You're probably doing this right now. Looking at your bank balance, looking at your pipeline, then trying to decide if you can afford to hire, replace a truck, add a provider, or take on a lease.

Most owners don't call that “revenue forecasting.” They call it trying to make the next smart move without getting burned.

That's why this matters. A forecast isn't a crystal ball. It's a working plan. It helps you answer simple but high-stakes questions. Are sales really growing, or did one good month fool you? If you win that big project, when does the revenue show up? If patients book more appointments, when does cash land in the account?

For service firms, healthcare practices, and construction companies, those questions get even harder because revenue and cash rarely move in a straight line. You can have a full schedule, signed work, and strong booked revenue, then still feel pressure on payroll because timing is off.

Stop Guessing and Start Planning Your Revenue

A lot of small business owners run on a mix of instinct, experience, and yesterday's bank balance. That works for a while. Then the business gets bigger, payroll gets heavier, and one wrong hiring decision suddenly matters a lot more.

I've seen this most often with firms that are busy but not clear. An agency has signed retainers, open proposals, and one-time projects. A clinic has strong appointment volume but uneven payment timing. A contractor has backlog on paper, but project starts keep shifting. On the surface, revenue looks healthy. Under the surface, nobody knows what the next few months really look like.

That's when owners start making decisions in a fog. They delay hiring too long. Or they hire too early. They spend based on confidence instead of visibility.

A good forecast doesn't remove uncertainty. It reduces avoidable surprises.

If you're learning how to forecast revenue, start with a simple mindset shift. You are not trying to predict the future perfectly. You are trying to build a useful map from what you already know.

That map should help you answer questions like these:

- Can we hire now: or do we need another month of stable revenue first?

- Can we handle a slow-paying customer: without creating pressure on payroll?

- Is this growth real: or is it coming from one unusual project?

- What happens if timing slips: on a few key deals or jobs?

If cash feels tight even when sales look decent, it helps to pair forecasting with a practical read on working capital. This small business cash flow guide does a good job showing why profit and cash are not the same thing.

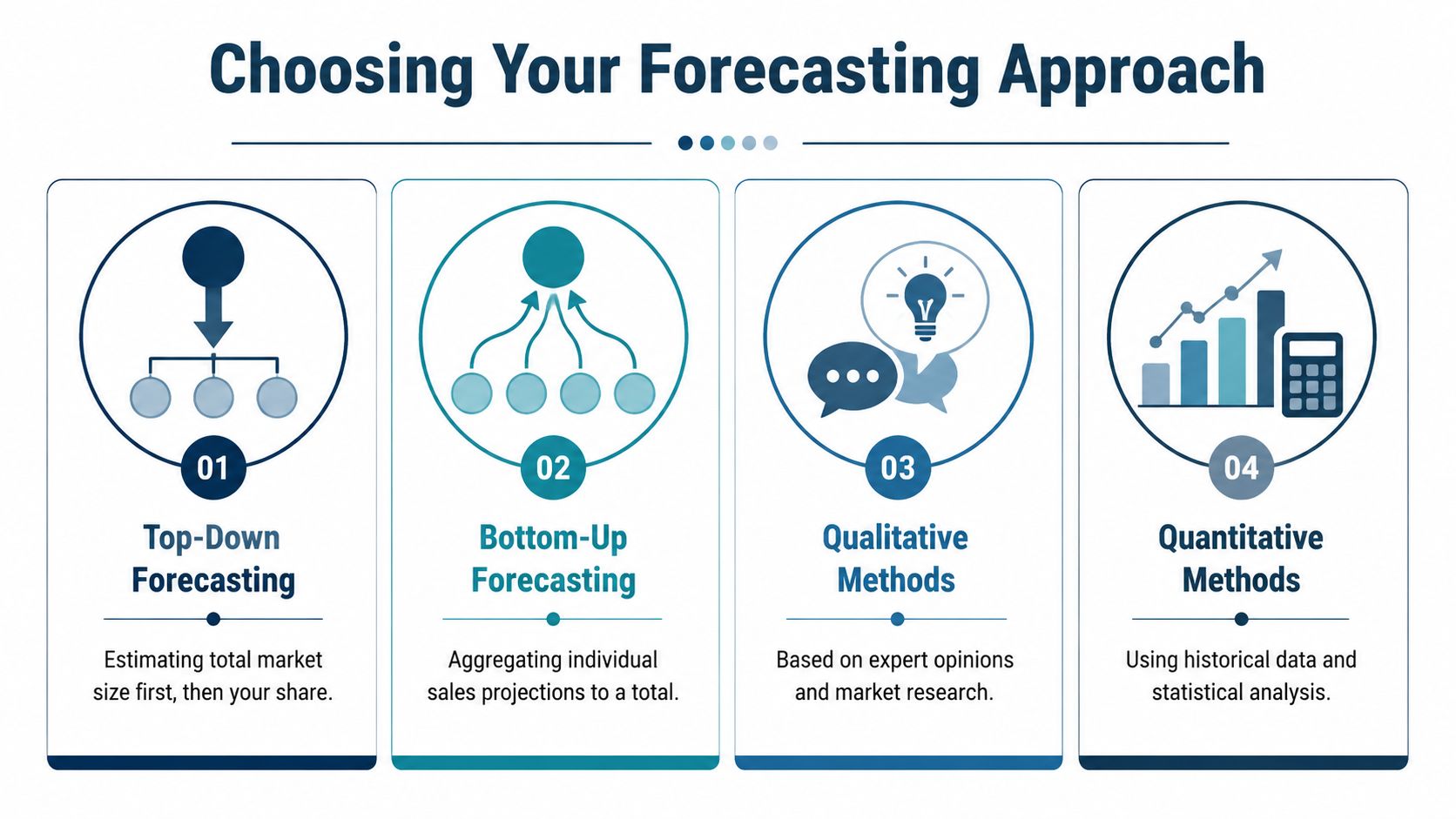

Choosing Your Forecasting Approach

Before you build a spreadsheet, pick the right lens. Most small businesses don't need a fancy model first. They need the right starting method.

Some methods are quick but blunt. Others take more work but reflect how the business operates.

Three practical ways to start

Think about forecasting the way you'd plan food for an event.

Top-down is like saying, “We have this many guests, so we probably need this much pizza.” In business, that means starting with a market size, a growth target, or an annual revenue goal, then working backward to monthly numbers.

This is useful when you're early-stage, launching something new, or planning strategically. It's weak as an operating tool because it often tells you what you want to hit, not what your business can realistically produce.

Bottom-up is like asking each guest how many slices they'll eat, then adding that up. In business, it means building the forecast from the ground level. Number of appointments. Billable hours. Active projects. Crews available. Proposal volume. Win rates.

This is usually the most useful approach for SMBs because it connects revenue to things you can see and manage.

Historical forecasting is like saying, “Last year's party needed this much, so this year will probably be similar.” Harvard Business School describes the straight-line method as multiplying last year's revenue by a past growth rate, while more advanced time series analysis can be more accurate when revenue has seasonality or complex patterns because it looks for trends and repeating cycles in the data through its financial forecasting overview.

What works for different business types

A new business with limited history often starts with top-down thinking, then shifts quickly into bottom-up once it has real operating data.

An established service business usually gets more value from bottom-up. If you know your team capacity, utilization, close rates, and average project size, you already have the bones of a forecast.

A healthcare practice often needs a mix. Historical trends can help, but appointment volume, payer mix, and provider schedules usually matter more than a simple growth assumption.

Construction is different again. Backlog matters. Timing matters more. Historical revenue can give context, but bottom-up forecasting tied to signed jobs, start dates, and conversion from backlog usually gives a truer picture.

A simple comparison

| Method | Best use | Main strength | Main weakness |

|---|---|---|---|

| Top-down | New initiatives and annual planning | Fast to build | Often too abstract for operations |

| Bottom-up | Daily management and hiring decisions | Tied to real drivers | Takes more discipline |

| Historical | Stable businesses with clean records | Easy starting point | Misses shifts in mix or timing |

Practical rule: If you're trying to decide on staffing, payroll, or short-term spending, don't rely on a top-down forecast alone.

For most owners, the right answer isn't one method. It's a combination. Start with history. Pressure-test it with current pipeline or workload. Then ask whether your team has the capacity to deliver what the number assumes.

Gathering the Right Ingredients for Your Forecast

A weak forecast usually isn't caused by bad math. It's caused by missing inputs.

Owners often pull last year's sales, add a growth rate, and call it a plan. That's easy, but it leaves out the actual drivers. If your close rates are falling, if one provider is leaving, if materials are delayed, or if a key client is cutting scope, last year's trend won't save you.

Start with revenue by type

Don't forecast one big revenue line if your business has very different kinds of work.

Break it apart in ways that match reality:

- Recurring work: retainers, maintenance contracts, monthly service plans

- One-time work: projects, implementations, special jobs

- Variable work: hourly labor, add-on services, change orders

- Timing-sensitive work: progress billing, insurance reimbursement, seasonal demand

Averaging across mixed revenue streams hides underlying problems. A firm can look steady at the top line while one profitable service line is slipping and a lower-margin one is carrying the month.

Map the drivers before the formula

Factors.ai notes that effective forecasting models map drivers such as sales headcount, average deal size, conversion rates, and churn before building the model, and that companies often combine methods rather than rely on one approach in its guide to revenue forecasting models.

That idea is simple. Revenue comes from activity plus conversion plus pricing plus timing.

For example:

- A law firm might track consultation volume, signed matters, billable hours, and realization.

- A clinic may watch appointment volume, no-show patterns, payer mix, and provider availability.

- A contractor may focus on bids submitted, jobs won, backlog, project starts, and billing milestones.

The best forecast inputs are the numbers your team can influence before month-end, not just the revenue number you see after month-end.

Use a clean collection process

If your data lives in QuickBooks, a practice management system, a CRM, job costing software, and a few sticky notes, the forecast will fall apart fast.

A repeatable process matters more than a perfect dashboard. If you need a simple way to organize source data before building reports, this step-by-step reporting framework is a useful reference.

Keep your checklist practical:

- Historical revenue by month for each main line of business

- Current pipeline or backlog with likely timing

- Operational capacity such as staff hours, provider days, crews, rooms, or equipment

- Price and mix changes that affect average revenue

- Customer retention or renewals where recurring work matters

- Seasonality and timing issues that repeat through the year

If you're not sure which operating numbers belong in the model, this list of key performance indicators for small business can help you narrow it down to a few KPIs that move revenue.

Building Your Revenue Model in a Spreadsheet

You don't need expensive software to learn how to forecast revenue well. A clean spreadsheet is enough if the model follows the way your business works.

The mistake I see most is this: one cell says “expected growth,” another cell says “next year revenue,” and that's the entire model. It looks tidy. It's also useless when you need to explain why the number changed.

Use a driver-based model instead.

A simple spreadsheet structure

Build the file in four tabs.

Tab 1: Assumptions You keep the key inputs here. Pricing, close rates, utilization, average project size, renewal assumptions, and any timing assumptions.

Tab 2: Volume drivers

In this tab, you forecast the activities that create revenue. Leads, appointments, proposals, projects, jobs, visits, or units.

Tab 3: Revenue output

Multiply the drivers into forecasted revenue by segment and by month.

Tab 4: Actual versus forecast

Once each month closes, plug in actuals and compare. That's how the model gets better.

Example for a professional services firm

Let's say you run a consulting or agency business. Don't forecast “monthly revenue growth.” Forecast the chain that creates revenue.

You might model:

- New opportunities created

- Proposal volume

- Win rate

- Average project value

- Retainer renewals

- Team utilization

Then the spreadsheet can estimate project revenue and recurring revenue separately. That matters because a firm with strong new sales can still miss revenue if the delivery team is full and can't start work on time.

The most actionable setup for SMBs is to tie revenue to a small set of controllable KPIs specific to the industry, such as utilization for professional services, appointment volume for healthcare, or backlog conversion for construction, as noted in this summary on industry-specific forecast implementation.

Industry examples that make the model usable

Here's what that looks like in plain terms.

| Business type | Core drivers to model |

|---|---|

| Professional services | Utilization, billable hours, realization, active clients |

| Healthcare practice | Appointment volume, provider schedule, payer mix |

| Construction | Backlog, project start timing, billing milestones, conversion from awarded work |

A healthcare clinic usually shouldn't start with a flat monthly growth rate. It should start with provider calendars, appointment slots, expected visits, and the mix of reimbursement sources.

A contractor usually shouldn't assume backlog turns into revenue evenly. Jobs slip. Materials lag. Billing depends on milestones. The model should reflect that.

Build the forecast at the level where your operations team actually manages the business. If the team talks about appointments, crews, and billable hours, the model should too.

Keep it rolling, not annual

A static annual budget gets stale fast. A rolling model stays useful.

Use a 12-month rolling forecast. Every month, replace the completed month with actuals and add one new month at the end. That keeps your planning horizon alive.

A good spreadsheet also needs space for notes. If a major client pauses work, if a provider goes on leave, or if a project gets pushed, note it beside the driver change. That makes the model easier to trust later.

If you want a starting point for the cash side that connects to this revenue model, a cash flow forecasting template can help you extend the spreadsheet beyond topline revenue and into collections timing.

What If? Stress-Testing Your Forecast with Scenarios

One forecast number looks clean. It also creates false confidence.

If your entire plan depends on one version of the future, you're going to get surprised. The issue isn't that the forecast was “wrong.” The issue is that you didn't prepare for the range of likely outcomes.

Pick the few variables that really matter

You don't need endless versions. Most SMBs only need three scenarios:

- Base case: what likely happens if current conditions hold

- Upside case: what happens if a few things go right

- Downside case: what happens if timing slips or demand softens

The key is choosing the variables with the biggest impact.

For a service business, that might be utilization and client retention.

For a clinic, appointment volume and payer mix may matter most.

For construction, project delay and backlog conversion usually carry a lot of weight.

Connect scenarios to real signals

Scenario-based forecasting is especially useful when economic conditions are uncertain, and modern approaches can connect external signals like interest rates or labor availability to a rolling forecast instead of treating forecasting as a static annual task, according to Orb's overview of revenue forecasting models.

That matters because volatility rarely shows up as a neat percentage change across the whole business. It usually hits one part first.

A few examples:

- A contractor sees labor tightening and pushes project start assumptions out.

- An IT firm notices older pipeline deals are sitting longer and lowers expected conversion timing.

- A medical practice sees reimbursement pressure in one payer category and changes its mix assumptions.

Reality check: If one customer, one provider, or one project can swing the month, a single-number forecast is too fragile.

A scenario model gives you options. If the downside case happens, you already know which expenses to delay, which hires to pause, and how much cash cushion you need. If the upside case starts showing up, you can move faster without guessing.

Turning Your Forecast into Smart Business Decisions

A forecast earns its keep when it changes what you do. If it sits in a spreadsheet and nobody uses it, it's just decoration.

The practical value shows up in decisions. Can you hire now? Should you take on debt? Is the new service line adding useful revenue or just adding complexity? Do you need to push harder on collections before expanding?

Separate bookings, revenue, and cash

Many owners stumble on this point. Signed work is not the same as recognized revenue. Recognized revenue is not the same as cash in the bank.

A common error in SMB planning is mixing booked revenue with recognized revenue and ignoring collection lags. A stronger forecast combines revenue timing with invoicing and collections data so owners can make cash-aware decisions on payroll and hiring, as discussed in this piece on revenue forecast accuracy tips.

That single distinction changes how you run the business.

A contractor may have great booked work but delayed cash because billing milestones haven't been reached.

A clinic may recognize revenue before payment clears because collections take time.

A service firm may sign a project this month, start work next month, invoice after that, and get paid even later.

Put a review rhythm around the model

A forecast should move on a schedule. For most SMBs, monthly is the minimum. Weekly can make sense if revenue is lumpy or cash is tight.

Use a short review meeting and ask:

- What changed in pipeline or backlog

- What changed in staffing capacity

- Which assumptions are now stale

- Where did timing slip

- What does that do to cash, not just revenue

Here, actual-versus-forecast reporting becomes useful. Not to shame anyone. To learn. If you want a practical read on that discipline, this guide on improve reporting with budget analysis is worth a look.

Use the forecast to answer operating questions

A living forecast helps with decisions like these:

| Decision | What to check in the forecast |

|---|---|

| Hiring | Revenue by month, utilization, collections timing |

| Equipment purchase | Cash timing, backlog stability, near-term downside scenario |

| Adding a service line | Segment-level demand, staffing capacity, margin path |

| Owner distributions | Expected collections, tax obligations, upcoming payroll pressure |

One detail that matters a lot in practice is forecast cadence. A rolling monthly forecast tends to be more useful than a once-a-year plan because owners can react while there's still time to do something.

For businesses that want support beyond a DIY spreadsheet, tools range from QuickBooks and Excel to outsourced advisory support. One option in that mix is MyOfficeOps, which provides bookkeeping, forecasting, KPI reporting, and CFO-style support for SMBs that need help turning financial data into operating decisions.

Don't stop at revenue

The strongest forecast for a small business links four things:

- Demand

- Delivery capacity

- Revenue timing

- Cash collection timing

If one of those is missing, the forecast may still look good on paper while the business feels stressed in real life.

Good forecasting helps you make calmer decisions because you can see the trade-offs before the bank account forces them on you.

When to Get Expert Forecasting Help

Building your own forecast is worth doing, even if the first version is rough. You'll understand your business better the moment you stop looking only at last month's revenue and start looking at what creates next month's.

But there's a point where the spreadsheet starts fighting back.

That usually happens when you have multiple service lines, more than one location, a complicated billing model, or major decisions on the table. Maybe you're thinking about opening a second office, buying equipment, adding a provider, or preparing for a sale. In those moments, forecasting stops being a simple planning task and starts becoming part of risk management.

Signs it's time to bring in help

- The file is getting too complex: and only one person knows how it works

- Your revenue streams behave differently: but the model still treats them the same

- Cash keeps surprising you: even when revenue appears solid

- You need scenario planning: for a lender, investor, expansion, or transition

- You're spending too much time updating numbers: and not enough time acting on them

An outside advisor can help structure the model, clean up assumptions, and tie the forecast back to decisions on hiring, pricing, and cash reserves. More importantly, they can challenge the blind spots that owners and internal teams often miss because they're close to the day-to-day.

If you're weighing whether it's time for that level of support, this overview of CFO services for small business can help you see what that kind of partnership usually includes.

If you want help building a revenue forecast that's useful for hiring, payroll, and cash planning, MyOfficeOps works with small and midsize businesses to turn messy financial data into clear operating decisions. The goal isn't a prettier spreadsheet. It's a forecast you can trust when the stakes are real.