You know the feeling. April hits, your CPA sends over the return, and what looked like a strong year suddenly turns into a punch in the gut. You owe a big tax bill, and it's due now. Not “sometime soon.” Now.

That kind of surprise messes with everything. Payroll feels tighter. Owner draws get awkward. You start moving money around just to cover something that should have been planned months earlier. I've seen this with consultants in Center City, contractors in Delco, agency owners on the Main Line, and practice owners out in Chester County. The pattern is the same. The business was doing fine. The tax plan wasn't.

Estimated tax payments fix that. They don't make taxes fun, but they make them manageable. Instead of one ugly bill landing in your lap, you build a rhythm. You pay as you earn. You keep cash flow cleaner. You stop treating tax time like a yearly ambush.

That Awful April Tax Surprise You Can Avoid

A lot of owners think a giant tax bill means they did something wrong. Usually, that's not the primary issue. More often, it means the business made money and nobody built a system to pay taxes along the way.

Take a simple real-world example. A West Chester consultant has a good year. Clients pay on time. Revenue climbs. She reinvests in software, travel, and maybe a part-time admin. On the surface, things look solid. Then the return gets finished and she learns she owes far more than she expected. Why? Because no employer was withholding taxes from those payments, and no one set up a quarterly plan.

That's where panic starts. You scramble. You ask whether you can wait. You wonder if you should pull from savings. You look at the business account and think, “How is there not enough cash if I had a profitable year?”

Profit is not the same as cash you can spend

That's the part many owners learn the hard way.

Money comes into the business account and it all looks available. But some of that money was never really yours to spend. A chunk of it belongs to the IRS, the state, and if you operate in Philadelphia, possibly the city too. If you don't peel that off as you go, April becomes ugly fast.

Practical rule: If tax money stays mixed in with operating cash, you will be tempted to spend it.

Estimated tax payments are the adult version of putting money aside before the bill comes due. Think of them as turning a massive annual hit into scheduled installments. It's less dramatic. That's the point.

For business owners trying to get organized before the next filing season, both Steingard Financial's tax season guide and this practical checklist on how to prepare for tax season are useful places to tighten up your process.

The fix is boring, and boring is good

Nobody brags about estimated tax payments. They're not exciting. But they do something better than exciting. They create predictability.

Here's what changes when you handle this right:

- Cash flow gets calmer because you're not trying to fund one giant payment all at once.

- Bookkeeping gets more honest because your profit number starts matching reality.

- Decision-making improves because you stop confusing pre-tax income with spendable money.

That last one matters. A lot of owners hire, lease, or expand based on cash that looks available but really isn't.

The goal isn't to make taxes disappear. It's to stop being surprised by them. Once you accept that tax payments need to happen during the year, the whole thing gets less emotional and more mechanical. That's how it should be.

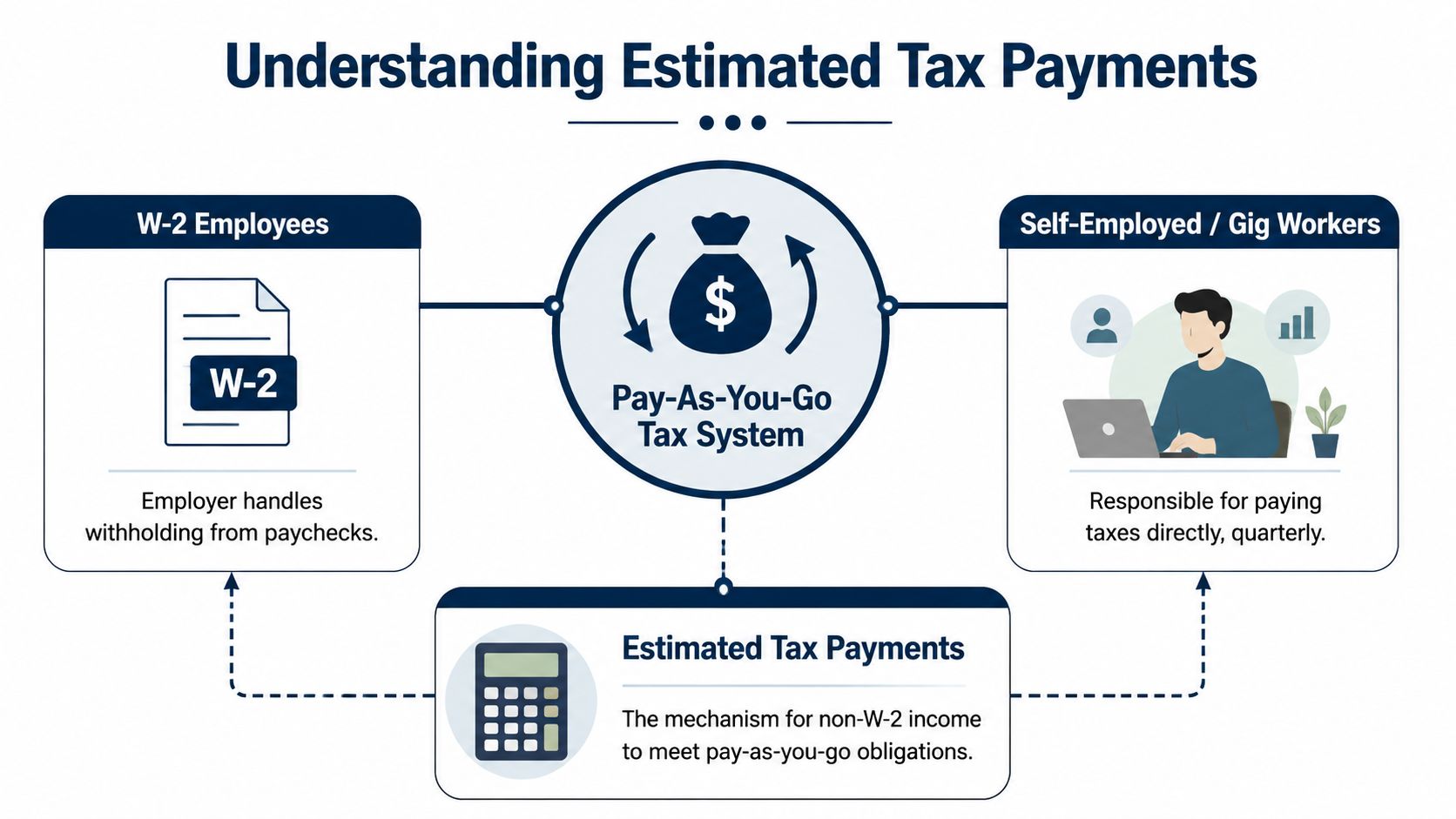

What Are Estimated Tax Payments Anyway

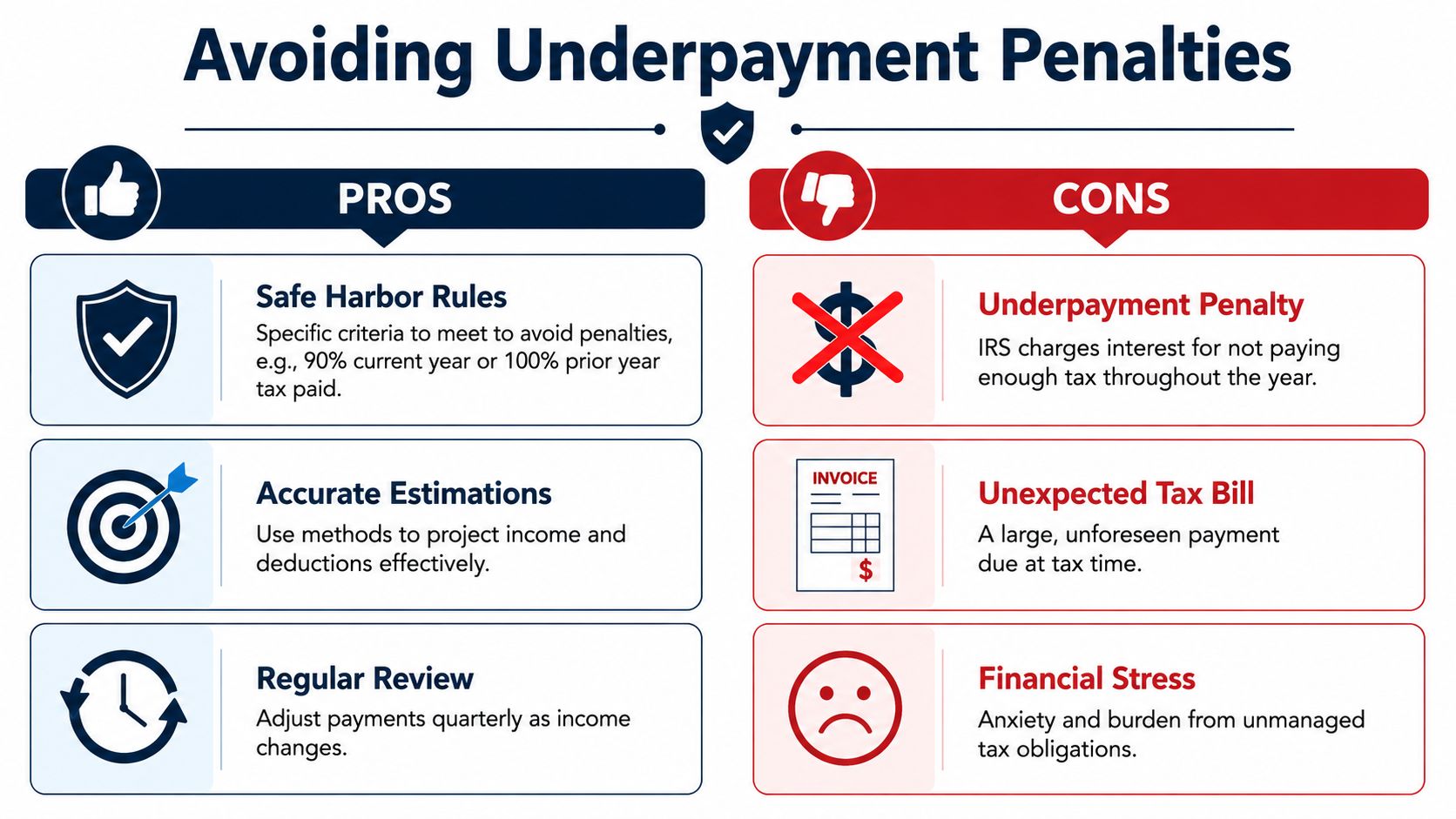

The U.S. tax system is pay-as-you-go. That means the government expects tax money during the year, not just when you file. The IRS says estimated taxes are mainly for income that isn't covered by withholding, and individuals such as sole proprietors, partners, and S corporation shareholders generally must make them if they expect to owe $1,000 or more when filing. Corporations generally must make them if they expect to owe $500 or more. Most taxpayers can avoid a penalty by paying at least 90% of the current year's tax liability or 100% of the prior year's tax, and for higher-income taxpayers with prior-year adjusted gross income above $150,000 or $75,000 if married filing separately, that prior-year safe harbor rises to 110% of the prior year's tax, according to the IRS estimated taxes guidance.

That sounds technical, but the idea is simple. If you're a W-2 employee, your employer sends tax money in from each paycheck. If you own a business or get pass-through income, you have to do that job yourself.

Think of it like a tax layaway plan

That's the cleanest way to explain it.

You're not prepaying something optional. You're sending in tax money as income shows up, instead of holding everything until filing time. For Philly-area owners, this is common if you're any of the following:

- A sole proprietor getting paid directly by clients

- A partner receiving income from a partnership

- An S corporation shareholder taking pass-through income

- A corporation with tax due that won't be covered another way

If your income doesn't have withholding attached to it, you should assume estimated tax payments are on the table until proven otherwise.

Who might not need to pay

The IRS also gives one clear exception. If you had no tax liability in the prior year, were a U.S. citizen or resident alien for the full year, and had a 12-month tax year, you may not need to make estimated payments for the current year. That matters for newer businesses and owners coming off a low-income year.

The mistake I see most often is not misunderstanding the rule. It's assuming the rule doesn't apply because nobody reminded you.

A few practical examples make this easier:

| Business situation | How this usually plays out |

|---|---|

| W-2 employee with one job | Taxes are usually handled through payroll withholding |

| Freelance designer in Fishtown | Often needs estimated tax payments because client checks don't include withholding |

| S corp owner taking a salary plus distributions | Payroll may cover part of the tax, but pass-through income can still create an estimated payment need |

| Small C corporation | May need corporate estimated payments if it expects to owe enough tax |

This is why I tell owners not to ask, “Do I file taxes in April?” Of course you do. Ask, “Who is sending tax money in during the year?” If the answer is “nobody,” then you probably need a plan.

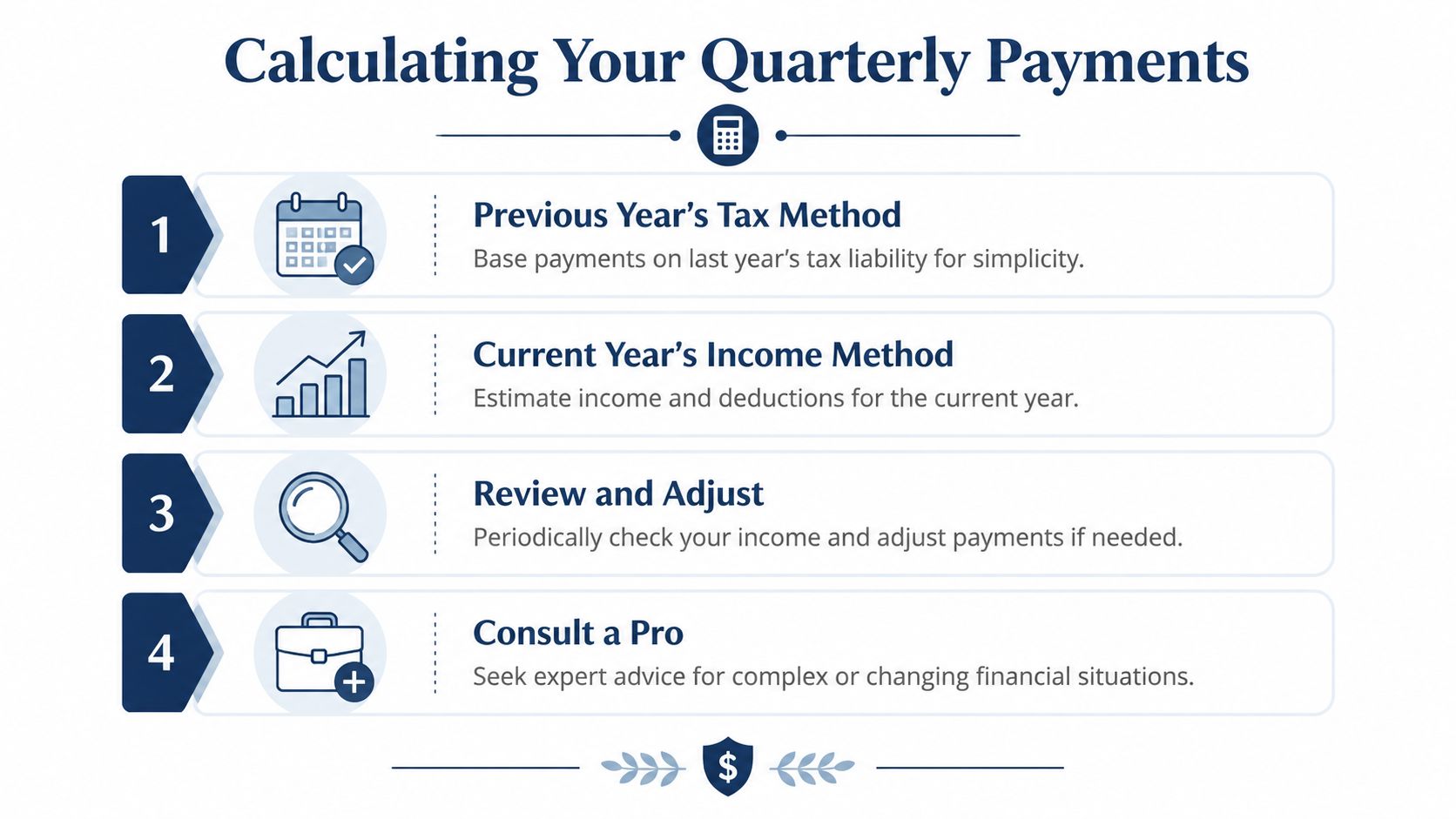

How to Calculate What You Owe

Owners often freeze up, but it's not as bad as it looks. You've got two common paths. One is simpler and more predictable. The other is better if your income bounces around.

A fictional example helps. Let's use Dana, a consultant based near Philadelphia. She has a good spring, a slower summer, and a strong year-end push. That kind of uneven income is normal around here, especially for consultants, agencies, and project-based firms.

Path one uses last year as your anchor

This is the method most owners should start with. It's straightforward. You look at last year's total tax, then build current-year payments around that safe-harbor framework discussed earlier.

Why this works: it gives you a target you can plan around, even if the current year is still taking shape.

Dana's version of this would look something like this in plain English:

- Pull last year's return.

- Find the total tax figure your advisor uses for estimated payment planning.

- Use that as the base for current-year installments under the safe-harbor rules.

- Revisit during the year if income jumps.

This approach is not about perfect precision. It's about avoiding ugly surprises and staying inside the lines.

Path two follows the money as it comes in

If Dana earns most of her money in a few busy stretches, the annualized income method may fit better. This method tracks what the business earned during the year and adjusts payments based on that pattern.

That's useful for owners with:

- Seasonal work like event businesses, tourism-related firms, or trades with weather swings

- Project-based income where one large contract can change the year

- Uneven partner distributions from professional firms

If spring is huge and summer is quiet, this method can match the timing better than using flat installments.

If your income is lumpy, don't force a smooth-payment strategy onto an uneven business.

The tradeoff is paperwork and discipline. You need current books. Not “I'll reconcile that later” books. Real books.

Use tools, but don't let them replace judgment

An estimator can help you pressure-test the numbers. If you want a quick gut check on self-employment tax exposure, VerticalRent tax estimator is a handy starting point. For planning the bigger business picture, this guide on how to forecast revenue helps tie estimated taxes back to actual income planning.

Here's the key point. Your estimate is only as good as your bookkeeping. If your revenue is stale, expenses are uncategorized, or owner draws are mixed with business spending, your tax estimate becomes a guess wearing a tie.

A clean process usually looks like this:

| What to review | Why it matters |

|---|---|

| Year-to-date revenue | Shows whether you're ahead of or behind plan |

| Major deductions | Affects taxable income |

| Owner compensation mix | Changes how much tax is already being covered |

| Prior-year tax return | Gives you a planning baseline |

Most owners don't need more tax jargon. They need a repeatable routine. Review the books. Compare to last year. Pick the method that fits your income pattern. Then pay on purpose instead of reacting later.

The Quarterly Payment Schedule and How to Pay

The schedule trips people up because it doesn't line up neatly with normal calendar quarters. You can't just think, “I'll handle this every three months,” and hope for the best. You need the actual due dates on your calendar.

The standard federal schedule typically falls on April 15, June 15, September 15, and January 15 of the following year, and those payments are tied to Form 1040-ES for individuals and Form 1120-W for corporations, as outlined in Fidelity's overview of estimated tax payment due dates and forms. If a due date lands on a weekend or federal holiday, it shifts to the next weekday.

Treat these like vendor deadlines

If you miss a client deadline, there's fallout. Same idea here.

Put the dates in your calendar, your accounting software, and your task manager. Don't rely on memory. Owners are juggling too much already.

A simple rhythm works best:

- After each month closes, review profit

- A few weeks before each due date, decide the payment amount

- On payment week, confirm the transfer went through

That last step matters. “I thought it was scheduled” is not a defense.

How owners usually pay

Most businesses stick to one of these methods:

- Online payment portals because they're faster and easier to track

- Direct debit if you want less manual work

- Mail-in vouchers if you prefer paper and a physical trail

- Tax software or accounting workflows if your advisor builds payments into your routine

For federal payments, the forms above give you the framework. For Pennsylvania and Philadelphia obligations, you also need to follow the state and local systems that apply to your business. More on that in a minute.

The best payment method is the one you'll actually use on time, every time.

If you're new to this, keep it simple. Pick one payment method. Use it consistently. Save the confirmation. Don't create a different process every quarter.

Avoiding Penalties with Smart Planning

Underpayment penalties are one of the dumbest leaks in a business. I'm being blunt on purpose. If you owe tax, you owe tax. Fine. But paying extra because you didn't plan the timing well is a self-inflicted wound.

A lot of owners treat penalties like bad luck. Usually, they're not. They happen because nobody monitored income, nobody adjusted payments, or everybody waited too long.

The overlooked move for owners with W-2 income

This is one of the most useful planning tools out there, and a lot of business owners miss it.

The IRS says income taxes withheld from wages are treated as paid evenly throughout the year. That creates flexibility. A business owner with both W-2 wages and pass-through income can increase payroll withholding later in the year to help cover a shortfall, and that can work better for penalty purposes than trying to catch up with a big late estimated payment, according to the IRS underpayment penalty guidance.

That matters if you:

- Own an S corp and run payroll

- Have a spouse with W-2 income

- Work a job while also running a side business

- Took distributions or bonus income and fell behind on estimates

Why withholding can be a cleaner fix

Here's the practical version. Let's say it's late in the year and you realize your estimated payments are short. You may be able to adjust withholding through payroll instead of sending a large quarterly check and hoping it solves the problem. Because withholding is treated as if it were paid evenly through the year, it can function like an escape hatch.

That doesn't mean you should wing it until December. It means you have one more tool.

If you have payroll, you may have more flexibility than you think.

For owners with a salary component, a year-end withholding adjustment can be smarter than panic-paying estimated tax in a rush. The move is legal. It's practical. And it often fits cash flow better.

What smart planning looks like in real life

Not every business needs the same process, but the habits are consistent:

| Habit | What it prevents |

|---|---|

| Mid-year tax review | Finding out too late that income is ahead of plan |

| Payroll withholding check | Missing the chance to fix a shortfall efficiently |

| Updated books each month | Basing payments on stale numbers |

| Cash reserve for taxes | Scrambling when due dates hit |

If there's one takeaway here, it's this: penalties are usually preventable. The owners who avoid them aren't lucky. They review numbers early, make adjustments before year-end, and use every legal tool available.

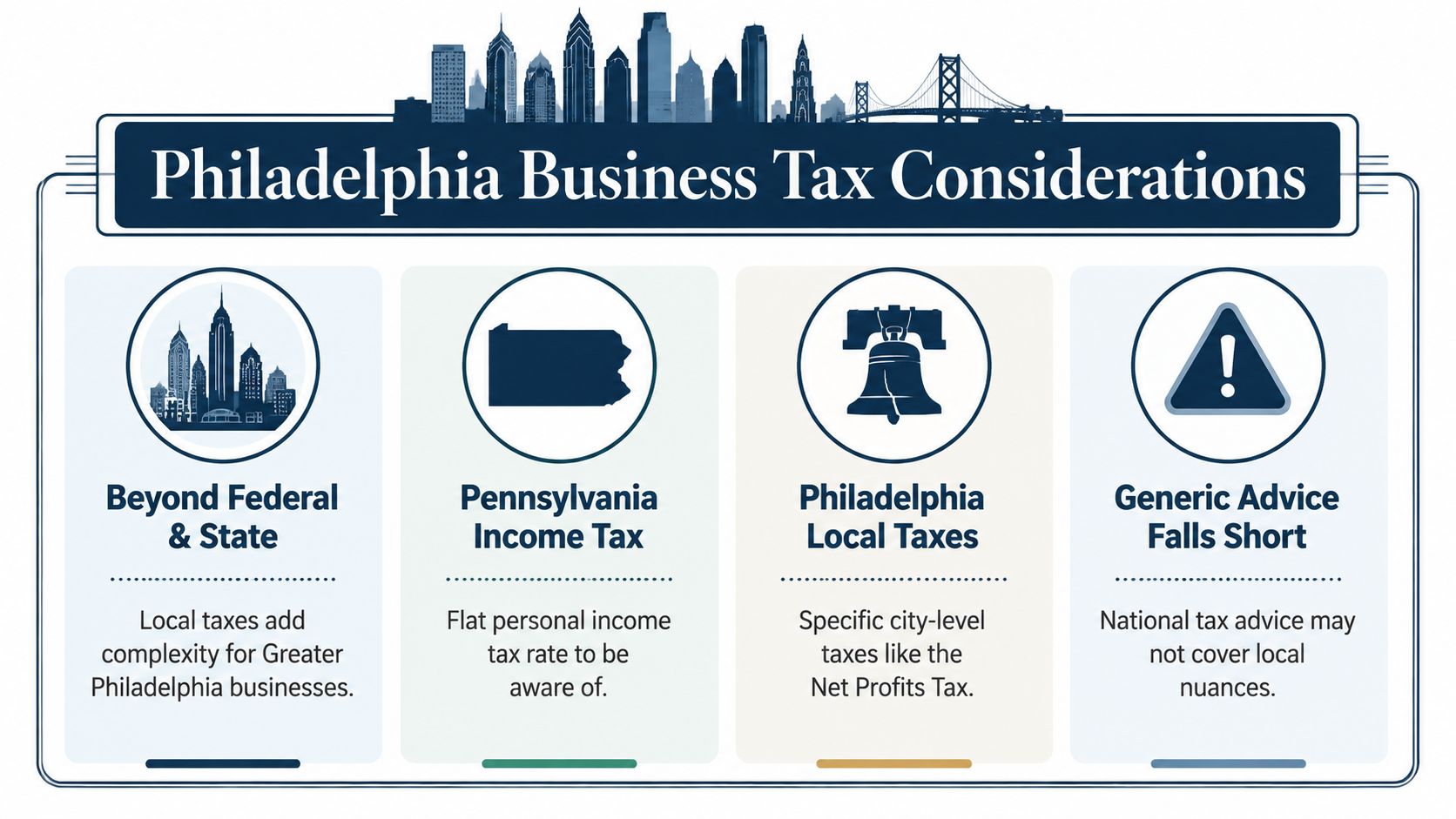

Special Tax Rules for Philadelphia Businesses

Generic tax advice falls apart fast once you're doing business in and around Philadelphia. Federal rules are only part of the story. Pennsylvania has its own state obligations, and the City of Philadelphia adds another layer that many owners underestimate.

That's where local businesses get tripped up. They'll plan for the IRS, maybe remember Pennsylvania, and then get blindsided by a city notice later. If you operate in Philly, or have business activity there, you need to think local from the start.

Pennsylvania is only one layer

Pennsylvania personal income tax is often simpler than federal tax in practice because the structure is more straightforward. That simplicity helps, but it can also create false confidence. Owners start thinking the whole tax picture is simple.

It isn't, especially once city taxes enter the mix.

If you're a pass-through owner in the Greater Philadelphia area, your planning usually has to account for:

- Federal estimated tax payments tied to business income not covered by withholding

- Pennsylvania tax obligations based on your business and personal filing situation

- Philadelphia local taxes if you operate in the city or have taxable business activity there

Don't ignore Philadelphia BIRT

Philadelphia's Business Income & Receipts Tax, usually called BIRT, is one of the biggest local blind spots for business owners. People hear “business income tax” and assume it works like a standard profit-based tax. Then they find out the city's approach has its own rules, filing expectations, and estimated payment considerations.

That's why national articles don't help much here. They explain federal estimates and stop. Philly owners need a local compliance checklist.

A practical approach is to keep a separate city-tax review on your calendar and make sure your bookkeeping can answer these questions quickly:

- Is the business doing work that creates a Philadelphia tax filing obligation?

- Are gross receipts and net income being tracked cleanly enough to support city filings?

- Did anyone plan for city estimated payments, or are you waiting for a surprise notice?

If those answers are fuzzy, the fix usually starts in the books, not in the tax return.

Local compliance depends on clean records

This is why I tell Philly owners not to treat bookkeeping like back-office clutter. Your books drive your tax visibility.

If your records are messy, local taxes become guesswork. If your records are current, city and state compliance become a routine process. For a stronger local planning framework, this resource on integrated tax consultants is a useful reference point.

Philadelphia business owners don't just need tax prep. They need tax coordination.

That's the difference. A return tells you what happened. Coordination helps you prepare for what's coming, including city-level obligations that don't show up in generic small-business advice.

Cash Flow Habits for Stress-Free Tax Payments

Estimated tax payments get easier when your bookkeeping gets tighter. Not glamorous. Just true.

Most owners don't have a tax problem first. They have a visibility problem first. If you don't know what the business earned, what it spent, and what cash is already spoken for, then every tax estimate becomes a rough guess. That's why one quarter feels manageable and the next one feels like a fire drill.

Build one habit around every deposit

The easiest way to lower tax stress is to stop treating every dollar that hits the bank as operating cash.

A lot of owners use a simple version of the “set it aside now” method. Revenue comes in. A portion moves to a separate tax savings account. You don't wait until quarter-end to see what's left. You move the money while cash is fresh.

That habit does three useful things:

- It protects tax cash from daily spending

- It makes quarterly payments feel routine

- It forces you to look at what's really available to run the business

If you don't separate the money, your checking account lies to you.

Monthly books beat quarterly panic

Here's the plain truth. You cannot estimate taxes well from bad books.

If your reconciliations are behind, if expenses are uncategorized, or if payroll and owner transactions are mixed together, you're driving in the fog. The tax payment might still get made, but it won't feel controlled.

A better monthly rhythm looks like this:

| Monthly habit | Why it matters |

|---|---|

| Reconcile bank and credit card accounts | Keeps profit numbers real |

| Review income by service line or project | Shows what's actually driving taxable income |

| Clean up owner draws and personal spending | Prevents distorted reporting |

| Compare cash balance to tax reserve | Confirms whether set-aside money is still intact |

Good systems reduce stress because they reduce surprises

Modern tools prove helpful. Accounting software, payroll integration, and simple dashboards can make tax planning less reactive. But software only works if someone is reviewing the output and making decisions from it.

That's the part owners often delay. They buy the tools, but they don't create the rhythm.

Clean books turn estimated tax payments from a guess into a calendar task.

And that's the whole game. Not perfection. Predictability.

If running the business already takes all your attention, there's no prize for wrestling bookkeeping, payroll coordination, tax tracking, and forecasting by yourself. A partner like MyOfficeOps can take that weight off your plate by keeping the books clean, building a reliable reporting cadence, and helping you make tax decisions before they become emergencies.