You're busy serving clients, managing staff, chasing payments, and solving problems all day. Then someone asks how the business is doing, and you give the answer most owners give when the books aren't clear: “We're busy, so I think we're doing fine.”

Busy and profitable are not the same thing.

That's the gap I see all the time with service businesses around West Chester. A law firm can have a full calendar and still struggle with cash. A clinic can be booked solid and still not know which services make money. A contractor can finish jobs every week and still feel broke because labor, materials, and timing aren't showing up clearly in the numbers.

Good accounting fixes that. Not fancy accounting. Not accounting that lives in a drawer until tax season. Just clean, useful, up-to-date accounting that helps you make decisions while they still matter.

Why Your Business Needs More Than Just Bookkeeping

A lot of owners think bookkeeping and accounting are the same thing. They overlap, but they are not the same.

Bookkeeping is the act of recording what happened. Accounting is what turns those records into answers. It tells you whether you can hire, whether your pricing works, whether a service line is pulling its weight, and whether cash is tightening before it becomes a real problem.

The real problem is not missing data

Most businesses have data somewhere. It's in the bank feed, the payroll system, the credit card portal, the invoicing app, or the owner's inbox. The problem is that the information often isn't organized in a way that helps you decide anything.

That's why some owners feel blindsided even when they “have software.” The software has transactions. It does not automatically give you clarity.

The gap is bigger than many people realize. The IRS's 2024 Small Business/Self-Employed Tax Gap data shows an estimated net tax gap of about $540 billion for tax years 2021 through 2023, with a voluntary compliance rate of about 85.8%, according to this discussion of the IRS small business tax gap data. That points to a basic issue. A lot of owners still don't have complete, decision-ready records.

Practical rule: If your books only answer tax questions once a year, they're not doing enough for the business the other eleven months.

What owners actually need from accounting

Think of accounting like the dashboard in your truck or car. You don't need it because you enjoy looking at gauges. You need it because driving blind is a bad plan.

For service businesses, the right accounting system should help you answer things like:

- Hiring decisions. Can the business support another admin, tech, associate, or provider?

- Pricing questions. Are your rates covering payroll, overhead, and the time it takes to deliver the work?

- Cash timing. Are you collecting fast enough to keep up with payroll, rent, and vendor payments?

- Profitability by service or job. Which work pays well, and which work just keeps everyone busy?

If you want a simple breakdown of where bookkeeping fits into that bigger picture, this guide on what a bookkeeper does for a small business is useful.

The shift that changes everything

Once owners stop treating accounting like a compliance task, they make better decisions. They stop asking, “Did we make money last year?” and start asking, “What's changing right now?”

That's the point.

You don't need perfect numbers every minute of the day. You need clean enough numbers, often enough, to run the business with your eyes open.

Understanding the Core Accounting Concepts

If accounting feels confusing, it usually comes down to too much jargon. The basics are simpler than they sound.

Your business has money coming in, money going out, things it owns, and things it owes. Accounting is just a system for sorting that information the same way every time so the reports mean something.

Think of the chart of accounts like a filing cabinet

Your chart of accounts is the list of buckets where every transaction goes. If that list is messy, your reports will be messy too.

For a service business, those buckets should be clear and practical. Payroll. Rent. Software. Subcontractors. Medical supplies. Job materials. Travel. Owner draws. Client revenue. That sort of thing.

A bad chart of accounts creates bad answers. If a contractor mixes tools, materials, and subcontractors into one big expense category, job profitability gets fuzzy. If a consulting firm dumps all software costs into “miscellaneous,” no one can tell what the tech stack is really costing.

Here's an easy way to understand it:

| Account type | What it means in plain English |

|---|---|

| Assets | What the business owns |

| Liabilities | What the business owes |

| Equity | The owner's stake |

| Revenue | Money earned from services or sales |

| Expenses | What it costs to run the business |

Cash and accrual tell different stories

One of the biggest choices in accounting for small business owners is the method you use.

According to Coursera's small business accounting guide, cash-basis accounting records transactions when cash changes hands, while accrual-basis accounting records income when earned and expenses when incurred.

That sounds technical, but the day-to-day effect is easy to understand.

Say a contractor finishes work in January and sends the invoice then, but the client pays in February.

- Under cash basis, the income shows up in February when the money lands.

- Under accrual basis, the income shows up in January when the work was earned.

That difference matters. Cash basis can help you watch near-term liquidity. Accrual gives a fuller picture of profitability and working capital.

A profitable month on paper can still be a tight month in the bank. That's why the method matters.

The concepts you actually need to know

You don't need to become a CPA to run your business better. You do need to know what your reports are trying to tell you.

A simple checklist helps:

- Know your revenue categories. Don't lump every service into one line if different services earn very different margins.

- Separate direct costs from overhead. Job labor and materials tell a different story than office rent.

- Pick your accounting method early. Your invoicing, bank rules, and month-end process should match it.

- Keep owner activity clean. Personal spending and owner draws should never blur operating numbers.

When these basics are set up right, the business stops feeling like a guessing game.

Building a Rock-Solid Bookkeeping Routine

The businesses with the least accounting stress usually aren't the ones with the fanciest systems. They're the ones with the most consistent habits.

A good bookkeeping routine is boring in the best way. It captures what happened, stores proof, and keeps things current enough that month-end isn't a rescue mission.

Start with separation

The first rule is simple. Keep business money separate from personal money.

That means a dedicated business bank account and, in most cases, a dedicated business credit card. Once spending gets mixed, every review takes longer, every report gets less trustworthy, and tax prep becomes more painful than it needs to be.

According to QuickBooks' small business accounting overview, best practice is to record every cash movement, attach source documents like invoices and receipts, and use dedicated business bank accounts and accounting software to create a clean audit trail and support reconciliation.

A weekly rhythm that works

Most owners don't need to touch the books every day. They do need a weekly routine.

A simple version looks like this:

Pull in the transactions

Review what cleared the bank and credit card accounts.Categorize each item

Don't leave expenses sitting in “ask my accountant” or “uncategorized” forever.Attach backup

Add receipts, invoices, payroll reports, and loan statements where they belong.Check for odd items

Look for duplicate charges, missing deposits, owner spending, or vendor payments that don't make sense.Flag questions right away

If you can't remember what a transaction was, you probably won't remember next month either.

Source documents matter more than people think

A clean transaction without backup is still weak.

If a clinic buys equipment, there should be an invoice. If a consultant bills a client, there should be a copy of the invoice. If payroll runs, there should be payroll records. Good bookkeeping creates a trail someone else can follow without asking you to explain every line.

That matters for taxes, of course. It also matters for normal business decisions. If you want to review software costs, job expenses, or marketing spend, you need to trust what's sitting behind the number.

Clean books are built from two things. Accurate entries and proof that supports them.

What usually does not work

Some systems look fine for a month or two and then fall apart.

Common trouble spots include:

- Shoebox bookkeeping. Saving receipts without entering the transactions doesn't create usable books.

- Bank-feed autopilot. Automation helps, but rules can misclassify transactions fast if nobody reviews them.

- Quarterly catch-up. Waiting too long makes errors harder to fix and trends harder to spot.

- Owner memory. “I'll remember what that charge was later” is almost always false.

A steady routine beats a heroic cleanup every time.

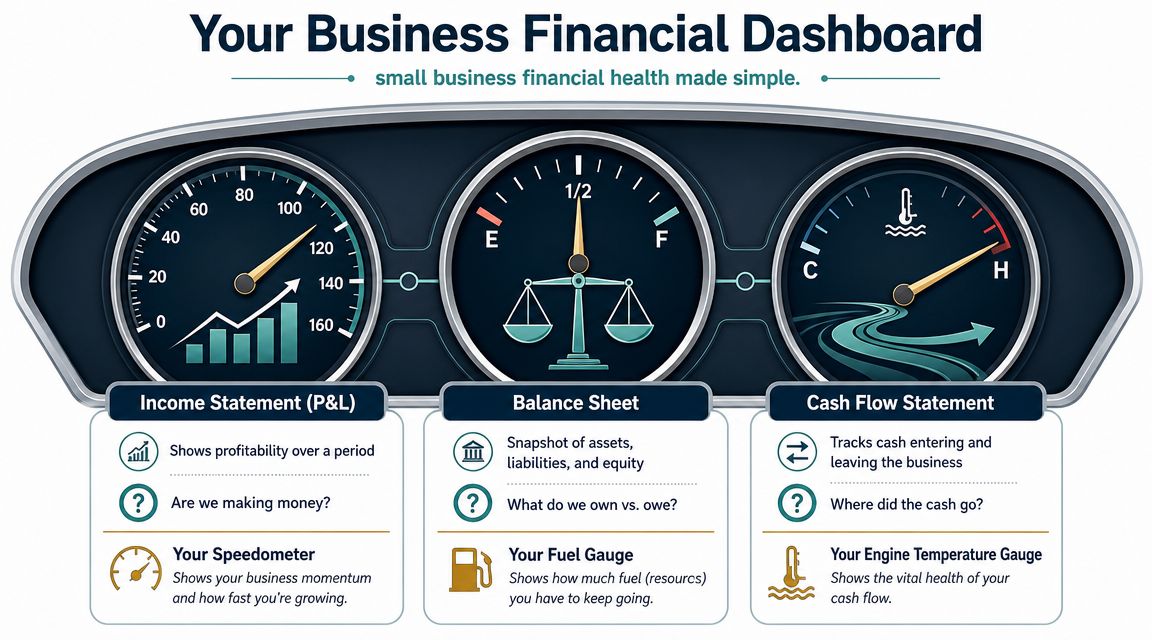

The 3 Financial Reports Every Owner Must Understand

Most owners don't need more reports. They need to understand the three reports that matter.

Think of them like your business dashboard. If you only look at one gauge, you can still get into trouble. Profit, balance, and cash each tell a different part of the story.

According to Accounting.com's guide to small business accounting, the balance sheet, income statement, and cash flow statement are the foundational reports for small businesses because they help owners track assets, liabilities, revenue, expenses, and cash movement for decisions on pricing, hiring, and growth.

The income statement shows performance

A small consulting firm is a good example.

In one month, it bills clients, pays staff, covers software subscriptions, and spends money on rent and insurance. The income statement, also called the profit and loss statement or P&L, shows whether that activity produced profit over a period of time.

This is your speedometer. It tells you how fast the business is moving financially.

Look at it to answer questions like:

- Are we making money from operations?

- Are payroll costs rising faster than revenue?

- Is one service line carrying the whole business?

- Are overhead costs getting out of line?

If you want a clearer look at how to read these reports in practice, this resource on financial reporting for small business is a helpful next step.

The balance sheet shows position

Now take that same consulting firm on the last day of the month. It has cash in the bank, invoices still waiting to be paid, a computer setup, a credit card balance, maybe a loan, and owner equity.

That's what the balance sheet captures. It's a snapshot at a point in time.

I often describe it as the mechanic's inspection report. It tells you the shape of the machine.

A balance sheet helps you see:

| Question | Where to look |

|---|---|

| Do we have cash and receivables to cover near-term bills? | Assets and current liabilities |

| Are we leaning too hard on debt? | Loans and credit balances |

| Is the business building value or draining it? | Equity trends over time |

The cash flow statement shows movement

This is the one owners skip too often, especially if the P&L looks decent.

Cash flow explains why a profitable period can still feel tight. Maybe clients are paying slowly. Maybe loan payments are pulling cash out. Maybe the business bought equipment. Maybe payroll hit before collections came in.

That's why I call cash flow your fuel gauge. You can be headed in the right direction and still run out of gas.

Profit answers whether the work made money. Cash flow answers whether the business can breathe while doing it.

For service businesses, this report matters even more when payroll is heavy, payment cycles are uneven, or project timing shifts from month to month.

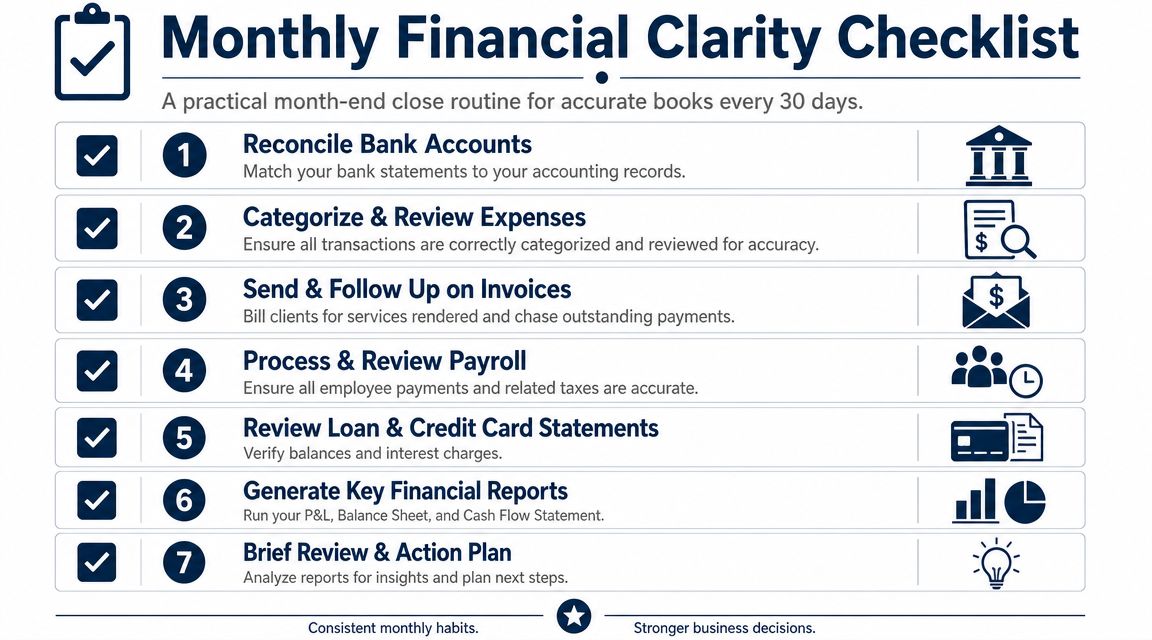

Your Monthly Close Checklist for Financial Clarity

A monthly close sounds like something only a large company would do. In reality, it's just the routine that turns a month of activity into numbers you can trust.

I explain to owners that it's much like locking up the shop at night. You don't leave the doors open and hope everything's fine in the morning. The same idea applies to the books.

What a clean month-end looks like

A solid close does not need to be dramatic. It needs to be complete.

Use this checklist:

- Reconcile bank accounts. Match the books to the actual bank and credit card statements.

- Review expense coding. Fix items that landed in the wrong place.

- Make sure invoices went out. Service work that isn't billed on time hurts cash fast.

- Review collections. Look at who still owes you and what needs follow-up.

- Check bills and debt activity. Make sure loan, credit card, and vendor balances make sense.

- Review payroll entries. Confirm wages, taxes, and related costs posted correctly.

- Run the main reports. Look at the P&L, balance sheet, and cash flow statement together.

What to look for when you review

The close is not just a data exercise. It's a review step.

Ask practical questions:

| Area | Question to ask |

|---|---|

| Revenue | Did all completed work get invoiced? |

| Expenses | Is anything unusually high or coded oddly? |

| Receivables | Who is late, and what is the follow-up plan? |

| Payables | What's due soon, and will cash cover it? |

| Cash | Are we heading into a squeeze next month? |

If you run a medical practice, that might mean checking whether insurance-related timing is slowing collections. If you run a construction business, it might mean looking for project costs that posted late or to the wrong job. If you run a law firm, it might mean making sure billed time turned into invoices and not just draft entries.

Monthly close is where bookkeeping becomes management.

The biggest benefit is not cleaner books

It's fewer surprises.

When owners skip month-end review, small problems get buried. A missing deposit, an old unpaid invoice, a duplicate software charge, a misposted loan payment. None of these are hard to fix early. They become annoying and expensive when they sit.

A few focused hours each month can save a lot of confusion later. More important, it gives you a steady rhythm for making decisions while there's still time to act.

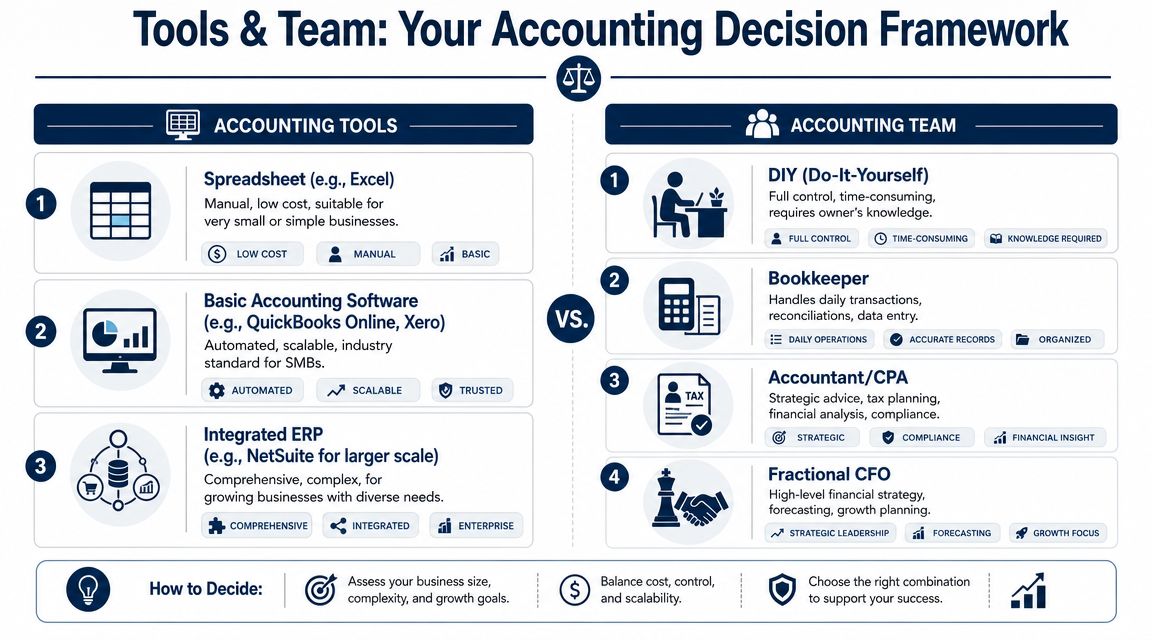

Choosing Your Accounting Tools and Team

Owners usually ask two questions here. What software should I use, and who should handle the work?

The right answer depends on the business, but the wrong answer is easy to spot. It's the setup that saves a little time today and creates confusion every month after that.

Choose tools that fit the work

For very simple businesses, a spreadsheet can work for a while. But once you have recurring expenses, payroll, client invoicing, credit cards, or multiple people touching the process, software usually makes more sense.

Most service businesses end up comparing tools like QuickBooks Online and Xero. Larger or more complex operations may look at systems with broader integrations. What matters is not the logo. What matters is whether the system supports your workflow.

Use these criteria:

- Invoicing and collections. Can it handle how you bill clients?

- Bank feeds and rules. Does it reduce data entry without turning review into a mess?

- Payroll integration. Can payroll flow in cleanly?

- Reporting. Can you pull useful reports without a lot of manual cleanup?

- User access. Can staff, owners, and advisors have the right level of access?

- Document storage. Can you attach the backup where it belongs?

For owners comparing options, this guide on how to choose accounting software lays out the decision points clearly.

Decide who owns the process

The team side is just as important as the software side.

Here's the practical trade-off:

| Option | Works well when | Main downside |

|---|---|---|

| DIY | The business is still simple and the owner is disciplined | It steals owner time and often slips |

| Bookkeeper | You need consistent transaction entry and reconciliations | May not provide deeper analysis |

| Accountant or CPA | You need review, tax alignment, and stronger reporting | Often not focused on day-to-day bookkeeping |

| Fractional CFO support | You need forecasting, pricing help, or strategic planning | Usually overkill if the books aren't clean first |

One option in this mix is an outsourced partner like MyOfficeOps, which handles bookkeeping, reporting, payroll-related coordination, and advisory support for small and midsize businesses. That kind of setup can make sense when an owner wants one team managing the routine work and helping interpret the numbers.

Automation helps, but controls matter more

This part gets ignored too often. Software can speed up accounting, but it can also speed up mistakes.

The U.S. Small Business Administration's 2025 cybersecurity guidance emphasizes that small businesses are frequent targets of payment fraud and need controls like multifactor authentication and secure backups, as summarized in this article discussing SBA cybersecurity guidance for small businesses.

That matters in accounting because owners now rely on bank feeds, online payments, vendor portals, and automation rules.

A few plain rules go a long way:

- Use multifactor authentication on accounting, banking, and payroll tools.

- Limit access so not everyone can add vendors, change bank details, or approve payments.

- Review automation rules regularly so software isn't repeating a bad assumption.

- Keep backups of key financial records and source documents.

- Separate approval from payment when possible, even in a small office.

A tool should make your process cleaner. It should not remove human judgment from the points where errors and fraud usually show up.

Turning Your Numbers into Your Next Big Move

At some point, every owner asks a bigger question than “Are the books up to date?”

They ask whether the business is worth expanding, whether it can support another hire, whether it's healthy enough to weather a rough patch, or whether it could eventually be sold.

That's where accounting for small business owners becomes more than administration. It becomes direction.

Good numbers create better choices

When your books are current and your reports are clear, decisions stop feeling like guesses.

You can look at a service line and decide whether to raise prices. You can see whether slow collections are the cash problem. You can compare labor-heavy work to higher-margin work. You can tell whether growth is helping the business or just making it more complicated.

That's the payoff. Better accounting shortens the distance between what happened and what you do next.

Your financials are not a report card. They're a map.

This matters now and later

Owners often think valuation is only relevant when they're ready to sell. That's too late.

The habits that make a business easier to run also make it easier to value. Clean financial statements, steady reporting, visible profit drivers, and documented processes all matter when a buyer, lender, or investor looks at the company. If you want a plain-English overview of how buyers think about value, Miro Capital's valuation guidance is a useful reference point.

Even if selling isn't on your radar, building a business with clear numbers gives you options. It helps with transitions, financing, partner conversations, and simple peace of mind.

The next move is usually simpler than owners think

You do not need to fix everything at once.

Start by making the books current. Then make them consistent. Then review them monthly. Once that rhythm is in place, the reports become useful, and useful reports lead to better decisions.

That's how a business moves from reacting to planning.

If you want help turning messy books into decision-ready reports, MyOfficeOps works with small and midsize businesses in Greater Philadelphia and beyond on bookkeeping, reporting, payroll coordination, and advisory support. It's a practical fit for owners who want clear numbers, a steady monthly process, and better visibility into cash flow and profitability.