A cash flow forecasting template is like a crystal ball for your business's money. It shows you the cash coming in and going out over the next few weeks or months. Think of it as a simple tool to see what your bank account will look like in the future. It helps you make smart decisions instead of just guessing.

Why Your Business Needs a Financial Roadmap

Running a business without knowing your cash situation is like driving with your eyes closed. You might be moving, but you don't know if you're heading for a cliff. A cash flow forecast is your map. It gives you a clear view of the road ahead.

It helps you answer important questions before they become big problems:

- Can we afford to hire a new person next month?

- Will we have enough money for our big tax bill in three months?

- What happens if our biggest customer pays 30 days late?

A forecast turns these scary questions into simple plans. This isn't just about avoiding trouble; it's also about finding opportunities. When you know you'll have extra cash in a few months, you can plan to buy new equipment or start that marketing idea you've been thinking about.

A Real-World Example

I once worked with a coffee shop owner who was worried about the slow winter season. We sat down and made a simple cash flow forecast. It quickly showed a possible cash shortage coming in about three months, right when tourist season ended.

Because she saw it coming, she didn't panic. She made a plan.

She changed her staff schedule for the slow months, ran a "locals only" discount to bring in more business, and decided to wait until spring to buy a new espresso machine. She got through the winter just fine, all because her forecast gave her a heads-up.

This is the real power of a forecast. It’s not about guessing the future perfectly. It’s about giving yourself time to react and stay in control.

Tools for the Job

Most small businesses start with a simple spreadsheet. In fact, 80–90% of forecasts start in Excel or Google Sheets because they are flexible and free. While big companies might use fancy software, a good template is the perfect place to start.

Here are the main parts of a cash flow forecast and what they really mean.

Your Forecasting Template at a Glance

| Component | What It Means for You | Simple Example |

|---|---|---|

| Cash Inflows | All the money coming into your business. | Payments from customers, money from a loan. |

| Cash Outflows | All the money leaving your business. | Paying employees, rent, buying supplies. |

| Net Cash Flow | The difference between money in and money out for a period (like a month). | $10,000 In – $8,000 Out = $2,000 Net Cash Flow. |

| Opening/Closing Balance | Your bank balance at the start and end of the month. | Start with $5,000, add $2,000 net cash, end with $7,000. |

This simple setup gives you a powerful look at your financial health.

For an even better financial roadmap, think about integrating payment and accounting systems. This can automatically put clean, accurate information into your forecast. Good financial planning for business owners is the foundation, and a forecast is the first big step.

Getting Started with the Free Template

Okay, let's get to it. Seeing your own numbers in a clean spreadsheet is where the magic happens. We’ve built a simple and free cash flow forecasting template to get you started easily.

This isn't a complicated file with a hundred tabs you'll never use. It’s a simple template for Excel and Google Sheets with all the formulas already set up. Your job is just to put in your numbers.

Opening and Setting Up the Template

First, download the template and open it. You'll see it’s organized by month, with clear sections for money coming in and money going out. We'll go through it step by step, so don't worry.

The very first number to enter is your opening bank balance. This is just how much cash you have in your business bank account right now. Think of it as your starting line.

A Simple Example: A Freelance Web Designer

Let's imagine we're a freelance web designer named Alex. Alex is ready to plan out the next few months and just downloaded this template.

Alex’s first step is to check the business bank account. The balance is $8,500. Alex finds the cell for "Opening Balance" for the first month (let's say July) and types in that number. That's it. Step one is done.

This starting number is the base for your whole forecast. Every bit of money in and out that we add from now on will build on this number, showing you how your cash changes over time.

A forecast is only as good as its starting point. Always begin with the real balance from your bank statement to make sure everything else is accurate.

Identifying Your Cash Categories

Next, you’ll see rows for different types of income and expenses. These are your cash categories, and you should change them to fit your business. For Alex the web designer, income might be split into:

- Project Payments: Money from finishing websites.

- Monthly Retainers: Regular payments for helping clients with their sites.

- Consulting Fees: Money from one-off advice sessions.

For expenses, the list might include things like software subscriptions ($150/month for Adobe tools), marketing costs, and internet bills. These categories help you see exactly where your money comes from and where it goes.

Having good bookkeeping really helps here. The categories in your forecast should match the ones in your accounting system. If you want to learn more about organizing your finances, check out our guide on what is a chart of accounts. It's the backbone of any good financial system.

By filling in just this basic info—your starting balance and your categories—you’ve already made the template your own. You've turned a blank sheet into a tool that shows what your business is doing. Now, you're ready to start adding your expected income and expenses.

How to Fill Out Your Forecast

Okay, you have the template open and your starting balance is in. Now it's time to fill in the numbers. Don't worry, you don't need to be a psychic. We're just going to make smart guesses based on what you already know about your business.

Let's break this down into two simple parts: money coming in (inflows) and money going out (outflows).

Projecting Your Cash Inflows

Cash inflows are all the ways money comes into your business. For most businesses, this is mainly from sales, but it can include other things too. The most important thing is to be realistic, not just hopeful. Your past sales are your best guide.

Start by looking at your records. What did you make this time last year? How about last quarter? History is a great teacher when you're forecasting.

Here are the most common places to find the numbers you need:

- Outstanding Invoices: Look at your accounting system and list every bill you've sent that hasn't been paid. Check the due dates—this tells you which month to expect the payment.

- Recurring Revenue: Do you have clients who pay you every month? This is the easiest income to forecast because it's predictable. Add it up and put it in for each month.

- Sales Pipeline: Look at your potential new deals. If you have a 75% chance of closing a $10,000 project in August, you could conservatively guess you'll get $7,500 that month.

For businesses with sales that are harder to predict, like a new online store, you’ll have to make an educated guess. Look at your marketing plans. If you're spending $500 on ads and you usually get $3 in sales for every $1 you spend, you can forecast $1,500 in sales. The more you learn about different cash flow forecasting techniques, the better your guesses will be.

Nailing Down Your Cash Outflows

Now for the other side: money going out. This part is usually easier because many of your costs are the same each month. Outflows are simply all the bills you pay to keep the business running.

I like to split them into two groups:

- Fixed Costs: These are the bills that are the same every month, no matter what. Think rent, insurance, and software payments. They're easy to plan for.

- Variable Costs: These expenses change with your business activity. If you sell more T-shirts, your shipping costs go up. If you start a big ad campaign, your marketing costs will be higher.

To make sure you don't miss anything, grab your bank and credit card statements from the last three months. Go through them line by line and list every single expense. This is a great way to get a full picture of your spending.

So many business owners I work with are shocked to find "forgotten" subscriptions or small costs that add up. Looking at your statements is the only way to make sure your forecast is based on reality.

To help you get started, here's a checklist of common business expenses to include in your cash flow forecasting template.

Common Business Expenses Checklist

- Rent or Mortgage: Your office or store space.

- Payroll: Paychecks and taxes for your team.

- Utilities: Electricity, gas, water, and internet.

- Software & Subscriptions: All your monthly or yearly software fees.

- Marketing & Advertising: Ad costs and social media tools.

- Inventory or Supplies: The cost of the products you sell or materials you need.

- Insurance: Business, property, and health insurance.

- Professional Fees: Money paid to lawyers or accountants.

- Taxes: Don't forget sales tax and quarterly taxes.

- Loan Payments: Any regular payments on business loans.

A typical forecast will track everything from your starting cash to your payments and sales. But as your business grows, updating a spreadsheet by hand can take a lot of time. For some, using bank statement converter software can automate getting old data into your spreadsheet.

The main idea is to add up your starting balance with all the money you expect to come in and go out. By putting in these numbers, you're turning a blank spreadsheet into a clear picture of your business's financial future.

Understanding What Your Forecast Is Telling You

So, you've done the work and filled out the template. That's a huge step, but the real value is in learning to read the story your forecast is telling you. This spreadsheet is now your financial map, showing you the road ahead.

Let's start with the most important number on the sheet: the closing cash balance. Find that row at the bottom. This number shows you how much cash you are predicted to have in the bank at the end of each month.

Watching this number change from month to month is like checking your business's pulse. If the balance is always growing, that's a sign of a healthy business. But if you see that number getting low a few months from now, that's your early warning system going off.

Spotting a Cash Gap Before It Happens

The main reason we do this is to see trouble coming from far away. A cash gap happens when your costs for a month are higher than your income, leaving you with less money than you started with. Your forecast can show you this problem months before it happens.

When you see a future month's closing balance looking low, you have time to do something about it. You're no longer reacting to a surprise; you're planning ahead. This is where your template becomes a real decision-making tool.

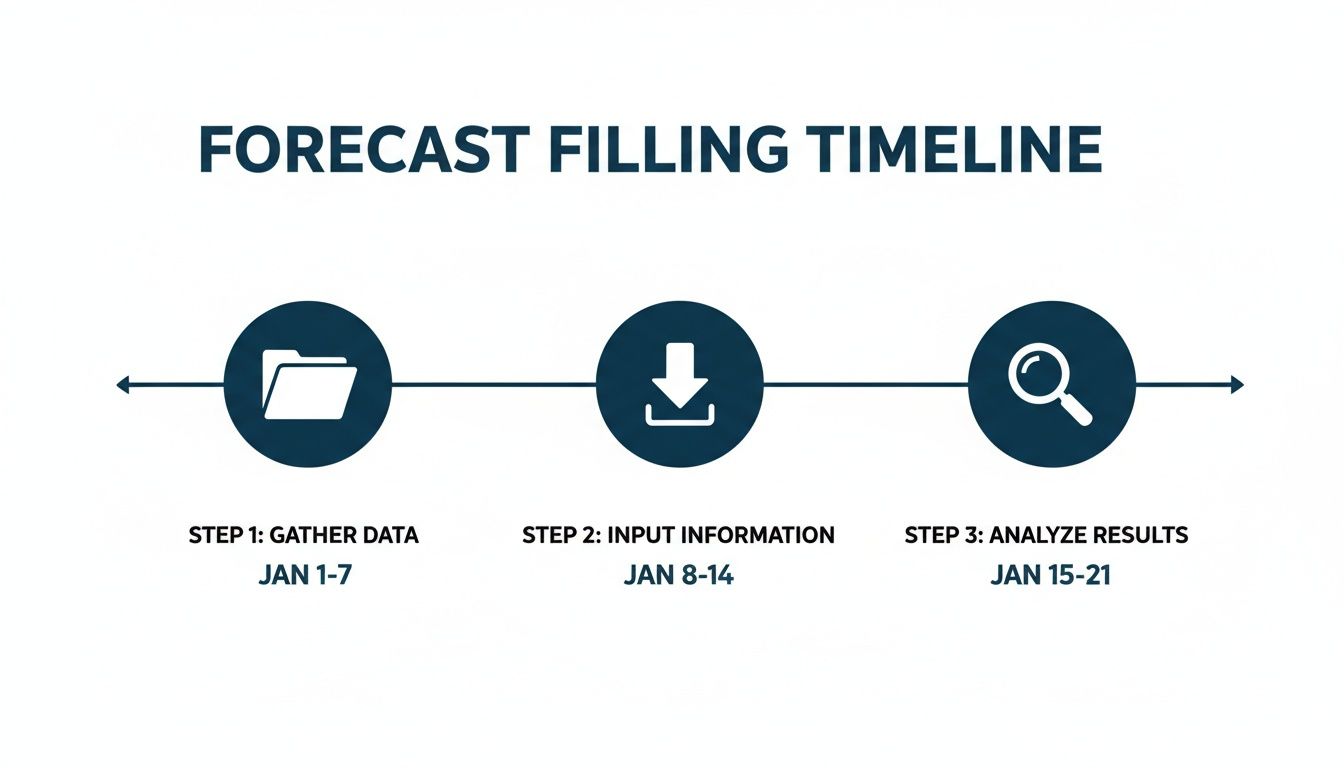

This timeline shows the simple flow from getting your data to figuring out what it means for your business.

The key is that looking at the numbers isn't the last step. It's how you turn that data into smart business decisions.

Planning for Different Scenarios

Now for the really cool part: planning for "what if?" Business is never predictable, so your plan shouldn't be either. This is where you can ask questions and see the impact on your cash without risking any real money.

Start by saving a few copies of your forecast. I suggest making three versions:

- Most Likely Case: This is the forecast you just built, based on your most realistic guesses.

- Best Case: What if that big deal you're hoping for actually happens? What if your new marketing plan doubles your sales?

- Worst Case: This is the most important one. What if a big client pays 60 days late? What if your supply costs suddenly jump by 20%?

Let’s take a construction company as an example. The owner could plan a "worst-case" scenario by delaying a project's payment by a month and increasing material costs. The forecast would instantly show if that creates a cash problem, giving them time to get a loan or delay buying new equipment.

By making these different versions, you're not just hoping for the best—you're getting ready for the worst. This process takes away the fear and gives you a real plan, no matter what happens.

How Far Out Should You Look

It's tempting to forecast years ahead, but it gets less accurate over time. A forecast's error gets bigger the further out you look. That's why it's a good idea to break your forecast into different time frames.

A short-term forecast, for the next 0–13 weeks, should be very detailed and updated often. For longer periods, like up to 12 months, your forecast can focus on bigger trends and ideas.

Companies that use good templates and connect them to their bank and accounting data often see their forecast mistakes drop by 20–40% in that important short-term period. You can read more about these best practices from J.P. Morgan.

By reading your closing balance, spotting possible problems, and planning for different scenarios, you are taking control of your financial future. Your cash flow forecasting template becomes less of a spreadsheet and more of a partner in your business.

Common Forecasting Mistakes and Pro Tips

Making your first forecast is a big step, but it’s easy to make a few common mistakes. Think of this as some advice from someone who’s seen it all. Let's look at the simple traps that can make your forecast less helpful, and some easy tips to make it a powerful tool.

One of the biggest mistakes I see is being too optimistic. It's your business, so of course you're excited! But when your sales guesses are based more on hope than on history, your whole forecast is no longer trustworthy. You have to base your numbers on reality, even if it feels a little boring at first.

Another common mistake? Forgetting about taxes. This happens more than you’d think. I once worked with a restaurant owner who had a great quarter but forgot to save cash for his tax payment. He had to scramble at the last minute and almost couldn't pay his employees. It was a stressful lesson in planning for all the money going out, not just the daily stuff.

Simple Mistakes That Can Derail Your Forecast

Besides being too optimistic or forgetting taxes, a few other slip-ups can mess up your numbers. The good news is they are all easy to fix once you know to look for them.

- Ignoring Seasonality: Many businesses have busy and slow times. A landscaper is busy in the spring but slow in the winter. Forgetting these cycles leads to bad surprises when sales drop right on schedule.

- Confusing Profit with Cash: A sale is great, but the money isn't in your bank until the customer pays. Your forecast needs to show when the cash actually arrives, not just when you make the sale. This is a very important difference.

- The "Set It and Forget It" Attitude: A forecast isn't something you make once and then ignore. It's a living tool. To be useful, it needs regular updates.

The best cash flow forecasting template is one that you look at and change regularly. Think of it less like a report and more like a live dashboard for your business's money.

An old forecast is almost as bad as no forecast at all. It can make you feel safe when you aren't, and lead you to make bad decisions based on old information.

Pro Tips for a More Powerful Forecast

Once you've avoided the common mistakes, you can start using some smarter strategies to make your forecast even better. These aren't complicated tricks; they're just good habits that turn your spreadsheet into a real asset.

A great first step is to link your cash flow forecasting template to your accounting software. Tools like QuickBooks or Xero can often export data that you can easily put into your template. This saves a lot of time and reduces mistakes. It also helps you quickly compare your forecasted numbers to your real results, which is how you get better at this.

Another great tip is to build in a buffer for surprises. No forecast is perfect. Equipment will break, or a surprise bill will arrive. By including a "contingency" line in your outflows, you're building a cushion for the unknown. Even 5% of your total expenses can make a huge difference when handling surprises.

Finally, make your forecast visual. Use the chart tools in Excel or Google Sheets to create a simple line graph of your closing cash balance over time. Seeing that line go up or down is often much clearer than looking at a grid of numbers. It helps you and your team quickly understand the story your forecast is telling.

Clearing Up Common Questions About Cash Flow Forecasting

Whenever I talk to business owners about forecasting, the same few questions always come up. They’re great questions, and the answers are usually simpler than people think. Getting these basics right is like learning to ride a bike—a few key pointers make all the difference.

Let’s clear up some of that confusion right now.

How Often Should I Update My Cash Flow Forecast?

Think of your forecast as a living document, not something you create once and put in a drawer. For most small businesses, updating it once a month is perfect. It gives you a chance to compare what you thought would happen with what actually happened.

That monthly check-in is where you really start to learn. You’ll see patterns in your business you never noticed before, and your guesses will get more accurate over time.

However, if your business is going through a big change—like growing fast or hitting a slow patch—or if cash is very tight, you should update it more often. Checking it weekly is a smart move in those situations. The most important thing is to be consistent. Put it on your calendar and treat it like an important meeting.

What Is the Difference Between a Cash Flow Forecast and a Budget?

This is a great question because people mix these two up all the time, but they do very different jobs. It's like the difference between a grocery list and a meal plan.

A budget is your plan or your goal. It’s where you set spending limits. For example, a budget says, "We will not spend more than $500 on ads this month."

A cash flow forecast, on the other hand, is all about timing. It predicts when that $500 will actually leave your bank account. More importantly, it predicts when the money from the new customers you got with those ads will finally arrive.

You really need both. The budget is your map, but the cash flow forecast tells you if you have enough gas in the tank to make the trip.

My Sales Are Unpredictable. How Can I Possibly Forecast Them?

I hear this one all the time, especially from new businesses. The key is to stop thinking of forecasting as predicting the future perfectly. It’s not about being right all the time; it's about being prepared for what might happen.

Even if your sales seem random, your own history is the best place to find clues. Look back at your records. You’ll probably see some kind of pattern, even if it’s just a busy season and a slow season. Use that as your starting point.

From there, don't just make one forecast. Make three:

- Worst-Case: What happens if sales drop 20%? How does that change your cash?

- Realistic Case: This is your most likely plan, based on past sales and current leads.

- Best-Case: What if that huge project you quoted comes through? What if your new marketing works really well?

This simple planning turns worry about the future into a real, actionable plan. You’ll know what to do if things go wrong and how to take advantage if things go great.

Can I Use This Template for My Personal Finances?

Yes, absolutely! The ideas in a cash flow forecasting template work the same way for a company or a household.

Your 'inflows' are just your paychecks and any other money you get. Your 'outflows' are your bills like rent or a mortgage, plus all your other spending on things like food, gas, and fun.

Honestly, using a forecast for your personal life is a great idea. It shows you exactly where your money is going and helps you save for big goals, like buying a house or going on vacation. It brings the same clarity and control to your personal life that it brings to a business.

Feeling like your forecast is telling you a story you don't have time to read? At MyOfficeOps, we turn those numbers into a clear plan for growth. Our team handles the bookkeeping and forecasting so you can focus on running your business, not just your spreadsheet.

Let's build a clearer financial future for your business together. Schedule a call with us at https://myofficeops.com today.