You're probably here because your numbers are talking, but they're not saying anything useful.

Maybe revenue looks fine, but cash still feels tight. Maybe payroll clears, vendors get paid, and the business keeps moving, yet you still can't answer simple questions with confidence. Can we hire? Can we open another location? Are we priced right? If I wanted to sell in a few years, what would a buyer see?

That's where a lot of owners get stuck. They know they need outside help, but they don't know whether they need financial advisory or consulting. Those two labels get thrown around like they mean the same thing. They don't.

For a small or midsize business in Philadelphia, West Chester, or the surrounding area, the difference matters. Choose the wrong type of help and you can spend money on a polished report that sits in a drawer, or pay for ongoing support when what you really needed was a sharp, focused project.

Are You Looking for a Roadmap or a Repair Manual

A common small business scene looks like this. The owner opens the laptop after hours, stares at the P&L, flips to the balance sheet, and then jumps into the bank account because that still feels more real than any report.

The business isn't falling apart. That's what makes this confusing. It's running. Clients are active. The team is busy. But something feels off because the numbers don't lead to a clear next move.

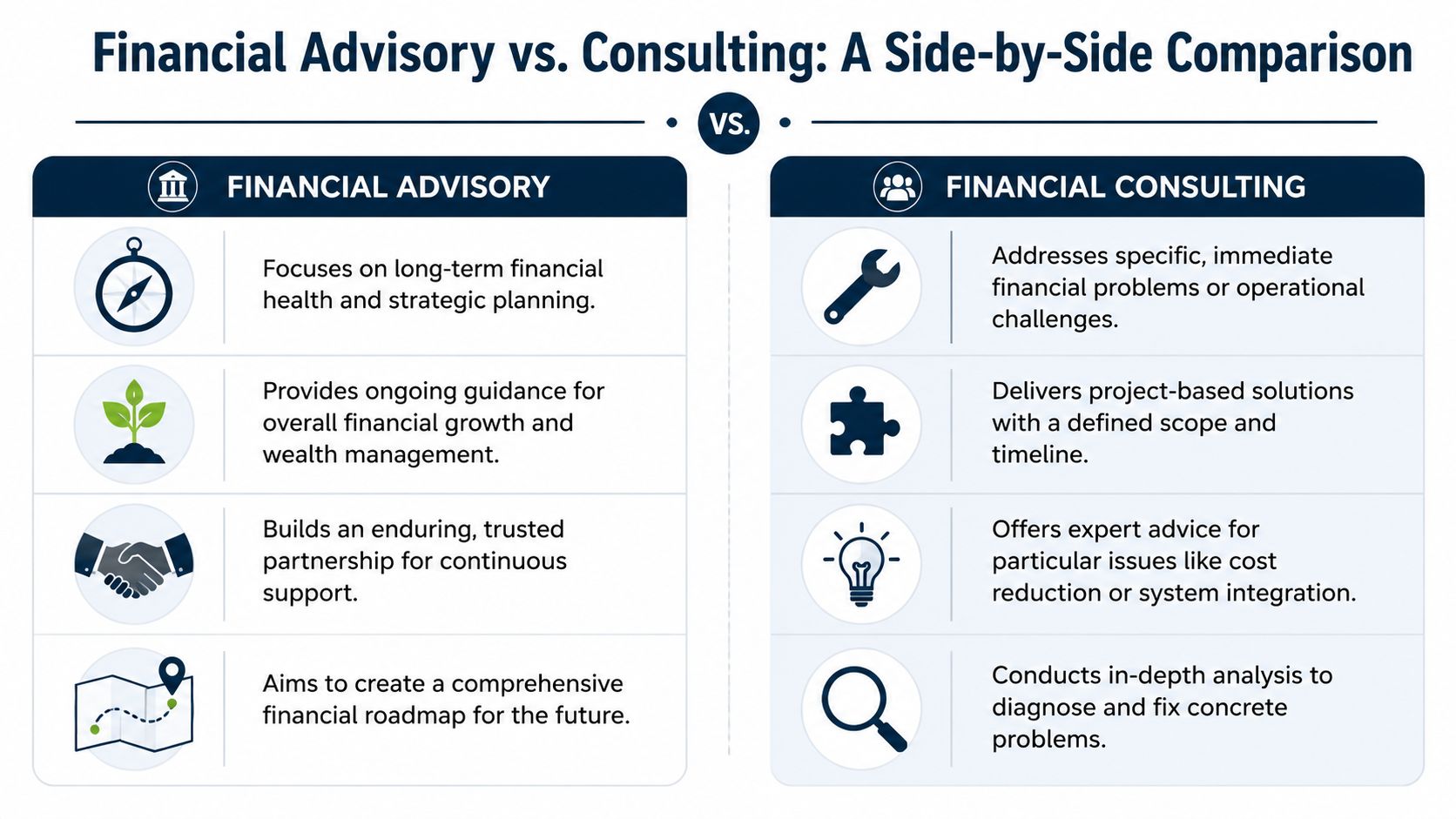

That's the easiest way to understand financial advisory vs consulting.

Financial advisory is your roadmap. It helps you decide where you're going, what route makes sense, and whether the business can handle the trip.

Financial consulting is your repair manual. You pull it out when something specific needs fixing, diagnosing, or rebuilding.

The difference in plain English

If you're trying to answer questions like these, you're usually in advisory territory:

- Growth questions: Should we hire another admin, estimator, or associate?

- Planning questions: Can we afford to expand, or will it squeeze cash?

- Performance questions: Which service line makes money?

If your issue sounds more like this, you're usually in consulting territory:

- Special project: We need a valuation because we may sell.

- Deep analysis: Margins dropped and we need to find out why.

- Big decision: We're looking at an acquisition, restructure, or major pricing reset.

Most owners don't need more reports. They need help turning reports into decisions.

More businesses are looking for that kind of support. The global financial advisory services market is projected to grow from USD 122.39 billion in 2026 to USD 161.19 billion by 2031, and services for SMEs are the fastest-growing segment, according to Mordor Intelligence's financial advisory services market report.

That tells you something important. Owners aren't just buying bookkeeping anymore. They're looking for judgment, direction, and help making better calls.

Financial Advisory Is Your Ongoing Growth Partner

Advisory works best when the business needs someone in the financial passenger seat on a regular basis.

Think of basic accounting as the rearview mirror. It tells you what happened. That matters. But it doesn't help much when you're asking what to do next. Advisory is closer to a GPS. It helps you choose the route before you make the turn.

What advisory looks like in real life

A good advisor usually stays close to a few core areas:

- Cash flow visibility: Not just what's in the bank today, but what's likely to happen over the next few weeks and months.

- Budgeting and forecasting: So hiring, equipment purchases, and marketing spend aren't guesses.

- KPI tracking: So you can see whether profit is coming from the right customers, jobs, or service lines.

- Decision support: You bring the business context. The advisor helps pressure-test the numbers.

For a law firm, that might mean tracking realization, collections, and partner draws. For a construction company, it could mean job costing, billing timing, and overhead recovery. For a medical practice, it may center on payroll pressure, provider productivity, and vendor creep.

What an advisor actually helps you decide

Here are the kinds of questions that fit an advisory relationship well:

Can we afford this hire?

Not “Do we have cash today?” but “Will this still make sense three months from now?”Is our pricing working?

Revenue can rise while margin slips. An advisor helps spot that early.Are we growing the right way?

Some businesses get bigger and less healthy at the same time.

That's why the relationship matters. Advisory isn't just about producing a monthly packet. It's about pattern recognition. Someone sees the same business month after month and notices what changed, what's drifting, and what needs attention.

Practical rule: If your question keeps coming back every month, you probably need advisory, not a one-time consulting project.

This also changes how owners think about risk. Financial firms often focus on revenue, margins, and cash, but many owners forget the operational side. If you run an advisory practice yourself, it's worth understanding basics like commercial coverage for financial advisors, because one claim or operational issue can disrupt more than a spreadsheet ever shows.

Founders and early-stage teams often need this same kind of steady guidance even more than larger companies do. That's why a resource like financial advisory for startups is useful. It frames advisory as a working relationship, not a pile of reports.

Financial Consulting Is Your Project-Based Problem Solver

Consulting is different. You bring in a consultant when you have a defined problem, a sharp question, or a time-sensitive project that needs specialist attention.

This work is narrower and more intense. It has a start date, a finish line, and a concrete deliverable.

When consulting makes sense

Consulting usually fits situations like these:

- A possible sale: You want to understand business value, weaknesses in the financial story, and what a buyer will question.

- A profit leak: Revenue is steady, but margins dropped and no one can explain where the money went.

- A financing event: You need stronger analysis before talking to lenders or investors.

- A change project: Compensation, reporting structure, or decision rights need to be rebuilt.

This kind of engagement is less about companionship and more about precision. The consultant comes in, gets deep fast, and works the issue until there's an answer.

The work is technical on purpose

Financial advisory consulting often leans hard into valuation modeling, scenario analysis, and transaction support. These projects typically last 3 to 6 months and focus on high-precision work, according to this financial advisory vs consulting breakdown. The same analysis cites a 2023 McKinsey report saying this specialized approach can achieve 20% to 30% higher accuracy in deal valuation predictions than general consultants.

That matters if you're trying to value a business, test debt capacity, or understand whether an acquisition target is worth chasing. A broad operator can give you sensible advice. A financial consultant should be able to build the model, challenge the assumptions, and show where the risk sits.

A consultant should leave you with a decision, a model, or a plan you can actually use. If all you get is a deck, the project probably wasn't scoped well.

Some consulting work also overlaps with org structure. If a business is changing reporting lines, flattening management, or trying to fix role confusion, the money side and people side often move together. That's why pieces on effective organizational redesign strategies can be useful context alongside the financial analysis.

And if you're comparing these roles from the talent side, financial analyst consultant salary helps explain why project-based finance specialists are usually priced differently from ongoing advisory support.

Comparing Advisory vs Consulting Side-by-Side

Most owners don't need a lecture here. They need a clean side-by-side comparison they can use in five minutes.

| Criterion | Financial Advisory | Financial Consulting |

|---|---|---|

| Primary role | Ongoing financial guide | Project-based specialist |

| Best for | Recurring decisions and long-term planning | A defined problem or major event |

| Relationship | Continuous and collaborative | Intensive, narrower, and temporary |

| Time frame | Ongoing | Usually tied to a set project scope |

| Common work | Forecasting, budgeting, KPI reviews, cash planning | Valuation, scenario modeling, due diligence, profitability deep dives |

| Typical output | Better decision-making over time | A solution, diagnosis, or project deliverable |

| Pricing style | Often monthly or recurring | Often project-based |

Scope and relationship

Advisory is broader. The advisor helps you run the business with more clarity over time.

Consulting is narrower. The consultant is there to attack a specific issue. Once the issue is solved, the engagement often ends.

A simple way to test this is to ask yourself one question: Will this issue still be with us after the project ends? If the answer is yes, you probably need some level of advisory around it.

Timeline and engagement

Advisory relationships often unfold through regular check-ins, recurring dashboards, and frequent decision support. The work builds on itself because each month adds context.

Consulting work is built around a project calendar. There's usually a defined question, a workplan, and a final recommendation.

That same difference shows up in other professional fields too. The discussion around navigating high-stakes people decisions with Paradigm makes a similar distinction on the HR side. Ongoing advisory supports repeat decisions. Consulting is usually called in for a sharper event or transition.

Pricing and how owners experience it

Owners usually feel advisory as a steady operating cost. That can be easier to budget for because it becomes part of the monthly rhythm.

Consulting often feels more expensive in the moment because it's concentrated. But that doesn't mean it's the wrong choice. If you're dealing with a valuation, acquisition review, or profitability problem, a targeted project can save far more than it costs by preventing a bad decision.

Outcome and what success looks like

Success in advisory is cumulative. You don't always feel it in one dramatic moment. You feel it when decisions get faster, surprises get smaller, and the business becomes easier to steer.

Success in consulting is more visible. The project answers a question, uncovers a problem, or gives you a model and recommendation you didn't have before.

If advisory is about running the business better, consulting is about solving the issue that's blocking the next move.

Neither one is automatically better. They solve different problems. A key mistake is hiring a consultant when you need a steady financial partner, or expecting an advisor to magically produce a transaction-grade analysis on short notice.

Real-World Scenarios for Philadelphia Businesses

This gets clearer when you put it into local, everyday business situations.

A contractor in West Chester

A contractor is busy. Jobs are coming in. The owner is frustrated because cash still pinches between billing cycles, supplier payments, and payroll.

That owner usually needs advisory first. The problem isn't one broken thing. It's ongoing visibility. They need better forecasting, cleaner job costing, and a clearer view of when cash gets tight.

If that same contractor later wants to buy a smaller competitor, that turns into consulting. Now the issue is valuation, deal structure, and due diligence.

A healthcare practice adding providers

A practice with one location is thinking about adding another provider or expanding space. The owner wants to know if patient volume, payroll, and overhead can support the move.

That's usually advisory. The question lives in planning. The owner needs regular financial guidance, not just a one-time opinion.

But if the practice is restructuring compensation, untangling a messy entity setup, or preparing for a transaction, that's when consulting becomes the better fit.

A professional services firm with uneven profit

A law firm, agency, or IT company can look healthy from the outside and still have margin problems underneath. One client type may be profitable while another eats time and cash.

That often starts with advisory, especially if the owner needs recurring visibility into utilization, realization, pricing, or staffing decisions.

If leadership decides to redesign partner compensation or rebuild how incentives work, that becomes a consulting assignment because it's a defined project with a difficult endpoint.

A lot of SMB pain sounds like a one-time problem at first. Then you look closer and realize the business needs a better financial operating system.

This is one reason many smaller companies hesitate before hiring outside help. A 2025 AICPA report showed that 68% of SMBs struggle with cash flow visibility, yet only 22% use external advisory, often because they think the cost will be too high, according to this analysis of consulting vs advisory for SMBs.

That hesitation is understandable. But it also creates a trap. Owners wait until stress is high, then hire for a crisis, when what they really needed months earlier was a lighter, ongoing advisory rhythm. If you're trying to sort through options locally, a practical starting point is reviewing what small business financial advisors near me should help with.

Getting the Best of Both Worlds with a Hybrid Model

For most small and midsize businesses, this isn't really an either-or decision.

The strongest setup is often a hybrid model. You keep ongoing advisory in place for regular planning, reporting, and decision support. Then you layer in consulting when a bigger event shows up, like a sale, restructuring, capital raise, or acquisition review.

Why the hybrid approach works

Small businesses don't operate in neat categories. One month you need cash flow forecasting. The next month you need a deeper pricing study. Six months later you might need a business valuation.

That's why a rigid split between financial advisory and consulting often fails in practice.

A 2026 Deloitte report noted a 28% rise in remote financial outsourcing, with AI blurring the line between advisory and consulting. It also noted predictive cash flow can reach up to 85% accuracy, according to this review of financial advisory consulting trends. In plain terms, owners can now get ongoing support and sharper project analysis from the same remote-friendly financial partner more easily than before.

What a practical hybrid can look like

One workable example is a three-part structure:

- Core accounting: Clean books, reconciliations, payroll coordination, and dependable monthly reporting.

- Profit optimization: Ongoing advisory around forecasting, KPIs, pricing, cash flow, and margin visibility.

- Exit strategy: Consulting support for valuation, deal readiness, and transition planning.

That's the basic logic behind MyOfficeOps. It combines bookkeeping, financial analytics, and CFO-level advisory with project-based support when the business reaches a bigger decision point.

The simplest way to choose

If you're still unsure, use this filter:

- Choose advisory when the business needs regular guidance.

- Choose consulting when there's a defined problem or event.

- Choose a hybrid when you need both better day-to-day decisions and occasional deep project work.

That last option is where many Philadelphia-area SMBs end up. Not because it seems especially advanced, but because it matches how real businesses work. Daily operations don't stop just because a major project appears. You still need cash visibility, payroll confidence, and clear reports while the bigger issue gets solved.

If your business needs clearer numbers, steadier cash flow insight, or a sharper plan for growth or exit, it may be time to talk with MyOfficeOps. They work with small and midsize businesses on bookkeeping, accounting, financial analytics, and CFO-level guidance, with project support when a valuation, transaction, or transition is on the table.