You open your Profit & Loss statement hoping for answers and get a pile of labels instead.

Revenue is up. Maybe. Payroll looks heavy. Materials costs moved again. A few clients pay fast, a few don’t, and somehow your bank balance still feels tighter than the sales number says it should. You’re trying to decide whether to hire, buy equipment, raise prices, or just hold steady for another quarter. The reports tell you what happened. They don’t tell you what to do next.

That gap is where most small and midsize businesses get stuck.

In Philadelphia, I see this with law firms, clinics, agencies, contractors, and owner-led service businesses all the time. They aren’t lazy. They aren’t bad with money. They’re just busy, and the financial system underneath the business often grew piece by piece. A payroll app here. A bookkeeping file there. Spreadsheets for the rest. By the time the owner wants a clear answer, the data is scattered and late.

That’s why the phrase insight accounting solutions matters. It’s not fancy language for bookkeeping. It’s a better way to turn financial data into decisions you can use.

Your Financial Data Is Talking Are You Listening

A business owner in the Philadelphia area sits down on a Friday afternoon with three things open. The P&L. The bank app. A spreadsheet the office manager updates when she has time.

None of them agree in a way that feels useful.

The owner’s question is simple. Can we afford to bring on a project manager before the summer rush hits? The reports don’t answer it. One shows last month’s revenue. Another shows cash in the bank. A third has unpaid invoices, but half the customer names are abbreviated and a few vendor bills haven’t been entered yet.

That’s the core problem. Most businesses aren’t short on data. They’re short on usable meaning.

When bookkeeping stops at history

Traditional bookkeeping is important. You need clean records, reconciled accounts, and filed taxes. But if your accounting only tells you what happened last month, it’s like reading yesterday’s weather report while deciding whether to carry an umbrella today.

That’s why owners feel frustrated by numbers they paid good money to produce.

A solid report should help you answer questions like these:

- Hiring: Can payroll support another salary without putting pressure on cash flow?

- Pricing: Are your current rates covering labor, overhead, and the messier costs nobody sees at first glance?

- Growth: Which service lines create profit, and which ones just create activity?

- Risk: Where are the leaks, duplicate charges, unusual spending patterns, or timing issues?

For businesses that want clearer spending signals, tools built around spend analysis and anomaly detection can help surface odd transactions and patterns that are easy to miss in manual review.

What owners need

Owners rarely ask for “better accounting.” They ask for confidence.

They want to know whether the next move is safe, smart, and affordable. That only happens when the financials are current, organized, and translated into plain English.

Practical rule: If your reports create more follow-up questions than decisions, your accounting process is incomplete.

A good starting point is learning what strong reporting should look like in a small business setting. This guide on https://myofficeops.com/resources/financial-reporting-for-small-business/ is useful because it focuses on reports as decision tools, not just compliance paperwork.

Once your numbers start speaking clearly, you stop running the business by instinct alone. You still use judgment, but now the numbers back you up.

What Are Insight Accounting Solutions Really

Most owners hear “insight accounting” and assume it means expensive software, a dashboard full of charts, or a consultant using more jargon than necessary.

It’s simpler than that.

Insight accounting solutions are the people, process, and tools that turn raw financial records into practical guidance. Not just what happened. What it means, what’s changing, and what decision makes sense next.

Rearview mirror versus GPS

Traditional accounting is a rearview mirror. It shows you exactly where you’ve been.

That matters. You need accurate records. You need reconciliations. You need tax filings and financial statements.

But a rearview mirror has limits. You wouldn’t drive across Philadelphia using only that view.

Insight accounting is more like GPS. It tells you where you are right now. It helps you choose the route toward a goal. It warns you when traffic is building. It helps you reroute before you waste time and fuel.

In business terms, that means:

- Current position: What does cash look like after payroll, debt, and vendor payments?

- Route options: Is growth better served by adding staff, raising prices, tightening expenses, or improving collections?

- Traffic alerts: Are margins slipping on one service line? Are receivables stretching out? Are direct costs rising faster than revenue?

It’s a mindset first

Some owners think they need to buy a whole new system before they can do this well. Usually, that’s not the first issue.

The bigger shift is philosophical. Instead of treating accounting as a monthly chore, you use it as an operating tool.

That changes the questions you ask.

Old question: Did we make money last month?

Better question: Which work made money, which work tied up cash, and what should change before next month starts?

The best financial reporting doesn’t just close the books. It opens better decisions.

Demand for strategic guidance is rising. Xero says demand for remote CFO and advisory services surged by 40% in the last year as owners look for more forward-looking support (https://www.xero.com/).

What this looks like in daily business

A healthy insight accounting setup should help an owner do three things without waiting for year-end:

- Spot problems early

- Test decisions before committing

- See the business by driver, not just by total

That last point matters. Total revenue can hide a lot of trouble. One big client might be slow to pay. One team might be overloaded. One service might look busy but carry thin margins.

Insight accounting pulls those pieces apart so you can steer with less guesswork.

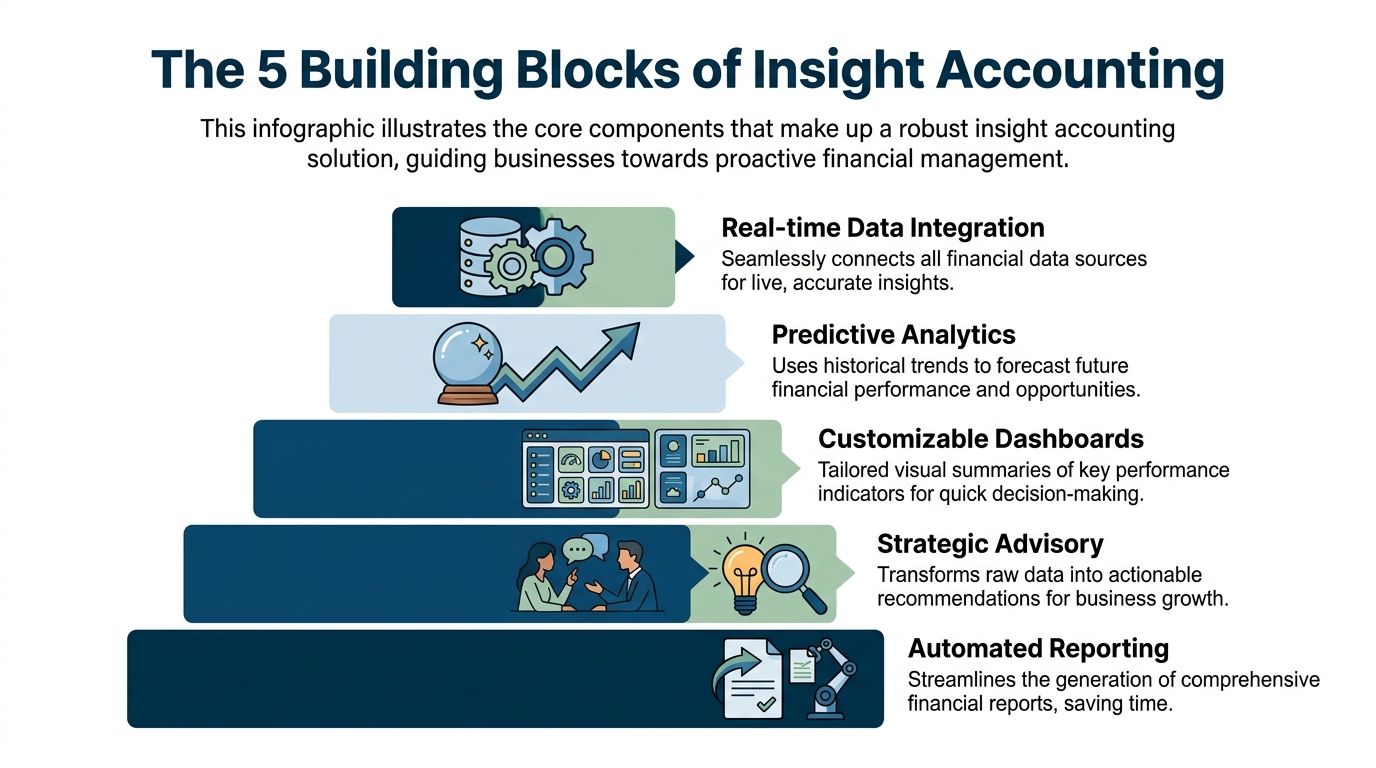

The 5 Building Blocks of Insight Accounting

The phrase sounds broad because it is broad. But in practice, strong insight accounting usually rests on five parts. If one is weak, the whole system gets shaky.

Clean data foundation

If the books are late, incomplete, or inconsistent, the advice built on top of them won’t hold up.

This is the least glamorous part of the work, but it’s the one that makes everything else possible.

A clean foundation means:

- Transactions are coded consistently

- Bank and credit card accounts are reconciled

- Loan balances, payroll entries, and sales tax items are posted correctly

- Customer and vendor records are organized well enough to track trends

Owners often want forecasting before cleanup. That’s understandable, but risky. Forecasting from messy books is like building a budget on a crooked floor.

Smart automation

Automation is not about replacing judgment. It’s about removing repetitive tasks that drain time and create avoidable errors.

Good automation handles bank feeds, recurring entries, invoice capture, approvals, reconciliations, and reporting workflows. That gives your accountant or advisor more time to interpret the numbers instead of typing them.

If you want a plain-English overview of where this helps most, this piece on automation in accounting is a practical primer.

One widely used cloud platform example is Sage Intacct. Sage says AI-powered automation can deliver a 90% faster month-end close by automating work such as reconciliation and journal entries, which leaves more room for strategic analysis (https://www.sage.com/en-us/sage-business-cloud/intacct/).

Deep analytics

Accounting becomes useful to an owner here.

Analytics answers questions that basic reports don’t answer on their own. Why did gross margin slip? Which locations or service lines generate dependable profit? Which clients absorb far more labor than expected? Why does cash feel tight even when sales look healthy?

A simple profit number is a score. Analytics tells you how the game was played.

Here’s what deep analysis often includes:

- Trend review: Looking at shifts across months, not just one snapshot

- Margin analysis: Breaking down profitability by job, client, service, or department

- Cash flow patterns: Understanding timing gaps between billing, collections, and obligations

- Variance review: Comparing actual results against plan and explaining the gap

Clear dashboards

A dashboard should not try to impress you. It should help you decide.

That means a short list of metrics, updated consistently, with labels a non-accountant can read. For one company, that may be cash on hand, accounts receivable aging, gross margin, payroll ratio, and backlog. For another, it may be patient collections, insurance lag, and provider productivity.

Owner test: If a dashboard needs a translator every time you open it, it’s not helping.

Strong dashboards show the business’s vital signs in one place. Weak dashboards bury the point in too many charts.

Human advisory

Software can organize data. It can’t sit across from you and say, “If you hire now, collections need to tighten first,” or “This client looks big but their margin is dragging down the quarter.”

That’s where human guidance matters.

A capable advisor helps you:

- connect the numbers to business choices

- challenge assumptions

- identify trade-offs

- keep the conversation grounded in reality

This part gets overlooked because it doesn’t feel technical. But it’s often the most valuable piece. The goal isn’t more reports. The goal is better judgment.

Practical Payoff What Is the ROI

Most owners don’t care about accounting features for their own sake. They care about what those features let them do.

Can we stop the cash surprises?

Can we price work with more confidence?

Can we grow without creating chaos?

That’s the key return.

Better timing, not just better math

The first payoff is speed with trust.

If reports arrive late, you make decisions late. If they arrive fast but need correction, you still hesitate. That’s why process improvement matters so much. insightsoftware says firms using automated accounting solutions see 50 to 70% faster financial reporting cycles and a 40% reduction in audit adjustments, which gives leadership more time and cleaner information for growth decisions (https://insightsoftware.com/accounting/).

That improvement matters because timing changes outcomes.

A staffing decision made two months too late can strain delivery. A pricing change made one quarter too late can lock in low-margin work. A cash issue noticed after the bank balance gets tight limits your options.

Where owners usually feel the gain

The payoff often shows up in a few practical areas first.

Cash flow visibility

A profitable business can still feel broke if cash arrives late and bills come due early.

Insight accounting helps you look ahead instead of staring at the checking account and hoping the month works out. You can see collection patterns, payroll timing, debt obligations, and expected vendor pressure before they collide.

Pricing discipline

A lot of businesses underprice because they only look at direct labor and obvious materials.

Once you layer in overhead, admin load, rework, payment delays, and seasonality, a “good” client or project can look a lot less good. Better reporting helps owners price work for reality, not optimism.

Smarter hiring calls

Hiring is one of the most emotional decisions an owner makes.

With stronger insight, the question changes from “Do we feel busy?” to “Can current and projected margins support this role without squeezing cash?” That’s a much better question.

Focus on profitable work

Some clients buy a lot and still wear your team out. Some jobs look exciting and eat margin. Insight accounting helps separate volume from value.

A business grows faster when it knows what to repeat and what to decline.

A useful way to think about ROI is simple: what costly mistakes become less likely once your numbers are timely and clear? That’s often where the return starts.

If you want a simple framework for evaluating that return in dollars and decisions, this guide on https://myofficeops.com/resources/how-to-calculate-return-on-investment/ is a good place to start.

One practical example

Take a professional services firm reviewing project bids.

If the owner only sees total revenue and total payroll, every proposal feels like a rough guess. But once historical project profitability is tracked by scope, labor mix, write-downs, and timeline, bidding improves. The firm can spot the kinds of work that travel well through the business and the kinds that create noise without enough margin.

That’s what ROI looks like in real life. Fewer blind spots. Better calls. Less expensive learning.

Insight Accounting in Action Philadelphia Business Stories

The idea gets easier to grasp when you see how it plays out in actual businesses.

A Center City law firm stops confusing revenue with partner performance

A growing law firm in Center City looked busy from the outside. Bills were going out. Revenue looked solid. The partners were working hard.

But the owners still had a nagging problem. They couldn’t tell which matters were profitable after write-offs, support time, and collection delays. One practice area brought in high fees but required heavy attorney involvement and a lot of cleanup after billing. Another looked smaller on paper but collected faster and created less drag on staff.

Once the firm started looking at profitability by matter type and payment pattern, the conversation changed. Instead of asking, “Who billed the most?” they started asking, “Which work turns into clean, usable profit?”

That kind of shift often improves partner decisions faster than any generic budget meeting ever will.

A Main Line healthcare practice gets ahead of timing gaps

A healthcare practice on the Main Line had a familiar problem. Payroll hit on schedule. Insurance payments did not.

The books weren’t technically broken. But the owner was still making choices under stress because the timing between services rendered and money received was uneven. Some weeks looked fine. Others felt tight for no obvious reason.

With better forecasting and cleaner visibility into receivables timing, the practice could plan around the lag instead of reacting to it. That changed simple but important decisions:

- Staff scheduling: Matching labor planning to expected cash timing

- Vendor payments: Knowing when to pay promptly and when to preserve flexibility

- Owner distributions: Taking money out based on real operating capacity, not hopeful assumptions

In healthcare, “profitable” on paper can still mean “tight” in the bank if collections are delayed.

The owner didn’t need more reports. The owner needed a clearer sequence of what money was coming, when, and what had to be covered first.

A West Chester contractor catches margin bleed before it gets buried

A contractor based in West Chester had plenty of job activity. Crews were active. Equipment was moving. Invoices were being sent.

But the owner had the classic construction problem. By the time a project looked bad in the financials, the damage had already happened.

Integrated job costing changes that. The Construction Financial Management Association says companies using job costing reports integrated with their main accounting system see an average 15 to 20% improvement in project profitability by catching budget overruns sooner (https://cfma.org/).

That matters because small overruns don’t stay small for long when labor, materials, and schedule changes stack up.

In practice, the contractor needed to know three things quickly:

- Which jobs were drifting from estimate

- Whether labor hours were tracking to plan

- Which change orders were approved, pending, or not billed yet

Once that information became visible in time to act on it, job reviews stopped being postmortems. They became management tools.

That’s the thread across all three stories. The books moved from recordkeeping to guidance. And once that happens, owners stop guessing as much.

How to Implement Insight Accounting in Your Business

Most businesses don’t need a dramatic overhaul. They need a sensible sequence.

Trying to jump straight into dashboards and strategy before fixing the accounting basics usually creates frustration. A better path is steadier and a lot more useful.

Start with cleanup

If your books are behind, inconsistent, or full of workarounds, fix that first.

This means cleaning the chart of accounts, reconciling balance sheet accounts, checking payroll postings, reviewing accounts receivable and payable, and making sure recurring transactions are handled consistently. It also means deciding who owns what. Many accounting problems are really process problems wearing an accounting costume.

Ask simple questions:

- Are reports current enough to trust?

- Do bank balances reconcile cleanly?

- Can we explain major balance sheet items without hunting through emails?

- Do we have one source of truth for invoices, bills, and payroll data?

If the answer is no to several of those, cleanup is the right first move.

Choose tools that work together

Owners often buy software one pain point at a time. Payroll gets solved first. Then invoicing. Then expense management. Then reporting. Pretty soon the stack is fragmented.

A better setup connects your core systems so data doesn’t have to be hand-carried from one tool to another.

Look for fit, not flash. The best system is the one your team will use consistently and your advisor can support well. In some businesses, remote support also matters. For firms that need a mix of virtual help and hands-on operational support, reviewing options like https://myofficeops.com/resources/on-site-accounting/ can help clarify what level of involvement makes sense.

Pick a service model that matches your growth stage

The structure of the relationship matters as much as the tools.

A 2025 AICPA report found that 68% of SMBs using tiered accounting service models reported actionable profitability insights 25% faster than businesses using traditional ad hoc services (https://www.aicpa.org/).

That finding lines up with what many owners feel in practice. If support is only reactive, insight arrives late. If support follows a structured model, decision support tends to be more consistent.

Good accounting support should feel like an operating rhythm, not a rescue mission.

Checklist for choosing an accounting partner

| Question to Ask | What a Good Answer Sounds Like | Red Flag |

|---|---|---|

| How do you keep books current and accurate? | They explain a repeatable close process, reconciliations, review steps, and deadlines in plain English. | “We’ll clean things up as needed.” |

| What reports will I get each month? | They name the reports, explain what each one means, and connect them to business decisions. | They talk only about tax filings or generic financial statements. |

| How do you handle payroll and cash flow visibility? | They describe how payroll data, reporting, and forecasting work together. | Payroll is treated like a separate afterthought. |

| Can you help us understand profitability by client, service, or job? | They ask how your business makes money and suggest ways to track margin by driver. | They only discuss total revenue and total expenses. |

| What happens if our needs grow? | They can describe a path from bookkeeping to analytics to advisory support. | They offer one fixed service with no room to expand. |

| How do you communicate with clients? | You hear specifics about response times, meetings, ownership, and who to contact. | You’re not sure who will handle the work or when you’ll hear from them. |

| What does onboarding look like? | They lay out a clear handoff, document request list, cleanup plan, and timeline. | Onboarding sounds improvised. |

A good partner doesn’t just promise clean books. They show you how clean books turn into usable answers.

MyOfficeOps Is Your Philadelphia Insight Accounting Partner

For Philadelphia-area businesses that want more than basic bookkeeping, MyOfficeOps is built around the exact shift this article has been talking about. The firm helps owners move from scattered records and after-the-fact reporting to a system that supports decisions on cash flow, pricing, hiring, and growth.

That matters because insight accounting solutions only work when the service model is designed for insight, not just compliance.

A three-tier model that matches how businesses grow

MyOfficeOps organizes support around three levels.

Core Accounting gives owners the stable base. Clean books, day-to-day bookkeeping, account management, payroll integration, and reporting that’s readable.

Profit Optimization goes further. With Profit Optimization, financial analytics, KPI dashboards, forecasting, budgeting, and profitability consulting help owners understand what’s driving results, not just what showed up on the statement.

Exit Strategy supports the bigger picture. Business valuation, M&A readiness, and enterprise value planning help owners prepare for transition, sale, or long-term succession.

That structure matters because businesses rarely need the same level of support forever. They need a partner that can meet them where they are and help them move forward without rebuilding the whole relationship every time the company changes.

Why that works for Philadelphia SMBs

Local owners usually don’t want a giant firm with layers of handoffs and slow replies.

They want someone who answers the phone, explains reports without jargon, and understands the practical realities of running a business in this market. That includes professional services firms trying to price work correctly, healthcare practices managing payroll against uneven collections, and contractors trying to protect margin job by job.

MyOfficeOps brings that mix of local understanding and broader advisory capability.

What the experience feels like

The process is straightforward. Discovery Call. Custom Plan. Smooth Onboarding. Ongoing Growth Partnership.

That sounds simple because it should be simple.

The best accounting relationship feels less like outsourcing and more like having a steady financial operator in your corner.

For owners in West Chester, Greater Philadelphia, and beyond, MyOfficeOps offers the kind of support that turns accounting from a monthly task into a working roadmap.

From Overwhelmed to In Control

A lot of owners think the answer is more effort. Read more reports. Ask more questions. Stay later. Check the bank balance one more time.

Usually, the answer is a better system.

When your books are clean, your tools connect, your reports are clear, and your advisor can translate the numbers into action, the business feels different. You stop reacting to old information. You start steering with current information. That changes hiring decisions, pricing choices, cash flow planning, and growth strategy.

That’s what good insight accounting solutions are for.

They don’t exist to make accounting look smarter. They exist to help you run the business with less guesswork.

If you’ve been living with reports that feel late, confusing, or disconnected from real decisions, you don’t need to stay stuck there. You can move from overwhelmed to in control. And once you do, the numbers stop feeling like a burden and start acting like a tool.

If you want help turning messy books into clear decisions, schedule a Discovery Call with MyOfficeOps. They’ll help you build a financial roadmap that fits the way your business runs.