You might be in that spot right now. The business is doing fine. Clients still call. Payroll still runs. But for the first time, you're wondering what an exit would look like.

Maybe you're tired. Maybe you want to retire. Maybe you don't want to carry the whole thing on your back for another decade. Or maybe you want to know what you've built before you decide what comes next.

Most owners think valuation starts with a formula. It doesn't. It starts with clarity. If you want to know how to value a small business for sale, you need to understand what a buyer is buying, what risk they think they're taking, and how clearly your numbers support the story.

For small service businesses around West Chester, Philadelphia, and the surrounding counties, that story usually isn't about machinery or real estate. It's about reliable cash flow, client relationships, repeat work, good systems, and whether the business can keep running when the owner steps back.

Your Business Is Worth More Than Just Numbers

A lot of owners open their profit and loss statement and expect it to tell the whole truth. It rarely does.

Two businesses can show similar profit on paper and have very different value. One has recurring clients, a strong manager, clean books, and simple handoff procedures. The other depends on the owner for every sale, every client fire drill, and every hard decision. A buyer won't treat those businesses the same.

Buyers aren't paying for your effort

This is the hard part. Buyers don't pay you for the years you worked late, the weekends you gave up, or the stress you carried. They pay for what they believe the business will produce after they take over.

That means your valuation sits at the intersection of math and trust.

If you're a bookkeeping firm, a consulting company, a healthcare practice, or a specialty construction business, your value often lives in places that don't show up neatly on the balance sheet:

- Client loyalty: Do people stay with you?

- Repeatable work: Is revenue one-off, or does it renew?

- Transferability: Can someone else step in without chaos?

- Documentation: Are processes in your head or in writing?

- Team depth: Does the business rely on one person?

A buyer is asking one simple question. “If I write this check, what exactly am I getting, and how much of it disappears when the owner leaves?”

The story behind the numbers matters

I've seen owners undersell themselves because they only talked about tax return profit. I've also seen owners ask too much because they confused reputation with transferable value.

The right approach sits in the middle. You build a case with numbers, then explain why those numbers are dependable.

Think about a small healthcare support business in the Philadelphia area. If the owner has long-standing client relationships, clear monthly reporting, recurring contracts, and staff who handle day-to-day work, that business usually tells a stronger story than another firm with the same revenue but constant client churn and no systems.

Value is usually a range, not one magic number

A serious valuation rarely lands on one perfect figure. It usually produces a reasonable range.

That range gets tighter when:

- the books are clean,

- the earnings are normalized,

- the owner can explain unusual expenses,

- and the business has proof that its cash flow is sustainable.

If your numbers are messy, buyers widen the risk discount. If your records are strong, buyers spend less time guessing.

That shift alone can change the conversation from “prove this is real” to “let's talk terms.”

First Get Your Financial House in Order

Before anyone tries to price your business, clean up the books.

That's not glamorous advice, but it's the advice that matters most. Buyers don't want a pile of statements they have to decode. They want a clear picture of what the business earns, what expenses are personal or unusual, and what a new owner could expect to keep.

Selling a business is a lot like selling a house. You don't leave laundry on the stairs and hope people see the potential. You clean it up, fix what's obvious, and make it easy for someone else to picture living there.

Start with normalized earnings

For many owner-operated small businesses, the reported net profit is only the starting point.

Owners often run legitimate but non-transferable expenses through the company. That can include the owner's salary, certain benefits, or personal items mixed into business spending. A buyer wants those items pulled apart so they can see the actual earning power of the business.

That adjustment process is called normalizing the financials.

What SDE means in plain English

Seller's Discretionary Earnings, or SDE, is commonly used for businesses with under $600,000 in SDE because it adds back the owner's salary and perks to show the true cash flow available to a buyer, according to Grifco's explanation of small business valuation methods. The same source notes that SDE multiples typically range from 2x to 4x, and gives a simple example where a business with $100,000 in profit at a 10% capitalization rate would be valued at $1,000,000.

If that sounds abstract, think of it this way. SDE asks, “What does this business produce before the current owner's personal choices muddy the picture?”

Common add-backs owners should review

Not every expense should be added back. That's where people get sloppy.

A proper add-back should be supportable. You need to show why it was personal, one-time, or non-operating. If a buyer thinks an expense will continue after closing, they won't accept the adjustment.

Here are the categories owners usually examine:

- Owner compensation: If your current salary is above or below what a future operator would pay, it needs context.

- Personal benefits: Health insurance, personal vehicle costs, and similar items may be added back if they aren't required for the business to run.

- One-time costs: A legal dispute, a one-off consultant project, or an unusual equipment purchase might be adjusted if it won't repeat.

- Non-business spending: Meals, travel, subscriptions, or family-related costs sometimes creep in. Buyers will look for them.

- Extraordinary repairs or unusual losses: If the event was not part of normal operations, explain it clearly.

Practical rule: If you can't defend an add-back with records and plain English, don't count on a buyer accepting it.

Where EBITDA fits

For somewhat larger businesses, buyers and advisors often use EBITDA, which stands for earnings before interest, taxes, depreciation, and amortization.

EBITDA strips out financing and certain accounting items so buyers can compare operating performance more cleanly. It's especially useful when the business has enough scale that the owner's personal compensation is less central to the valuation story.

SDE is often better for owner-led businesses. EBITDA is often better when the company is becoming more management-run.

A simple cleanup process

If you're getting your books ready for a sale, use a workshop mindset. Pull the records apart and label what belongs where.

Pull your profit and loss statements

Use consistent statements for multiple years. Make sure account names haven't changed in confusing ways.

Mark owner-related expenses

Review compensation, benefits, reimbursements, and anything personal that flowed through the company.

Separate one-time items

If you had an unusual event, flag it and keep backup documentation.

Fix categorization errors

Misclassified expenses create noise. Clean them up now, not during buyer diligence.

Tie the story to documents

If an adjustment matters, support it with payroll records, invoices, bank detail, or contracts.

A lot of this comes down to process discipline. If your payables, receipts, approvals, and expense coding are messy, your valuation work gets messy too. That's why it helps to tighten your back office before you ever go to market. Even operational topics like AP automation best practices matter here, because cleaner transaction flow makes your earnings story easier to prove.

Buyers want proof, not explanations after the fact

When a buyer sees too many vague adjustments, they start assuming more risk.

That's why many sellers benefit from a structured earnings review before going to market. A quality of earnings report helps test whether the earnings are clean, repeatable, and defensible. If you want to understand what that process looks like, this overview of a quality of earnings report is a useful starting point.

The goal isn't to make the numbers look better than they are. The goal is to make them clearer than they are now.

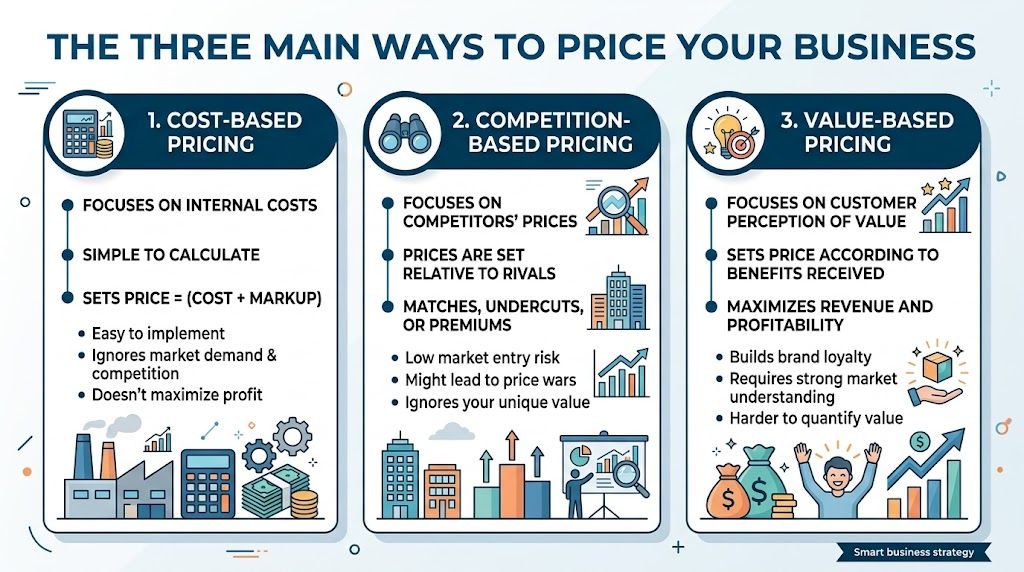

The Three Main Ways to Price Your Business

A business can be looked at from three different angles. Good valuations usually compare all three, then decide which one deserves the most weight.

For a service business, one method often matters more than the others. But if you ignore the rest, you're leaving holes in your own argument.

Market approach

This is the house comp method.

You look at what similar businesses have sold for and ask whether your company deserves to be in that same neighborhood, above it, or below it. That sounds simple. In practice, it gets messy fast.

Small business comparables aren't always easy to find, especially for local service firms. A bookkeeping practice in West Chester isn't automatically comparable to a firm in another region with a different client mix, pricing model, and staffing structure.

Still, the market approach matters because buyers think this way. They want to know what else they could buy for the same money.

Use this approach when:

- You have access to real comparables: Not guesses, not online rumors.

- Your business model is common enough to compare: This is easier in established industries.

- You need a market reality check: It helps prevent pricing from drifting too high.

Asset-based approach

This one is the floor.

You add up the assets, subtract the liabilities, and see what's left. For equipment-heavy businesses, that can be a meaningful part of total value. For service firms, it often understates what the company is worth.

A consulting firm, advisory practice, or healthcare support business may not own much beyond laptops, software, and furniture. Its primary value may sit in contracts, client relationships, systems, and staff know-how. The asset method doesn't capture those very well.

That doesn't make it useless. It gives you a baseline.

If the income story falls apart, buyers often look back to the asset floor.

Use this approach when:

- The business owns significant hard assets

- Profit is inconsistent

- You need a floor value for negotiation

- The buyer is focused on downside protection

Income approach

For many profitable service businesses, the serious conversation unfolds at this stage.

The income approach asks a simple question. What is the future earning power of this business worth today?

That can be measured in a few ways. One common small business method is capitalizing SDE. Another is using EBITDA multiples. A more detailed version is Discounted Cash Flow, or DCF, which projects future cash flow and discounts it back to present value.

According to Entrepreneurs Forever's guide to calculating small business value, the EBITDA Multiple Method is the most frequently used valuation approach, with small to medium-sized businesses often valued at three to six times their two-year average EBITDA. The same source notes that businesses with SDE under $600,000 typically use a Capitalization of SDE method instead.

How the methods compare

Comparing Business Valuation Methods

| Method | How It Works (In Simple Terms) | Best For |

|---|---|---|

| Market approach | Compare your business to similar businesses that already sold | Owners with access to reliable comps |

| Asset-based approach | Add up what the business owns, subtract what it owes | Asset-heavy companies or floor-value analysis |

| Income approach | Value the business based on the cash flow it can produce | Profitable service businesses with dependable earnings |

DCF is useful, but not always practical

DCF is often treated like the smart, advanced option. Sometimes it is. Sometimes it's just a spreadsheet with assumptions stacked on top of assumptions.

A proper DCF projects future profits over a defined period, often 3 to 5 years, and discounts them back using a risk-adjusted rate that typically ranges from 10% to 25%, according to Axial's discussion of valuing a company for sale. That same source also notes that over-optimistic projections can create valuations 20% to 40% higher than what buyers will accept.

DCF can work well when the business has stable forecasts, recurring revenue, and a clear growth path. It can be less helpful when the owner is guessing.

What usually works best for service firms

For many local professional service, healthcare, and construction businesses, the strongest valuation usually comes from combining methods instead of forcing one answer.

A practical sequence looks like this:

- Start with normalized earnings

- Check whether SDE or EBITDA fits better

- Test the result against real market data

- Use asset value as a floor, not the headline

- Use DCF only if the forecasts are grounded in reality

The point isn't to impress anyone with complexity. The point is to show a buyer that the number has logic behind it.

Applying a Multiple How to Pick the Right Number

At this stage, valuation stops being mechanical.

A multiple is not a prize you award yourself. It's a shorthand way of pricing risk, transferability, and upside. That's why two businesses with similar earnings can land at very different values.

A lot of owners hear a number from a friend, a broker, or a podcast and latch onto it. That's dangerous. A multiple only makes sense in context.

Buyers pay more when the business is less fragile

If a buyer thinks revenue will hold after the transition, the multiple usually improves. If they think revenue is tied to your cell phone, your reputation alone, or your memory of how things work, the multiple usually tightens.

That means the multiple reflects more than profit. It reflects confidence.

Here are the factors that usually matter most.

- Recurring revenue: Monthly retainers, service agreements, and repeat billing create predictability.

- Low customer concentration: A buyer gets nervous when too much revenue depends on one or two clients.

- Documented processes: Written workflows reduce transition risk.

- Team coverage: If a manager or senior staff member can carry operations, that helps.

- Stable margins: Consistency matters. Sharp swings create questions.

- Transferable relationships: If clients trust the firm, not just the founder, value holds better.

Intangibles count, but only if you can prove them

This is the part most generic valuation articles miss.

For service-based firms with few physical assets, the most important drivers are often intangible. Clearly Acquired's overview of the three core valuation methods notes that client retention rates of 80% to 90%, documented processes, and a strong brand can justify 3x to 5x revenue multiples for some firms. The same source warns that limited local comparable data often causes sellers to overestimate value by 20% to 30%.

That doesn't mean every service firm gets that kind of multiple. It means the business may deserve stronger pricing when those intangibles are real and transferable.

What this looks like in the Philadelphia market

In Greater Philadelphia, a buyer looking at a local service company usually wants answers to practical questions:

- Will the clients stay after the owner transitions out?

- Are contracts in writing and current?

- Does the team know how work gets done?

- Can the reporting package show client-level profitability?

- Are there sectors with stable demand, such as healthcare, construction, or professional services?

A good reputation helps. A documented handoff plan helps more.

The market gives credit for reputation only when a buyer believes that reputation belongs to the company, not just the founder.

A stronger multiple comes from reducing owner dependence

If you want to push toward the higher end of a valuation range, work on what a buyer sees as risk.

A buyer doesn't want to inherit a job. They want to acquire a business.

That means you should tighten the areas that usually drag down a multiple:

| Risk that hurts value | Change that helps |

|---|---|

| Owner approves everything | Managers handle routine decisions |

| Client knowledge lives in your head | SOPs and CRM notes capture it |

| Revenue is mostly one-off | More contract or retainer work |

| Pricing is inconsistent | Standard pricing logic is documented |

| Financials are delayed | Monthly close and reporting are reliable |

If you want a more grounded view of how buyers think about this by sector, this resource on business valuation multiples by industry can help frame the discussion.

The multiple isn't random. It's the score a buyer gives your business for being durable.

Putting It All Together A Valuation Example

Let's make this practical with a fictional Philadelphia-area consulting firm.

The owner has built a solid business over time. Revenue is healthy. Clients are a mix of project work and ongoing monthly advisory. The books show profit, but like many owner-led firms, they also include several expenses that need a closer look before anyone tries to set a price.

Step one is cleaning the earnings

The first pass through the profit and loss statement shows owner compensation, health insurance paid through the business, and a handful of expenses labeled as marketing that don't all appear to be ongoing operating costs.

None of that means the owner did anything wrong. It just means the statements were built for running the business and filing taxes, not for marketing the business to a buyer.

So the first job is to normalize the earnings:

- remove or explain owner-specific expenses,

- isolate anything one-time,

- and separate true operating costs from personal or unusual items.

Now the buyer can see what the business is likely to produce under ordinary conditions.

Step two is deciding which lens fits

Because this is a service firm with limited hard assets, the asset-based method won't tell the full story. It may provide a floor, but not the headline value.

The income approach will usually carry more weight here. If the business is still highly owner-led, SDE may be the cleaner lens. If a management layer is in place and the owner's role is less central, EBITDA may become more useful.

The market approach also matters, but only if the comparable businesses are comparable in size, service mix, and client quality.

Step three is choosing a realistic multiple

This is where judgment matters.

If the firm has a strong base of retainer clients, clear process documentation, and team members who can retain accounts after the transition, the valuation story strengthens. If most revenue comes from a few relationships tied tightly to the owner, the buyer will pull back.

A lot of owners make the same mistake here. They build a forecast that assumes smooth growth, no client losses, and no transition friction. That can make the business look better on paper than it will look in a buyer's model.

Axial's guidance on DCF valuation warns that overly optimistic growth projections can produce valuations 20% to 40% above what buyers will accept. That's why any forecast should be checked against market reality before it becomes part of your asking story.

Keep the forecast believable. A buyer will forgive caution faster than they will forgive fantasy.

The final answer is usually a range

After the earnings are cleaned up and the risk factors are weighed, the owner has something useful. Not a vanity number. A defensible range.

That range gives the seller a better basis for pricing, deal structure, and negotiation. It also tells them what still needs work before going to market.

For most owners, that's the moment the process becomes real. The business stops being a personal extension of themselves and starts becoming an asset someone else could buy with confidence.

Beyond the Number How to Actively Boost Your Sale Price

A valuation is not a final judgment. It's a snapshot.

That's good news, because snapshots can change. If you're planning to sell in the near future, the smartest move isn't just finding out what the business is worth today. It's improving what a buyer will see when they look at it later.

Build the file cabinet before you need it

Serious buyers will ask for documents. A lot of them.

If those records are scattered across inboxes, desktops, and old folders, diligence gets slow and trust starts slipping. Put together a clean data room early.

That usually includes:

- Financial statements: Consistent reports that tie back to tax filings and bookkeeping records

- Client contracts: Current agreements, renewal terms, and any assignment language

- Payroll and org information: Who does what, and who holds key relationships

- Vendor agreements: Important outside dependencies

- Process documentation: SOPs, training notes, handoff guides, checklists

- Legal and compliance files: Licenses, leases, insurance, and entity records

A buyer reads organization as competence.

Focus on changes that make the business transferable

If you want a higher sale price, make the company easier to own.

That often means working on a small group of value drivers:

- Increase recurring revenue: Retainers and ongoing service agreements usually tell a stronger story than one-off projects.

- Reduce owner reliance: Shift delivery, sales, or account management away from yourself where possible.

- Clean up contracts: Expired agreements and handshake arrangements create uncertainty.

- Sharpen reporting: Monthly close, KPI tracking, and client profitability analysis help buyers get comfortable faster.

- Protect margins: Buyers notice whether profit comes from a healthy model or from owner overwork.

Know when DIY stops helping

Owners should absolutely understand the basics. But there comes a point where self-valuing can turn into self-justifying.

That's especially true when:

- the books need normalization,

- the add-backs are debatable,

- the buyer asks for support,

- or local comparables are hard to interpret.

At that stage, outside help usually adds value because it brings discipline and objectivity. If you're thinking through positioning as well as pricing, this guide on selling a business for maximum value offers a useful lens on preparation and deal readiness.

If you're planning a sale, transition, or even just a future exit path, it also helps to review the moving pieces in a practical sale process. This overview of how to sell a business gives a useful framework for that.

The owners who do best in a sale process usually don't wait until the business is listed to start acting like sellers. They clean the books early. They document the operation. They build a business that can survive their absence.

That is what buyers pay for.

If you want a clear, practical view of what your business is worth and what would raise that number before a sale, MyOfficeOps helps business owners in Greater Philadelphia organize financials, normalize earnings, and prepare for exit conversations with facts instead of guesswork.