Let’s be honest—the word “budget” can make you want to close this tab. It often brings up images of tight spreadsheets and telling yourself “no” to every new idea. But that’s a common misunderstanding I see all the time.

A business budget isn’t about saying “no”; it’s about being in control.

Running a business without a plan for your money is like trying to drive across the country without a map. You might get somewhere eventually, but you’ll probably make a lot of wrong turns, run out of gas, and miss out on the best routes.

Why Your Business Needs a Budget

A budget is just a plan for your money. It shows you where your cash comes from and where it goes by adding up all your expected income and subtracting all your expected expenses. Think of it as a GPS for your business goals.

Putting You in the Driver’s Seat

A budget puts you in control of your company’s money. Instead of reacting to problems after they happen, you can see them coming and make changes ahead of time. It helps you answer big questions with real numbers, not just a gut feeling.

This simple plan helps you:

- Make Smarter Decisions: Should you hire a new person? Is it a good time to buy that new piece of equipment? Your budget will show you what you can actually afford.

- Spot Problems Early: If your marketing costs are going up faster than your sales, your budget will show you right away—not three months later when it’s a bigger problem.

- Secure Funding: If you ever need a loan or want to find investors, a good budget shows them you’re a serious business owner who knows your numbers.

Unfortunately, many business owners skip this step. A surprising 61 percent of small businesses don’t have a formal budget, which leaves them guessing. This statistic shows how common it is to “fly blind,” but it also shows you have a big chance to get ahead just by having a plan. You can explore more insights on these business finance trends to see why planning is so important.

It’s Simpler Than You Think

To prove that making a business budget isn’t scary or hard, let’s quickly look at its main parts. At its core, a budget just has a few pieces.

Your Budgeting Starting Blocks

Here’s a quick look at the basic pieces of any business budget, explained in simple terms.

| Budget Component | What It Means In Simple Terms | Why It Matters |

|---|---|---|

| Projected Revenue | The money you expect to make from sales. | This sets your money goal and helps you plan for growth. |

| Fixed Costs | Bills that stay the same each month, like rent or software subscriptions. | These are costs you have to cover no matter what. |

| Variable Costs | Bills that change based on how much you sell, like supplies or shipping. | Understanding these helps you see how your costs go up or down with your sales. |

| Profit | What’s left over after you subtract all costs from your revenue. | This is the main way to tell if your business is healthy and successful. |

That’s it. By putting your money into these simple buckets, you’re already on your way to building a powerful tool that will help your business grow.

Gathering Your Financial Puzzle Pieces

Before you can make a budget for the future, you need to get a clear picture of where your money has been going. This part is like a scavenger hunt—we’re going to find all the papers that tell the story of your business’s money from the last year.

Don’t worry if your records aren’t perfect. The goal is to get a good idea, not create a perfect accounting report.

Think of your past financial info as your secret weapon. It holds all the clues about your business’s rhythm—when you’re busy, when things are slow, and what your costs really are. Having this history makes it much easier to predict the future.

Your Financial Scavenger Hunt Checklist

To build a budget that works, you need to start with the right information. The first step is to pull together documents from the past 12 months. This gives you a full view of a business year, including any busy or slow seasons you might not have noticed.

Here’s a simple checklist to get you started:

- Bank and Credit Card Statements: Grab the statements for all of your business accounts. This is the best place to see every dollar that came in and went out.

- Sales Records: This could be from your cash register, invoicing software like QuickBooks, or even a simple sales spreadsheet. You need to see how much you sold each month.

- Payroll Reports: If you have employees, you’ll need reports that show how much you paid in wages, taxes, and benefits.

- Loan or Debt Statements: Collect statements for any business loans or credit cards you’re paying off.

- Major Receipts: Find the receipts for any big, one-time purchases you made—like a new computer, expensive software, or a piece of equipment.

This might feel like a chore, but getting organized now is a huge step. If your records are a bit of a mess, don’t worry. Check out these basic bookkeeping tips for business owners to help you get things in order.

What If You’re a Brand-New Business?

“But what if I don’t have a year of data?” This is one of the most common questions I hear, and the answer is simple. If you don’t have a financial history, you’ll have to make some good guesses.

Instead of looking back, you’ll look around. Your job is to research what costs and sales look like for a business like yours in your area.

The goal for a new business isn’t to be perfectly right. It’s about creating a good starting point that you can change as you start making real money and paying real bills.

For example, if you’re opening a coffee shop, you can look up average daily sales or the typical cost of coffee beans and milk. You can call local real estate agents to get a good idea of rent costs or ask utility companies for estimated monthly bills.

Your first budget will be built on these guesses instead of your own past results. As soon as you open, you’ll start replacing those guesses with actual numbers, turning your budget into a living tool that gets smarter every month.

Forecasting Your Income and Expenses

This is where you stop looking in the rearview mirror and start looking at the road ahead. Forecasting is just a fancy word for making a plan. It’s about taking the money information you gathered and painting a realistic picture of what your business will look like next month, next quarter, and next year.

The key here is to be realistic. This isn’t about pulling numbers out of thin air. A good forecast should be a bit of a stretch, but also something you can actually achieve.

Breaking Down Your Expenses

First, let’s look at the money going out. The easiest way to do this is to split your expenses into two simple buckets: fixed costs and variable costs. Honestly, understanding this difference is a game-changer.

Fixed costs are the bills you have to pay every single month, no matter what. They don’t change whether you sell one thing or one thousand.

Here are some common examples:

- Rent: Your monthly payment for your office or store.

- Salaries: The pay for your full-time and part-time staff.

- Software Subscriptions: All those monthly fees for tools like QuickBooks or your email service.

- Insurance: Your business insurance payments.

Variable costs, on the other hand, go up and down with your business. The more you sell, the higher these costs get. If you have a slow month, these costs should drop.

Think of things like:

- Inventory or Raw Materials: For a coffee shop, this is the coffee beans and milk. The more coffee you sell, the more beans you have to buy.

- Advertising Spend: You’ll likely spend more on ads during your busy season and less during slower months.

- Shipping and Packaging: These costs are directly tied to how many orders you ship.

- Sales Commissions: If you pay your sales team a percentage of what they sell, this cost goes up with every new sale.

Key Takeaway: Separating your costs this way is super helpful. It shows you the minimum you need to earn each month just to stay open (your fixed costs). It also shows you how much it costs to make each sale.

Predicting Your Income Realistically

Now for the fun part—planning the money you expect to bring in. This can feel like guessing, but you can get pretty close by looking for patterns in your past sales.

Think about the rhythm of your business. Does your lawn care company get busy in the summer? Does your shop see a huge rush around the holidays and then get quiet in January? Finding this seasonality is the secret to making a monthly plan that makes sense.

For example, a marketing agency I worked with knew that clients often pause projects in December but rush to use their budgets in November. By looking at last year’s numbers, they planned for a slow end to the year and a busy fall, making sure they had enough cash to get through the quiet time. Mastering this is a huge part of truly knowing your numbers. You can learn more about why understanding these metrics is so important for your company’s long-term health.

Don’t Forget One-Off Purchases

Your regular monthly bills are only part of the story. Businesses also have large, rare costs that can wreck your budget if you aren’t ready for them. We often call these capital expenditures.

Think about big-ticket items like:

- Buying a new company truck

- Upgrading all the computers for your team

- Investing in a special piece of machinery

These aren’t daily costs, but you have to plan for them. A smart budget has a spot for these purchases so you can save money and not be surprised when it’s time to buy.

Finally, think about other costs unique to your industry. For many companies, business travel is a big expense. The global business travel industry is huge, with spending expected to hit $1.57 trillion USD in 2025. Companies look at these big trends to help plan their own travel budgets. You can discover more insights about these global business travel trends and see how they might affect your planning. By planning for all these pieces, you’re not just budgeting—you’re building a full financial roadmap.

Building Your First Business Budget

Okay, you’ve gathered your numbers and made some good predictions. Now for the fun part: actually building your first business budget. This is where we turn all that information into a real plan you can use to run your business, no complicated stuff needed.

We’re going to build two key documents that give you the full money picture. First is your operating budget—your day-to-day plan. Then, we’ll do the cash flow budget, which, in my experience, is even more important for staying in business.

Creating Your Operating Budget

Think of your operating budget as the main plan for your business over the next 12 months. It’s a simple document that lists all the money you expect to bring in (your revenue forecast) against all the money you expect to spend (your fixed and variable costs). The goal is simple: see if you’re set up to make a profit.

I always recommend starting with a simple spreadsheet. Make 13 columns—one for your expense and income categories (like “Sales,” “Rent,” “Marketing”) and one for each month of the year.

Here’s how I walk people through filling it out:

- Put in your revenue forecast. At the top, put in your expected sales for each month, remembering to account for those busy and slow seasons.

- List all your fixed costs. Go down the list and enter every fixed cost for every month. This is the easy part since these don’t change—just copy your rent, software fees, and insurance costs across all 12 columns.

- Add your variable costs. This takes a little more thought. Based on your sales forecast, guess what your variable costs will be. If you’re expecting a huge May, your supply orders and shipping costs should be higher that month, too.

- Do the math. For each month, subtract your total costs (fixed + variable) from your total revenue. That number at the bottom is your expected profit or loss.

This simple exercise gives you an amazing amount of clarity. You can immediately see which months might be tight and which ones should be your best.

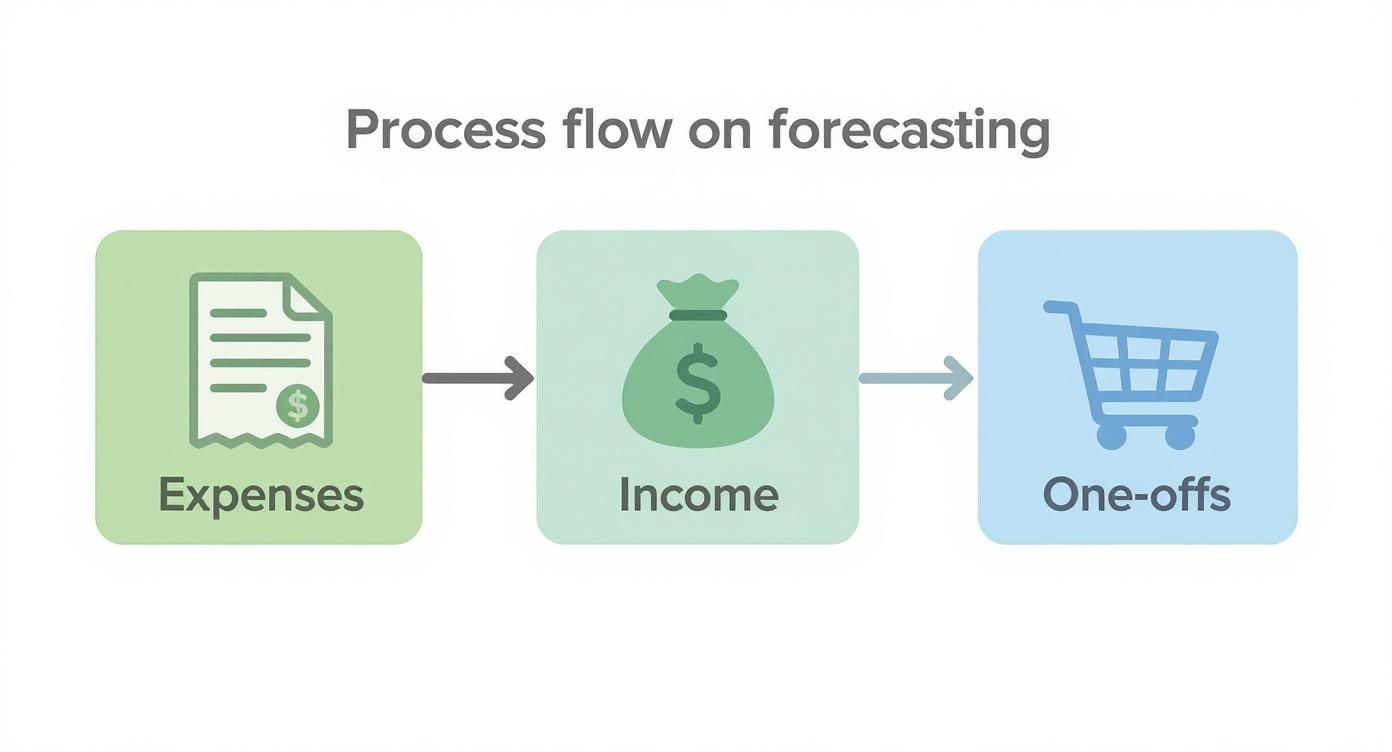

This infographic breaks down that forecasting process into three simple visual steps.

As you can see, you first map out your regular expenses, then add in your income, and finally plan for those big, one-time purchases to get the full picture.

The All-Important Cash Flow Budget

Here’s a situation I’ve seen happen hundreds of times: a business owner looks at their operating budget, sees a nice profit on paper, but their bank account is empty. This is a cash flow problem, and it’s one of the biggest reasons new businesses fail.

Profit isn’t cash. Let me say that again: profit is not the same as cash.

For example, you might make a $10,000 sale in March and write it down as income. But if your client has 60 days to pay, you won’t actually get that cash until May. In the meantime, you still have to pay rent and your employees in April.

A cash flow budget tracks when money actually comes into and leaves your bank account. It’s your financial survival guide.

To build it, create another spreadsheet that looks just like your operating budget. This time, however, you only record money when it moves. That $10,000 sale from March? It doesn’t get put in here until the payment hits your account in May. That big bill you have to pay in June? You record it in June, not when you first got the invoice.

This budget makes sure you always have enough actual cash to pay your bills on time. It helps you see money gaps coming weeks or even months away, giving you plenty of time to get ready—maybe by chasing down unpaid invoices or using a line of credit.

Budgeting for People

Whether you have a team of employees or use freelancers, people are almost always your biggest and most important expense. Budgeting for them the right way is a must.

For Employees:

- Don’t just budget for their salary. You have to include payroll taxes, benefits (like health insurance), and workers’ compensation insurance. These “hidden” costs can easily add an extra 20-30% on top of their base pay.

For Contractors or Freelancers:

- These costs are usually simpler since you don’t have to pay for their taxes or benefits.

- The key here is to budget for their work based on your projects. If you know a big client project is starting in July, make sure their fees are in your budget for that month and the months that follow.

By creating both an operating budget and a cash flow budget, and carefully planning for your people costs, you’ve built a complete financial roadmap. This isn’t just another spreadsheet; it’s a powerful tool that helps you go from reacting to problems to being a proactive leader who is truly in control.

Choosing the Right Budgeting Tools

You don’t need to be a spreadsheet expert to create a good business budget. Once you have your numbers, the next step is picking a tool to put it all together. Luckily, you have options from simple to very powerful.

The key is finding something that makes your budget a helpful partner, not a monthly chore you hate. For some, a simple spreadsheet is perfect. For others, an app that does the heavy lifting is a lifesaver.

The Classic Spreadsheet Approach

For many business owners, a simple spreadsheet is the best place to start. It’s easy, you probably already have access to one (like Google Sheets or Excel), and it gives you total control. You decide what goes where, and you build the formulas yourself.

If you go this route, you only need a few basic formulas to do most of the hard work for you:

- SUM: Use

=SUM(B2:B13)to quickly add up a column of numbers, like all your marketing costs for the year. - Simple Subtraction: Use

=B2-B3to find your monthly profit by subtracting total expenses from total income. - AutoFill: Don’t type the same thing over and over. If you have a fixed cost like rent, enter it once, then click and drag the little square in the corner to copy it across all 12 months.

Spreadsheets are a great, no-cost way to get started. More importantly, building it yourself forces you to truly understand how all the pieces of your budget fit together.

When to Consider Budgeting Software

While spreadsheets are great, they are a lot of manual work. You have to type in every transaction and double-check every formula. This is where special budgeting software can save you a huge amount of time.

Modern budgeting software can make this process much easier by automatically tracking expenses and creating profit-and-loss reports with very little work from you.

These tools are built to make budgeting easier by connecting directly to your business bank accounts. They automatically pull in transactions, suggest categories, and build reports for you. You get a real-time look at your money without spending hours typing in numbers. To see how this works, you can learn more about how budgeting software streamlines financial planning.

If you’re thinking about an app, make sure it has these key features:

- Bank Connection: This is a must-have. It has to safely link to your accounts and automatically import income and expenses.

- Receipt Scanning: A great time-saver that lets you take a picture of a receipt with your phone and have it instantly recorded and sorted.

- Simple Reporting: The whole point is to get answers quickly. The software should create easy-to-read reports, like a Profit & Loss statement, with just a few clicks.

Ultimately, choosing between a spreadsheet and software is a personal choice. Do you want full control and a hands-on approach? Stick with a spreadsheet. Would you rather save time and let technology do the hard work? It might be time to invest in software.

Making Your Budget a Living Document

Creating your budget is a huge first step, but the real magic happens when you start using it. I see too many business owners treat their budget like a New Year’s resolution—they make it in January and forget about it by March.

A business budget isn’t a file you “set and forget.” It’s a living tool that should help you make decisions every single month.

The most important habit you can build is a monthly budget review. This is where you sit down and compare what you planned to do with what actually happened. Accountants call this variance analysis, but it’s really just a fancy term for spotting the differences and asking “why?”

This simple check-in turns your budget from a boring report into your most trusted business advisor.

How to Review Your Budget Each Month

Set aside an hour or two at the end of each month to pull up your budget. Go line by line and compare your “planned” numbers to your “actual” numbers from your business records.

You’re looking for the story behind the numbers. Don’t just see that you went over budget on marketing. Dig deeper and ask yourself why.

- Positive Surprises: Did you spend an extra $500 on ads but land three new clients worth $5,000? That’s a win! That’s a great reason to go over budget, and you should think about doing it again.

- Negative Surprises: Did your sales dip? Maybe a big client paid late, messing up your cash flow, or a slow season was worse than you thought.

- Unexpected Costs: Did your delivery van get a flat tire? That’s a surprise expense, and now you know you might need a small emergency fund for vehicle repairs.

This process isn’t about judging yourself. It’s about gathering clues to make smarter, faster decisions for the future. You’re learning from your own data.

Making Smart Adjustments

The whole point of this review is to take action. Based on what you find, you can make small changes to your plan for the next month.

If you’re always overspending on office supplies, you might look for a cheaper place to buy them or put some rules on ordering. If one of your services is selling way better than you expected, maybe you should put more of your ad money toward promoting it.

Figuring out these money puzzles can get tricky as your business grows. If you find yourself staring at the numbers and aren’t sure what they mean, it might be time for some expert help. Many owners find that exploring fractional CFO services can revolutionize their small business by giving them high-level advice without the cost of a full-time executive.

This regular check-in keeps you in charge, helping you stay on track and find new opportunities before your competitors even see them.

Common Budgeting Questions Answered

Even with the best plan, questions are going to come up when you’re learning how to build a business budget. It’s totally normal. Here are a few common ones I hear from business owners just like you.

How Often Should I Update My Budget?

Think of your budget as a living document, not something you carve in stone. At a minimum, you need to sit down and review it every single month. A quick comparison of your planned numbers versus your actual results will tell you everything you need to know about what’s working and what isn’t.

That said, a major change or a brand-new budget build should only happen once a year. That annual check-up is your chance to set big goals for the upcoming year, using everything you learned from the last one.

What If My Projections Are Wrong?

Let me save you some stress: they will be. And that’s okay! Nobody has a crystal ball. The point of a budget isn’t to be 100% accurate. Its real job is to show you where you were off and make you ask the most important question in business: “Why?”

Your budget is a tool for learning. If your sales were lower than you thought, it pushes you to figure out what happened with your marketing or sales. If costs were higher, it shows you why.

What Is a Good Profit Margin?

This is the million-dollar question, and the only right answer is: it depends on your industry.

A grocery store, for example, might be very successful with a tiny 2% profit margin because it sells so much. On the other hand, a software company might be aiming for 20-30% or more. The best thing to do is research your specific industry to find a realistic number. That gives you a real-world target to aim for, not just a number you made up.

Feeling like you need a guide to help answer these questions for your specific business? The team at MyOfficeOps provides the financial clarity you need to stop guessing and start growing with confidence. Schedule your discovery call today.