You've probably done this before. You walk past a packed stockroom, a jammed supply closet, or a warehouse full of product and think, “We have plenty of stuff, so why does cash still feel tight?”

That tension is one of the most common problems I see. Owners assume inventory is a sign of strength. Sometimes it is. But a lot of the time, it's money sitting still.

That's why the inventory turnover ratio matters so much. It turns piles of products, parts, and supplies into a simple business question: How fast are you turning cash tied up in inventory back into usable cash? If you know that answer, you can make smarter calls about hiring, ordering, pricing, and growth. If you don't, you're guessing.

What Your Shelves Are Telling You About Your Cash

A full shelf looks safe. It feels like preparation. It feels like control.

But shelves don't pay payroll.

I've seen this play out in retail shops, contractors' yards, medical offices, and product businesses. The owner says sales are decent, customers are buying, and the business looks busy. Then they open the bank account and realize there's not enough room for a new hire, a marketing push, or a piece of equipment they need.

The problem isn't always revenue. The problem is often how long cash sits trapped in inventory before it comes back.

Inventory is cash wearing a costume

If you buy a pallet of materials, shelves of apparel, or a closet full of supplies, that money is no longer cash you can deploy elsewhere. It has changed form. It's now sitting in boxes, bins, or jobsite trailers.

That's why I tell owners to stop looking at inventory as “stuff” and start looking at it as stored money.

Practical rule: If inventory keeps growing faster than your ability to turn it into sales, your business will feel busier without feeling richer.

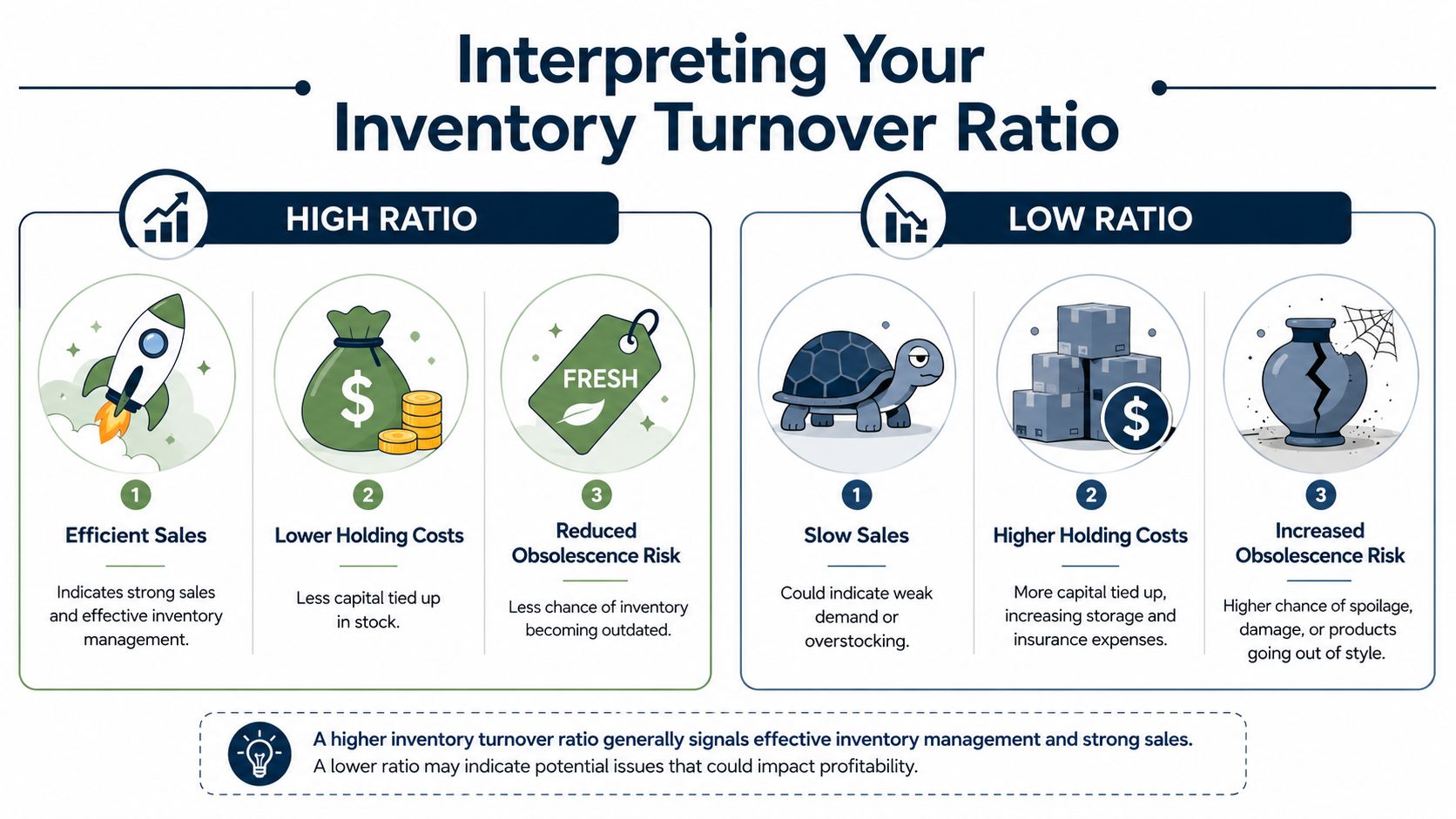

The inventory turnover ratio gives you a clean read on that issue. It tells you whether inventory is moving with purpose or just taking up space. A strong ratio usually means your business is converting stock into sales efficiently. A weak ratio often means cash is getting stuck.

Why this number matters beyond the warehouse

This isn't just an operations metric. It affects decisions far outside the stockroom.

- Hiring decisions: Slow-moving inventory can drain the cash you need for payroll.

- Growth investments: Money tied up in stock can't fund marketing, systems, or equipment.

- Borrowing needs: Owners often take on debt to solve a problem caused by too much inventory.

- Pricing pressure: Old stock often forces markdowns or rushed selling.

You don't need a finance degree to use this number. You just need to read it the right way. It acts as your business's pulse on inventory discipline. If it's sluggish, cash flow usually feels sluggish too.

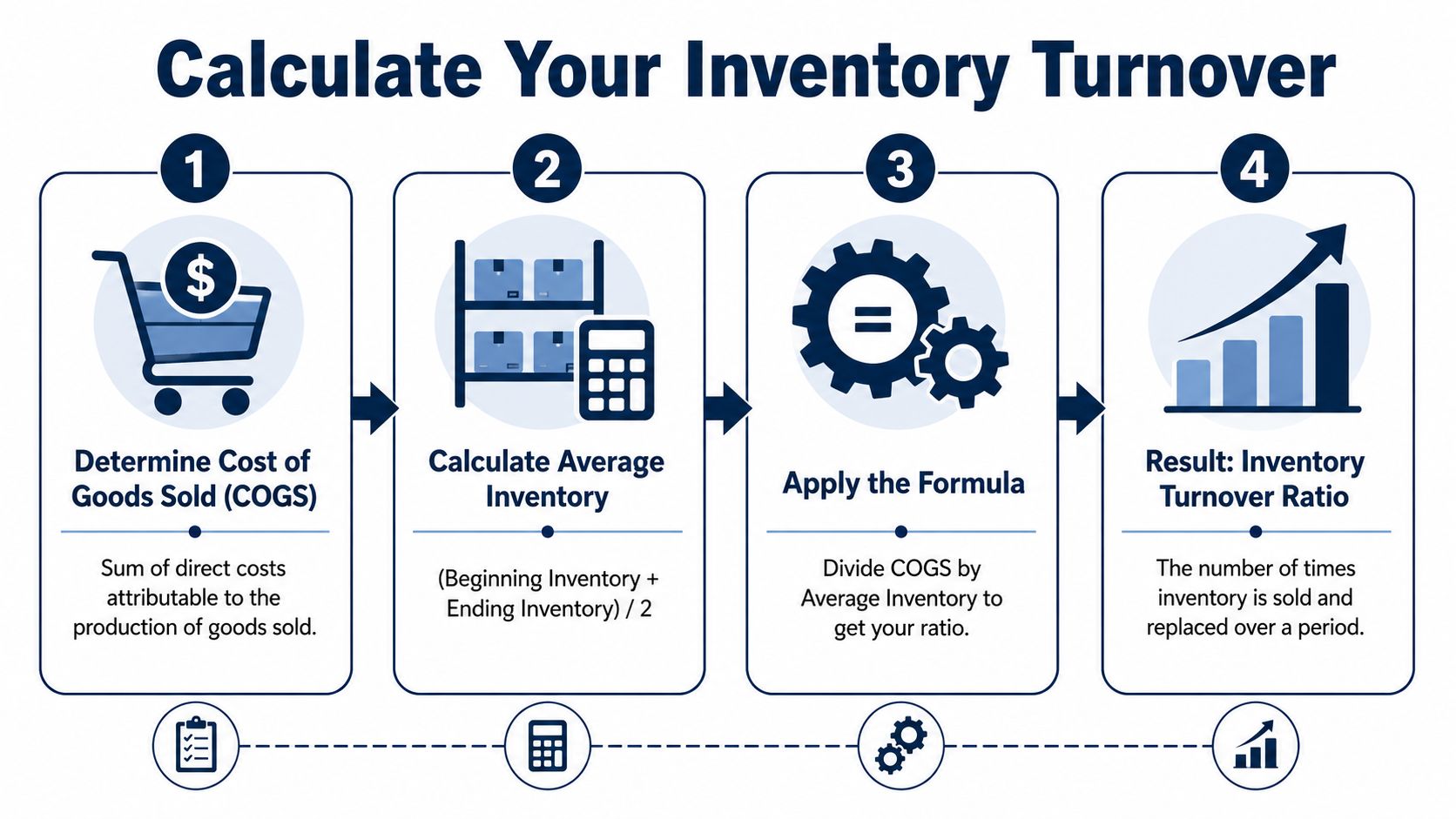

How to Calculate Your Inventory Turnover Ratio

Calculating the inventory turnover ratio requires two figures from your financial statements: COGS and average inventory.

The formula is inventory turnover ratio = COGS ÷ average inventory. Average inventory is usually (beginning inventory + ending inventory) ÷ 2. If you want to translate that into time, convert it to days on hand with 365 ÷ inventory turnover ratio, a standard approach described by the Corporate Finance Institute in its inventory turnover ratio guide.

The plain-English version

This ratio answers one practical question. How many times did you sell through your inventory during the period?

You only need two numbers.

COGS

Pull this from your profit and loss statement. It is the direct cost tied to the products, materials, or items you sold.Average inventory

Pull beginning and ending inventory from your balance sheet, add them together, and divide by two.Divide

COGS ÷ average inventory = inventory turnover ratio.

A quick example makes the point. Say a boutique has annual COGS of $600,000. It started the year with $80,000 in inventory and ended with $120,000. Average inventory is $100,000. Divide $600,000 by $100,000 and the turnover ratio is 6. That means the business sold through its average inventory six times during the year.

That number should drive decisions. A ratio of 6 means cash tied up in inventory cycled back into the business about six times. If that number drops, hiring gets tighter, purchase plans get riskier, and growth starts depending on borrowed money instead of operating cash.

Good math starts with clean books. If inventory is misstated, turnover gives you false confidence.

If you sell online, category-level analysis matters more than the companywide average. This practical guide on optimizing inventory for online sellers is useful because e-commerce businesses often have a few fast movers covering up a long tail of slow stock.

If your records are messy, fix that first. This guide to inventory accounting methods and reporting will help you clean up the numbers behind the ratio.

This same logic applies even if you do not run a classic warehouse business. A contractor can calculate turnover on core materials. A medical practice can track supplies and high-value consumables. A service firm can apply the same discipline to prepaid materials, stocked parts, or packaged client deliverables. The label matters less than the cash.

What a Good Inventory Turnover Ratio Looks Like

There is no single magic number for every business. Use benchmarks as a starting point, then judge the ratio by what it does to your cash, service levels, and growth plans.

A practical baseline for many product businesses is somewhere in the middle, not too slow and not so tight that one supply delay causes missed sales. Analysts at Netstock found manufacturing SMBs averaged about 5.3 turns annually in their inventory turnover by industry analysis. That works out to roughly 69 days of inventory on hand. For some businesses, that is disciplined. For others, it is sluggish.

Benchmarks help. Your business model decides what “good” means.

Use this table as a reference point, not a target you chase blindly.

| Industry | Typical Annual Turnover Ratio |

|---|---|

| Many stocked-product businesses | Often falls in the mid-single to higher-single digits |

| Manufacturing SMBs | Around 5.3 turns annually |

The right ratio depends on what you sell, how predictable demand is, how long lead times run, and how expensive stockouts are. A distributor with repeat demand can usually run leaner than a custom fabricator. A medical practice may accept slower turns on critical supplies because running out is unacceptable. A contractor may need deeper inventory on core materials during peak season to keep crews working.

That is the point. Good turnover supports the business model. It does not fight it.

High is only good if operations stay stable

A higher ratio usually means less cash is sitting on shelves. That gives you more room to hire, market, buy equipment, or build a cash buffer. If you want to improve those options, focus on the broader discipline of working capital management, because inventory is one of the biggest places cash gets stuck.

But a high ratio can also mean you are cutting inventory too close. Then the business pays somewhere else. Customer orders get delayed. Jobs pause while materials are rushed in. Staff wastes time chasing shortages instead of serving customers. Read more about the true cost savings with inventory automation if you are relying on manual processes and gut feel to manage that balance.

A low ratio usually points to one of three problems:

- You bought ahead of real demand

- Sales slowed and purchasing did not adjust

- Too much capital is trapped in stale or low-priority items

Read the ratio like an operator

Do not ask, “Is this good?” Ask, “What is this number forcing me to do with cash?”

If turnover is weak, hiring gets tighter because money is sitting in stock instead of payroll. If turnover improves, you can often fund growth internally instead of leaning on a credit line. That matters just as much for non-traditional inventory businesses. A service firm may be carrying stocked parts, prepaid materials, or bundled client deliverables. A healthcare practice may be tying up cash in consumables and specialty supplies. A construction company may have money buried in materials spread across jobs and storage yards.

The ratio is useful because it turns all of that into a management decision. Keep the inventory that protects revenue. Cut the inventory that only makes you feel prepared.

How Turnover Impacts Your Cash Flow and Profit

You feel turnover in your checking account before you see it on a report.

A shelf full of slow stock, a supply closet packed with items you may not use this quarter, or materials sitting across job sites all create the same problem. Cash is tied up in things that are not producing revenue yet. That limits what you can do next. It can delay a hire, postpone equipment purchases, force you to use a credit line, or make growth feel harder than it should.

Slow turnover drains the business

Slow-moving inventory creates costs from several directions at once:

- Cash gets stuck: Money sitting in products, supplies, or materials cannot cover payroll, taxes, rent, debt, or sales efforts.

- Overhead keeps running: You still pay for storage, handling, insurance, counting, and reordering.

- Loss risk goes up: Items get damaged, expire, go out of date, or disappear into write-downs and discounts.

- Margin gets thinner: The longer stock sits, the more likely you are to mark it down or absorb waste.

This is a working capital issue first. Profit matters, but cash decides whether you can act. If turnover improves, you need less money tied up to support the same sales volume. That gives you room to hire sooner, buy smarter, and fund growth with your own operations. If you want the broader playbook, review how to improve working capital and treat turnover as one of the fastest ways to strengthen it.

Higher turnover helps, until it starts hurting service

Some owners push this ratio too hard and create a different problem. They run so lean that one supplier delay, one spike in demand, or one missed reorder turns into late jobs, rush freight, and frustrated customers.

Allianz Trade makes the point clearly in their inventory turnover overview. A higher ratio does not automatically mean the business is healthier if you are creating stockouts or cutting margin to move product faster.

Use the ratio to support decisions, not to win a math contest.

A healthy turnover rate means you are carrying enough inventory to protect revenue and not enough to choke cash flow. For a retailer, that may mean fewer stale SKUs. For a healthcare practice, it may mean tighter control of consumables and specialty supplies. For a construction company, it may mean buying materials in line with job schedules instead of letting cash sit in yards and trailers. For a service firm, it may mean managing stocked parts, prepaid client materials, or bundled deliverables with the same discipline as a warehouse.

If your turnover is weak because the process is weak, fix the process. Better tracking, cleaner reorder points, and fewer manual mistakes usually beat bigger purchases. This breakdown of true cost savings with inventory automation is useful if you are evaluating systems that can reduce overordering and help inventory move with demand.

The goal is simple. Keep the inventory that protects sales. Cut the inventory that blocks cash.

Practical Ways to Improve Your Turnover

You don't improve inventory turnover ratio by staring at reports. You improve it by changing buying, stocking, and selling behavior.

Most businesses don't need a heroic overhaul. They need a tighter routine.

Start with the items that matter most

Not all inventory deserves equal attention. Some items carry the business. Others just take up room.

Use a simple product ranking approach. Identify the products, materials, or SKUs that sell consistently and produce strong margin. Protect those. Then identify the slow movers that sit for too long and need a decision.

That decision is usually one of these:

- Keep less of it

- Bundle it

- Promote it

- Discontinue it

Tighten the buying process

A lot of inventory problems start in purchasing, not sales.

Here are the moves I recommend first:

- Order smaller, more often: Big buys feel efficient but often create dead stock.

- Review supplier terms: Better reorder flexibility is often more valuable than a tiny price break.

- Use actual sales history: Stop buying from gut feel alone.

- Set reorder points carefully: Don't let one emergency stockout push you into permanent overbuying.

If your buyers are rewarded for “never running out” but not for controlling cash, inventory will swell.

Use targeted cleanup tactics

You don't need to wait for year-end to deal with stale inventory.

Try practical cleanup actions:

Run a slow-mover report

Pull items that haven't moved in a meaningful period for your business.Create bundles

Pair sluggish items with products customers already want.Use selective discounts

Don't slash prices blindly. Move stock with a purpose.Fix visibility

Sometimes products don't move because customers or sales reps don't notice them.

Improve the operating system behind the shelves

Good turnover comes from good process. Forecasting, reordering discipline, and clean data matter more than clever slogans.

If you're evaluating systems, this guide to Odoo ERP inventory management is a helpful example of how businesses use software to tighten purchasing and stock control without making everything more complicated.

My blunt advice is this: don't try to optimize every item at once. Pick the product lines that hold the most cash. Fix those first. That's where you'll feel the biggest relief.

Turnover for Service Healthcare and Construction Firms

A lot of owners hear “inventory turnover ratio” and think, “That's for warehouses, not for me.”

Wrong.

The principle applies anywhere money gets tied up before it turns into revenue.

Service firms

If you run a law firm, agency, IT company, or consulting business, your inventory usually isn't sitting on shelves. It's sitting in unbilled work-in-progress, prepaid software seats, and underused staff time.

Your version of turnover is simple. How quickly does work turn into invoices, and how quickly do invoices turn into cash?

Ask yourself:

- How much work is done but not billed yet

- How long are projects sitting before invoicing

- Are you carrying payroll faster than you're converting work into cash

If you want a broader view of how these patterns show up in the numbers, these cash flow analysis examples for operating businesses are useful.

Healthcare practices

In healthcare, supplies, pharmaceuticals, and specialty items can tie up a lot of cash. The pain gets worse when products expire, usage shifts, or purchasing happens in bulk without tight tracking.

The fix is operational discipline. Watch what gets used consistently, what gets wasted, and what sits too long.

Construction and trades

Construction companies often hide inventory in plain sight. Lumber, fixtures, conduit, tools, and job materials can sit in yards, vans, or jobsites for weeks. Sometimes longer.

That ties up cash and muddies job profitability.

For contractors, turnover questions should sound like this:

- Did we buy materials too early

- What stock is sitting across open jobs

- What was purchased for one project and never billed correctly

- Are field teams returning unused materials, or are they disappearing into the next job

If you don't sell products, track whatever behaves like inventory. That's where your cash is hiding.

The label matters less than the behavior. If money goes in and takes too long to come back out, you have an inventory turnover problem.

If you want help turning numbers like inventory turnover into decisions you can use, MyOfficeOps works with small and midsize businesses that need clear bookkeeping, better cash visibility, and practical CFO guidance. If your shelves, supplies, WIP, or job materials are eating cash, they can help you spot the leaks and make smarter calls on purchasing, pricing, hiring, and growth.