You look at your bank account and think, “We're fine.” Then your profit and loss statement lands in your inbox and says profit is down. Or the reverse happens. The P&L looks solid, but cash feels tight and payroll is coming up fast.

That gap is where a lot of small business owners get stuck.

It happens all the time in service firms, clinics, and construction businesses because money rarely moves in a clean straight line. A big client prepays a project. A supplier invoice hits late. Payroll lands before you bill a milestone. Retainers make one month look great, then the next month looks weak for no real reason. If you use accrual accounting, which is usually the right choice once a business gets more complex, the books are trying to show when income was earned and when costs were incurred, not just when cash moved. If you need a plain-English refresher, this guide to how accrual accounting works is a useful starting point.

That's why budget vs actual reporting matters.

Used badly, it becomes a stale report you glance at after month-end and then ignore. Used well, it becomes one of the simplest tools for making better decisions on hiring, pricing, project staffing, and spending. It helps you answer the question behind the numbers: Is this a real change in the business, or just a short-term wobble?

For owners with lumpy revenue, that difference is everything. A single month can look like a disaster when the trend is fine. Or a month can look strong while a margin problem is building underneath.

Why Your Bank Account and Profit Statement Tell Different Stories

A construction contractor finishes part of a job in June, sends the invoice, and gets paid in July. The bank account looks better in July. But the work that created that revenue happened in June. Meanwhile, materials for another job may have been purchased early, so cash went out before the matching revenue showed up.

A consulting firm runs into the same kind of mismatch. A client pays a deposit upfront. Cash jumps immediately. But that doesn't always mean the firm earned all of that money yet. The team still has to deliver the work over time.

That's why owners can feel like the business is sending mixed signals. The bank balance answers one question. “How much cash do we have right now?” The profit statement answers a different one. “Did the work we performed during this period produce profit?”

Those are both important questions. They're just not the same question.

| What you're looking at | What it tells you | What it can miss |

|---|---|---|

| Bank account | Cash available today | Unpaid bills, revenue earned but not yet collected, timing issues |

| Profit and loss statement | Revenue and expenses matched to the work period | Short-term cash pressure |

| Budget vs actual report | Where results differed from plan and where to investigate | It still needs interpretation, not just a quick glance |

Why this gets worse in lumpy businesses

If you run a business with project billing, grants, retainers, insurance reimbursements, or seasonal labor, your numbers naturally jump around. One large invoice can make a month look great. One delayed payment can make the next month look terrible.

That doesn't mean the business is broken. It means timing matters.

A useful budget vs actual report connects cash reality, accounting reality, and operating reality. You need all three if you want to make calm decisions.

The report that bridges the gap

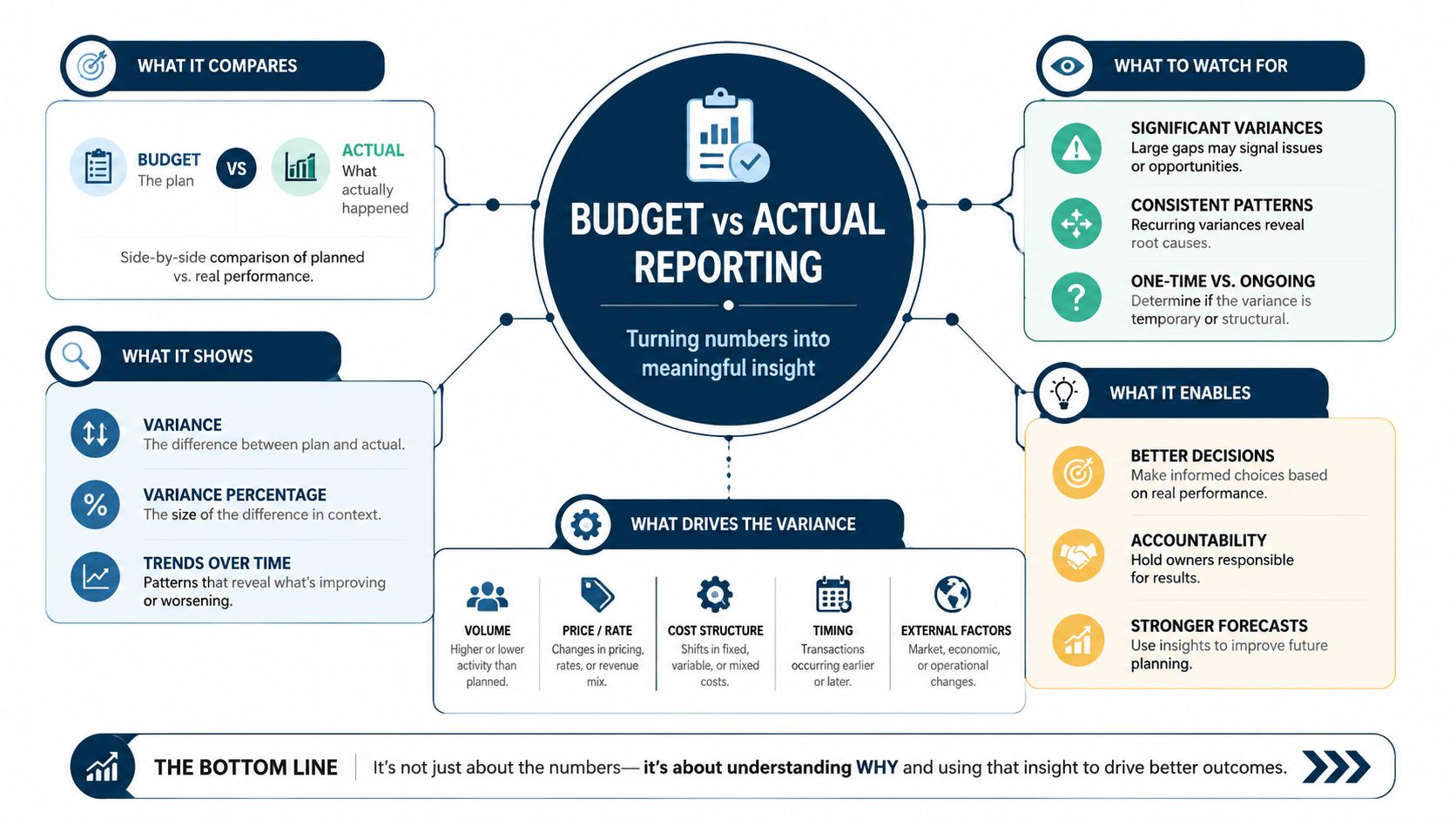

Budget vs actual reporting gives you a middle layer between your plan and what happened. It shows where the business went off script. Furthermore, it gives you a way to ask the right follow-up questions.

If payroll is higher than expected, did you add people, pay overtime, or process a pay cycle that landed earlier than usual? If revenue is behind budget, did demand soften, or is billing delayed by paperwork, approvals, or a client milestone that slipped a few days?

Without that lens, owners tend to overreact to noise or miss the actual signal.

What Budget vs Actual Reporting Really Tells You

Budget vs actual reporting is often considered a scoreboard. It's closer to a map.

Your budget is the route you planned to take. Your actuals are where the car really went. The variance is the detour. Sometimes the detour is harmless. Sometimes it means the original route no longer works.

That's why this report matters. It doesn't just tell you that something changed. It tells you where to look.

The three parts that matter

Here's the simple version:

- Budget: Your best plan for revenue, payroll, overhead, and profit.

- Actuals: What your accounting system says really happened in that same period.

- Variance: The gap between the two.

A positive variance isn't always good. A negative variance isn't always bad. It depends on the line item and the reason.

For example, if software expense is over budget, that might be sloppy spending. Or it might mean you added a tool that helps your team deliver faster. If revenue is ahead of budget, that sounds great, but it could also mean one unusually large project is masking weak new sales.

Why owners misuse the report

The most common mistake is treating the report like a report card. Red means bad. Green means good. That's too simple.

A better way to think about it is this:

Practical rule: A variance is a question, not a verdict.

The report should push you toward decisions. Should you hire now or wait? Raise prices or hold? Push collections harder? Rebid work? Delay equipment purchases? Review time tracking? Tighten purchasing approvals?

That's when budget vs actual reporting becomes useful. Not when it tells you the past in prettier formatting, but when it helps you change what happens next.

How to Build Your First Budget vs Actual Report

You don't need fancy software to start. If you have accounting software and a spreadsheet, you can build a useful first version this week.

The goal isn't to make it perfect. The goal is to make it readable enough that you can spot what needs attention.

Step one, line up the same period

Pull your budgeted profit and loss for the period you want to review. Then pull your actual profit and loss for that exact same period.

That “same period” part matters more than people think. If your budget is monthly, compare monthly. If your budget is quarterly, compare quarterly. If your books aren't closed yet, wait until they're cleaned up enough that the numbers mean something.

A simple setup looks like this:

| Account | Budget | Actual | Variance |

|---|---|---|---|

| Revenue | planned amount | actual amount | actual minus budget |

| Payroll | planned amount | actual amount | actual minus budget |

| Rent | planned amount | actual amount | actual minus budget |

| Net profit | planned amount | actual amount | actual minus budget |

If you want help before opening a spreadsheet, this guide on how to create a budget can help you build the planning side first.

Step two, keep your chart of accounts clean

A significant challenge for small businesses arises when categories diverge. If your budget has one line for “office expense” but your actuals split that into software, supplies, phones, and subscriptions, your report gets messy fast.

Try to make sure the budget and actual report use the same categories. You don't need dozens of lines. You need meaningful lines.

Good starter groups usually include:

- Revenue categories: Separate major revenue streams if they behave differently.

- Direct costs: Materials, subcontractors, labor tied to delivery.

- Operating expenses: Payroll, rent, software, insurance, marketing.

- Owner decision lines: The items you control and review.

If you want extra grounding on the planning side, there's some solid practical financial planning advice that explains how budgeting and forecasting support each other.

Step three, add comments, not just math

Most first reports stop at the variance column. Don't stop there. Add a short note beside any line that matters.

A note can be plain language:

- Revenue behind budget: One client milestone moved into next month

- Payroll over budget: Added temporary admin coverage

- Materials over budget: Supplier pricing changed on active jobs

- Marketing under budget: Campaign launch delayed

Those comments matter because a report without explanations turns into a guessing game. A simple line of context often tells you whether the issue needs action now, later, or not at all.

The best early version is not the prettiest one. It's the one your team will actually use every month.

The Art of Variance Analysis What to Actually Look For

A variance by itself doesn't help much. It only tells you where to point your flashlight.

Critical analysis begins when you ask why the number moved. For small businesses, especially firms with uneven billing or project work, budget vs actual reporting then either becomes a decision tool or dies as a spreadsheet chore.

One challenge comes up again and again. How do you separate timing variance from a real operating change? That question is often under-answered in basic finance content. A useful approach is to focus on year-to-date variances because that minimizes timing differences and better predicts annual results, then classify what remains by timing, volume, rate, or scope, each of which calls for a different action, as noted by Kevin Harper CPA in this discussion of effective budget vs actual reports.

Start with one question

Before you dig into any line, ask this:

Will this variance reverse on its own, or is it telling me the business has changed?

That one question keeps you from wasting energy on noise.

If a client paid a few days late and revenue slipped into the next month, that's different from a client cutting work, a competitor taking share, or your close rate falling. The first issue may need no action beyond collection follow-up. The second changes your hiring plan, pricing plan, and sales targets.

Use a simple four-part framework

This framework works because it ties each type of variance to a different response.

Timing

Timing variances happen when income or expenses land in a different period than expected.

Examples:

- A project invoice goes out later than planned

- A vendor bill hits after month-end

- Payroll falls into a different reporting cutoff

- Insurance renews in a different month than budgeted

Typical action: verify cutoff, billing date, and accruals. Then look at the year-to-date view before making a big decision.

Volume

Volume variances come from doing more or less business than planned.

Examples:

- Fewer patient visits in a clinic

- Fewer billable hours in a service firm

- More jobs completed than expected

- Lower unit sales in a product line

Typical action: review demand, staffing, scheduling, and sales pipeline.

Rate

Rate variances show up when the price per unit changed.

Examples:

- Material cost per unit increased

- Hourly labor cost rose

- Realized billing rate came in lower than planned

- Software subscriptions cost more than expected

Typical action: check pricing, vendor terms, purchasing discipline, and gross margin assumptions.

Scope

Scope variances happen when the business is doing work that wasn't in the original plan.

Examples:

- A project expands

- You add a service line

- You hire earlier than planned

- A clinic adds a provider or new equipment workflow

Typical action: update the budget or move to a refreshed forecast. Don't keep judging new reality against an old plan.

A simple example from a service business

Say a law firm budgets for a certain level of monthly fee revenue and comes in below budget. The wrong reaction is to panic and freeze spending immediately.

The better sequence looks like this:

- Check whether work was performed but not billed yet.

- Look at year-to-date revenue, not just the month.

- Ask whether hours were down, rates were down, or realization slipped.

- Decide whether the problem is collections, utilization, pricing, or client demand.

That's variance analysis. It's close cousin work to root cause analysis in data, where the point isn't to stare at a result but to identify the driver behind it.

What to do after you classify it

Once you know the type, the action becomes clearer.

| Variance type | What it usually means | Best next move |

|---|---|---|

| Timing | Month is noisy, trend may still be fine | Confirm dates, billing, accruals, then check YTD |

| Volume | Demand or output changed | Review sales, staffing, and capacity |

| Rate | Price or unit cost changed | Revisit pricing, vendors, and margins |

| Scope | Business moved beyond original plan | Reforecast and update expectations |

Most bad reactions happen because owners try to solve a timing problem with an operating decision.

That's how businesses end up cutting useful spend, delaying hires they need, or pushing discounts just because one month looked off.

If you only remember one thing from this section, make it this: classify first, act second.

If you want a broader explainer on the mechanics behind the process, this overview of variance analysis in budgeting is worth bookmarking.

Budget vs Actual Reporting in Your Industry

The same report looks different depending on how your business earns money. The lines may be similar. The meaning behind them usually isn't.

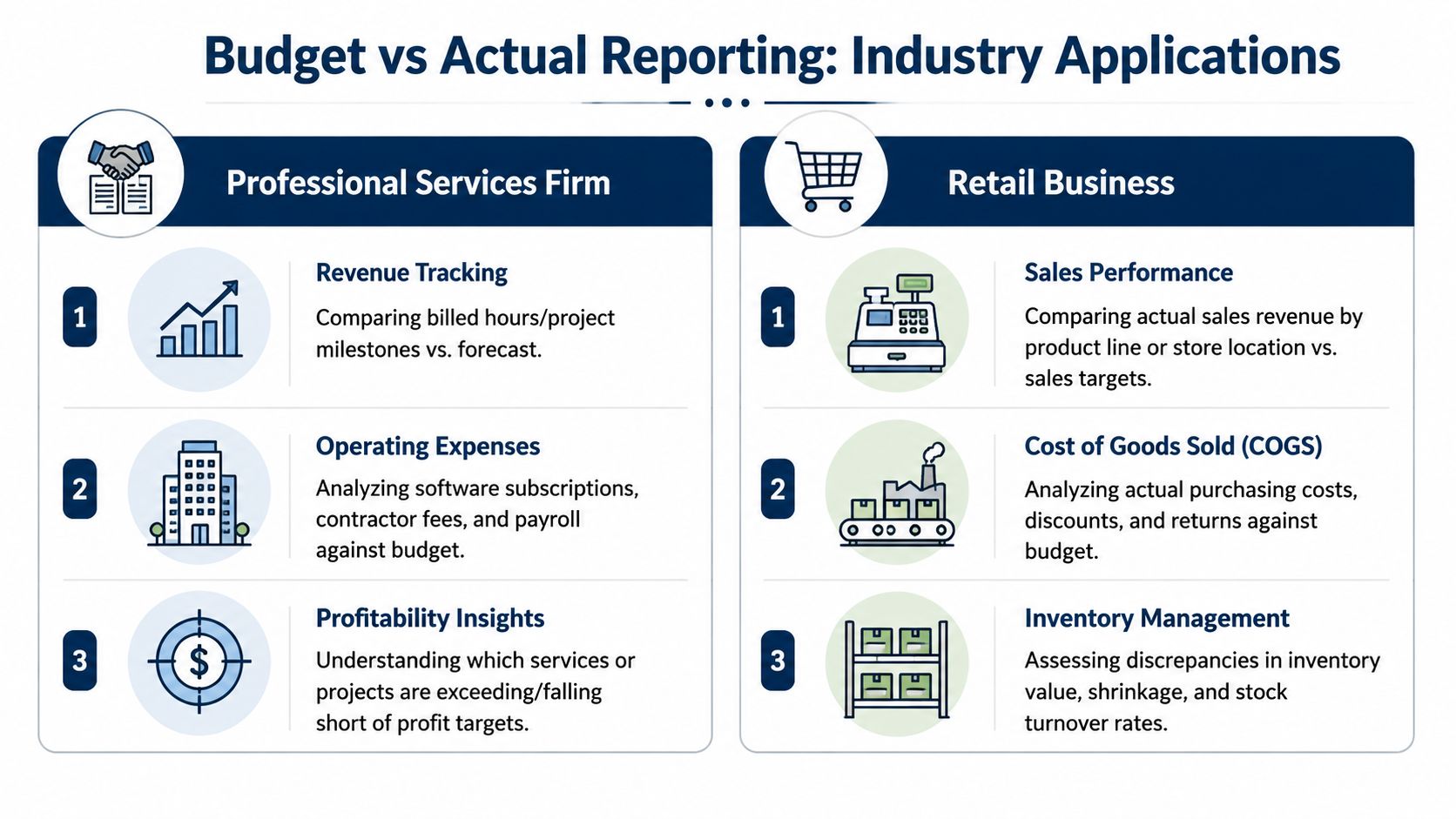

Professional services

A marketing agency, IT firm, or law practice usually lives and dies by capacity and realization. Revenue misses often trace back to one of a few drivers: fewer billable hours, lower billing rates, write-downs, or delayed invoicing.

A useful report here doesn't just compare revenue and payroll. It looks at the relationship between them. If payroll stayed on plan but revenue fell short, the owner should ask whether the team was underutilized, work wasn't billed promptly, or projects took longer than expected.

In service businesses, a revenue variance often starts as a time-use problem before it shows up as a profit problem.

Healthcare practices and clinics

A clinic can look busy all month and still miss budget. Why? Because volume alone doesn't tell the whole story. Reimbursement timing, payer mix, scheduling gaps, and supply costs all shape the final number.

A practical clinic review might ask:

- Were patient visits on target?

- Did collections lag behind services provided?

- Did supply costs rise faster than expected?

- Did overtime creep in because scheduling was uneven?

That kind of review helps the owner decide whether to adjust staffing, tighten scheduling, or dig into billing follow-up.

Construction and trades

Budget vs actual reporting proves especially valuable. Construction businesses often deal with front-loaded costs, change orders, retainage, and billing schedules that don't match labor and material timing neatly.

A contractor might see one ugly month and assume the job is going bad. But the issue may be timing on billing or delayed paperwork. On the other hand, a job can appear fine until actual labor hours and material costs show that the original estimate is no longer holding.

That's why contractors need to tie company-level reporting back to job-level reality. If you're estimating electrical work, tools like Exayard electrical estimating software can help tighten the front-end assumptions that later flow into budget comparisons.

What changes by industry, and what doesn't

The categories you watch will vary. The discipline doesn't.

Across industries, the useful questions stay familiar:

- What changed?

- Is it timing or a true shift?

- Does it affect margin, cash, or both?

- What decision should we make now?

Common Pitfalls and How to Avoid Them

A lot of budget vs actual reporting fails for a simple reason. The report is technically correct but operationally useless.

The biggest culprit is the stale budget. In a stable environment, an annual budget can hold up well enough. In a fast-moving one, it can go out of date quickly. Modern management reporting puts more weight on collecting variance commentary alongside the numbers and using rolling, driver-based analysis instead of a static month-end report. That approach turns the process into a near-real-time workflow and can also help surface hidden accounting errors or missing accruals, as described in Keboola's write-up on budget vs actual variance analysis in management reporting.

Pitfall one, treating the budget like a fixed contract

A budget is a planning tool. It's not a sacred document.

If your pricing changed, your team grew, a major customer left, or your supply costs shifted, don't keep measuring the business against assumptions that no longer fit. Move to a refreshed forecast and mark the change clearly.

Pitfall two, chasing every small variance

Owners burn out on reporting when every line demands a meeting. That's not analysis. That's clutter.

Set a simple rule for what deserves discussion. You don't need a complicated formula. You just need consistency. Big strategic lines like revenue, payroll, direct costs, and margin usually matter more than tiny office supply swings.

Pitfall three, using the report to blame people

Once a report becomes a tool for catching mistakes and assigning fault, people stop giving honest commentary. Then the report gets quieter right when you need more truth.

A better monthly review sounds like this:

- What changed?

- What caused it?

- Is it temporary?

- What decision follows?

That tone gets better answers.

Pitfall four, ignoring accounting clean-up issues

Sometimes a variance isn't operational at all. It's a bookkeeping problem. Missing accruals, misclassified costs, duplicate bills, or delayed reconciliations can distort the story.

That's why comments matter. If the controller, bookkeeper, or outside accountant can flag “waiting on accrual” or “invoice posted late,” the owner doesn't waste time solving a fake operating problem.

A bad report creates drama. A good report reduces it.

Putting It All Together Your Reporting Rhythm

For most small businesses, the best reporting rhythm is simple. Review monthly for operating decisions. Review quarterly for bigger strategic calls.

Monthly review

Use the monthly review to catch what needs attention now. Keep the meeting short. Look at the handful of lines that drive the business.

A solid monthly discussion usually includes:

- revenue

- direct costs

- payroll

- overhead categories that move

- cash concerns

- short written comments on major variances

The key question is: What one decision should we make because of this report?

That might mean pushing invoices out faster, slowing hiring, raising prices on new work, reviewing overtime, or correcting a posting issue before it snowballs.

Quarterly review

Quarterly is the better time for bigger conversations. That's when you step back from the noise of one month and ask whether the business is tracking toward the year you expected.

Use that review to look at broader patterns:

- is demand changing

- are margins holding

- does the staffing plan still fit

- does pricing still make sense

- is the original budget still useful

For owners with lumpy revenue, this is often where clarity shows up. A rough month may not matter much in a quarterly pattern. A gradual decline that looked harmless month by month may become obvious.

Keep the process plain. Pull the report. Add comments. Classify the major variances. Decide what changes.

That's enough to turn budget vs actual reporting from a backward-looking scorecard into a tool you can run the business with.

If you want help building reports that are clear, useful, and tied to real decisions, MyOfficeOps helps small and midsize businesses turn messy financial data into practical guidance on cash flow, pricing, hiring, and profitability.