In accounting, depreciation is just a way to spread out the cost of something big you buy for your business over the years you'll use it. Instead of taking a huge hit to your profits all at once, you record a small piece of the cost as an expense each year. This gives a much more realistic view of your company's financial health.

What Is Depreciation and Why Does It Matter?

Imagine your bakery buys a brand-new delivery van for $40,000. That's a huge check to write, and it feels like a major expense. But you know that van will be making deliveries for the next five years, not just for one month.

If you recorded the full $40,000 as an expense in January, your books would show a massive loss for that month, even if you sold tons of cakes. Then, for the next 59 months, the van would seem like it was "free" because the cost was already paid. That doesn't paint a very accurate picture of your business, does it?

Spreading the Cost Over Time

This is where depreciation comes in. It’s the tool that lets you match the cost of an item to the money it helps you make. Instead of that one-time $40,000 hit, you might record an $8,000 expense each year for five years.

Think of it like paying for a five-year Netflix subscription upfront. You use a little bit of that subscription each year, and your accounting should show that. This process does two important things:

- It smooths out your expenses. Your profit and loss statement becomes more stable and realistic, without huge spikes and dips from major purchases.

- It accurately reflects the asset's value. It shows that your van is slowly losing value over time from all the wear and tear.

Depreciation is an accounting method of allocating the cost of a tangible asset over its useful life. It's an expense that represents how much of an asset's value has been used up.

The Impact on Your Books

This expense is recorded on your income statement, which reduces your taxable income for the year. That's a big deal! By depreciating your assets the right way, you can lower your tax bill.

The expense is also tracked in your company's main financial ledger. To see how these accounts are organized, you can learn more about what a chart of accounts is and how it provides structure for your financial data.

Ultimately, understanding depreciation helps business owners make smarter decisions by giving them a true sense of their company's profitability. To see how this applies to specific assets, you can look into rental property depreciation. It’s not just about rules; it’s about getting an honest look at your financial health.

The Most Common Depreciation Methods Explained

Okay, so we know depreciation is about spreading out an asset's cost. The next question is: how exactly do you do that? It turns out there isn’t just one way to slice the pie. Accountants use a few different methods, and the one you pick depends on the asset and how it loses value.

Think about it. A new company truck loses a big chunk of its value the second you drive it off the lot. On the other hand, a big oak conference table loses its value much more slowly and evenly over many years. Different assets have different stories of value loss. Choosing the right method is key to painting an accurate financial picture.

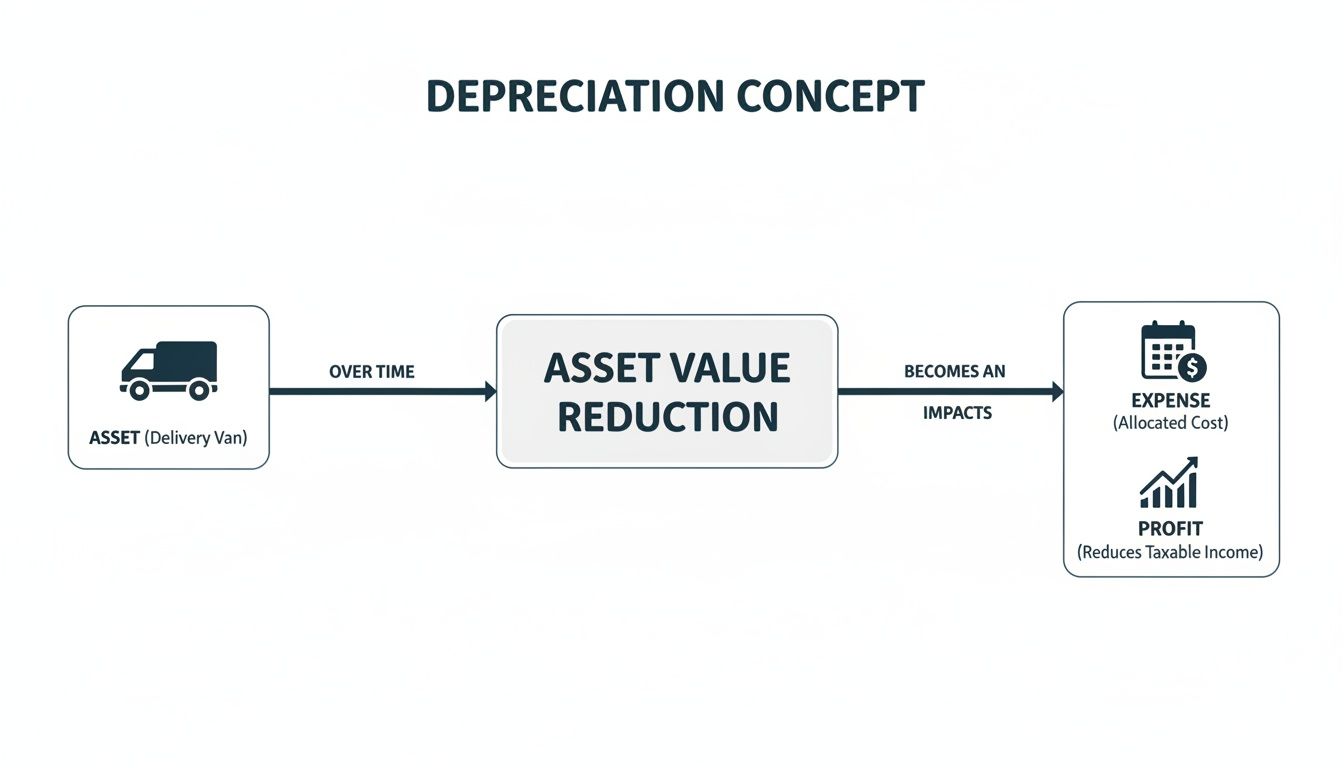

This flowchart breaks down the basic idea: you take an item on your balance sheet, and a piece of its value becomes a regular expense that reduces your taxable profit.

As you can see, the asset’s cost is turned into a depreciation expense on your income statement, which in turn lowers your net profit for tax purposes.

The Straight-Line Method

This is the most common and easiest method to understand. The straight-line method spreads the cost evenly over the asset's life. You expense the exact same amount every single year.

It’s a great fit for things that lose value at a steady, predictable pace, like office furniture, simple fixtures, or machines that do the same task day in and day out. No fuss, no complexity, just simple and consistent.

To figure out the number, you just need three things:

- Asset Cost: The total price you paid for it.

- Salvage Value: Your best guess at what it’ll be worth when you're done with it.

- Useful Life: How many years you realistically expect to use it.

The formula is as simple as it sounds: (Asset Cost – Salvage Value) / Useful Life = Annual Depreciation Expense.

The Declining Balance Method

But what about items that lose a lot of value right at the beginning? A new high-end computer is a perfect example; its value drops like a rock in the first year. For assets like these, the straight-line method doesn't really show what's happening.

That’s where an accelerated depreciation method like the declining balance method comes in. It lets you take a much larger expense in the early years and smaller expenses as the asset gets older. This approach often mirrors the real-world value loss of technology and vehicles much more accurately.

The most popular version is the double-declining balance method. It depreciates the asset at twice the rate of the straight-line method, giving you a bigger tax deduction upfront. This can be a great boost for a business's cash flow.

This method is a go-to for:

- Technology: Computers, servers, and software that become outdated quickly.

- Vehicles: Cars and trucks that lose the most value in the first couple of years.

- Heavy Equipment: Machinery that is most productive and valuable when it's brand new.

The Units of Production Method

Sometimes, an asset's wear and tear isn't about time at all—it's about how much you use it. Imagine a special printing press in a factory. Its value doesn’t drop just because a year has passed; it drops based on how many brochures it has printed.

The units of production method ties the depreciation expense directly to how much the asset is actually used. In busy years when the machine runs non-stop, you’ll record a higher depreciation expense. In slower years, the expense will be lower. It's the perfect model for manufacturing equipment or delivery vehicles where mileage is a better measure of an asset's life than age.

To use this method, you first calculate a depreciation rate per "unit" (like one brochure printed or one mile driven). Each year, you simply multiply that per-unit rate by the total units produced that year. This makes it a very accurate way to match the expense with the income an asset helps you make.

Comparing Depreciation Methods at a Glance

With a few options on the table, it can be helpful to see them side-by-side. Each method tells a slightly different story about how an asset's value is used up.

| Method | How It Works | Best For | Example Asset |

|---|---|---|---|

| Straight-Line | Spreads the cost evenly over the asset's useful life. Same expense every year. | Assets that lose value at a steady, predictable rate. | Office desks, shelving, simple fixtures. |

| Declining Balance | "Front-loads" the expense, with larger deductions in early years and smaller ones later. | Assets that lose value quickly after purchase, like tech. | Computers, company vehicles, smartphones. |

| Units of Production | Ties the expense directly to the asset's usage or output, not the passage of time. | Assets whose lifespan is determined by wear and tear. | Manufacturing machinery, delivery trucks. |

Choosing the right method isn't just an accounting task; it's a strategic decision that affects your financial statements and how much tax you pay. Your choice should reflect the true pattern of how your business uses up the value of the asset.

Calculating Depreciation with Step-by-Step Examples

Alright, let's put the theory aside and work with some real numbers. The best way to understand how depreciation really works is to walk through an example. Seeing the formulas in action makes it all click.

For this exercise, let's imagine a small landscaping company, "GreenScapes," that just bought a brand-new, top-of-the-line commercial lawn mower.

Here are the key details for our scenario:

- Asset Cost: GreenScapes paid $60,000 for the mower.

- Useful Life: They expect the mower to last for 5 years of heavy use.

- Salvage Value: After 5 years, they figure they can sell it for parts for about $10,000.

With these three numbers, we have everything we need. We'll run the numbers for the two most common methods—Straight-Line and Double-Declining Balance—to see just how different the results can be.

Calculating Straight-Line Depreciation

Like we talked about, the straight-line method is simple and predictable. It spreads the cost of the mower evenly across its five-year life. Think of it like cutting a cake into five perfectly equal slices.

First, we need to figure out the depreciable base, which is just the total amount of value the mower is expected to lose.

- Formula: Asset Cost – Salvage Value

- Calculation: $60,000 – $10,000 = $50,000

So, GreenScapes needs to expense a total of $50,000 over the next five years. To find the annual amount, we just divide that by the mower's useful life.

- Formula: Depreciable Base / Useful Life

- Calculation: $50,000 / 5 years = $10,000 per year

With the straight-line method, GreenScapes will record a $10,000 depreciation expense every single year for five years. Simple, right?

Here’s how the mower's value would look on their books over time:

| Year | Beginning Book Value | Annual Depreciation | Ending Book Value |

|---|---|---|---|

| 1 | $60,000 | $10,000 | $50,000 |

| 2 | $50,000 | $10,000 | $40,000 |

| 3 | $40,000 | $10,000 | $30,000 |

| 4 | $30,000 | $10,000 | $20,000 |

| 5 | $20,000 | $10,000 | $10,000 |

By the end of year five, the mower's book value is exactly $10,000, which matches our estimated salvage value perfectly. Clean and tidy.

Calculating Double-Declining Balance Depreciation

Now, let's switch gears. What if GreenScapes feels that a high-tech mower loses more of its value right away? The first year of heavy use takes the biggest toll, after all. In this case, an accelerated method like the double-declining balance makes a lot more sense.

This method sounds more complicated, but it’s just a couple of extra steps. First, we figure out the straight-line depreciation rate.

- Find the Straight-Line Rate: Divide 1 by the useful life. For our mower, that's 1 / 5 years = 0.20, or 20% per year.

- Double the Rate: Now, just double that number. So, 20% x 2 = 40%.

This 40% is our new depreciation rate. The key difference here is that we apply this rate to the asset's book value at the start of each year, not the original depreciable base. Also, we ignore the salvage value until the very end.

Let’s see how this plays out for GreenScapes:

Year 1: $60,000 (Initial Cost) x 40% = $24,000 Depreciation Expense

- New Book Value: $60,000 – $24,000 = $36,000

Year 2: $36,000 (Beginning Book Value) x 40% = $14,400 Depreciation Expense

- New Book Value: $36,000 – $14,400 = $21,600

Year 3: $21,600 x 40% = $8,640 Depreciation Expense

- New Book Value: $21,600 – $8,640 = $12,960

Wait a minute! If we keep going like this, we’ll depreciate the asset below its salvage value. The rule is you can never depreciate an asset for more than its total depreciable amount. We have to stop once the book value hits the salvage value.

Here's how we adjust for that:

Year 4: $12,960 x 40% would be $5,184. But hold on—if we take that whole expense, the book value would drop to $7,776, which is below our $10,000 salvage value. So, we can only take enough depreciation to get down to the salvage value.

- Adjusted Calculation: $12,960 (Book Value) – $10,000 (Salvage Value) = $2,960 Depreciation Expense.

Year 5: The book value is now $10,000, which means there's $0 depreciation left to take.

This process is important for small business owners managing assets like vehicles. National economic data shows that autos and trucks have some of the highest depreciation rates, at 33% and 27% annually, respectively, making the choice of depreciation method a big deal for tax liabilities. You can find more details in the original Hulten-Wykoff study.

The Final Comparison

Look at the difference. In Year 1, GreenScapes could claim a $24,000 expense with the double-declining method versus only $10,000 with the straight-line method. That's a $14,000 larger deduction, which means a smaller tax bill in the early years. This is exactly why businesses often prefer accelerated methods—it improves cash flow when the asset is new and the expenses are highest.

How Depreciation Impacts Your Financial Statements

So, you’ve done the math and figured out your depreciation expense for the year. That's a great first step, but where does that number actually go? It doesn't just sit on a spreadsheet; it plays a starring role on your two most important financial reports: the income statement and the balance sheet.

Understanding how this one number shows up in two different places is the key to seeing the true financial health of your business. It’s not just about tracking an asset's declining value. It’s about accurately reporting your profitability and your company’s net worth.

Depreciation on the Income Statement

First up is your income statement, which is all about your company’s performance over a period of time, like a month or a year. Here, depreciation is treated just like any other operating expense, such as rent, payroll, or utilities.

Each year, the depreciation amount you calculated gets listed as an expense. This has a direct—and positive—effect on your taxes.

- It reduces your net income. Since expenses lower your revenue, depreciation decreases your profit on paper.

- It lowers your tax bill. A lower net income means you owe less in taxes. It’s a non-cash expense that provides a real cash benefit.

This is why business owners pay such close attention to it. It’s a powerful tool for managing tax liability. In fact, depreciation's role in U.S. tax policy is nothing new; by 1985, corporate tax allowances for depreciation and amortization reached nearly $311 billion, a deduction that significantly influenced tax outcomes across the economy. To see the historical scale of these deductions, you can explore the full Treasury report on corporate tax policy.

Depreciation on the Balance Sheet

While the income statement shows a snapshot of this year's expense, the balance sheet tells the long-term story. The balance sheet gives a picture of what your company owns (assets) and what it owes (liabilities) at a single point in time.

Here, depreciation works a bit differently. Instead of just subtracting from the asset's value directly, we use a special account.

This account is called Accumulated Depreciation. Think of it as a running total—a bucket that collects all the depreciation expense recorded for an asset since the day you started using it. It’s a contra-asset account, meaning it has a credit balance and reduces the overall value of your assets.

This allows you to always see both the original cost of the asset and how much of its value you've "used up" over time. The formula to find an asset's current value on the books is simple:

Original Cost – Accumulated Depreciation = Book Value

For a complete guide on how all these pieces fit together, check out our resource on how to prepare financial statements.

A Simple Before-and-After Example

Let's make this real. Imagine your business buys a delivery truck for $50,000. On day one, your balance sheet shows a truck asset worth $50,000.

Now, let's say you calculate $10,000 in straight-line depreciation for the first year. At the end of Year 1:

- Your income statement will show a $10,000 depreciation expense.

- Your balance sheet will now show the truck at its original cost, but with a new line for accumulated depreciation.

Here's the breakdown:

| Balance Sheet Item | Before Depreciation | After 1 Year |

|---|---|---|

| Delivery Truck (Cost) | $50,000 | $50,000 |

| Less: Accumulated Depreciation | $0 | ($10,000) |

| Truck Book Value | $50,000 | $40,000 |

The truck is now officially worth $40,000 on your books. This two-sided entry—an expense on one report and a value reduction on the other—is how depreciation keeps your financial statements balanced and accurate.

Book Depreciation vs. Tax Depreciation

Here’s a concept that trips up a lot of business owners: the depreciation number you use for your own records can be completely different from the number you report to the IRS. And no, that’s not a mistake. It’s actually how the system is designed. You’re essentially keeping two sets of books, and both are correct.

Think of it this way: one set is for you (book depreciation), and the other is for the tax man (tax depreciation). They serve two entirely different purposes.

Why Are There Two Different Types?

Book depreciation is all about getting an honest, accurate picture of your company’s financial health. Its goal is to give you, your partners, or a potential buyer the most realistic view of your asset's declining value over time. You’ll typically use a steady, predictable method like straight-line, which helps you make smart internal decisions.

Tax depreciation, on the other hand, isn’t really about accuracy in the same way. It's about following a specific set of IRS rules designed to influence business behavior. The government often wants to encourage businesses to invest in new equipment to stimulate the economy, so it creates tax codes that let you take bigger deductions sooner.

The key takeaway is this: Book depreciation aims for a true financial picture for decision-making, while tax depreciation follows IRS rules designed to achieve economic goals, often by giving you faster tax write-offs.

The system used for tax purposes in the U.S. is called the Modified Accelerated Cost Recovery System, or MACRS. As the name implies, it generally lets you write off assets much faster than you would for your internal books.

The Power of Accelerated Depreciation for Taxes

This is where things get interesting for your cash flow. Tax rules often let you use accelerated depreciation, which means you get to claim a larger chunk of an asset's cost as an expense in the early years of its life.

Let's say you buy a $100,000 machine. For your books, you might record a $20,000 depreciation expense each year for five years. But for tax purposes, the IRS might let you deduct $40,000 in the first year alone. This larger expense reduces your taxable income more significantly upfront, meaning you pay less in taxes that year. It's a powerful tool for improving cash flow right after you've made a big purchase.

This is why many business owners rely on professional tax and business services that reduce tax burden to make sure they're maximizing these benefits correctly and legally.

Moreover, savvy investors frequently employ various real estate investment tax strategies, with accelerated depreciation being one of the most effective tools for maximizing returns. It’s a common and completely legal strategy to manage your tax obligations and keep more cash in your business.

A Few More Depreciation Questions Answered

Even after you get the hang of the basics, a few specific questions about depreciation always seem to pop up. Let's tackle some of the most common ones I hear from business owners.

Can I Depreciate Land?

Nope, you can never depreciate land.

The logic here is pretty simple: land is considered to have an infinite life. Unlike a building that wears down or a truck that gets old, land doesn't get "used up," so it’s assumed to hold its value indefinitely from an accounting perspective.

What Happens When I Sell a Depreciated Asset?

When you sell an asset, you have to compare the price you sold it for against its current book value (which is just the original cost minus all the depreciation you’ve recorded so far).

- If you sell it for more than its book value, you’ve got a taxable gain on your hands.

- If you sell it for less, you can claim a deductible loss.

This gain or loss gets reported on your income statement for that period. It's the final chapter in that asset's accounting story.

What’s the Difference Between Depreciation and Amortization?

Think of them as cousins. They do the exact same job—spreading out the cost of an asset over its useful life—but they’re used for different types of assets.

Depreciation is for tangible assets, which are things you can physically touch, like your company car, machinery, or office computers. Amortization is for intangible assets, which are valuable things you can't touch, like a patent, a trademark, or a copyright.

Can I Depreciate Used Equipment?

Absolutely! You can and definitely should depreciate used equipment you buy for your business.

The rules are pretty much the same, but your starting point is different. Your "cost" is simply what you paid for the used item, and its "useful life" is your best estimate of how long it will be useful for your business, not its total age.

Feeling like you're drowning in asset schedules and depreciation calculations? MyOfficeOps can handle all the details for you. We provide clear, jargon-free bookkeeping and financial guidance so you can focus on running your business, not just recording it. Find out how we help business owners build a stronger financial foundation at https://myofficeops.com.