Inventory accounting is the simple process of tracking the cost of the products and materials you sell so you can figure out your real profit. The basic math is Beginning Inventory + Purchases − Ending Inventory = COGS, and that number flows straight into gross profit, which is why even small mistakes can throw off your books.

A lot of owners learn this the hard way. Sales look solid, money is coming in, and the business seems busy. But the bank balance feels tight, margins look strange, and nobody can answer a basic question with confidence: Am I really making money on the stuff I sell?

If you run a trade business, a clinic, or a service company that also buys and uses products, this shows up fast. A contractor buys materials for several jobs and has leftovers sitting in a trailer. A healthcare practice orders supplies in bulk, then finds expired items months later. A service firm resells equipment or software-related hardware but records purchases inconsistently. Revenue gets recorded. Inventory gets ignored. Profit gets distorted.

That's what what is inventory accounting really comes down to. It's not an academic exercise. It's the system that tells you what you sold, what it cost you, what's still sitting on the shelf, and whether your reported profit is real.

Why Your Sales Numbers Don't Tell the Whole Story

Friday afternoon. Jobs are wrapped up, invoices have gone out, and the sales report looks strong. Then you check the bank balance and wonder why it still feels tight.

That gap usually comes down to timing and tracking.

A contractor might buy lumber, fittings, and fasteners for three jobs in April, use part of it in May, and leave the rest in a truck or storage unit. A clinic may order supplies in bulk, use them over several months, and throw some out when they expire. A service company that also sells equipment can bill the client this week even though the related product costs were recorded at the wrong time. Revenue shows up fast. The true cost often does not.

Revenue is not profit

Sales tell you what you billed. They do not tell you what it cost to deliver that work or sell that product.

Inventory accounting separates those two pieces. Items you bought are recorded as an asset until they are sold or used. Then the cost moves into cost of goods sold, or COGS, so your books show the revenue and the related cost in the same period.

That matters for one reason. It changes whether your gross profit is real or just flattering you for a month.

Here's the practical version:

- Sales show what you charged customers

- COGS shows what the sold items or used materials cost

- Gross profit shows what is left to cover payroll, rent, software, vehicles, and admin

If inventory is off, gross profit is off. If gross profit is off, pricing decisions, hiring plans, and cash expectations get shaky fast.

Where this breaks in real businesses

In my experience, owners usually understand the basic idea quickly. The trouble starts in the day-to-day mess of running the business.

A few patterns show up over and over:

- Materials get used without being recorded: Parts leave the shelf, van, or supply closet, but nobody logs them to a job or patient service.

- Purchases hit expense instead of inventory: The month looks worse upfront, then later months look stronger than they really are.

- Old or unusable stock stays on the books: Damaged, expired, or obsolete items still sit there at full value, making the balance sheet look healthier than reality.

Those errors do more than distort reports. They tie up cash.

Inventory is money you already spent. If it sits too long, gets lost, expires, or never gets assigned correctly, your business pays for it twice. Once when you buy it, and again when bad numbers lead to weak decisions. That is one reason many owners outgrow spreadsheets and start looking for accounting software for small business with inventory that can track quantities and costs with less cleanup at month-end.

If you have ever said, “Sales were good, so why didn't we feel it?” this is usually the missing piece.

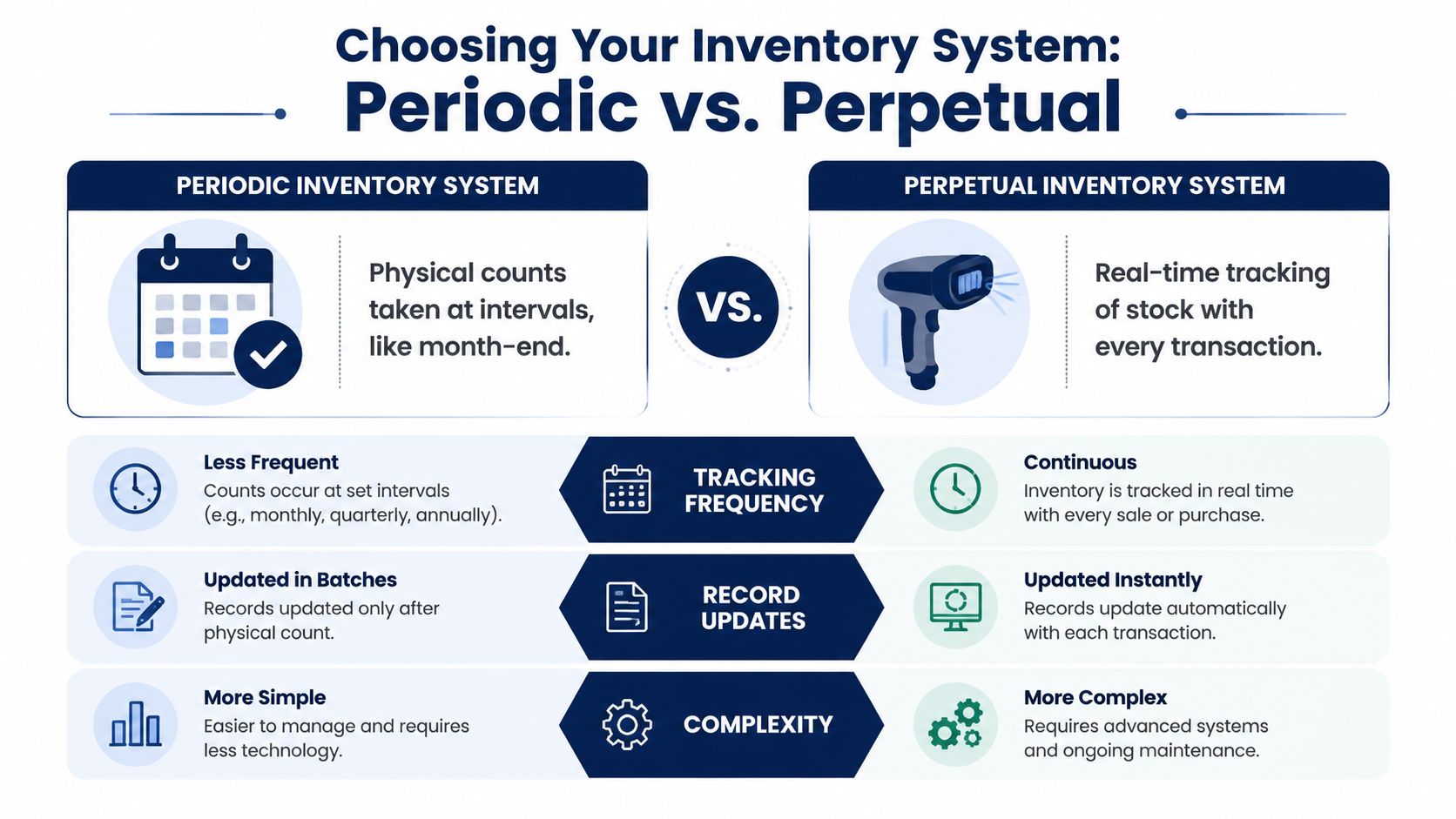

Choosing Your System Periodic vs Perpetual

There are two basic ways to track inventory: periodic and perpetual.

One is like checking your pantry once in a while. The other is like having every item scanned in and out as it moves. Both can work. The right choice depends on how fast inventory moves, how many items you carry, and how much accuracy you need during the month.

Periodic is count then adjust

A periodic system means you update inventory at set times, often at month-end or year-end, based on a physical count.

Performing a full grocery check at the end of the month is a good comparison. Until you stop and count everything, you don't really know what's left.

That can be fine for a smaller business with fewer items and slower movement. A small office that resells a limited number of standard products may be able to keep up this way. So might a contractor with a narrow list of stocked materials.

Periodic works best when:

- You carry a small number of items: Fewer moving parts means fewer surprises.

- Inventory doesn't move constantly: If items come and go slowly, monthly counts may be enough.

- You can tolerate lag: You won't have real-time numbers between counts.

The downside is obvious. If something goes missing in week one, you may not catch it until week four.

Perpetual is update as you go

A perpetual system updates inventory every time something is bought, received, sold, or adjusted.

This is the smart-fridge version. Every movement gets recorded, so you always have a current count if the process is followed correctly.

For clinics, ecommerce sellers, distributors, and busy trades businesses, this is usually more useful. It gives better visibility and makes it easier to spot errors before month-end.

Perpetual works best when:

- Stock moves daily: Frequent activity makes real-time tracking more valuable.

- You need better purchasing decisions: Current counts help avoid overbuying or stockouts.

- You use software and scanners: The system only works if people record transactions as they happen.

A perpetual system is only as good as the discipline behind it. If inbound items aren't scanned and transactions are entered late, the software gives you faster bad data.

Which system fits your business

Here's the simplest way to choose:

| Business situation | Better fit |

|---|---|

| Few items, slower activity, simple process | Periodic |

| Many items, frequent movement, stronger controls needed | Perpetual |

For businesses trying to manage stock more tightly, the inventory turnover ratio becomes useful because it shows how fast inventory moves. That matters even more when retailers are holding about $1.43 in inventory for every $1 of sales, and days inventory outstanding has risen 8.3% over the past five years, as noted in Sage's inventory accounting guide.

If you're reviewing systems, it helps to compare tools built for this job. This guide to accounting software for small business with inventory is a good place to start.

How to Value the Inventory on Your Shelves

Once you know how you'll track inventory, the next question is how you'll value it.

Owners often hear terms like FIFO, LIFO, and weighted-average cost and tune out. The ideas are simpler than they sound. They're just different ways to decide which cost gets assigned to the items you sold.

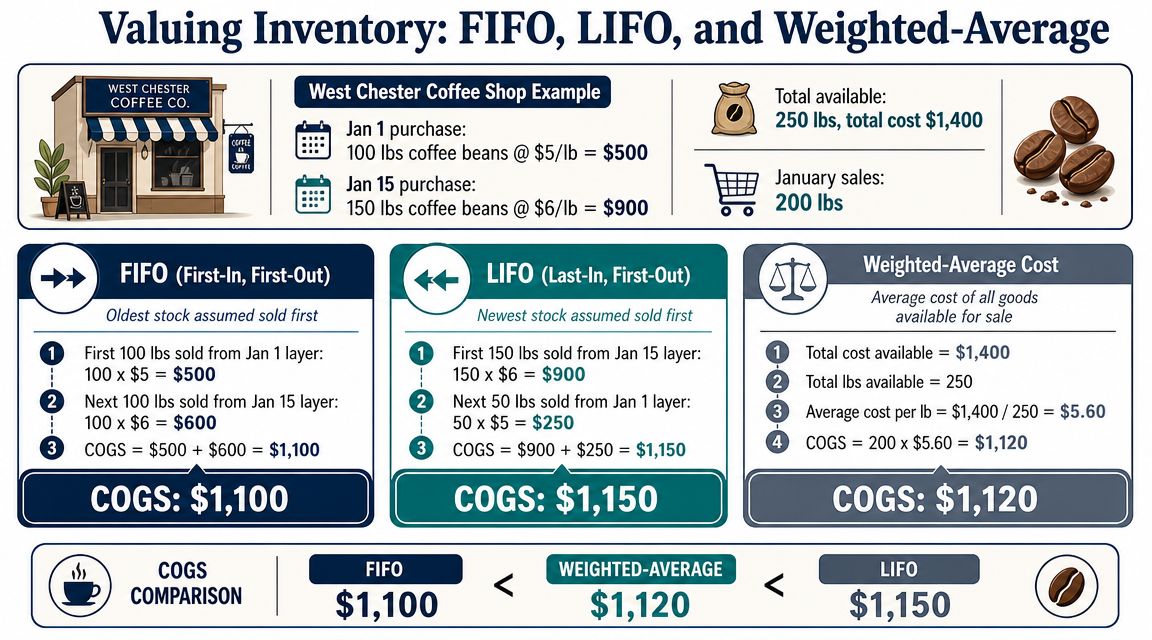

Use one example. A coffee shop buys the same beans at different prices over time. In one month, it buys beans at a lower cost. Later, the price goes up. When the shop sells coffee made from those beans, which cost should it use in COGS?

FIFO uses the oldest cost first

FIFO means first in, first out.

Under FIFO, you assume the oldest inventory gets sold first. In the coffee example, if older beans were bought at a lower price, those lower costs hit COGS first. Ending inventory reflects the newer, more recent costs.

This often makes sense because many businesses naturally use older stock first. Food, medical supplies, and many building materials often move that way.

FIFO is usually easier for owners to grasp because it follows a common-sense flow:

- Buy inventory

- Use or sell the oldest units first

- Leave newer units in ending inventory

LIFO uses the newest cost first

LIFO means last in, first out.

Under LIFO, the newest inventory costs go into COGS first. If prices are rising, that usually means higher COGS now and lower taxable income now. The trade-off is that ending inventory may reflect older costs that no longer look very current.

That's one reason method choice matters. The valuation method chosen materially affects reported profit and tax timing. Under LIFO, the most recent costs hit COGS first, which can reduce taxable income during periods of rising prices, though it may require a formal tax election in the U.S., according to MJCPA's review of inventory accounting.

For many small businesses, LIFO isn't the first place to start. It can be useful, but it adds complexity and should line up with tax and reporting advice.

Weighted-average smooths the swings

Weighted-average cost blends your inventory costs together and uses an average cost per unit.

If the coffee shop bought beans at different prices, it doesn't try to track which exact batch was sold first. It spreads cost across the total pool and uses one average number.

This method can work well when:

- Items are interchangeable: One unit is basically the same as another.

- Prices change often: Averaging can smooth sharp swings.

- You want simpler costing: It avoids some of the batch-by-batch detail.

If your costs jump around a lot, your valuation method can change your reported margin even when your sales volume stays the same.

What works in practice

The best method is usually the one that matches how your business operates and can be applied consistently.

A few examples:

- A coffee shop or clinic may prefer FIFO because older stock is often used first.

- A contractor buying the same materials repeatedly may prefer weighted-average if exact batch tracking adds little value.

- A business thinking about LIFO should talk through the tax and reporting impact before making the election.

One more point that owners often miss: your inventory cost may include more than just the supplier's invoice price. Shipping, duties, and delivery terms can affect the total cost you should capture. If those terms are fuzzy, this plain-English guide on FOB Incoterms explained is worth reading because it helps clarify when cost responsibility shifts.

And if you want the plain version of how cost flows into profit, this short overview of what is cost of goods sold makes the accounting side easier to connect.

Connecting Inventory to Your Profit and Loss

At this point, inventory accounting stops being a shelf-counting exercise and starts showing up on your financial statements.

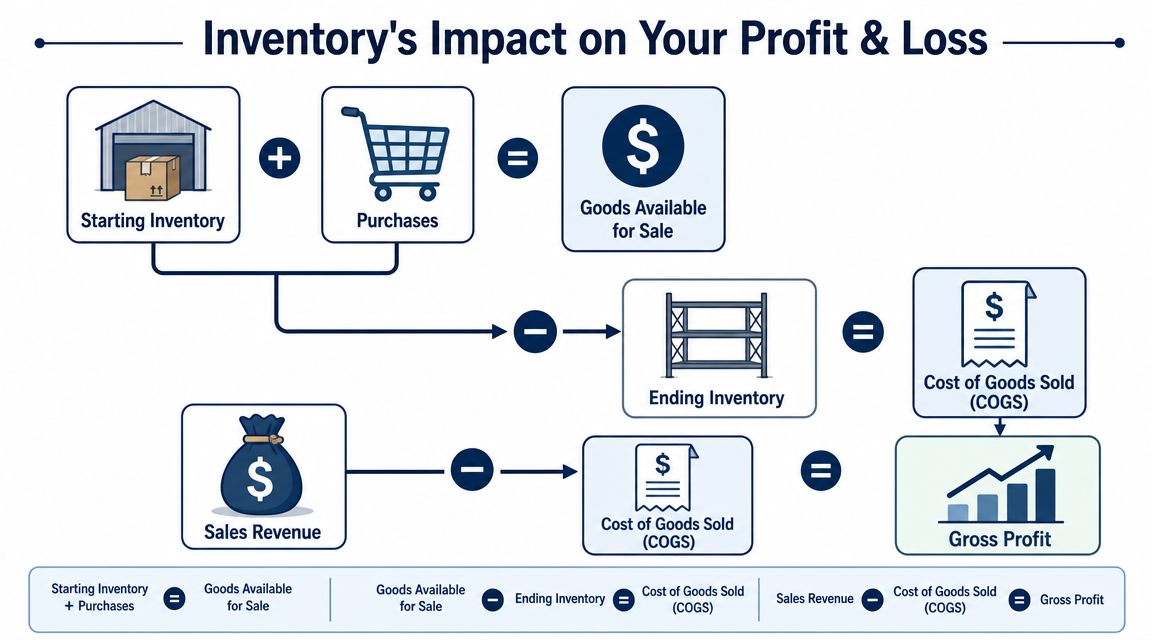

The core equation is simple: Beginning Inventory + Purchases − Ending Inventory = COGS. Then Sales − COGS = Gross Profit. Because this calculation directly affects gross profit, even small inventory valuation errors can distort taxable income and key performance indicators, as explained in Aurora Training Advantage's inventory accounting reference.

The basic flow

Here's what happens in plain English:

| Step | What it means |

|---|---|

| Beginning inventory | What you had at the start of the period |

| Plus purchases | What you bought during the period |

| Less ending inventory | What you still have left |

| Equals COGS | What was actually sold or used |

That COGS number lands on your profit and loss statement.

If ending inventory is too high, COGS looks too low, and profit looks better than reality. If ending inventory is too low, the opposite happens. That's why inventory mistakes create fake profit and fake panic, depending on which direction the error goes.

Why method choice changes the P&L

Go back to the coffee example.

If costs rose during the month, FIFO and LIFO won't give you the same COGS number. FIFO may show lower COGS and higher gross profit. LIFO may show higher COGS and lower gross profit. The coffee sold is the same. The sales price may be the same. Only the cost method changed.

That's the aha moment for most owners. Inventory accounting doesn't just track what's on the shelf. It helps determine the profit your financial statements report.

Your P&L can look healthy while your inventory records are weak. That doesn't make the margin real.

The journal entry side without the jargon

The bookkeeping behind this is straightforward.

When you buy inventory, it usually goes on the balance sheet as an asset. When you sell it, the cost moves off the balance sheet and into COGS on the income statement. At the same time, the sale itself gets recorded as revenue.

That's why one sale often creates two accounting effects:

- Revenue entry: You record the money earned from the sale

- Cost entry: You remove the inventory cost and record it in COGS

If you sell through channels like social commerce, it also helps to see how COGS is applied in those environments. This clear guide to COGS for TikTok Shop gives a useful operating view.

And if you want to see where gross profit sits in the bigger picture, this explanation of what is a profit and loss statement connects the dots.

Common Inventory Mistakes That Drain Your Cash

Most inventory problems don't start with a bad accounting method. They start with messy habits.

Owners often ask why their books, warehouse counts, and margins never match. For many small businesses, that gap comes from operational failures, especially when counts drift and transactions are mis-timed in manual processes, as described in Ramp's article on how inventory accounting works.

The mistakes that show up most often

You don't need a huge warehouse to have inventory trouble. A few common breakdowns can throw off the numbers fast.

- Counts happen too rarely: If nobody checks inventory except at year-end, problems sit for months.

- Receiving is sloppy: Items arrive, get used, but never get entered correctly.

- Shrinkage gets ignored: Loss from theft, breakage, or simple handling mistakes never gets recorded.

- Obsolete stock stays valued like new: Expired medical items, old parts, or dead product lines stay on the books too long.

- Materials are bought for one purpose and used for another: This is common in construction and job-based businesses.

A clinic may think supply costs are climbing when the underlying issue is expired stock. A contractor may think one job was profitable when materials were pulled from inventory but never assigned properly. A service business may keep buying replacement items because the records say stock is low when it's in a closet.

What good control looks like

Good inventory control is boring in the best way. It relies on repeatable habits.

A practical setup usually includes:

- Clean receiving: Someone checks what arrived against what was ordered and enters it the same day.

- Regular cycle counts: You count smaller groups of items throughout the month instead of waiting for one giant count.

- Documented write-downs: Damaged, expired, or obsolete inventory gets reduced on the books promptly.

- Clear ownership: One person is responsible for the system, even if several people touch inventory.

If inventory leaves the shelf but not the system, your books are wrong. If it enters the system but never really arrived, your books are wrong too.

For retailers and product-based operators, it can help to compare your process to broader operating advice like these Reddog Consulting retail insights, especially around stock handling and ordering habits.

The cash flow part owners feel first

Inventory mistakes don't stay in the accounting file. They show up in cash.

Overbuying ties up money. Missed write-downs inflate profit. Bad counts lead to rushed reorders. Then owners wonder why they're paying vendors quickly while the shelf is full of slow-moving items.

That's why the fix isn't “count better” by itself. The fix is building a process where purchasing, receiving, usage, and accounting all tell the same story.

Turn Your Inventory Data into Smarter Decisions

A lot of owners look at sales first. I look at inventory next, because that is usually where the cash story gets clearer.

Reliable inventory records help you answer the questions that affect profit this month, not just at year-end. What needs to be reordered now? What has been sitting too long? Which items still sell well but no longer produce the margin you thought they did? Which jobs or service lines keep consuming materials without enough return?

The goal is not more reporting. The goal is better judgment.

A small set of inventory views usually gives business owners enough to act with confidence:

- Inventory turnover: Shows how quickly stock is turning into sales.

- Aging by item or category: Highlights products or supplies that are tying up cash for too long.

- Gross profit by product or job: Shows where margin holds up and where it slips.

- Purchasing patterns: Helps you catch overbuying, poor timing, and repeat ordering habits that create excess stock.

If these numbers live in spreadsheets, come from delayed counts, or depend on someone remembering to update them, decisions get slower and riskier. Owners start buying based on stress instead of evidence. That usually leads to two expensive outcomes. Too much money on the shelf, or not enough of the right items when customers need them.

I see this play out differently by industry, but the pattern is the same. A contractor keeps reordering common materials because no one trusts the count in the shop. A medical practice carries more supplies than it needs because nobody wants to risk running short, then finds expired items months later. A service business that resells parts or products sees revenue growing but still cannot explain why cash stays tight.

Better inventory data fixes those conversations. You can see whether margin pressure comes from rising costs, waste, slow-moving stock, poor pricing, or inconsistent purchasing. That matters because each problem needs a different response. Cutting purchases will not fix bad pricing. Raising prices will not fix expired stock. Buying earlier will not fix bad counts.

Keep it practical:

- Pick a system your team will keep current.

- Use one valuation method consistently.

- Match physical counts to the books on a regular schedule.

- Review inventory reports often enough to change purchasing, pricing, or usage before cash gets squeezed.

Clean inventory accounting helps you make calmer decisions. You buy with more discipline, price with better margins in mind, and spot problems while they are still small enough to fix.

If your inventory, margins, and cash flow never seem to line up, MyOfficeOps can help you clean up the process and make the numbers useful again. We work with small and midsize businesses that need clear books, better reporting, and practical guidance on profitability, not more accounting jargon.