You hire a nanny because your calendar is packed. Or a caregiver because your parent should not be alone during the day. Or a housekeeper because you are running a company, getting kids to school, and trying to keep your head above water.

Then one small question shows up and ruins a perfectly normal Tuesday.

“Do I need to give them a W-2?”

For a lot of business owners, this is the first time they realize household payroll is a real payroll issue. Not a casual Venmo issue; not a “we’ll figure it out at tax time” issue. It is a payroll issue with employer rules, tax filings, and deadlines.

The good news is this is fixable. You do not need to become a tax nerd overnight. You need to know where the line is between household help and a contractor, how to set yourself up the right way, and how to avoid the common mistakes that create cleanup work later.

This guide is written for the owner who already has enough on their plate, especially if you are also running business payroll and want clean books on both sides.

The Moment You Realize Your Nanny Needs a W2

A lot of people back into this.

It starts with a simple arrangement. You pay someone every week to watch your kids after school. Or you bring in a caregiver for your father while you are at the office. Maybe your housekeeper started at one day a week and now works a regular schedule.

At first, it feels informal. You are paying for help at home. That does not feel like “becoming an employer.”

Then tax season comes around. Your worker asks for year-end paperwork. Your CPA asks what you paid. You start hearing terms like “nanny tax,” “Schedule H,” and “household employee.” That is usually the moment the stress kicks in.

I see the same reaction from owners all the time. They are not trying to dodge rules. They assumed home help worked like hiring any other service person. It often does not.

If the person works in your home and you control the job, there is a good chance you are dealing with an employee relationship, not a contractor relationship. That matters because a proper w2 for household employees protects both sides.

Your worker gets wage reporting tied to Social Security and Medicare. You get a cleaner record if the IRS ever asks questions. You also avoid the mess that comes from trying to reclassify payments after the fact.

Tip: Household payroll feels annoying mostly when it is handled late. When it is set up early, it becomes a routine admin job, like any other payroll process.

The key is not to panic. You do not need to solve all of it in one sitting. Start with the classification question, as that is the fork in the road.

Is Your Helper an Employee or a Contractor

This is the question that causes the most trouble.

People want the simpler answer. They think, “I’ll just 1099 them.” But the IRS does not let you pick the easier form. The working relationship decides it.

For household help, the simplest test is control. If you control the work, the person is usually an employee.

Three practical questions

Ask yourself these:

Do you set the schedule

If you decide when the person shows up, when they leave, and what days they work, that points toward employee status.Do you control how the work gets done

If you tell them how to care for your child, what meals to prepare, what tasks to do during nap time, or how the house should be cleaned, that also points toward employee status.Is the person working as part of your household routine

If the person is built into your home life on an ongoing basis, that usually looks like employment. A true contractor tends to run an independent business and serve clients on their own terms.

Employee vs. Independent Contractor at a Glance

| Factor | Household Employee (Needs a W-2) | Independent Contractor (Gets a 1099-NEC) |

|---|---|---|

| Schedule | You set hours and days | Worker sets their own schedule |

| Work methods | You direct how work is done | Worker decides how to do the job |

| Tools and supplies | You usually provide what is needed in the home | Worker often brings their own tools or systems |

| Relationship | Ongoing part of your household routine | Project-based or service-based |

| Tax treatment | You handle payroll reporting | Worker handles their own taxes |

Real-world examples

A nanny is the classic employee example.

She comes to your house Monday through Friday. You tell her when to arrive, what the kids eat, which activities are okay, whether screen time is allowed, and when the baby naps. That is not an outside business serving you on its own terms. That is an employee working under your direction.

A weekly cleaning company is different.

You hire the company to clean every Thursday. They decide who shows up. They bring their own supplies. They use their own process. You care about the result, but you are not standing there directing each task. That is much closer to a contractor setup.

The same logic applies to caregivers. If a caregiver works in your home on a schedule you control, and you direct the care arrangement, that usually fits the employee side.

What business owners get wrong

Owners who already hire vendors in their company sometimes carry that mindset into the home.

A plumber is a contractor. An IT consultant is a contractor. A marketing freelancer can be a contractor. But household roles are different because they are usually tied to your instructions, your schedule, and your home environment.

That is why misclassification causes so many problems. If you call someone a contractor because it feels simpler, you can end up with back taxes, corrected forms, and a bigger mess than if you had set up payroll properly from the start.

A good rule of thumb: if you are managing the person more like staff than like an outside service business, treat them like an employee until proven otherwise.

Once you are confident the worker is an employee, the next move is paperwork. Not exciting, but it keeps the rest of the year from turning into a scramble.

Getting Your Paperwork in Order as an Employer

Before you run payroll, you need a basic employer file. This is the part most owners delay, but it is usually much less painful than they expect.

Get your EIN first

You need an Employer Identification Number, or EIN.

Think of it as the employer version of a Social Security number. It identifies you when you file wage forms and payroll tax documents. You should not use your personal Social Security number in place of it for this job.

To correctly generate Form W-2, you must have your EIN and the employee's SSN, according to this household employee W-2 guide.

If you already own a business, people often get tripped up by this. They assume the business EIN automatically covers household payroll. Sometimes the practical question is less about whether you have an EIN and more about whether your records cleanly separate household payroll from business payroll. That is where a lot of bookkeeping confusion starts.

Gather the employee documents

You need clean, accurate employee information up front.

Keep these on file:

Form I-9 details

You need the employee’s identifying information and work eligibility support. Accuracy matters. Bad names, addresses, or Social Security numbers can create filing problems later.Form W-4 if they want income tax withheld

Federal income tax withholding for household employees is optional when the employee requests it. If they want withholding, get the W-4 before payroll starts.Pay agreement records

Write down the regular rate, schedule, start date, and any reimbursement arrangement. Do not rely on texts and memory.

Pennsylvania owners need one more layer

If you are in Pennsylvania, do not stop at the federal side.

Household employment can also trigger state unemployment requirements. A lot of owners miss this because they assume personal household help does not touch state payroll systems. It can.

If you are used to company payroll, you already know the headache caused by missing a state registration and trying to fix it later. Household payroll is no different. Get the state setup sorted early and keep household records separate from your company wage records.

For owners who want a broader look at payroll setup habits that keep things organized, this guide on how to set up payroll for small business is useful because the same discipline applies here.

Build one clean filing folder

The easiest way to stay sane is to create one folder, digital or physical, for household payroll only.

Put in:

- Employer ID records

- Employee forms

- Pay logs

- Tax payment confirmations

- Year-end filing copies

That small bit of organization saves you from chasing paperwork in January.

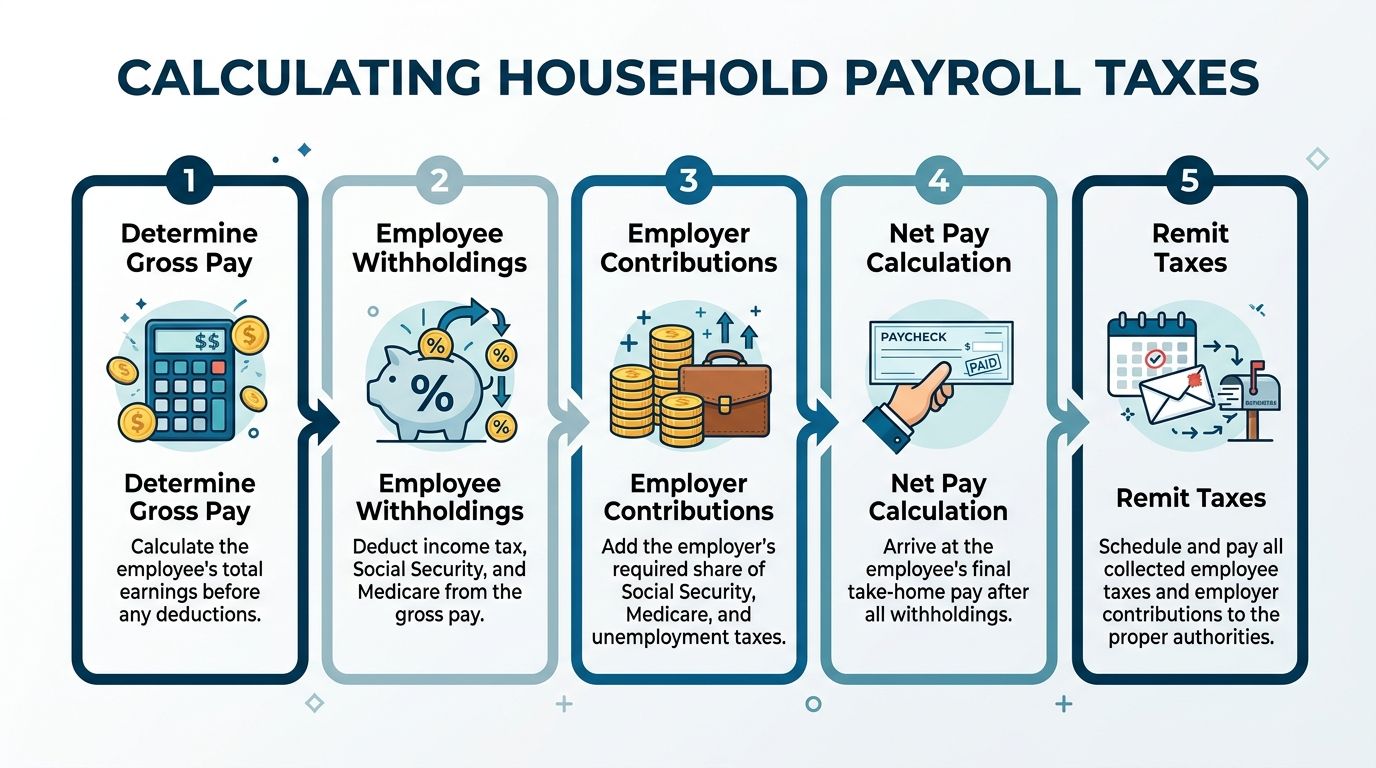

Calculating Payroll Taxes The Simple Way

This is the part people dread, but the math is not the hard part. The hard part is understanding which numbers matter and when they apply.

For 2026, household employers must withhold and pay Social Security and Medicare taxes on cash wages paid to any household employee who reaches the annual threshold of $3,000, and the tax rates are 6.2% each for Social Security and 1.45% each for Medicare for both employee and employer, according to IRS Publication 926.

Start with gross pay

Gross pay is the full amount earned before any withholding.

If your nanny earns a weekly amount, that weekly amount is your starting point. If hours vary, multiply hours worked by the agreed rate and start there.

Do not make this more complicated than it is. Gross pay is what the worker earned.

Then handle FICA

Once wages are high enough to trigger the rule noted above, you deal with FICA, which is Social Security and Medicare.

The combined rate is 7.65% for the employee and 7.65% for the employer under the same IRS publication. That means two things happen:

- You withhold the employee share from pay

- You match it as the employer

That second part matters. Owners sometimes remember to deduct from the worker’s paycheck but forget they owe their own matching share too.

Here is the plain-English version:

Employee side

Social Security and Medicare come out of the worker’s wages.Employer side

You pay the same percentages yourself.

If you are doing this manually, keep a simple worksheet for each payroll date with gross wages, employee FICA withheld, employer FICA owed, and net pay.

Tip: The employee’s paycheck amount and your total payroll cost are not the same thing. Your real cost includes the employer tax share.

Do you also withhold income tax

Sometimes yes. Sometimes no.

Federal income tax withholding is optional for household employees and generally happens when the employee asks for it and gives you a Form W-4. If they do not ask, you usually are not required to withhold federal income tax.

That is different from normal business payroll, and it throws people off.

In practice, some workers prefer withholding because it keeps their own tax filing cleaner. Others prefer to handle it themselves. The key is to document the choice and stick to it.

Do not forget FUTA

Federal unemployment tax is a separate item.

FUTA applies to household employers who pay $1,000 or more in cash wages in any calendar quarter of the current or prior year. It applies to the first $7,000 of each employee’s annual wages at 6%, and many employers qualify for a 5.4% credit for state unemployment contributions, which can reduce the effective rate to 0.6%, according to this summary of tax obligations for household employees.

That sounds more complicated than it feels in real life.

The practical takeaway is this: once household pay reaches the quarterly trigger, unemployment tax is part of the picture too. Track it from the start instead of trying to rebuild quarterly wage history at year end.

A simple payroll routine that works

For a busy owner, the cleanest process usually looks like this:

Record hours or the fixed weekly amount

Use the same method every pay period.Calculate gross pay

This is the employee’s earned wage before deductions.Calculate employee withholding

Include FICA when applicable, plus any agreed federal income tax withholding.Calculate employer taxes

Add your matching FICA and any unemployment taxes that apply.Pay the employee and save the payroll record

Do not rely on bank transfers alone as your payroll system.

The crossover problem for business owners

Home payroll and company payroll start stepping on each other here.

A key challenge for SMB owners is integrating household payroll with business accounting. Many business owners run into compliance problems because payroll systems do not properly separate household and business wages, which complicates FUTA credit calculations and financial tracking, as noted in this discussion of household employee tax obligations for SMB owners.

That is why I tell owners to treat household payroll like its own lane. Separate records. Separate reporting logic. Separate review.

Do not bury nanny wages in owner draw notes, random transfers, or a business payroll batch. That is how people create confusion for themselves and their tax preparer.

What works and what does not

What works:

- A consistent pay schedule

- A simple spreadsheet or household payroll software

- Saving tax money as you go

- Keeping household payroll out of your business wage accounts

What does not:

- Paying cash with no log

- Guessing at year-end totals

- Using the same bookkeeping bucket for both home and business payroll

- Assuming your regular payroll app automatically handles household rules the right way

The owners who stay out of trouble are usually not doing anything fancy. They are organized early.

Annual Filing Your W2 and Schedule H

Year-end filing is where all your recordkeeping either pays off or punishes you.

If your payroll records are clean, preparing a w2 for household employees is a straightforward wrap-up job. If your records are messy, January gets ugly fast.

What goes on the W-2

The basics are not mysterious.

To correctly generate Form W-2, you must have your EIN and the employee's SSN. Use Box 1 for total wages, Box 2 for federal income tax withheld if any, Boxes 3 and 5 for Social Security and Medicare wages, and Boxes 4 and 6 for the corresponding taxes withheld. The deadline for giving the employee copy and filing with the SSA is January 31, according to this guide to preparing a household employee W-2.

That January 31 date matters. It is one of those deadlines you do not want to drift past while you are also closing books for the business and gathering tax documents.

Why the W-2 matters to your worker

The W-2 is not just paperwork for the IRS.

It gives your employee a formal wage record. That matters for their tax filing and for the wage history tied to Social Security and Medicare. If you skip the W-2 and hand over a total on a sticky note, you are creating a problem for them and for yourself.

For household workers who depend on steady documented income, a proper W-2 is part of being treated like a real employee, because they are one.

Schedule H is the bridge to your personal return

This is the part that surprises business owners.

Even if you run a company and already deal with payroll there, household employment taxes generally flow through Schedule H, which attaches to your Form 1040. In other words, your household payroll reporting typically lands with your personal tax return, rather than inside your regular business payroll filing rhythm.

That crossover is why records need to be clean. You do not want your CPA trying to untangle household tax obligations from business payroll history after the fact.

A simple year-end checklist

Use this list in January:

Confirm employee legal name and SSN

Small errors here can cause filing issues.Reconcile total wages paid

Match your pay log to your bank records and payroll records.Review what you withheld

Make sure wage figures and tax figures line up.Prepare and furnish the W-2 by January 31

Do not wait for your employee to ask.File with the Social Security Administration by January 31

Handle it the same day if you can.Give your tax preparer the Schedule H support

Make their job easier and your bill smaller.

If you want a broader checklist mindset for year-end organization, this guide on how to prepare for tax season is useful because the same habit applies here. Good prep beats good recovery every time.

Key takeaway: Household payroll does not end when the last paycheck goes out in December; it ends when the W-2 is filed correctly and Schedule H is ready for the return.

Common Household Payroll Mistakes to Avoid

Most household payroll problems are not caused by complicated tax law. They are caused by ordinary shortcuts.

People mean well. They are busy. They assume they will fix it later. Later usually costs more.

Calling an employee a contractor

This is the biggest one.

A nanny, housekeeper, or caregiver often gets called a contractor because the owner wants to keep things simple. But if the relationship is really employment, using a 1099 instead of a W-2 is the wrong form and the wrong tax treatment.

Why it happens is easy to understand. Owners are used to hiring contractors in their business. They think household help works the same way. It often does not.

The fix is simple. Decide the classification based on control, not convenience.

Mishandling noncash wages

This one catches smart people because it sounds backward.

IRS rules can exempt wages paid to certain family members (like a spouse, a child under a certain age, or a parent) from FICA taxes in many cases. Also, noncash wages, such as room and board, may have different tax treatment: often subject to income tax but potentially exempt from FICA. Specific rules apply, so checking official IRS guidance is important.

Where people slip

Lodging gets ignored entirely

The owner thinks, "I’m not paying cash, so nothing needs to be tracked."Everything gets run through FICA

That can be wrong too if the compensation is noncash.There is no written value record

Then year-end reporting becomes guesswork.

The practical answer is to document any noncash arrangement clearly and review how it should be reported before year-end, not during a filing panic.

Missing payment timing

Some owners think the only important deadline is the W-2 in January.

It is not. If you wait all year without planning for tax payments, you can create a cash squeeze and possible penalties. Even when the annual filing is the headline item, the smarter move is to set aside tax amounts throughout the year, so you are not funding everything in one shot.

This is especially true for owners whose cash flow already swings with the business.

Forgetting family-member exceptions

Family employment rules are full of assumptions.

People either think family members are always exempt or they think family members are never exempt. Both approaches cause mistakes.

Better habit

Look closely when the worker is:

- A spouse

- A child under 21

- A parent

These relationships can have different tax treatment. Do not copy your treatment from a nonfamily worker and assume it is correct.

Tip: Family payroll is where “I thought that sounded right” causes expensive errors. Check the relationship before you process the pay.

Mixing household and business records

This one is common with owner-operated firms.

You are already paying staff in your company, so you drop the nanny into the same mental bucket. Or worse, you reimburse yourself through the business books and leave unclear notes.

That creates problems in three places:

- your bookkeeping

- your tax prep

- your audit trail

Keep household payroll in its own record stream. Your future self will be grateful.

When to Outsource Your Household Payroll

Some owners should do this themselves.

If you have one household employee, a steady pay arrangement, clean records, and the patience to stay on top of filing, it can be manageable. Plenty of people handle it just fine.

But a lot of business owners are already running enough systems. They have company payroll, vendor payments, cash flow pressure, tax prep, and family responsibilities. Adding household payroll to that pile is often where little mistakes start.

The actual workload

Household payroll is not just cutting a check.

You need to:

- Track wages accurately

- Handle withholding correctly

- Set aside employer taxes

- Keep records organized

- File year-end forms on time

- Make sure household and business accounting stay separate

None of those jobs are impossible. Together, they become one more recurring process to manage.

The crossover is the deciding factor

For many owners, the issue is not the household payroll by itself. It is the fact that it sits right next to their business accounting.

When you are already operating a company, the cleanest solution is often to hand household payroll to someone who understands both sides. The bookkeeping side matters just as much as the tax side, because poor separation creates confusion in reports, tax prep, and payroll tracking.

That is where outsourcing earns its keep. Not because the forms are magical, but because someone is watching the details consistently.

A good test for whether you should hand it off

You should seriously think about outsourcing if any of these sound familiar:

- You are paying household help regularly and still tracking it manually

- You are not sure whether your current records would support a W-2 today

- Your company payroll is already taking enough mental space

- You are mixing personal, household, and business transactions in ways that are hard to explain

- You want one clean financial picture instead of a patchwork of apps, notes, and transfers

If that sounds like your situation, review options for accounting and payroll services that can handle the admin work properly and keep the records clean.

The best outsourcing choice is the one that removes repeat stress, not just at tax time, but all year.

If you are a business owner juggling company books and household payroll, MyOfficeOps can help you get both sides organized without turning your weekends into tax admin time. We help owners build clean processes, keep payroll records straight, and create a clear financial picture so nothing gets buried between home and business.