Outsourced bookkeeping for a small business usually runs from about $300 to over $1,200 per month. Where your business lands in that range depends on how much work your books need, not just whether you call it “bookkeeping.”

If you're reading this after a long day, trying to figure out why the bank balance doesn't match QuickBooks and whether you can afford help, you're in good company. A lot of owners around Philadelphia and West Chester wait too long because they assume bookkeeping is either cheap data entry or a luxury they can skip. It's neither.

Clean books help you answer basic questions fast. Did we make money this month? Are we behind on receivables? Can we afford to hire? Those answers matter a lot more than whether someone charged you one way or another for reconciliations.

How Much Do Bookkeeping Services Cost a Small Business

A small business usually pays about $300 to $1,200 per month, or $3,600 to $14,400 per year, for outsourced bookkeeping, based on published pricing guidance from CoCountant's small business bookkeeping cost breakdown. At the lower end, you're usually paying for basic transaction entry and reconciliations. At the higher end, the work often includes payroll, monthly reporting, or catch-up cleanup.

That range helps, but it doesn't solve the problem. Two businesses can both be “small” and need very different levels of support. A solo consultant in Center City with one bank account and a handful of monthly expenses isn't buying the same service as a contractor in the Philly suburbs trying to track job costs, vendor bills, payroll, and customer deposits.

Practical rule: Don't ask only, “What does bookkeeping cost?” Ask, “What level of financial clarity do I need every month?”

I've seen owners treat bookkeeping like a once-a-year tax chore. That usually leads to the same mess. Missing transactions. Old unreconciled accounts. A CPA bill that gets larger because someone has to clean everything up before a return can be filed.

A better way to think about it is as a recurring operating cost that keeps your numbers usable. If you're also sorting through software and workflow questions, these AI automation questions for bookkeepers are worth a look because they get into what can be automated and what still needs human review.

What the lower and higher ends usually mean

- Lower-range support: Basic coding of income and expenses, bank and credit card reconciliation, and a clean general ledger.

- Mid-range support: More review, cleaner monthly closes, and reports an owner can use.

- Higher-range support: Payroll coordination, catch-up work, management reporting, and more oversight when the business has moving parts.

The mistake that costs more later

Owners often shop by monthly fee alone. That sounds sensible, but it can backfire. A lower fee doesn't help if the provider isn't handling the parts that create problems later, like unreconciled accounts or messy payroll mapping.

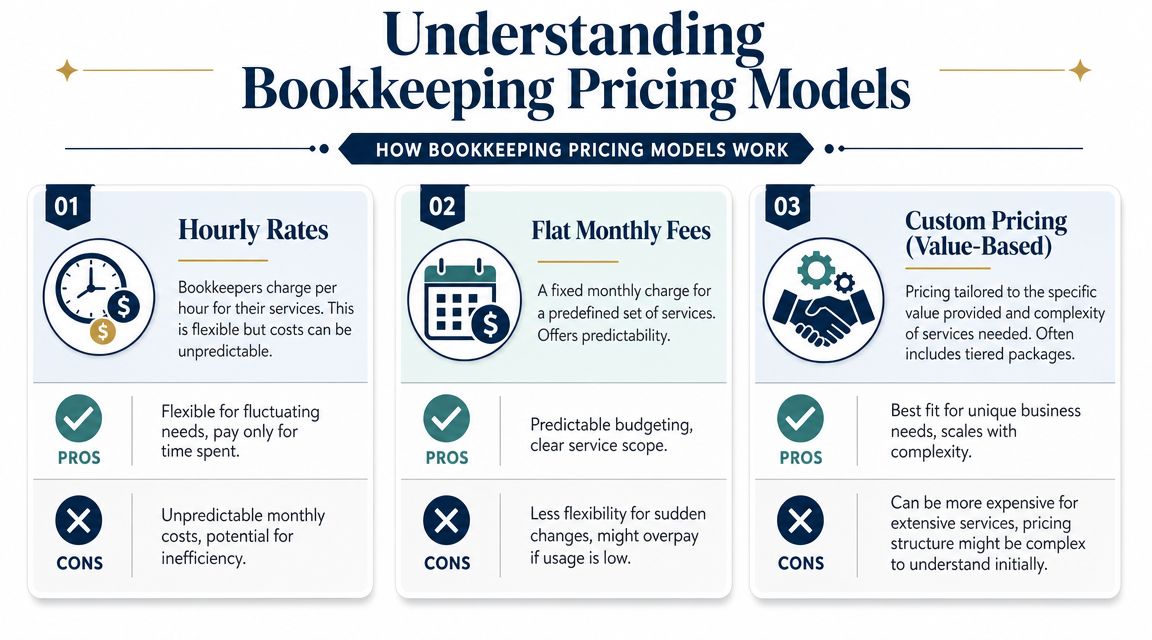

How Bookkeeping Pricing Models Work

Once you start getting quotes, you'll usually see three billing styles. Think of them like phone plans. Some are pay-as-you-go. Some are a steady monthly bill. Some are built around what your business needs.

Published pricing guides note that bookkeeping often falls between $30 and $100 per hour, while many firms now use fixed monthly retainers around $300 to $850 for small businesses because predictable pricing helps both the client and the firm, according to Orbit Accountants' guide to bookkeeping fees.

Hourly pricing

Hourly billing is the easiest model to understand. The bookkeeper tracks time and invoices for the hours used.

This can work well if your needs are light or uneven. Maybe you only need clean-up help once in a while. Maybe your business is brand new and there just isn't much activity yet.

The downside is obvious. Your monthly cost can swing around. If your books are messy, if bank feeds break, or if someone dumps a backlog of receipts on your bookkeeper, the bill moves up with the hours.

Flat monthly fees

Flat monthly pricing is common now because owners want a number they can budget for. You agree on a scope, such as reconciliations, monthly close, and standard reports, and you pay the same fee each month unless the scope changes.

For most small businesses, this model is easier to live with. You know what's coming out of cash flow. The bookkeeping firm knows what work it's responsible for. Expectations stay clearer.

A flat fee works best when both sides are honest about volume and complexity.

The catch is scope creep. If your business adds payroll, another entity, a new location, or a lot more transactions, the old price may stop making sense. That's not a red flag. It just means your bookkeeping needs changed.

Custom packages

Some businesses don't fit neatly into hourly or basic monthly service. A healthcare practice may need bookkeeping plus payroll coordination and reporting. A contractor may need job costing support. A professional service firm may want bookkeeping tied to forecasting and owner reporting.

In those cases, custom pricing often makes more sense.

- For professional services: You may need clean monthly financials and help tracking project or retainer profitability.

- For healthcare: You may need tighter workflow around payroll, reimbursements, and reporting.

- For construction: You may need more review because job costing errors can distort margin fast.

The main question isn't which model is cheapest. It's which one matches how your business runs.

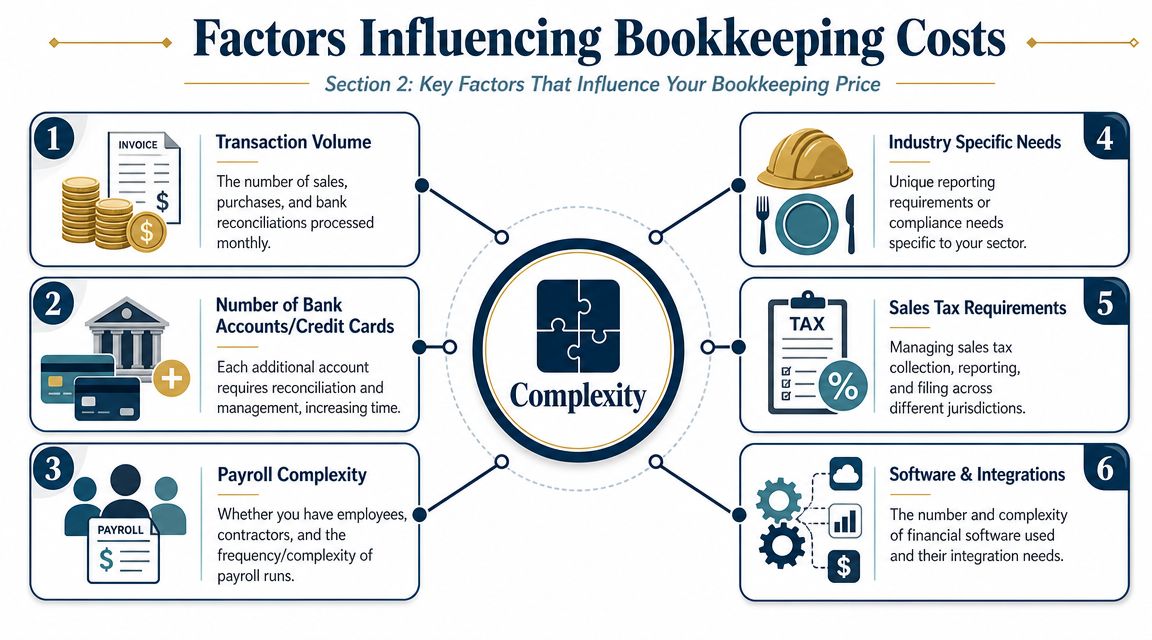

Key Factors That Influence Your Bookkeeping Price

The biggest driver of bookkeeping cost is complexity. Not the label on your business card. Not your revenue alone. Complexity.

That's also why pricing changes when the work moves past basic data entry. The U.S. Bureau of Labor Statistics reported a median hourly wage of $23.66 for bookkeepers in 2024, and that helps explain why more time-intensive work like payroll integration and industry-specific reporting costs more, as summarized in Use Haven's review of bookkeeper charges.

Transaction volume is only the starting point

A business with a light stream of deposits, a few expenses, and one bank account is simpler to maintain than one with lots of card activity, transfers, loan payments, and customer refunds.

But raw volume doesn't tell the whole story. Fifty clean transactions can be easier than a smaller pile of transactions that are coded badly, duplicated, or mixed between business and personal spending.

Accounts and reconciliations add work fast

Every bank account and credit card needs to be reconciled. Every loan account needs to be tracked correctly. Payment platforms need to tie out. If you use systems like QuickBooks, Xero, Gusto, or a merchant processor, someone has to make sure the numbers agree.

More accounts usually means more exceptions. More exceptions means more review time.

Payroll changes the level of work

Payroll isn't just pushing a button. It creates wage expense, tax liabilities, benefit deductions, reimbursements, and timing issues that have to hit the books correctly.

A solo owner with no staff is one thing. A practice with employees, or a contractor juggling field crews and office staff, is another. Once payroll enters the picture, bookkeeping often becomes less about entry and more about review.

Industry needs matter more than many owners expect

A law firm, a clinic, and a construction company can all be similar in size and still need very different books.

- Professional services: Often care about owner draws, payroll, monthly reports, and client profitability.

- Healthcare practices: Usually need cleaner reporting and tighter handling around payroll and operating expenses.

- Construction and trades: Often need job costing, progress billing support, vendor tracking, and more careful review of margins by project.

If your business needs the books to answer operational questions, not just tax questions, your bookkeeping will usually cost more. It should.

Bad books cost more than good books

Catch-up and cleanup work changes everything. If accounts haven't been reconciled in months, if opening balances are off, or if prior entries were posted incorrectly, your bookkeeper has to fix the foundation before monthly work becomes routine.

That's why the cheapest monthly quote sometimes turns into the most expensive relationship. The provider prices for tidy books, then finds a mess.

Sample Bookkeeping Costs for Different Businesses

National averages are useful, but local business owners usually want to know one thing. What would this look like for a business like mine?

Here's a practical way to think about bookkeeping costs for small business owners in Philadelphia, West Chester, and the surrounding suburbs. These examples stay within the published ranges already discussed and show how complexity drives price.

Estimated monthly bookkeeping costs by business type

| Business Profile | Key Needs | Estimated Monthly Cost |

|---|---|---|

| Solo IT consultant in Center City | Basic transaction coding, one or two accounts, monthly reconciliation, standard reports | About $300 to $850 per month |

| Small law firm in West Chester | Reconciliations, payroll coordination, monthly reporting, cleaner close process | About $850 to $1,200 per month |

| Therapy or healthcare practice | Payroll support, expense tracking, monthly reporting, tighter review needs | About $850 to over $1,200 per month |

| Residential contractor in the Philly suburbs | Reconciliations, payroll, vendor tracking, job-level review, more exception handling | About $1,000 to over $1,200 per month |

| Multi-entity service business | More accounts, more reporting layers, owner-level reporting, possible controller review | Over $1,200 per month |

A solo consultant

Think about a one-person IT consultant billing clients monthly. There's one operating account, maybe one credit card, software subscriptions, travel, and a straightforward set of expenses.

That business is often a fit for the lower or middle part of the monthly range. The owner usually needs clean books, reconciled accounts, and reports that make tax season easier. They usually don't need heavy oversight.

A small law office

Now take a small law office in West Chester with a few employees. There's payroll, more recurring expenses, and more pressure to keep records tight every month. The books need to be current, not just “good enough eventually.”

That kind of business often lands in the middle to upper part of the usual outsourced range. The extra cost comes from review time and consistency, not just more transactions.

A healthcare practice

A small clinic or therapy practice often looks simple from the outside, but the bookkeeping can get layered quickly. Payroll matters. Expense categories need to be dependable. Owners usually want reports they can trust because staffing decisions and scheduling affect margins.

At this stage, many businesses move beyond bare-bones bookkeeping. They still may not need a controller, but they do need more than basic categorization.

The right question for a clinic or practice isn't “Can someone keep up with the books?” It's “Can someone keep them clean enough to run the business?”

A contractor or trade business

Construction and trades are where cheap bookkeeping often falls apart. Vendor bills hit at different times. Customer deposits need to be handled properly. Job costs need to land in the right place. Payroll may tie into project work.

That business usually lands at the high end of standard bookkeeping or into a more customized package. If the owner wants to know which jobs are making money and which ones are draining cash, the books need more structure and more attention.

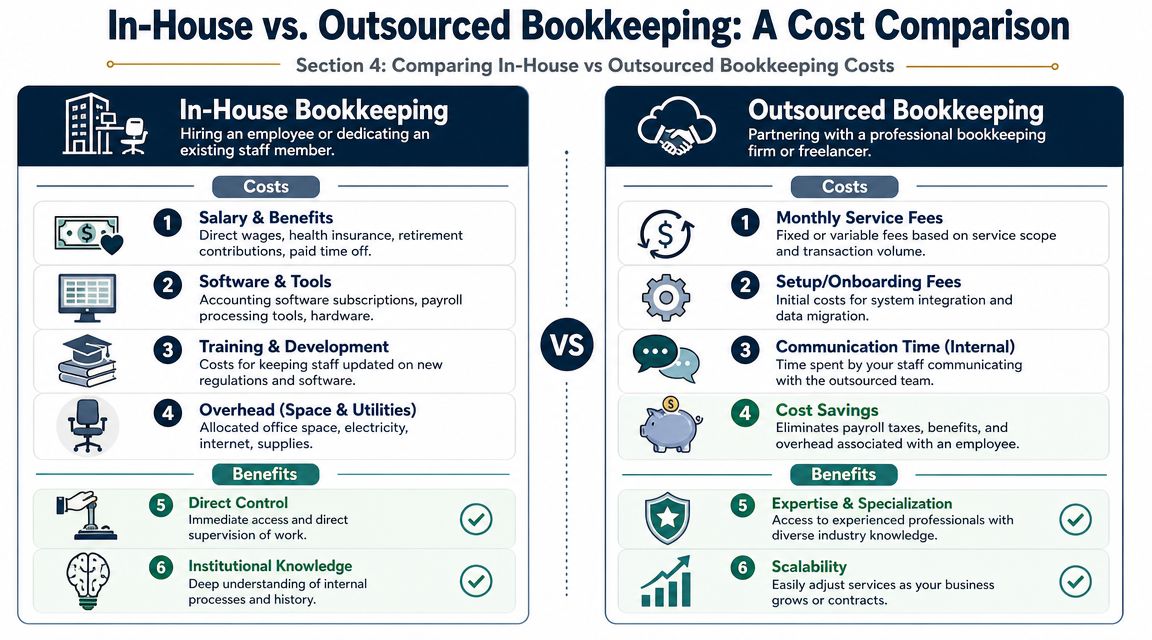

Comparing In-House vs Outsourced Bookkeeping Costs

A lot of owners reach the same fork in the road. Keep outsourcing, or hire someone in-house.

Published industry guidance puts a full-time bookkeeper's salary at roughly $48,000 to $70,000, and employer cost often goes 20% or more above salary once benefits and overhead are included, which pushes the effective monthly cost to about $4,000 to $6,000, according to GrowthForce's analysis of small business bookkeeping costs.

What in-house really buys you

An in-house bookkeeper can be a good fit if you need daily coverage, immediate internal access, and someone fully embedded in your office workflow.

That setup gives you direct control. It can also create dependence on one person. If they leave, take time off, or aren't strong in your industry, the business feels it right away.

What outsourcing usually changes

Outsourcing gives smaller businesses flexibility. You buy the level of support you need instead of carrying a full payroll cost every month.

You also avoid a lot of side costs owners forget at first:

- Benefits and taxes: Salary is only part of the bill.

- Software and training: Someone has to stay current on tools and processes.

- Management time: You still need to supervise, review, and cover gaps.

- Downtime risk: One employee can become a bottleneck.

If you're weighing in-house versus outsourced support, the logic is similar to other back-office decisions. This piece on Rebus insights on marketing choices makes the same basic point in another function. Internal hires bring control, but outside partners often bring flexibility and broader expertise.

When outsourced stops being enough

Some businesses do outgrow basic outsourced bookkeeping. If you need hands-on internal support more often, or your operation has enough moving parts to justify more direct coverage, that can be the right time to look at a more embedded setup such as on-site accounting support.

For many small and midsize businesses, though, outsourced support remains the more practical step. Firms like MyOfficeOps handle bookkeeping, payroll integration, reporting, and advisory support without forcing the owner into a full-time hiring decision.

How to Save Money on Bookkeeping Services

The smartest way to lower bookkeeping costs isn't to squeeze your provider for the cheapest fee. It's to make the work cleaner.

Mess creates labor. Labor creates cost.

Get organized before your bookkeeper has to

If your receipts are scattered across email, glove compartments, and desk drawers, someone has to sort that out. The more organized you are, the less time gets spent on avoidable cleanup.

A few habits help right away:

- Use one business card when possible: Fewer mixed charges means fewer questions.

- Upload documents consistently: Don't wait until quarter-end to send statements and receipts.

- Keep personal spending out of business accounts: That one habit saves more cleanup time than most owners realize.

Respond quickly to questions

Good bookkeeping slows down when the owner disappears. A transaction gets flagged. A payment needs explanation. A transfer doesn't make sense. Then the month stays open longer than it should.

Quick answers from the owner keep bookkeeping efficient. Slow answers turn simple close work into detective work.

Use the tools you already have better

If you're on QuickBooks Online, Xero, Gusto, Bill, or another common platform, make sure the setup is sensible. The goal isn't fancy automation for its own sake. It's reducing repetitive manual work and improving review.

For a useful owner-level refresher, even outside our region, this practical roundup of bookkeeping advice for San Diego businesses covers habits that apply almost anywhere.

Buy the right level of service

Some businesses overpay because they buy controller-style review when they only need solid monthly bookkeeping. Others underbuy and end up paying for cleanup later.

A better move is to match service level to need. If you're sorting through that decision, these advantages of outsourcing bookkeeping services lay out where outsourced support tends to make financial sense.

Choosing the Right Bookkeeping Partner in Philadelphia

Price matters. Fit matters more.

A Philadelphia-area business needs a bookkeeper who understands how local owners operate. A Center City professional firm doesn't run like a Chester County contractor. A healthcare practice in the suburbs has different reporting pressure than a solo consultant who mostly needs clean books and clear tax-ready records.

Questions worth asking before you sign

Don't settle for vague promises. Ask direct questions.

- Local experience: Do they understand Philadelphia and suburban business realities, including common local tax and reporting headaches?

- Industry fit: Have they worked with firms like yours in professional services, healthcare, or construction?

- Software comfort: Can they work inside QuickBooks, Xero, payroll systems, and the apps you already use?

- Communication style: Will they answer questions in plain English, or bury you in accounting language?

- Scope clarity: What is included every month, and what triggers extra fees?

What a strong bookkeeping partner should feel like

You shouldn't feel confused after talking to your bookkeeper. You should feel calmer. You should know what happened in the business last month and what needs attention next.

That means looking beyond price sheets and asking whether the provider can help you make decisions, not just reconcile accounts. It also means choosing someone who can grow with you if your needs shift from basic monthly bookkeeping toward reporting, forecasting, or tighter cash flow management.

If you want a local angle on that hiring process, this guide to hiring a local bookkeeper in Philadelphia is a solid starting point.

The best bookkeeping relationship is usually pretty simple. Your books stay current. Reports make sense. Problems get surfaced early. You spend less time guessing and more time running the business.

If you're trying to figure out what your business should realistically budget for bookkeeping, MyOfficeOps works with Philadelphia and West Chester businesses in professional services, healthcare, construction, and other service industries. A practical first step is to talk through your current setup, what's messy, what's working, and what level of support you need each month.