If you've ever looked at a profit and loss statement and felt your eyes glaze over, you’re not the only one. But there’s one number on that report that tells a huge story about your business: Cost of Goods Sold (COGS).

Simply put, COGS is the direct cost of making the stuff you sell. Think of it like this: if you bake a cake, COGS is the cost of the flour, sugar, and eggs. It’s not the cost of the oven you used to bake it. Getting this number right is the first step to knowing if you're actually making money on each sale.

What Is Cost of Goods Sold In Simple Terms?

Let's skip the accounting talk. Imagine you run a coffee shop. Your Cost of Goods Sold is everything that went into the cup you just handed to a customer.

This includes things like:

- The coffee beans you ground for their espresso.

- The milk you steamed for their latte.

- The paper cup, sleeve, and lid they took with them.

These are direct costs. Without them, you literally couldn't have made the drink.

What COGS Is Not

It’s just as important to know what isn't part of COGS. These are your operating costs—the things you need to run the business, but they aren't tied to making one specific item.

For that same coffee shop, these costs are kept separate from COGS:

- The monthly rent for your shop.

- Your barista's salary.

- The power bill that keeps the lights on.

- The flyers you printed to advertise a new drink.

These are indirect costs. You have to pay them whether you sell one cup of coffee that day or one thousand. They're part of running the business, not making the product itself.

Key Takeaway: COGS includes only the direct costs tied to making what you sell. It’s the raw materials and direct labor needed to create your final product. Everything else is an operating expense.

Why Does This Matter?

Separating these costs is super important for any business owner. Once you know your COGS, you can figure out your gross profit—the money left over from sales before you pay for things like rent and marketing.

This one number tells you how profitable your main business activity really is. It’s the first building block for understanding your company's financial health.

Knowing your COGS helps you answer big questions like, "Are my prices high enough?" or "Are my material costs getting too high?" It gives you the information you need to make smarter decisions that help your business grow.

The COGS Formula Explained Step By Step

Alright, let's do the math. Don't worry, it's easier than it sounds. The official formula for the Cost of Goods Sold is something accountants use daily, but it's really just a logic puzzle.

The COGS Formula:

Beginning Inventory + Purchases – Ending Inventory = COGS

Think of it like this: You start the month with a pile of stuff to sell. You buy more stuff during the month. At the end of the month, you count what’s left. The stuff that's gone is what you sold. That’s it.

Breaking Down the Formula

This calculation has three parts, and each one tells a piece of your inventory’s story over a set time, like a month or a quarter.

Breaking Down the COGS Formula

Here’s a simple table to put each part of the Cost of Goods Sold formula into plain English.

| Component | What It Means In Simple Terms | Example (For a T-Shirt Shop) |

|---|---|---|

| Beginning Inventory | The value of all the products you had on hand, ready to sell, at the very start of the period. | The dollar value of all t-shirts in the stockroom on April 1st. |

| Purchases | The cost of all the new inventory you bought or made during that same period. This adds to your pile. | The total cost of all new t-shirts ordered from suppliers during April. |

| Ending Inventory | The value of all the products you have left unsold at the very end of the period. | The dollar value of all t-shirts left on the shelves on April 30th. |

When you add what you started with to what you bought, you get the total value of everything you could have sold. Then, you just subtract what you didn't sell (your ending inventory). What's left over is the direct cost of what you did sell. That’s your COGS.

A T-Shirt Shop Example

Let's make this real. Imagine you own a small t-shirt shop and you want to figure out your COGS for April.

First, you check your records. On April 1st, you had $2,000 worth of t-shirts in stock. This is your Beginning Inventory.

During April, you ordered more shirts from your supplier. The total cost of these new shirts, including shipping to your store, came to $5,000. These are your Purchases.

Now, let's add those together to see what you had available to sell:

$2,000 (Beginning Inventory) + $5,000 (Purchases) = $7,000

This $7,000 represents the total cost of all the shirts you could have sold during April.

On the night of April 30th, you count your stock. You find you have $3,000 worth of t-shirts left. This is your Ending Inventory.

Finally, you just plug that last number into the formula:

$7,000 (Goods Available for Sale) – $3,000 (Ending Inventory) = $4,000

And there you have it. Your Cost of Goods Sold for April is $4,000. This number tells you exactly what it cost you to get the shirts that your customers bought that month.

Of course, before you can use the COGS formula, categorizing business expenses correctly is key to make sure you're only including direct costs. Getting this simple calculation right is the foundation for understanding your profit.

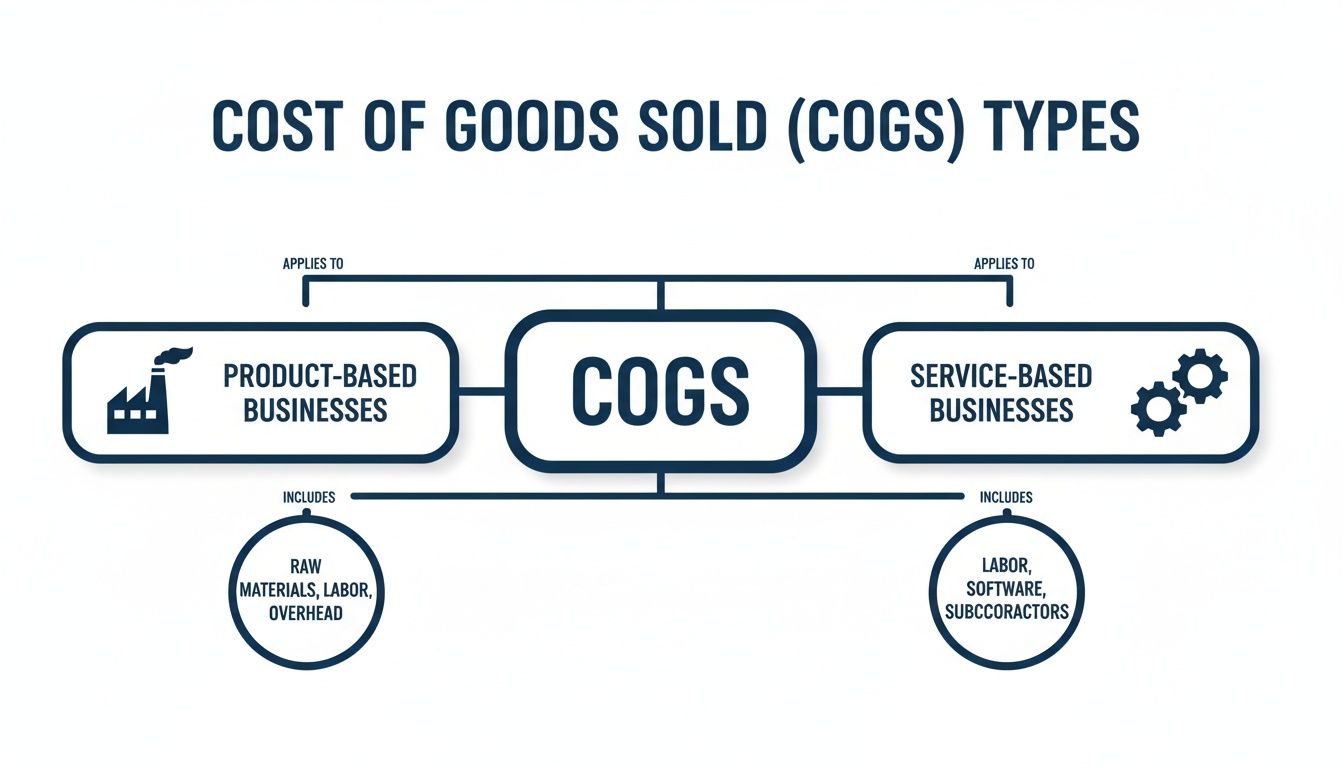

Calculating COGS for Different Business Types

The Cost of Goods Sold calculation isn’t the same for every business. The direct costs for a brewery making beer are very different from a marketing agency selling its services. Let's see how it works for each.

For Product-Based Businesses

If you sell a physical product—like beer, furniture, or clothes—your COGS is all about the direct costs of making that item.

Let's say you own a small brewery. To figure out the COGS for a keg of beer, you’d add up three main things:

- Direct Materials: These are the ingredients that go into the beer. Think hops, barley, yeast, and water. This also includes the cost of the keg itself.

- Direct Labor: This is what you pay the people who are actually brewing the beer. The salary of your head brewer and their assistants goes here.

- Manufacturing Overhead: This includes factory-related costs needed for production but not tied to a single keg. This would be things like the electricity used by the brewing tanks or wear-and-tear on your canning machine.

Add those three together, and you have a clear COGS for each keg. This number is the foundation for pricing that keg to make sure every sale is profitable.

For Service-Based Businesses

So, what about businesses that don't have a physical product? A marketing agency, an IT consultant, or an accounting firm sells time and expertise. They don’t have inventory on a shelf, so how do they calculate their direct costs?

Service businesses use a similar idea, but it usually goes by another name: Cost of Revenue or Cost of Services.

Think of it this way: Cost of Revenue is the service world's version of COGS. It includes all the direct costs needed to deliver the service a client paid for.

Let's say you run a marketing agency hired to manage a client's social media. Your Cost of Revenue for that project would include:

- Direct Labor: For most service businesses, this is the biggest piece. It’s the portion of the salaries for the team members who actually did the work—the social media manager, writer, and designer who spent time on that client's account.

- Direct Software Costs: Any software or tools that were needed to do that project would be included here. This could be a subscription to a social media scheduling tool used for that client’s work.

Notice what’s missing? The agency’s office rent, the salesperson’s commission, and the office manager's salary are all indirect costs. They're needed to run the business, but they aren't directly tied to delivering the service to that one client.

A construction company is another great example. For them, understanding the true cost of labor, materials, and equipment for each job is the difference between making money and losing it. To see how this works in detail, you can learn more about how job costing in the construction industry works. This helps contractors know exactly what each project costs them so they can price their services correctly.

How Inventory Methods Change Your COGS and Taxes

This is where COGS gets interesting—and directly affects your tax bill. How you value your inventory isn't just a small accounting detail; it’s a choice that can change your reported profit and how much you owe in taxes.

Let's look at the three main ways to track inventory costs. Think of it like a grocery store stocking milk.

The FIFO Method: First-In, First-Out

FIFO (First-In, First-Out) is the most common and simple way. It assumes the first items you buy are the first ones you sell.

Imagine your store gets a milk delivery on Monday for $2 per carton. On Wednesday, you get another delivery, but the price has gone up to $3 per carton. When a customer buys milk on Friday, FIFO assumes you sold one of the $2 cartons from Monday's delivery. The oldest inventory gets "sold" first.

This method makes sense and often matches how goods actually move, especially for things that can spoil. You obviously want to sell the oldest milk first.

The LIFO Method: Last-In, First-Out

LIFO (Last-In, First-Out) is the opposite. It assumes the last items you brought into inventory are the first ones to be sold.

Using our milk example, when that customer buys a carton on Friday, LIFO assumes you sold one of the newer, more expensive $3 cartons from Wednesday.

This might seem strange—why sell the newest milk first? While it doesn't usually match how products physically move, LIFO has a big financial advantage when prices are rising.

The Weighted Average Cost Method

The Weighted Average Cost method smooths everything out. Instead of tracking each purchase cost, you calculate an average cost for all the items you have in stock.

Let's say you have ten milk cartons that cost you $2 each and ten that cost you $3 each. You have 20 total cartons with a total cost of $50 ($20 + $30). Your weighted average cost is $2.50 per carton ($50 / 20 cartons). Every carton you sell is recorded at this average price.

This method is useful for businesses where individual items are hard to tell apart, like gallons of paint or bushels of grain.

This concept map breaks down the different types of direct costs that feed into your overall COGS calculation for either a product or a service.

The map shows how, no matter your business type, the main idea is to pull out the direct costs needed to deliver value to your customer.

Why Your Choice Matters for Taxes

So, which method is best? It depends on your goals and what's happening with prices. This choice is a big deal, especially when costs are rising—which is happening to a lot of businesses today.

Let's go back to our milk example during a time of rising prices:

- With FIFO: You "sold" the older, cheaper milk ($2). Your COGS is lower, your reported profit is higher, and you'll likely pay more in taxes.

- With LIFO: You "sold" the newer, more expensive milk ($3). Your COGS is higher, your reported profit is lower, and you'll likely pay less in taxes.

This isn't a small difference; it’s a tool you can use to manage your taxes. When costs are going up, LIFO can offer tax advantages by increasing your COGS and lowering your taxable income.

FIFO vs LIFO: How They Impact Your Profit

To see this in action, here is a simple side-by-side comparison when costs are rising.

| Method | How It Works | Impact on COGS | Impact on Profit and Taxes |

|---|---|---|---|

| FIFO | Assumes the first (oldest) inventory purchased is the first one sold. | Lower COGS, as older, cheaper costs are used first. | Higher reported profit, leading to a higher tax bill. |

| LIFO | Assumes the last (newest) inventory purchased is the first one sold. | Higher COGS, as more recent, expensive costs are used first. | Lower reported profit, leading to a lower tax bill. |

As you can see, the accounting method you choose directly affects how much profit you show on paper and, in turn, how much you pay in taxes.

However, you should know that LIFO is not allowed under international accounting standards (IFRS) and has stricter rules from the IRS in the U.S. Choosing an inventory method is a big decision you should definitely make with your accountant.

The recent economy has shown just how fast costs can change. In 2025, new tariffs caused prices to jump for businesses that import goods. Data from Yale's Budget Lab showed that core goods prices in the US climbed 1.9% above pre-2025 trends.

For a construction company buying materials from overseas, these price hikes mean COGS can grow almost overnight, making inventory choices more important than ever. You can read more about the effects of the 2025 tariffs on the Yale Budget Lab website.

The best method depends on your industry, inventory type, and financial strategy. The key is to pick one and stick with it so your financial reports are consistent.

Why COGS Is a Secret Weapon for Your Business Strategy

Most business owners see Cost of Goods Sold as just another number for their tax forms. But treating COGS this way is like having a powerful tool and only using it as a paperweight.

COGS is more than an accounting task. It's a strategic guide that helps you make smarter decisions. When you really understand your COGS, you see if your business is truly healthy. It tells you, straight up, if the core of your operation—making your product or delivering your service—is profitable.

Suddenly, a number on a spreadsheet becomes real-world business intelligence.

Using COGS to Perfect Your Pricing

How do you know if your prices are right? It’s a question that keeps owners up at night. Guessing is a bad idea, but COGS gives you a solid, data-backed starting point for your pricing.

Think about it: your price has to cover the direct cost of what you’re selling. If it doesn't, you’re losing money on every sale. By getting clear on your COGS, you set the absolute floor for your pricing.

This helps you answer key questions:

- Is the gap between my COGS and sale price big enough to cover my other costs like rent and salaries?

- After all costs are paid, is there a healthy profit left?

- If a supplier raises their prices, how much do I need to adjust my own prices to stay profitable?

Knowing these answers lets you set prices with confidence. A firm grasp of your costs is the first step in learning how to improve your gross profit margin and building a stronger business.

Spotting Trouble Before It Starts

Think of your COGS as an early-warning system for your business. When you track it regularly, you can see problems long before they become crises.

Is your COGS percentage slowly going up month after month? That’s a red flag. It’s a clear signal that your direct costs are rising faster than your sales, quietly eating away at your profit.

By watching this number, you can find trouble before it finds you. It tells you when it’s time to act, not when it’s too late.

Maybe a key material just got more expensive, or a problem in your production process is wasting resources. When you see COGS trending up, you know it’s time to dig in. You can start looking for new suppliers, negotiating better prices, or finding ways to operate more efficiently.

This is more important than ever in today's online world. For online sellers, COGS isn't just about materials; it's about shipping costs, surprise tariffs, and supply chains that can hurt your profits.

Global online retail sales are expected to hit $7.4 trillion by 2025. You can dig into more stats about the state of online retail on invespcro.com. For a small business trying to compete, mastering these costs is key to survival. By treating COGS as a strategic tool, you gain the edge you need to succeed.

Common COGS Mistakes and How to Avoid Them

Getting your COGS calculation right is important, but getting it wrong can cause real headaches. A wrong number can lead to paying too much in taxes, making bad pricing decisions, or thinking your business is more profitable than it is. It’s like trying to bake a cake with the wrong measurements—the result won't be what you expect.

Let's look at a few common mistakes business owners make and how you can avoid them.

Misplacing Expenses

The most common mistake is putting the wrong costs into the COGS bucket. It’s an easy slip-up. Remember, only direct costs belong here. When you include operating expenses, they inflate your COGS and make your business look less profitable.

A classic example is putting your marketing budget into COGS. While marketing helps you sell products, it isn't a direct cost of making one. That’s an operating expense, like office rent.

Here’s a quick checklist to help you separate them:

- Shipping-In Costs: The cost to get raw materials to you is part of COGS.

- Shipping-Out Costs: The cost to ship a finished product to a customer is a selling expense, not COGS.

- Salaries: Wages for factory workers who build the product are COGS. Salaries for your sales team or office staff are not.

Forgetting All the Direct Costs

On the other hand, some owners forget to include all the direct costs. This makes their COGS seem lower and their profit seem higher, which can be just as dangerous.

For example, a furniture maker might remember to include the cost of wood but forget the shipping fees to get that wood delivered. That shipping fee is a direct cost and belongs in the COGS calculation. Small mistakes like this add up.

Getting your Cost of Goods Sold right is the foundation of good financial reporting. It’s not just an accounting task; it’s a key piece of information that guides your strategy.

Inconsistent Tracking Methods

Another mistake is switching between inventory methods (like FIFO and LIFO) from year to year. While it might seem like a good idea to change methods to get a better tax outcome, the IRS requires you to be consistent. Pick one method that works for your business and stick with it. This is key for accurate financial planning.

To prevent common errors, it helps to review these essential small business bookkeeping tips. Building strong bookkeeping habits is your best defense against these mistakes.

A Few Lingering Questions About COGS

Even after breaking it all down, a few questions usually pop up. Here are some quick, simple answers to the most common ones.

Can a Business Have Zero COGS?

Yes, it's possible, but it’s pretty rare. A pure service business that has no direct costs tied to delivering its service might have zero COGS.

For example, think of a solo consultant who only sells their advice. If they aren't using any paid software or hiring contractors, they might not have any direct costs to report. However, most service businesses have at least some Cost of Revenue, which is the service world’s version of COGS.

Does COGS Include Marketing Costs?

Nope. This is a common point of confusion, but the answer is a firm no. Marketing and advertising costs are not part of COGS.

Think of it this way: COGS includes the costs to create the product. Marketing costs are what you spend to sell the product. They are an operating expense and get their own line on your income statement.

What Is the Difference Between COGS and Operating Expenses?

This is probably the most important distinction to get right. COGS covers the direct costs of making what you sell, while operating expenses (OpEx) are the costs of simply running the business.

- COGS: These are your direct costs, like raw materials and wages for production workers. Without these expenses, the product couldn't be made.

- Operating Expenses: These are your indirect costs—think rent, marketing, and the office power bill. You pay these whether you sell one item or a thousand.

Separating these two is a must. It’s how you calculate your gross profit, which tells you if your core business is profitable before you pay for all your overhead.

How Often Should I Calculate COGS?

You should calculate your Cost of Goods Sold for every reporting period. For most small businesses, that means doing it monthly and quarterly.

Calculating COGS regularly gives you a real-time pulse on your business's financial health. It helps you spot rising material costs, track profit, and make smarter pricing decisions before it's too late. Waiting until the end of the year can be a problem; by then, small issues can become big ones. Staying on top of this number is key to managing your business well.

Understanding and accurately tracking your Cost of Goods Sold is fundamental to building a profitable business. But as a busy owner, you don’t have to manage it all alone. The team at MyOfficeOps provides expert bookkeeping and financial guidance to help you get your numbers right, so you can focus on strategy and growth. Schedule a call with us today and let's get your COGS under control.