A lot of owners try to run the business off two things. The bank balance and a gut feeling.

That works right up until it doesn't. A contractor sees cash in the account and green-lights a truck purchase. A practice owner adds a staff member because the schedule looks full. Then payroll hits, a client pays late, supplies cost more than expected, and suddenly everyone is asking the same question. Where did the money go?

If that's where you are, you don't need a prettier spreadsheet. You need a budget that helps you make decisions before the pressure shows up.

Stop Guessing and Start Planning

A working budget is not a punishment. It's a decision tool.

For a construction company in Chester County, that might mean knowing whether you can take on another estimator before spring ramps up. For a healthcare practice, it might mean deciding if a new provider, billing software change, or equipment lease fits the next few months without creating a cash squeeze.

What a budget really does

Most owners think a budget is just a list of limits. That view is too small.

A budget is your best estimate of what the business is going to do next. Revenue in. Payroll out. Materials, rent, insurance, subscriptions, loan payments, taxes, and the money you need to keep in reserve. It turns vague plans into numbers you can test.

The most widely taught budgeting method uses a 50/30/20 split for needs, wants, and savings, and that same idea can work in a business by creating simple buckets for core obligations, flexible spending, and reserves (Citizens Bank budgeting guidance). The point isn't that every business should force itself into that exact split. The point is that simple buckets make decisions easier.

Practical rule: If your budget has so many categories that you stop using it, it's not helping you.

What works and what doesn't

What works is a budget tied to real decisions. Hiring. Raises. Owner draws. Equipment. Marketing. Debt payoff. Tax planning.

What doesn't work is looking at your checking account on a Tuesday and saying, "We seem fine."

I've seen owners confuse cash in the bank with profit, and I've seen profitable businesses get tight on cash because they had to front labor or supplies before collections came in. That's why good budgeting has to connect to bookkeeping, reporting, and the kind of ongoing review you see in solid effective financial management strategies.

If you want to learn how to create a budget that is effective in practice, start with a simple idea. Every dollar in the business has a job. Your budget tells you what that job is before the month starts.

Gather Your Financial Puzzle Pieces

Before you build a budget, gather your history. If the history is messy, the budget will be messy too.

That doesn't mean you need perfect books before you begin. It does mean you need enough clean information to stop guessing.

Pull the right reports

Start with the last 12 to 24 months of financial activity from your accounting system, bank records, payroll reports, and loan statements. You're trying to see patterns, not create a museum archive.

Here are the three reports that matter most:

- Profit and loss statement. This shows whether the business was profitable over a period. It helps you spot trends in revenue, payroll, supplies, subcontractors, rent, software, and other operating costs.

- Cash flow activity. This shows when money moved. That's a different question from profit. A month can look fine on paper and still feel tight if cash came in late.

- Balance sheet. This tells you what the business owns and owes. Loans, credit cards, equipment debt, sales tax payable, and old receivables all affect how realistic your budget needs to be.

If you want a plain-English refresher on what these reports mean, this guide on how to read financial reports is worth keeping open while you sort through your numbers.

Know why each report matters

Owners often grab a P&L and stop there. That's not enough.

A P&L can tell a medical practice that provider revenue covered payroll and overhead. It won't always tell you whether insurance payments came in when expected. A contractor's P&L can show a profitable quarter while cash is tied up in jobs that haven't billed cleanly yet.

Clean books save time twice. Once when you pull reports, and again when you trust what they say.

The same report can mean different things depending on the business. In a service firm, labor utilization may be the key issue. In construction, job materials and timing may drive the biggest swings. In healthcare, payroll, collections, and reimbursement delays usually deserve a closer look.

Gather more than reports

Pull supporting detail too. Not forever. Just enough to explain the story behind the reports.

Use this short checklist:

- Bank statements for operating and savings accounts

- Credit card statements so recurring charges don't get missed

- Payroll summaries including taxes and benefits

- Loan and equipment payment schedules

- Lease agreements for office, vehicle, or equipment costs

- Major vendor bills for materials, lab costs, software, or supplies

- Accounts receivable aging so you know who still owes you

If you're weak on reading a P&L line by line, this article on P&L insights for DTC growth is written for a different business model, but the core lesson still applies. You can't budget well if you don't understand which lines drive profit.

Watch for bad history

This part matters more than owners think. A bad budget often starts with bad categorization.

Examples:

- A truck payment buried under "miscellaneous"

- Owner personal spending mixed into office expenses

- Payroll taxes lumped into wages

- Equipment purchases mixed with repair expense

- One-time legal bills treated like normal monthly overhead

Those errors create false averages. Then the budget gets built on numbers that never meant what you thought they meant.

If your books are clean, this step is straightforward. If they're not, slow down and fix the chart of accounts, recode obvious errors, and separate one-time items from normal operations. Budgeting from bad books is like framing a house on a crooked slab.

Map Your Money In and Out

Once your history is in front of you, sort it into categories that make sense for how the business runs.

Often, owners overcomplicate the budgeting process. They create too many lines, too many tabs, and too many little buckets nobody reviews. Keep it clear enough that you can scan it in a few minutes and know what changed.

Group income by how you earn it

Start with revenue.

A healthcare practice might split income by provider services, recurring patient programs, and ancillary services. A contractor might split by residential jobs, commercial jobs, service calls, and change orders. A professional service firm might separate recurring retainers from project work.

That matters because not all revenue behaves the same way. Some is steady. Some arrives in bursts. Some comes with heavy labor or materials attached.

Ask yourself:

- Which revenue streams are consistent?

- Which ones are seasonal?

- Which ones carry the best margins?

- Which ones create the most strain on labor or cash?

Sort expenses by behavior

The best budgets don't just list expenses. They classify them by how they move.

Use three broad types.

| Category | Type | Examples |

|---|---|---|

| Payroll and admin salaries | Fixed | Office manager pay, salaried staff, standard benefits |

| Rent and core software | Fixed | Office rent, EMR subscription, accounting software, phone systems |

| Insurance and debt payments | Fixed | Liability insurance, vehicle insurance, equipment loan payments |

| Job materials or clinical supplies | Variable | Lumber, concrete, disposables, lab supplies, medical inventory |

| Subcontractors and hourly labor | Variable | Specialty trades, per-diem staff, overtime tied to workload |

| Sales and delivery costs | Variable | Merchant fees, mileage, shipping, jobsite fuel |

| Owner perks and optional spend | Discretionary | Team events, upgraded software you don't use fully, nonessential travel |

A fixed cost tends to show up whether sales are strong or weak. A variable cost rises and falls with work volume. A discretionary cost is usually optional or easier to delay.

Keep categories useful

A good category helps you answer a business question.

"Materials" is useful if you're trying to control job costs. "Office stuff" is not. "Clinical supplies" is useful if reimbursements are getting squeezed. "General expense" is where clarity goes to die.

If a category doesn't help you make a decision, rename it or remove it.

For example, a construction company might separate:

- direct materials

- subcontractors

- equipment rental

- permits

- office overhead

A therapy practice might separate:

- clinician payroll

- admin payroll

- rent

- billing costs

- software

- supplies

- continuing education

- owner distributions

Match the budget to real operations

Bookkeeping and budgeting need to interact. If your books lump five different spending patterns into one account, your budget won't tell you much.

One option is to work with a bookkeeping and advisory partner like MyOfficeOps, which handles bookkeeping, payroll integration, financial analytics, and budgeting support for small and midsize businesses. Another option is to clean up your own chart of accounts inside QuickBooks Online or a similar system and rebuild the categories yourself. Either way, the goal is the same. Make the numbers easy to read and useful in a meeting.

If you're learning how to create a budget for the first time, don't aim for perfect detail. Aim for categories that show where money comes from, where it goes, and which parts of the business deserve attention first.

Set Realistic Targets and Assumptions

Now you stop looking backward and start making bets about the future.

Many budgets go off track. Owners use hope as a forecast. They plug in the sales number they want, add a few expense lines, and call it a plan. Then the year starts, reality shows up, and the budget gets ignored.

Build targets from evidence

Start with what your business has done. Then adjust for known changes.

That could include:

- one provider leaving or joining the practice

- a major contract starting or ending

- a rate increase already communicated to clients

- a new truck lease

- a rent increase

- planned hiring

- software changes

- debt payoff that will reduce monthly pressure

If you need help shaping those assumptions into a usable model, this resource on how to forecast revenue gives a practical way to build revenue expectations from actual activity instead of wishful thinking.

Use three views, not one

For a busy owner, the easiest forecasting method is to run three versions.

Base case

This is the most likely outcome if things stay fairly normal. No miracle months. No disaster month either.

Use recent trends, booked work, current staffing, and realistic collection timing.

Strong case

This reflects what happens if hiring goes smoothly, collections come in on time, and sales activity lands where you expect.

This version helps you decide what you'd do with extra capacity or stronger cash. Pay down debt. Add staff. Rebuild reserves. Replace equipment.

Lean case

This one matters more than most owners want to admit.

Many guides assume stable income, but businesses with volatile revenue need a more defensive plan. One practical approach is ruthless prioritization with contingency funds for lean months, sometimes shifting the split to something like 95% for needs, 0% for wants, and 5% for savings during stressful periods (bare-bones budget guidance).

That doesn't mean your business should always operate that way. It means you should know what gets cut first if revenue drops, jobs get delayed, or reimbursements slow down.

Plan for irregular income

Construction and healthcare both deal with timing problems, just in different ways.

A contractor may have seasonal work, retainage, delayed draws, or change orders that take time to bill. A healthcare practice may deal with payer delays, credentialing timing, or uneven appointment volume around holidays and vacations.

So don't build the budget as if every month is identical.

Use a few practical rules:

- Budget from post-tax reality when possible. Work from what the business has available after known obligations.

- Tie revenue to timing. If invoices usually get paid later, don't pretend cash arrives the same week the work is done.

- Separate committed costs from flexible ones. Payroll and rent are different from optional software or marketing tests.

- Create a contingency line. If nothing goes wrong, good. If something does, you already planned for it.

A realistic budget should feel a little boring. That's usually a good sign.

Avoid fantasy assumptions

Be careful with these common mistakes:

- Assuming every proposal will close

- Counting one-time revenue as recurring

- Ignoring the cost of a new hire beyond wages

- Forgetting payroll tax, benefits, training time, and equipment

- Treating owner draws like an afterthought

- Planning equipment purchases without considering timing

A budget should support decisions, not flatter the owner. If the assumptions are honest, the budget becomes useful fast.

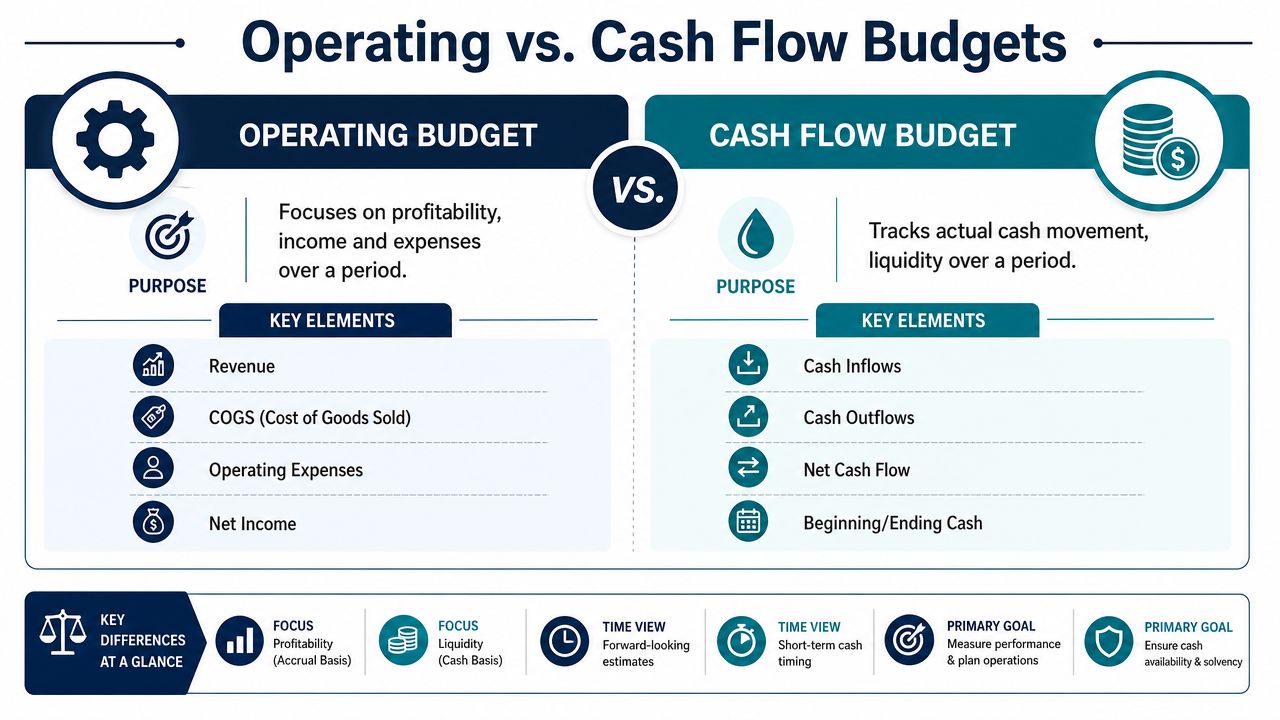

Build Your Operating and Cash Flow Budgets

At this point, you need two different budgets. Not one.

Owners often build an operating budget and think they're done. Then they run into a cash crunch and wonder why the plan failed. The problem is that profit and cash are related, but they are not the same thing.

The operating budget shows whether the business works

Think of the operating budget as the scorecard for profitability.

It includes expected revenue and expected expenses over a period. That usually means labor, occupancy, software, supplies, subcontractors, admin costs, and debt-related operating items that hit the P&L.

This budget answers questions like:

- Are we pricing work correctly?

- Can gross margin support another hire?

- Is overhead too heavy?

- Will this service line make money?

- Are we likely to end the period with profit?

For a contractor, the operating budget helps test whether jobs are priced with enough room for labor burden, materials, and overhead. For a medical office, it helps show whether collections can support provider compensation, staff payroll, and facility costs.

The cash flow budget shows whether the business can breathe

Now look at cash.

A cash flow budget tracks when money comes in and goes out. It includes receipts, payroll timing, loan payments, tax payments, owner draws, deposits, and large purchases that may not hit the P&L the same way.

This is the budget that keeps you from getting blindsided.

A profitable month can still be a dangerous month if cash arrives late.

Here's a simple example. A contractor bills a good month of work. On paper, the month looks solid. But payroll was weekly, materials had to be paid upfront, and the customer won't pay for another few weeks. The operating budget says the job made money. The cash flow budget says the company may need a tighter spending plan right now.

Build them side by side

The easiest way to do this is in a monthly layout.

For each month, list:

- expected revenue

- direct costs

- operating expenses

- expected profit

Then build a second view:

- beginning cash

- cash received

- cash paid out

- ending cash

That second view is where timing lives. Timing is what gets owners in trouble.

If you're introducing a new service, market, or pricing model, line those assumptions up with your broader growth plan too. A strategy framework can prove helpful. A resource like Stamina's GTM strategy playbook can help you pressure-test whether your revenue assumptions match how you expect to win business.

Use a template, then adjust for reality

Most businesses don't need a fancy system to start. A clean spreadsheet works if it's updated and reviewed.

Use columns for months. Keep payroll separate from contract labor. Break out debt payments. Flag one-time spending. Show beginning and ending cash. Build notes for known timing issues like annual insurance payments, equipment deposits, or tax deadlines.

If you want a structure you can adapt, this cash flow forecasting template gives a solid starting point for turning your budget into something you can review monthly.

Don't mix long-term plans with monthly survival

A lot of owners bury important decisions in the wrong budget.

A truck purchase, new X-ray machine, major software conversion, or office expansion shouldn't just appear as a casual line item. Those decisions affect debt, cash reserves, staffing, and future operating costs. Put them in the budget on purpose, with timing attached.

That's how to create a budget that supports real management. Not just reporting after the fact.

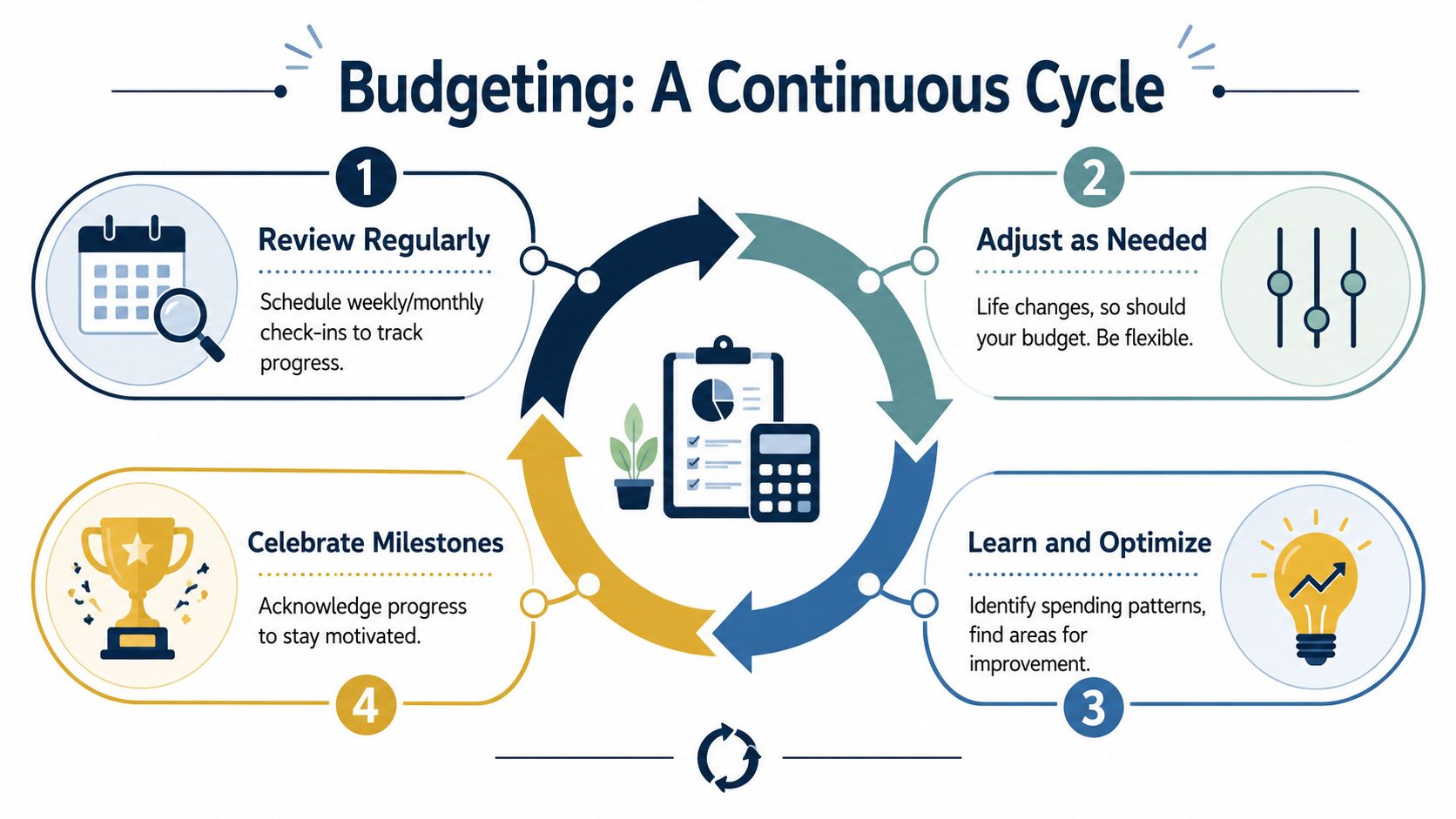

Make Your Budget a Living Document

A budget that sits untouched is just an old guess.

Value comes from review. Compare the plan to actual results every month or each quarter, keep records, and adjust as needed. That kind of repeated check is central to budgeting discipline, and a 2023 budgeting survey found that 84% of people with a monthly budget still say they exceed it (NerdWallet budgeting report). The lesson is simple. The review process matters as much as the plan.

Review the gaps without panic

When actual results differ from the budget, don't treat that as failure. Treat it as information.

Ask:

- Did revenue come in slower than expected?

- Did payroll rise because you added capacity?

- Did supply costs increase because work volume increased?

- Did a one-time repair hit the month?

- Did collections slip?

Some variances are bad. Some are a sign the business is growing. You need to know the difference.

Review isn't about scolding the business. It's about learning what changed and deciding what to do next.

Put the review on the calendar

Busy owners won't do this by accident. Set a recurring review meeting.

A good monthly or quarterly check-in usually includes:

- budget versus actual revenue

- major expense variances

- cash position

- receivables and payables

- upcoming hiring or equipment decisions

- whether reserves are improving or shrinking

Keep it short and useful. If the meeting turns into an accounting lecture, people stop showing up mentally.

A living budget helps you answer hard questions faster. Can we hire? Can we raise pay? Can we replace equipment? Can we afford another location? Can the owner take a larger draw? You don't need perfect certainty. You need a current plan, clean books, and a habit of review.

If you want help turning messy books and scattered reports into a budget you can use, MyOfficeOps works with business owners around West Chester and Greater Philadelphia on bookkeeping, reporting, cash flow planning, and advisory support. The goal is simple. Give you clear numbers you can use for hiring, pricing, equipment decisions, and day-to-day cash management.