Tax season usually hits small business owners the same way every year. You're closing the books, chasing year-end invoices, and staring at a folder full of mortgage statements, charity receipts, property tax bills, and medical paperwork. Then the question shows up again: should you take the standard deduction or itemize?

This isn't just a tax form choice. It's a money decision. One path is fast and clean. The other can save more, but only if the numbers justify the extra work.

Most generic tax articles make this sound harder than it is. They drown you in IRS language and leave out the traps that cost people money. If you own a business, that's a problem. You don't need theory. You need a clear answer that protects your bottom line.

Your Annual Tax Season Dilemma

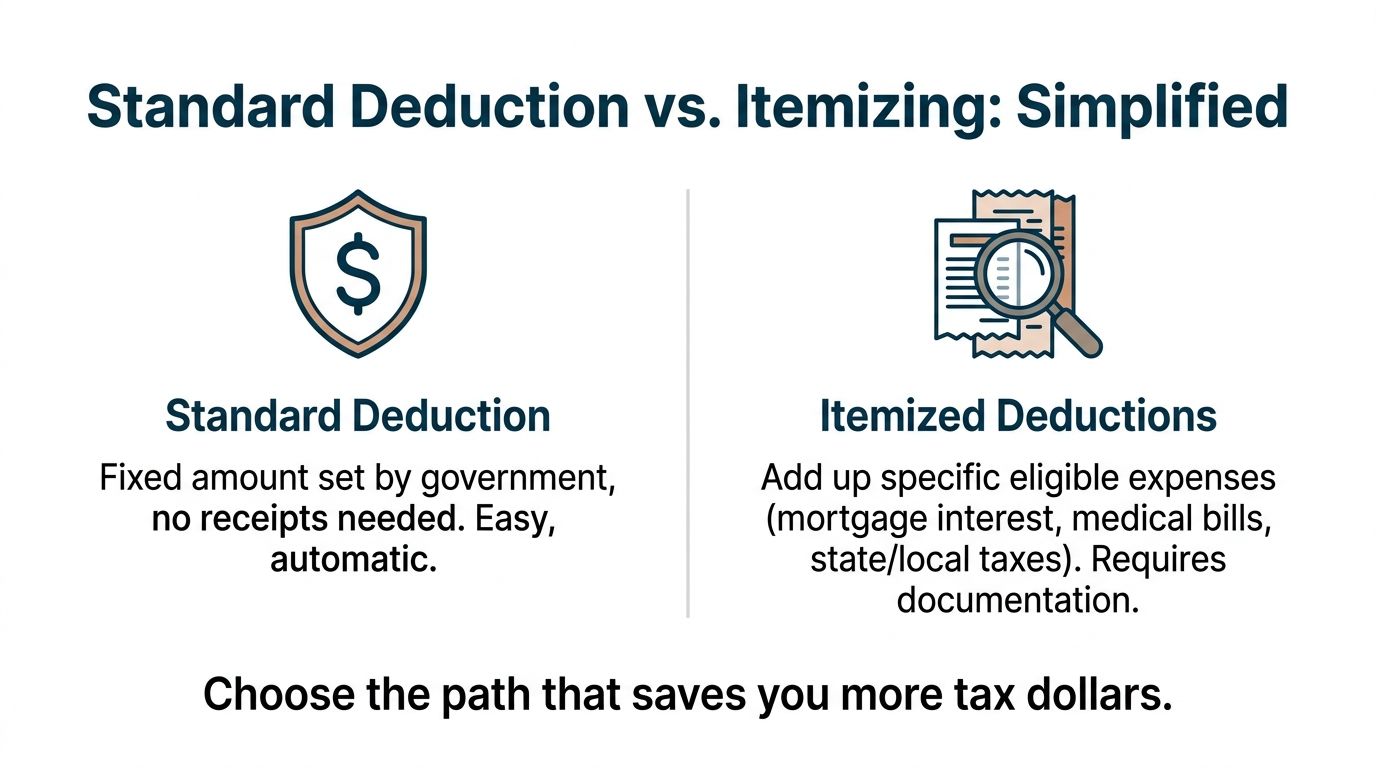

If you're like most owners, your year-end tax prep starts with two piles. One pile is simple. It's your standard deduction. You take the fixed amount and move on.

The other pile is messy. That's itemizing. You gather specific deductible expenses, add them up, and hope the total beats the fixed amount.

That's the standard deduction vs itemizing decision. It's not mysterious. It's a side-by-side comparison between an automatic discount and a custom-built one.

Why this matters to business owners

As a business owner, you already track business deductions all year. That can create a false sense of confidence on the personal side. People assume that because they run payroll, manage expenses, or use QuickBooks, they should probably itemize too.

That's not how this works.

Your personal tax deduction choice depends on whether your eligible personal itemized deductions are strong enough to beat the standard amount for your filing status. If they don't, itemizing is just extra paperwork with no payoff.

Practical rule: Don't itemize because you have receipts. Itemize only because the receipts save you more than the standard deduction.

Start with a clean process

Before you make the call, get organized. Pull your mortgage interest forms, property tax records, charitable donation receipts, and medical expense documentation. If your books are behind, fix that first. A messy close leads to sloppy tax decisions.

A simple tax season preparation checklist for business owners can help you gather what matters without wasting time on papers that won't affect the outcome.

Here's the short version of the decision:

| Option | How it works | Best for | Main downside |

|---|---|---|---|

| Standard deduction | Fixed amount based on filing status | Owners who want speed and simplicity | You might leave money on the table if your eligible expenses are high |

| Itemizing | Add up specific eligible deductions | Owners with large deductible personal expenses | More paperwork, more recordkeeping, more room for mistakes |

If you remember one thing, remember this. The smartest choice isn't the more complicated one. It's the one that leaves you with the lower tax bill after factoring in the hassle.

The Two Paths Explained Simply

You have two lanes on your personal return, and one of them is usually a waste of time for business owners.

The standard deduction is the flat amount the IRS lets you subtract based on filing status. No item-by-item tally. No stack of personal receipts. You claim it and keep moving.

Itemizing means you add up specific personal deductions one by one, then use that total instead of the standard deduction if it gives you a better result. That sounds simple, but here is where owners get sloppy. They mix business write-offs with personal itemized deductions and end up comparing the wrong numbers.

What the standard deduction means in real life

For 2026, the federal standard deduction for Single filers and Married Filing Separately is $16,100, while Married Filing Jointly is $32,200.

For 2025, the standard deduction is $15,750 for single filers and married couples filing separately, $31,500 for married couples filing jointly, and $23,625 for heads of household, based on H&R Block's 2025 standard deduction summary.

Those numbers are the hurdle. If your itemized deductions do not clear it, itemizing does nothing for your bottom line.

One trap deserves extra attention. Married Filing Separately is not a casual choice. If one spouse itemizes, the other spouse must itemize too, even if the standard deduction would have been better for them. The IRS explains that rule in its instructions for Schedule A. Business owners who file separately for liability, student loan, or cash-flow reasons miss this all the time and pay for it.

What counts if you itemize

Itemized deductions usually come from a short list of personal expenses:

- Mortgage interest on a qualifying home loan

- State and local taxes, subject to the $10,000 SALT cap

- Charitable contributions

- Certain medical expenses that meet IRS limits

That is a personal tax list, not a business deduction list.

Your equipment, software, contractor payments, mileage, and home office deduction belong on the business side of the return. They do not help you decide between standard deduction and itemizing. If you need a clean separation, use this small business tax deductions list and keep your business write-offs out of the personal deduction conversation.

The business-owner version of the decision

Use a blunt test.

If you do not have sizeable mortgage interest, a full SALT cap, meaningful charitable giving, or an unusually expensive medical year, the standard deduction is usually the right move.

If you are a higher-income owner, do not assume itemizing will win just because you earn more. Income does not create itemized deductions. Large eligible personal expenses do. The break-even point is simple. Your itemized total has to beat your standard deduction by enough to justify the recordkeeping, error risk, and time cost.

My advice is straightforward. Start with the standard deduction as your default. Switch to itemizing only when your personal numbers clearly top it, and make sure you are not dragging business expenses into the wrong bucket.

When Does Itemizing Actually Make Sense

You sit down to finish your return, add up a few deductions, and start convincing yourself itemizing should win because you own a home and pay plenty in taxes. That is where business owners lose time. Itemizing only makes sense when your personal deductions beat the standard deduction by a clear margin and produce savings worth the paperwork.

The expenses that move the needle

A handful of categories usually decide this. Small deductions rarely do.

- Mortgage interest is often the biggest driver, especially if you bought more recently and your interest costs are still high.

- State and local taxes help, but only up to the $10,000 SALT cap. If you are a high earner in a high-tax state, this is one of the biggest traps. Many owners assume their tax bill will carry them over the line. The cap shuts that down fast.

- Charitable contributions can tip the scales if your giving is consistent and documented.

- Medical expenses matter in expensive years, but only the qualifying portion counts, so do not overestimate this bucket.

The break-even point is not your income level. It is the moment your itemized total gets far enough past the standard deduction to justify the extra work and audit risk.

Run the break-even test like an owner

Use a simple table and make the call based on dollars, not instinct.

| Deduction method | What you compare | Decision rule |

|---|---|---|

| Standard deduction | Fixed amount for your filing status | Use it if your itemized total is lower or barely higher |

| Itemizing | Total of eligible personal deductions | Use it only if the tax savings are clearly better |

Do the math in this order:

- Total your mortgage interest

- Add state and local taxes, capped at $10,000

- Add charitable gifts with records

- Add qualifying medical expenses

- Compare that number to your standard deduction

- Ask whether the tax savings justify the recordkeeping

That last step matters more than many articles admit. A paper-thin win is still a bad business decision if it costs you hours of cleanup, missing receipts, and avoidable mistakes.

Hidden traps generic tax articles miss

The biggest one is the Married Filing Separately rule. If one spouse itemizes, the other spouse must itemize too. That can create a lopsided result where one return benefits and the other gets dragged into extra paperwork for little or no gain. For married business owners with uneven deductions, this rule can erase the advantage fast.

High-income owners hit another trap. They assume higher earnings mean itemizing should be the default. Wrong. Income does not create itemized deductions. Eligible personal expenses do. A strong business year may raise your tax bill, but it does not change the fact that the SALT cap blocks a big chunk of state and local tax deductions.

If you are sorting out bigger-picture tax losses from a rough year, that is a separate issue from personal itemizing. Start by understanding net operating loss and keep that analysis separate from Schedule A math.

When the paperwork pays for itself

Itemizing requires proof. Receipts, donation letters, mortgage statements, medical records, and a clean paper trail. TurboTax explains that itemizing tends to make sense only when those deductions exceed the standard deduction by enough to make the effort worthwhile, and that about 10% of taxpayers itemized in tax year 2022 according to TurboTax's guide to choosing between standard and itemized deductions.

Here is my advice. Start from the assumption that the standard deduction wins. Make itemizing prove its value. If your total does not clear the standard deduction by a healthy amount, keep it simple and move on.

Real-World Scenarios for Business Owners

Generic tax articles talk in abstract terms. That's not helpful when you're running a real company, paying real bills, and trying not to overpay the IRS.

Here's how this looks in the wild.

Maria the real estate agent

Maria sells homes around the Philadelphia suburbs. She owns her house, pays meaningful property taxes, and has a mortgage with enough interest to matter. She also gives to a local charity every year.

Maria is the kind of taxpayer who should at least run the itemizing math. Her profile has the usual ingredients that can push someone over the line. If her total beats the standard deduction clearly, itemizing may be the better move.

If it doesn't, she should stop there and take the standard deduction. A lot of homeowners assume they automatically benefit from itemizing. That stopped being true for many people once the standard deduction got bigger.

David the IT consultant

David runs a consulting firm. He has clean books, low personal housing costs, and he donates regularly. But his charitable giving alone probably won't be enough to make itemizing the winner.

This is a common business-owner mistake. People latch onto one deductible category and ignore the full picture. One strong category doesn't guarantee itemizing makes sense. You need the whole total.

David should still track his donations. He just shouldn't assume they change the outcome.

Nina and the separate filing trap

Nina owns a therapy practice. Her spouse has personal medical expenses that may make itemizing attractive for one side of the return. They consider filing as Married Filing Separately and think they can split the difference. One spouse itemizes, the other takes the standard deduction.

That doesn't work.

A critical and often misunderstood rule is that if you file as Married Filing Separately and one spouse itemizes, the other spouse must also itemize. That forces the second spouse to give up the standard deduction even if their own itemized total is zero, and it's a trap that over 40% of MFS filers unknowingly violate, according to this explanation of the Married Filing Separately itemizing rule.

That rule matters more than commonly understood. A couple can make what seems like a smart move for one spouse and accidentally create a worse outcome for both.

Married Filing Separately is where a lot of “simple” deduction advice falls apart. If one spouse itemizes, both are in.

The owner with a rough year

Some owners also have years with uneven income, carryforwards, or losses from one part of their financial life that affect the bigger tax picture. In those situations, personal deductions aren't the only thing worth reviewing. If you're dealing with prior losses or trying to understand how they affect future taxes, this guide to understanding net operating loss is worth reading.

The bigger lesson is simple. The right deduction method doesn't live in a vacuum. It sits inside your full tax picture.

Hidden Rules and the Hassle Factor

The worst tax advice on this topic is also the most common: “If itemized deductions are higher than the standard deduction, itemize.”

That's incomplete.

For many taxpayers, it's a fine starting point. For higher-income earners, it can be wrong in practice because the value of each deduction dollar may not be what you think.

The hidden break-even problem for high earners

Starting in 2026, there's a hidden computational issue that a lot of standard deduction vs itemizing content ignores. For taxpayers in the highest bracket, itemized deductions other than QBI now yield only 35 cents of tax savings per dollar instead of 37 cents, which means the break-even point for switching from the standard deduction to itemizing is effectively higher than many generic calculators suggest, as discussed in Kahn Litwin's analysis of the new deduction value cap.

That matters if you're a business owner with a high-income year after a strong run of contracts, a liquidity event, or a spike in pass-through income. In plain English, the old shortcut math can overstate the benefit of itemizing.

If you're in that group, don't rely on a basic calculator and assume the answer is clean. It may not be.

The cost that doesn't show up on the return

Itemizing also has a labor cost. Not a tax cost. A people cost.

You or someone on your team has to gather the records, store the receipts, and make sure the paper trail is solid. If the IRS asks later, “I'm pretty sure I had that receipt” is useless.

Here's what itemizing usually demands:

- Receipts and proof for charitable gifts, medical expenses, and tax payments

- Mortgage statements and tax forms that tie back to the deduction claimed

- A retention system that lets you find those records later without a scavenger hunt

A practical way to think about the hassle

Use this simple filter before you itemize:

| Question | If the answer is yes | If the answer is no |

|---|---|---|

| Do your potential deductions clearly exceed the standard amount? | Keep going | Stop and use standard |

| Do you have clean records for each category? | Itemizing is realistic | The risk and hassle go up |

| Are you in a high-income situation with special rules? | Get a deeper review | Basic comparison may be enough |

Advisor's view: Tax savings only count if you can support them. A deduction you can't document is not a strategy.

My blunt take

If itemizing saves you real money, do it right. If it only saves a little, don't create a second job for yourself.

Business owners are already stretched thin. You don't need a tax choice that eats hours, clutters your files, and creates audit risk just to chase a marginal benefit. Simpler is better when the savings are close. Precision matters when the savings are meaningful or your income puts you into a more technical zone.

Your Decision Guide and Next Steps

Here's the call I want you to make. Choose the option that leaves more money in your pocket after tax savings, recordkeeping time, and audit risk are all counted.

A lot of owners overcomplicate this. The choice is usually clear once you run the numbers and account for the hassle.

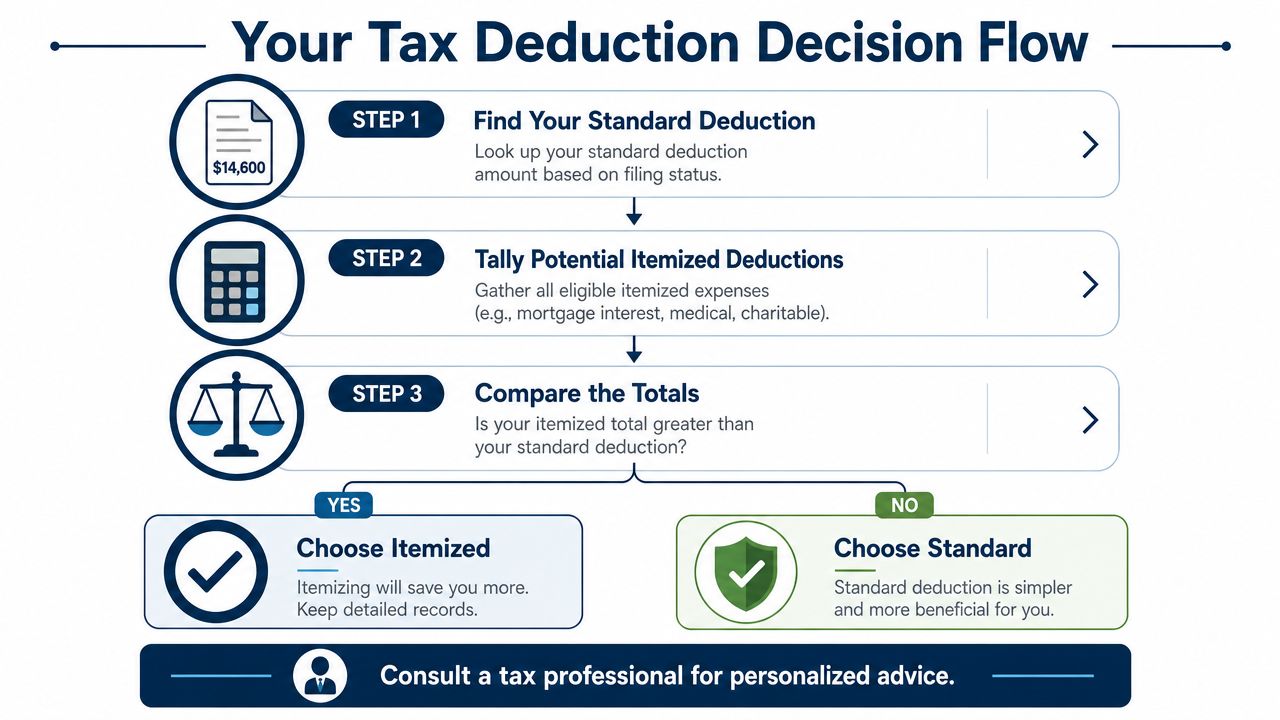

Use this decision flow

- Pull your standard deduction amount based on filing status.

- Add up your likely itemized deductions using the major categories, not wishful guesses.

- Compare the totals and look at the gap.

- Stop and check special rules if you are Married Filing Separately or your income is high enough that phaseouts and limits may change the math.

- Make the call based on net value. More deduction on paper means nothing if the support is weak or the savings are tiny.

My recommendation for most owners

Use the standard deduction when itemized deductions are lower, close, or annoying to prove. That is the right move for many business owners because your time matters, your records may already be stretched across business and personal expenses, and a small tax win can turn into a paperwork headache fast.

Itemize when the gap is clear. If your deductions beat the standard amount by a meaningful margin and your documentation is clean, take the savings and do it right.

The danger zone is the middle. A narrow win for itemizing often looks better on a worksheet than it feels in real life.

If you share files with your accountant, bookkeeper, or tax preparer, Turbotax cloud hosting can help keep filing season organized across devices and users. Organization does not replace judgment, but it does cut wasted time.

Don't make this decision in April only

This choice ties back to decisions you make all year. Charitable gifts, medical timing, mortgage interest, state tax payments, and even how you handle owner compensation can change the result.

If your income moves around during the year, review your estimated tax payment responsibilities before underpayment penalties show up. Business owners get burned when they focus on deductions and ignore cash flow timing.

The biggest mistake I see is treating this like a tax form question instead of a planning question. Married Filing Separately is a common trap. If one spouse itemizes, the other usually has to itemize too, even when that second return would be better off with the standard deduction. High-income owners miss a different trap. They assume itemizing always wins because their expenses are larger, but the break-even point can be higher than expected once limits, filing status, and weak documentation are factored in.

Good tax decisions start before year-end. Filing is the last step.

If you want the blunt version:

- Take the standard deduction if your itemized total is lower, close, or poorly documented.

- Itemize if the tax savings are clearly higher and your records can back up every number.

- Bring in help if you are high income, Married Filing Separately, or juggling a complicated mix of personal and business finances.

If you want help making that call with real numbers instead of guesswork, talk with MyOfficeOps. Their team helps business owners clean up the books, understand the tax impact of financial decisions, and build a year-round plan instead of scrambling at filing time.