So, what does a bookkeeper really do for a small business? Think of them this way: they take a messy pile of receipts, bills, and bank info and turn it into a clear story about your company's money. They help you stop guessing and start making smart choices based on real numbers.

Bringing Your Business Finances From Chaos to Clarity

Let's be real—when you run a small business, you do a little bit of everything. You're trying to find customers, lead your team, and figure out what to do next. On top of all that, there's that growing stack of paperwork, unpaid bills you need to chase, and a shoebox full of receipts you promise you'll sort out later.

This is where a bookkeeper steps in and becomes a huge help. They take all those messy, daily numbers and build a simple system that actually makes sense.

A bookkeeper’s main job is to create a correct record of your company's money story. They make sure every dollar is tracked, giving you a solid base for every business decision.

To really get what a difference this makes, it helps to understand some accounting and bookkeeping essentials. This background knowledge shows you how a bookkeeper turns messy data into a useful tool for your business.

The 'Before and After' of Hiring a Bookkeeper

I once worked with a contractor who was amazing at his job but was always worried about money. He had no real idea where his money was going each month. After a bookkeeper came on board, he could finally see it clearly: he was making good money, but he was losing a lot of it on last-minute, expensive trips to buy materials.

That's the kind of clarity a bookkeeper gives you. They don't just type in numbers; they build a system that tells you the story behind those numbers. If you feel like you're stuck in that "before" stage, our guide on how to manage business finances is a great place to start.

Here’s a look at the common headaches small business owners have and how a good bookkeeper makes them go away.

Before and After Hiring a Bookkeeper

| Common Problem | How a Bookkeeper Solves It |

|---|---|

| Piles of unsorted receipts and bills. | Records and sorts every single transaction. |

| Not sure if you're actually making a profit. | Creates simple reports that show your real profit or loss. |

| Stressing about taxes at the last minute. | Keeps your books clean all year for an easy tax season. |

| Late payments from customers hurting cash flow. | Tracks who owes you money and helps you follow up. |

| Worrying about surprise bills. | Manages bills so you know what you owe and when. |

| Making business decisions with guesswork. | Provides accurate reports for smart, confident decisions. |

In the end, what a bookkeeper really gives you is your time and peace of mind back. Instead of spending your nights and weekends lost in spreadsheets, you can get back to doing what you love—running and growing your business.

The Daily, Weekly, and Monthly Tasks of a Bookkeeper

So, what does a bookkeeper actually do all day? It's not just about typing numbers into a calculator. It’s about creating a steady money rhythm for your business—a set of tasks that keeps everything running smoothly, from your cash to your taxes.

Think of it like taking care of a car. You don't wait for the engine to break down before you change the oil. In the same way, a good bookkeeper does regular checks on your money to stop small problems from turning into big ones.

This rhythm is a simple schedule of daily, weekly, and monthly jobs. Each one builds on the last, creating a complete and correct picture of your company’s money situation.

Daily Bookkeeping Jobs

Daily tasks are all about grabbing money information as it happens. The goal is simple: make sure no payment or sale gets lost in a busy workday. The daily to-do list is focused on recording the money moving in and out of the business.

Imagine you run a busy doctor's office. Your bookkeeper would make sure every patient payment is written down and every payment from an insurance company is recorded and put in the right place.

Here are the main daily jobs:

- Recording Transactions: This is the most basic job. Every time money is spent or earned, it gets written down. This includes sales, bill payments, credit card purchases, and any other money activity.

- Categorizing Expenses: When you buy something, the bookkeeper doesn't just write down the amount; they put it in the right "bucket." Was that purchase for "office supplies," "advertising," or "materials"? This step is super important for getting accurate reports and for tax time.

A key part of a bookkeeper's day is helping small businesses figure out how to track business expenses easily. Doing this every day keeps the financial records clean from the start.

Weekly and Monthly Responsibilities

As the week and month go on, the focus changes from just recording things to checking and managing accounts. These tasks give a bigger-picture view and make sure the business is keeping up with its money commitments.

A great bookkeeper doesn't just record the past; they organize the present to get you ready for the future. They make sure you pay your bills on time and, just as important, that your customers pay you.

Think about a construction company. Each week, their bookkeeper would be busy sending out bills for finished work, checking on unpaid bills, and paying workers and suppliers. This is what keeps cash coming in and projects moving.

Common weekly and monthly tasks include:

- Managing Accounts Payable (A/P): This is the list of who your business owes money to. The bookkeeper tracks upcoming bills and makes sure they are paid on time. This helps you keep a good name with your suppliers.

- Managing Accounts Receivable (A/R): This is the opposite—the money your customers owe you. A bookkeeper sends out bills, tracks when they are due, and follows up on any late payments to keep your cash flow strong.

- Processing Payroll: This is a big one. The bookkeeper makes sure every employee gets paid the right amount on time. This includes figuring out wages, taking out the right amount for taxes, and sending payments.

- Bank Reconciliations: At the end of the month, the bookkeeper compares your company's bank statements to your own records. This is like balancing your checkbook, but for your business. It’s how you catch bank mistakes, fake charges, or missed payments. It’s the final check to make sure everything lines up.

Imagine running a busy company, juggling client meetings and project deadlines—now add tracking every bill, expense, and payroll entry to that list. That's what many small business owners face. The 1.6 million bookkeeping and accounting clerks in the U.S. are key because they record this money data to create complete and correct records for businesses. You can read more about the important role of these clerks on the U.S. Bureau of Labor Statistics website.

Financial Reports That Help You Make Smarter Decisions

A great bookkeeper does more than just track your money. Their real value is turning all those separate transactions into reports you can actually understand and use. They take the raw numbers and build a story, showing you exactly how your business is doing.

These reports are like your business’s dashboard. They answer the big questions: “Are we actually making money?” and “Can we afford to hire a new person?” Without them, you’re basically driving with your eyes closed.

Having this money clarity is key, yet a huge 42% of small business owners admit they knew almost nothing about finance when they started. A bookkeeper fills that gap, creating solid reports from every bill, sale, and payroll run. To see more about this, you can discover more insights about financial literacy on QuickBooks.com.

Let's walk through the three key reports your bookkeeper will give you.

The Income Statement

Think of the Income Statement (also called a Profit and Loss or P&L) as your business's report card for a certain time, like a month or a quarter. It's simple: it lists all your income, subtracts all your expenses, and shows you the bottom line—if you made a profit or had a loss.

This is the report that helps you answer questions like:

- Are my prices high enough to cover my costs?

- Is that new ad campaign actually bringing in more sales?

- Which of my services make the most money?

For example, a marketing company might use its P&L to see that while sales are up, their software costs have doubled. That one piece of information lets them look at their tools and cut what they don't need, which directly improves their profit.

The Balance Sheet

While the P&L looks at a period of time, the Balance Sheet is a snapshot of your company's money health on one specific day. It gives you a clear picture of what you own (Assets) and what you owe (Liabilities).

It all comes down to a simple formula that never changes:

Assets = Liabilities + Equity

This just means that everything the business owns was paid for in one of two ways: with borrowed money (Liabilities) or with money from owners and past profits (Equity). It's the truest measure of your business's net worth.

A balance sheet tells you, at a glance:

- How much cash you have.

- How much debt the business has.

- The total value of your equipment, products, or property.

The Statement of Cash Flows

For many small businesses, this is the most important report for survival. The Statement of Cash Flows shows exactly how actual cash has moved in and out of your business. This is important because cash in the bank can be very different from the profit you see on your income statement.

Here’s a perfect example: a real estate agency closes a huge deal and records the big payment on its P&L. On paper, the business looks very profitable. But what if that check won’t show up for another 90 days? The agency has no cash to pay its agents or cover rent.

The cash flow statement shows these kinds of timing gaps. It tells the real story of your bank account, helping you know if you have enough cash to actually run your business. It’s the report that tells you if you can afford to hire that new person or buy that new truck right now. Our guide on financial reporting for small business explains these ideas more.

Together, these three reports give you the control panel for your business. They give you the hard data you need to stop guessing and start making truly smart decisions.

How a Great Bookkeeper Helps You Grow

Sure, good bookkeeping keeps the government happy and gets your bills paid on time. But a great bookkeeper does something more—they actively help you grow your business. This is where the service stops being just about recording history and starts being a real partnership.

A great bookkeeper doesn't just look back at what happened last month. They use that same money data to build a map for where you’re going. This is the next-level value that turns bookkeeping from a simple chore into a smart investment in your company’s future.

Creating Budgets and Forecasts

Think of a budget as a plan for your money. It’s you telling every dollar where to go, instead of logging into your bank account and wondering where it all went. A great bookkeeper helps you build a real budget based on your past numbers and your future goals.

For example, a construction company might want to buy a new excavator next year. Your bookkeeper can create a budget that sets aside a certain amount of money each month, showing you exactly what sales goals you need to hit to make it happen without taking on risky debt.

But they also help with forecasting, which is a bit different.

- Budgets are your money goals—the plan you’ve set for the future.

- Forecasts are your best guess at what will actually happen, based on current info and trends.

A forecast is your early warning system. If your sales are trending lower than your budget planned, a forecast gives you a heads-up so you can change your spending or boost your marketing before you're in a bad spot.

Tracking Key Performance Indicators (KPIs)

Every business has a few numbers that tell the real story of its health. These are your Key Performance Indicators, or KPIs. A great bookkeeper doesn't just track general numbers; they help you pick and watch the right KPIs for your specific industry.

"Total sales" is fine, but it doesn't tell you why things are happening. KPIs give you information you can act on to make real changes.

A great bookkeeper helps you measure what matters. They move you beyond basic profit and loss to see the specific things that drive your business's success, helping you make smarter, faster decisions.

Let's look at some real-world examples:

- For a Marketing Agency: A key KPI is Customer Acquisition Cost (CAC). Your bookkeeper can figure out exactly how much you spend on sales and ads to get one new client. If that number starts going up, you know you have a problem with your sales or marketing that needs to be fixed.

- For a Construction Company: Gross Profit per Job is everything. Your bookkeeper tracks all the direct costs for a project—materials, labor, outside help—and compares them to the payment. This shows you clearly which types of jobs are actually making you money and which ones are just wasting your time.

- For a Healthcare Practice: A key number is the Collection Rate. This KPI tracks the percentage of billed services that are actually collected from insurance and patients. A low collection rate is a huge red flag that a bookkeeper will spot right away, helping you fix a major leak in your income.

Improving Your Cash Flow Management

Profit is a nice number to talk about, but cash is what keeps the lights on. I’ve seen plenty of "profitable" businesses fail simply because they ran out of cash. A top bookkeeper becomes your cash flow champion, actively managing the money moving in and out of your bank accounts.

And no, this isn't just about sending a few reminders for late bills. It's about building a real strategy.

For instance, they might look at who owes you money and notice that your biggest clients are always paying 60 days late, even though your terms are 30 days. With that hard data, you can have a direct talk with those clients or decide to offer a small discount for paying early.

They can also help you manage your own bills in a smart way. By creating a calendar of your payments, they can help you time them to avoid draining your bank account right before you need to pay your employees. It’s all about smoothing out the money bumps in the road so you can run your business with confidence, not worry.

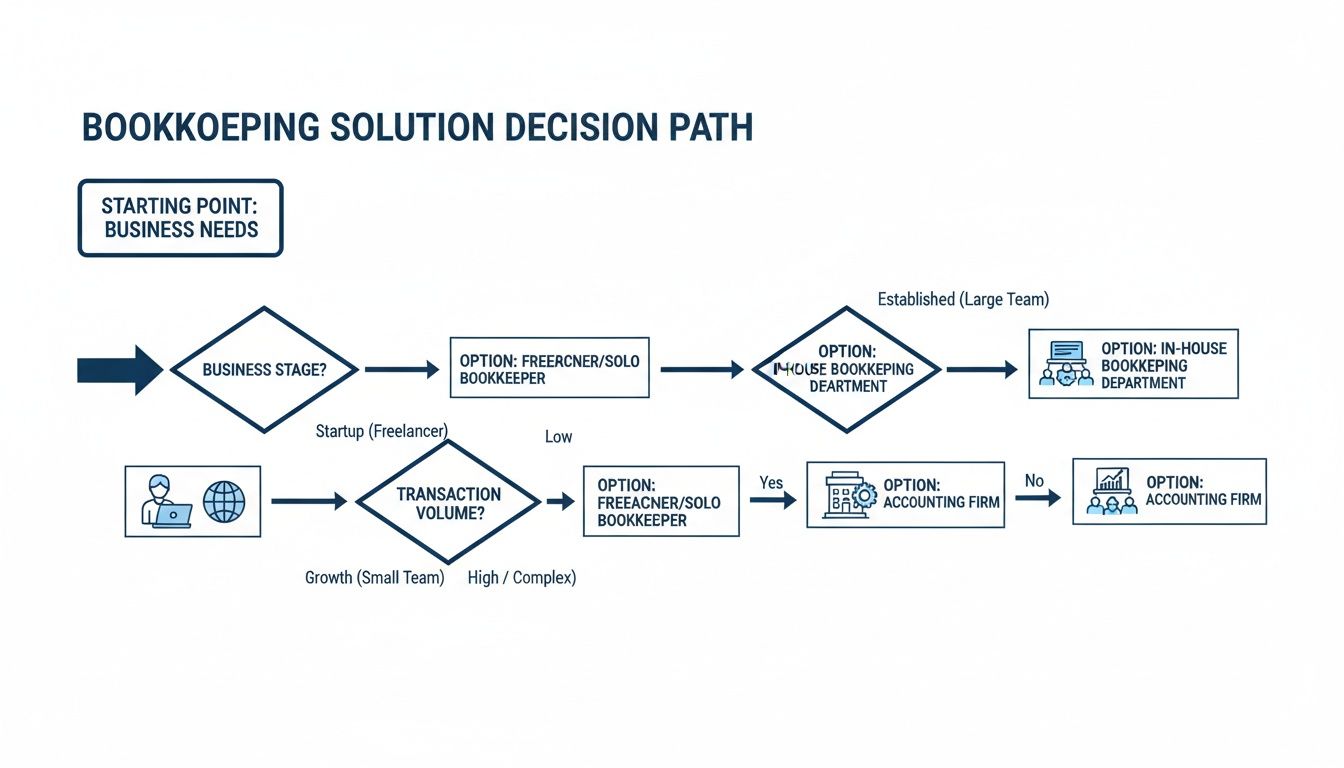

So, Who Should Handle Your Books?

Alright, you get it—you need help with your books. But what does that help actually look like? The decision is not the same for everyone. The right answer for you depends on where your business is today and where you plan to go.

You have three main paths: hiring an employee, finding a freelancer, or working with an outside firm like ours. Each has its pros and cons, and the best choice balances cost, control, and the level of help you really need.

This flowchart can help you match your current business stage to the solution that makes the most sense.

As you can see, the "right" choice often changes as your business grows and your money situation gets more complicated. What works for a new startup is rarely the best fit for a company with 15 employees and several ways of making money.

Comparing Your Three Main Options

Let's look at what each of these choices really means for your business.

The Freelance Bookkeeper: Think of a freelancer as a one-person show you hire for a set number of hours or tasks each month. This is often the cheapest starting point and works great for new businesses or those with few, simple transactions. A good freelancer will get your accounts organized, handle payroll, and create basic reports.

The In-House Bookkeeper: This is a part-time or full-time employee who works directly for you, in your company. This option gives you one person who is fully focused on your day-to-day business. It makes sense for bigger businesses with the money for a salary and benefits, and enough work to keep that person busy.

The Outsourced Bookkeeping Firm: This is when you partner with a full team of money experts. You get the deep knowledge of a professional firm without the cost and hassle of hiring an employee. It's the perfect middle ground for growing businesses—like a local construction company or a busy medical office—that need more than just data entry. They need smart advice, KPI tracking, and a partner who can grow with them.

For many owners, the search for help only starts after they've tried—and failed—to do it all themselves. It’s no surprise, since a 2021 survey found that 64% of owners are still trying to manage their own books, even when they know it's too much. Outsourcing turns bookkeeping from a chore you hate into a tool for success.

An outsourced firm offers the best of both worlds: access to a team of experts for a set monthly price. You get a team that understands your industry, not just one person.

What to Expect When Getting Started

No matter which path you take, the first few steps with any good provider should be all about understanding your business. A good money partner will want to know about your goals and problems long before they ask to see a bank statement.

The getting-started process should be this simple:

- Discovery Call: This is a simple, no-pressure chat about your business. What's working? What's keeping you up at night? We want to hear about your goals, your frustrations, and where you want to be in a year.

- Custom Plan: After that talk, a real partner will give you a clear, written plan. It should say exactly what they'll do, the software they’ll use, and what it will cost. No surprises.

- Smooth Onboarding: This is where the work gets taken off your plate. Your new partner will get safe access to your accounts, start cleaning up any past messes, and build a solid system for the future.

If you’re ready to start looking at your options, our guide on how to find a bookkeeper has more detail on how to check them out. The goal isn't just to hire help; it's to find a partner who makes your business stronger and your life easier.

A Few Questions We Hear All the Time

Even after seeing everything a bookkeeper handles, it's normal to have a few more questions. Let's go over the ones I hear most often from business owners who are in your shoes.

What's the Difference Between a Bookkeeper and an Accountant?

Let’s use a building analogy. Your bookkeeper is the crew that builds the house. They're on the job every day, doing the groundwork—pouring the foundation, putting up the walls, and making sure every piece is in the right place. They record every dollar, pay the bills, and keep your financial house solid and organized.

Your accountant is the architect and the final inspector. They take the solid house your bookkeeper built and use it for bigger-picture planning. They figure out the best tax strategy, file your official tax returns, and check to make sure everything is done right. You need both, but the daily, foundational work of the bookkeeper always comes first.

Can't I Just Use QuickBooks and Do It Myself?

Bookkeeping software like QuickBooks or Xero is a great tool. But it’s a bit like having a fancy, professional kitchen—it doesn’t automatically make you a chef. The software is only as good as the information you put into it, and it can't tell you why something looks wrong.

A good bookkeeper understands the story behind the numbers. They know how to label a tricky expense to save you the most money on taxes. They can spot when you've been charged twice or see a weird transaction that software would just accept. The program is the tool; the bookkeeper is the expert who knows how to use it to get the right results.

Software tracks what you tell it to. A bookkeeper understands what the numbers actually mean for your business and can help you make better decisions based on that information.

How Much Is This Going to Cost Me?

I get this question all the time, and the honest answer is: it depends completely on your business. There’s no single price because a local real estate office has totally different needs than a big construction company.

A few key things will affect the cost:

- Transaction Volume: A business with 500 transactions a month just needs more time than one with 50.

- Complexity: Are we just handling one bank account, or are we managing different currencies, complicated payroll, and job costs for construction projects?

- The Model: A freelance bookkeeper might charge by the hour (often $50-$100+), which can be hard to predict. An outsourced firm like ours usually gives you a flat monthly fee so your cost is always the same.

Instead of looking at it as a cost, I tell owners to see it as an investment. The time you get back and the expensive mistakes you avoid—not to mention the peace of mind—usually means professional bookkeeping pays for itself many times over. The first step is just having a conversation to see what you actually need.

At MyOfficeOps, we take the confusion out of your finances so you can focus on what you do best. If you're ready for clear reports and a true financial partner, let's talk. Schedule your free Discovery Call with us today.