digital limitations remain a major pain point, with 68% of small businesses citing banking fees as a top issue in the 2025 PYMNTS Small Business Banking Report, as referenced in local WSFS-related coverage. That’s why Bank of America should be reviewed carefully. Big-bank power is real, but so is fee complexity.

What usually works:

- Large-bank toolset: Good for companies that want strong treasury and analytics capabilities.

- Nationwide footprint: Useful if your owners or staff move around a lot.

- API and integration potential: Helpful when finance reporting is becoming more technical.

What often doesn’t:

- Small business intimacy: Very small firms can feel invisible.

- Complex fee review: You need to understand the account, not just open it.

For the right business, this bank can be a strategic platform. For the wrong one, it’s just a more expensive checking account.

Direct website: Bank of America Marketplace at Westtown

Top 10 West Chester Banks Comparison

| Bank / Location | Core offerings | UX & Quality (★) | Pricing & Value (💰) | Best for (👥) | Standout / USP (✨ / 🏆) |

|---|---|---|---|---|---|

| WSFS Bank – West Goshen | Checking, money markets, loans/lines, cash management, RDC, local credit decisioning | ★★★★, relationship-driven, fast underwriting | 💰 Moderate, relationship pricing | 👥 Owner-managed SMBs in Chester County | ✨ Local decisioning & dedicated relationship managers 🏆 |

| First Resource Bank – West Chester | Business deposits, loans/lines, CRE financing, mobile/RDC | ★★★★, very responsive local bankers | 💰 Low–Moderate, simple, transparent fees | 👥 Small community businesses | ✨ Community-focused accessibility |

| Fulton Bank – West Chester | Multiple checking, merchant services, treasury (ACH/wire), RDC, SBA & CRE | ★★★★, solid cash-management & branches | 💰 Competitive for growing firms | 👥 Growing SMBs needing cash mgmt | ✨ Strong treasury tools + local branches |

| First Bank (NJ) – West Chester | Business checking, treasury, lines, equipment & CRE lending, local decisioning | ★★★★, relationship-first service | 💰 Flexible, negotiable commercial terms | 👥 Professional services & real estate owners | ✨ Relationship model + convenient hours |

| S&T Bank – West Chester | Checking, treasury/ACH, RDC, C&I & CRE, equipment financing | ★★★, consistent local underwriting | 💰 Solid, traditional lender value | 👥 Contractors, healthcare practices | ✨ Reliable regional lending & service |

| Truist – West Chester | Business tiers, treasury, merchant & payroll integrations, SBA, modern digital | ★★★★, advanced digital + strict onboarding | 💰 Moderate–Premium, broad product set | 👥 SMBs needing integrations & industry programs | ✨ Industry-focused teams & modern platform 🏆 |

| TD Bank – West Chester | Extended hours, business checking, merchant solutions, RDC | ★★★★, very convenient branch hours | 💰 Moderate, higher if waivers not met | 👥 Owner-operators & retail businesses | ✨ Extended/weekend hours for busy owners |

| PNC Bank – East Bradford | Analyzed accounts, RDC, ACH/wires, Positive Pay, merchant, SBA | ★★★★, deep treasury capabilities | 💰 Premium, fees can add up without waivers | 👥 Growing firms needing advanced treasury | ✨ Extensive treasury & integration tools 🏆 |

| M&T Bank – West Chester | Business deposits, SBA & commercial lending, cash management, RDC | ★★★★, reliable regional support | 💰 Balanced, SMB-friendly pricing | 👥 Medical & professional practices | ✨ Practice-banking expertise |

| Bank of America – Marketplace at Westtown | Multiple checking tiers, robust treasury, merchant services, APIs, nationwide footprint | ★★★★, enterprise tools; less personal | 💰 Premium/complex fee schedules | 👥 SMBs needing scale, APIs & global payments | ✨ Enterprise-grade integrations & APIs 🏆 |

Final Thoughts

A lot of owners make this decision after a bad week. Payroll is due, deposits are slow to post, the bookkeeper cannot match transactions cleanly, and nobody at the bank picks up. That is usually when it becomes obvious that your bank is part of operations, not just a place to park cash.

Choose the bank that fits how your business runs day to day. Brand matters far less than how well the account structure, lending access, online controls, and support model match your workflow.

I’d judge the choice on three practical points.

First, map how money enters and leaves the business. If you take card payments, deposit checks, send wires, sweep cash between entities, or keep separate accounts for payroll and taxes, the bank needs to support that without creating extra cleanup work in the books. A good setup should make reconciliation faster, not harder.

Second, decide what kind of support you will need when something goes sideways. Some businesses need a banker who can help with a line increase, a fraud issue, or a tight cash week. Others care more about strong online tools and approval controls than personal contact. Those are different service models, and owners usually feel the gap only after a problem shows up.

Third, connect the bank to the rest of your financial operations. Growth usually strains the system. If bank feeds are messy, payroll timing is off, merchant deposits are hard to trace, or nobody reviews cash by account, revenue can rise while cash still feels unpredictable. In my experience, that is rarely a bookkeeping issue alone. It is a setup issue across banking, reporting, and process.

West Chester gives business owners a useful mix of options. Local and regional institutions can offer better access to decision-makers. Larger banks usually bring stronger treasury tools, broader payment capabilities, and tighter integrations with payroll and merchant platforms. Credit unions and community banks can also be a good fit if your needs are straightforward and you value responsiveness. The right answer depends on how complex your operation is and how much change you expect over the next 12 to 24 months.

Security deserves attention too. If your bank account ties into payroll, ACH, wires, and vendor payments, one weak process can create a very expensive mess. This guide to bank data breach threats and responses is worth keeping on your radar.

A good bank should help you run a cleaner business. It should support faster closes, better cash visibility, fewer payment surprises, and better decisions as the company grows.

If you want help choosing the right banking setup, cleaning up the books around it, and connecting bank activity to payroll, reporting, forecasting, and profitability, talk to MyOfficeOps. They work with West Chester and Greater Philadelphia businesses that need more than bookkeeping. They help owners turn bank data into better decisions.