A cash flow statement tells you a simple but super important story: where your money actually came from and where it actually went. Think of it as a video recording of your bank account. It shows all the cash moving in and out of your business over a certain time, like a month or a quarter.

This gives you a real, honest look at your ability to pay bills, buy supplies, and keep the lights on.

The Real Story of Your Business's Money

Imagine your business is a person running a marathon. Your income statement shows how fast you're running—that's your profit. But your cash flow statement shows how much water you have in your bottle. You can be the fastest runner in the world, but if you run out of water, you’re not going to finish the race.

Profit on paper is nice. But you can't pay your employees with profit. You can't buy new equipment with profit. You pay for those things with cash. That's why the cash flow statement is so important; it tracks the actual money that keeps your company alive.

Profit Is Not the Same as Cash

This is a lesson that trips up a lot of business owners. Let's say you're a painter and you land a huge job. The moment you send the invoice, you can record a big profit. But if the client has 90 days to pay you, you have zero cash from that sale today. This gap between the profit you’ve earned and the cash you have is where businesses get into big trouble.

During the 2008 financial crisis, for example, many businesses that looked profitable on paper went under because they didn't have enough cash to pay their bills week to week.

A cash flow statement closes this gap. It cuts through the accounting rules and shows you what's really happening in your bank account. To see how all these reports fit together, check out our guide on how to prepare financial statements.

To make it even clearer, let's look at the main differences between an income statement and a cash flow statement.

Income Statement vs Cash Flow Statement at a Glance

This table gives you a quick summary of what these two key reports tell you.

| Aspect | Income Statement (The Profit Story) | Cash Flow Statement (The Cash Story) |

|---|---|---|

| Main Question | Did we make a profit? | Do we have enough cash to run the business? |

| Timing | Records sales when you earn them, even if you haven't been paid yet. | Records cash only when it enters or leaves your bank account. |

| Focus | Measures how profitable you are. | Measures if you can pay your bills. |

| Key Number | Net Income (Profit or Loss) | Net Change in Cash |

| Example | Shows a $50,000 sale the day you send the invoice. | Shows the $50,000 only when the customer's payment hits your bank. |

While your income statement tells you if your business idea is a good one, the cash flow statement tells you if your business can survive right now.

Why It Matters for Your Decisions

Understanding where your cash goes lets you answer big questions with confidence. Can you afford to hire a new person? Is now a good time to buy that new piece of equipment? The cash flow statement gives you the real-world facts you need to make smart choices.

A business can be profitable on paper and still go bankrupt if it runs out of cash. The cash flow statement is your early warning system. It tells you if your day-to-day work is actually generating enough money to stay healthy.

Beyond just looking at the statement, you can dig deeper with metrics like Days Inventory Outstanding (DIO). This calculation can give you a much sharper view of how efficiently your business is turning its inventory into cold, hard cash.

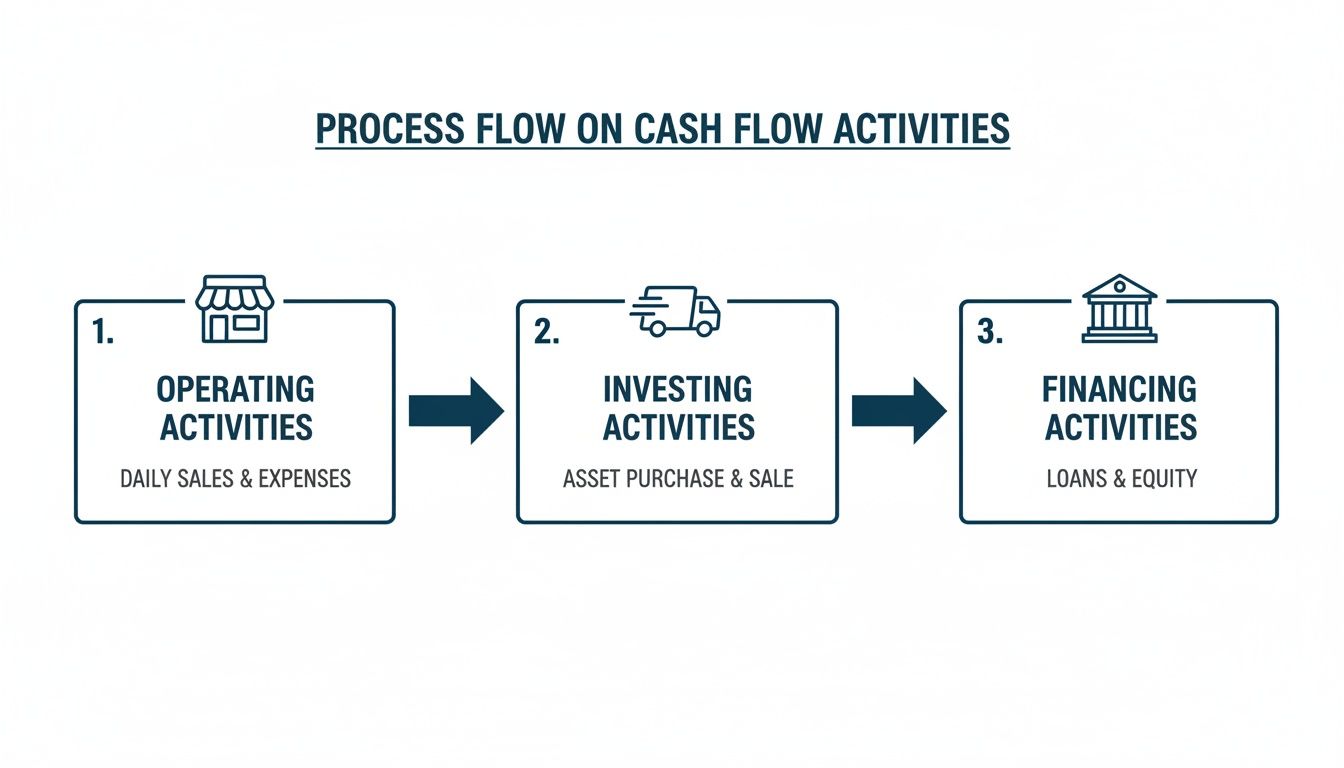

Breaking Down the Three Core Activities

Every cash flow statement is split into three simple parts. Think of them as three buckets that catch and release your cash. Understanding these buckets is the key to reading the report.

This breakdown helps you see if the main part of your business is actually making money, or if it's just burning through cash to stay afloat.

Cash from Operating Activities

This is the most important section. It shows the cash you make from your normal, everyday business—the reason you're in business in the first place.

This is the money that comes from selling your stuff or your services, minus the cash you spend to keep the doors open, like paying employees, rent, and suppliers. A healthy business should always bring in more cash from operations than it spends. If this number is positive, it’s a great sign that your business is working.

Cash from Investing Activities

The second bucket tracks cash you spend on or get from big-ticket items that will help your business grow in the long run. This isn't about the regular inventory you sell; it's about major purchases or sales.

Here’s what that looks like in the real world:

- Cash Out: Buying a new delivery truck for your business.

- Cash Out: Buying new computers for your team.

- Cash In: Selling an old piece of equipment you don't need anymore.

This section tells a story about your company's future plans. Spending money here (a negative number) is often a good thing—it means you're investing in growth.

Cash from Financing Activities

The last bucket shows how you get money from owners, investors, and banks, and it also tracks how you pay them back. It's all about the money flow between your company and the people funding it.

Think of it this way: Operating activities fund today, investing activities fund tomorrow, and financing activities help fill any money gaps. All three need to work together.

Examples of financing activities include:

- Cash In: Taking out a loan from a bank.

- Cash In: Getting money from an investor.

- Cash Out: Making payments on a loan.

- Cash Out: Paying owners or shareholders a dividend.

Together, these three sections give you a complete picture of not just if your cash changed, but why. This is really important, especially when you're waiting on customers to pay their invoices. For more on that, you might want to check out our guide on how to manage accounts receivable effectively.

A Real-World Cash Flow Example

Let's make this real. The whole idea of a cash flow statement clicks when you see it in action. We'll use a simple example for a local contractor we'll call "Reliable Renovations" to see how it all works.

Imagine Reliable Renovations just finished a great quarter. Their income statement shows a nice profit of $20,000. On paper, business is great. But the owner knows the bank account balance doesn't quite match that shiny number, and they need to figure out why before payroll is due.

Finding the Real Cash from Operations

First, we take that $20,000 net income and adjust it to find the actual cash that came from their day-to-day work.

Add back depreciation: The company’s tools and truck lost $3,000 in value this quarter (that's depreciation). This was an expense that lowered their profit, but no cash actually left the business for it. So, we add that $3,000 back.

Account for unpaid invoices: Reliable Renovations was busy, and the amount of money clients owe them went up by $10,000. Even though that’s counted as a sale, the cash isn't in the bank yet. We have to subtract that $10,000 for now.

Look at unpaid bills: They also bought a lot of materials, and the money they owe their suppliers went up by $5,000. This means they held onto their cash instead of paying those bills right away, so we add that $5,000 back to our cash total.

After these changes, the actual cash from operations is $18,000 ($20,000 + $3,000 – $10,000 + $5,000). That’s $2,000 less than the profit they thought they had to work with.

Accounting for Investing and Financing

Next, we look at the other two activities. This part is usually simpler because it tracks direct cash moving in and out.

- Investing Activities: The owner bought a new trailer to haul equipment, which cost $8,000 in cash. This is a cash outflow.

- Financing Activities: To help pay for that trailer, they got a small business loan, bringing in $10,000 of new cash. This is a cash inflow.

The Final Tally

Now, let's add it all up to see the net change in cash for the quarter.

Cash from Operations: +$18,000

Cash from Investing: -$8,000

Cash from Financing: +$10,000

Net Change in Cash: +$20,000

This example shows something that happens to a lot of small businesses. Even though the company was profitable, a big chunk of that profit was stuck in unpaid invoices. Without that $10,000 loan, Reliable Renovations would have only increased its cash by $10,000—not the $20,000 profit shown on paper. This is how the report connects your daily work to the actual money you have in the bank.

How to Spot Red Flags in Your Cash Flow

Now that you get the basics, you can use your cash flow statement as an early warning system. Think of it like a smoke detector; it warns you about trouble before you see the fire.

Learning to read between the lines helps you spot problems before they get too big. It's about asking simple questions like, "Are we collecting money from customers fast enough?" or "Are we relying too much on loans to get by?"

Negative Cash Flow from Operations

This is probably the biggest red flag. If the money coming in from your main business is always less than the money going out, it’s a sign that your business might be broken. It’s like trying to fill a bucket that has a hole in it.

Of course, a single bad month can happen, especially if your business is seasonal. But if you see a trend of negative operating cash flow month after month, it’s time to investigate. It means your day-to-day work is burning through cash instead of making it.

Growing Unpaid Customer Invoices

Here's another big warning sign: the amount of money customers owe you keeps climbing faster than your sales. This looks good on the income statement because it makes your sales numbers look high, but it's a cash flow nightmare. You're basically acting as a free bank for your customers.

This usually points to a problem with how you collect payments. For small businesses, having more cash from operations than net profit is a sign of strength. When there's a big gap in the other direction, it can signal trouble. You can read more about how to interpret these financial signals on kpmg.com.

Key Takeaway: A cash flow statement doesn’t judge—it just reports the facts. Your job is to look at those facts and ask tough questions. Is this a small dip, or is it a sign of a deeper problem we need to fix now?

Depending on Loans to Cover Daily Expenses

Take a good look at your cash from financing activities. If you are constantly taking out new loans just to cover payroll or rent, you’re in a dangerous spot.

Getting a loan to buy a new piece of equipment (an investing activity) can be a smart move for growth. But using debt to pay for your day-to-day operations isn't sustainable. It’s a short-term fix that can lead to a long-term disaster if the real problem isn't solved.

Turning Cash Flow Insights Into Smart Decisions

A financial report is only helpful if you use it to make decisions. The real power of a cash flow statement is using the numbers to make smarter business choices. It turns a page of data into a roadmap for your future.

Instead of guessing, you can start answering big questions with real facts. Is now the right time to hire that new person? Can you actually afford that new equipment that would make your team work faster? A clear view of your cash flow gives you the answers.

From Report to Action Plan

Looking at your cash flow statement should give you ideas. If you see that cash is always tight, it's a signal to make a plan. The goal is simple: get more cash in the door faster and keep it there longer.

Here are a few things you can do right away:

- Change how you send invoices: Don't wait until the end of the month. Bill customers the moment a job is done to start the payment clock sooner.

- Offer discounts for paying early: A small incentive, like 2% off for paying in 10 days, can get clients to pay you weeks faster. This gives your cash a quick boost.

- Review your expenses: Look for small, regular costs you might have forgotten about. Are you still paying for software you don't use? A few small cuts can add up to a big difference.

Your cash flow statement is a tool that shows you where the money leaks are so you can fix them. Small, steady improvements lead to a much stronger business over time.

Make Better Strategic Decisions

Beyond the daily fixes, cash flow information should guide your biggest moves. Knowing your true cash situation helps you plan for growth without getting into trouble.

For example, if you have strong, positive cash flow from your operations, you might feel more confident getting a loan for a big expansion. But if your operating cash is weak, you’ll know to focus on fixing your main business before taking on new debt. Good bookkeeping is the key here. For a deeper dive, explore these strategies for mastering cash flow planning.

Thinking even further ahead, you can start planning for what might happen. Our cash flow forecasting template can help you see what would happen if you land a huge new client—or what happens if a key customer pays late. This kind of planning takes the surprise out of managing your money and puts you in control.

Common Questions About Cash Flow Statements

Even after you get the hang of it, a few questions always come up. Let's go over some of the most common ones.

Getting these final details straight helps make the whole idea much more practical.

What's the Difference Between the Direct and Indirect Method?

Think of it as two different ways to get to the same place. The Indirect Method is the one you’ll see most of the time. It starts with your net profit and then works backward, making adjustments to find out where your cash really went. It's popular because it clearly shows why your profit and your cash are two different things.

The Direct Method, on the other hand, is more like a simple list of all the cash that came in and all the cash that went out from your operations. While it's easier to understand, the Indirect Method gives you more insight, which is why it's the standard.

How Often Should I Review My Cash Flow Statement?

For most small businesses, looking at your cash flow statement monthly is perfect. It’s often enough to spot problems before they get out of hand, but not so often that you get lost in the daily details.

But if your business is growing really fast or has big busy seasons—like a landscaping company in the spring—checking it weekly might be a good idea. The most important thing is to be consistent. A regular review turns this report into a powerful tool you can use to plan for the future.

Can My Business Be Profitable but Have Negative Cash Flow?

Yes, absolutely. This is one of the most common—and dangerous—traps for business owners. It's the exact problem the cash flow statement was designed to solve.

Imagine you're a designer and you just finished a huge project, sending the client a $50,000 invoice. Your income statement immediately shows a big profit.

The problem? The client has 90 days to pay you. In the meantime, you still have to pay your employees, your rent, and your other bills. While you are "profitable" on paper, real cash is flowing out of your bank account. That’s negative cash flow, and it’s exactly why this statement is so important.

What Is Free Cash Flow and Why Does It Matter?

Free Cash Flow is a really important number that shows you how much cash your business has left over after paying for everything it needs to run and grow. This includes paying for big things like new equipment or vehicles.

Think of it as the "extra" cash you have the freedom to use for other things, like:

- Paying down debt faster

- Paying the owners a dividend

- Saving for a rainy day

- Investing in a new project

Investors love looking at free cash flow because it shows a company's real financial strength. For you as an owner, having healthy free cash flow means you have more flexibility and control over your company’s future.

Understanding and acting on your cash flow statement can feel like a full-time job. At MyOfficeOps, we transform these numbers from a source of stress into a tool for growth. We provide clear, jargon-free financial reports and the expert guidance to help you make smarter decisions about hiring, spending, and planning. Let us handle the books so you can focus on building your business. Learn more about how we can help at MyOfficeOps.com.