If your bookkeeping lives in your inbox, a pile of receipts, and the notes app on your phone, you're not alone. A lot of owners run the business first and deal with the numbers later. Then tax time shows up, cash feels tight, and suddenly you're trying to remember why the card was charged at the supply house three months ago.

That's the problem. Not just “keeping records,” but trying to make decisions with messy information. You can't price jobs well, hire with confidence, or spot a cash problem early if your books are half memory and half guesswork.

A good bookkeeping format for small business should make your life simpler, not harder. It should tell you where money came from, where it went, what you owe, what customers owe you, and whether the work you're doing is worth it. If it doesn't do that, it's the wrong format.

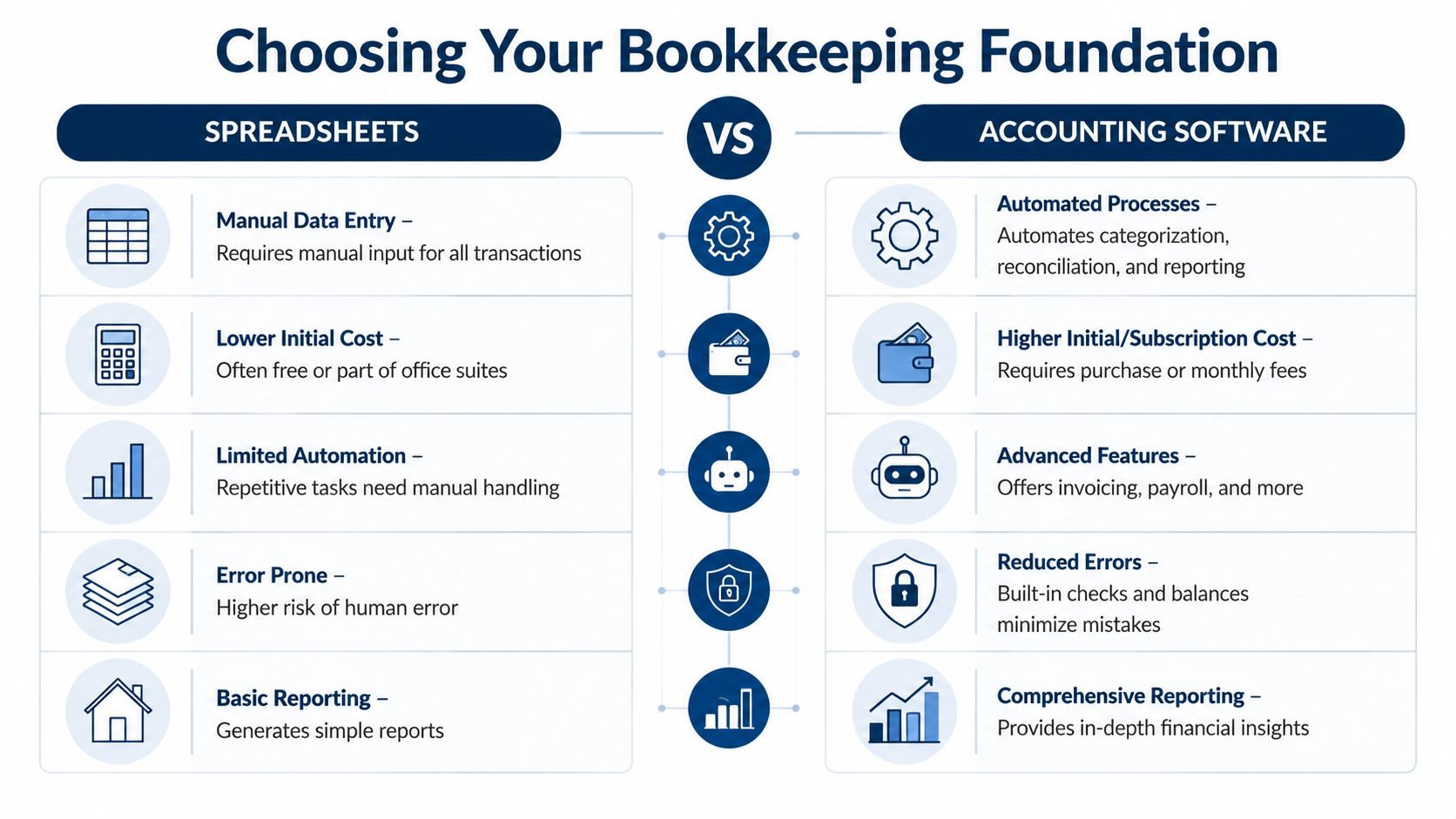

Choosing Your Bookkeeping Foundation

Before you worry about categories, reports, or tax prep, decide where your numbers will live. For most owners, choices are simple: spreadsheet, accounting software, or a bookkeeping partner.

The mistake I see all the time is choosing based on price alone. That's backwards. Choose based on what you need your books to tell you. Good bookkeeping isn't just for compliance. It affects cash flow visibility, profitability analysis, and whether you're ready for financing or tax filing, which is a gap many generic guides miss, as noted in this practical bookkeeping decision framework.

When a spreadsheet is enough

A spreadsheet is fine when your business is still simple. Think solo consultant, new freelancer, or a service business with low transaction volume, one bank account, and no payroll.

It works because it forces you to pay attention. You type in every sale, every expense, and every payment yourself. That can be useful early on. You learn the shape of your business fast.

But spreadsheets break down once real-world mess enters the picture.

| Format | Good fit | Where it starts to fail |

|---|---|---|

| Spreadsheet | Very simple business, low volume, no inventory, no payroll | Easy to miss entries, duplicate work, weak reporting |

| Accounting software | Growing business that invoices regularly or needs cleaner reports | Still needs review and cleanup |

| Bookkeeping partner | Owner wants accurate books without doing the work personally | Requires handoff and communication |

When software stops being optional

If you're sending regular invoices, collecting deposits, paying contractors, running payroll, or using business credit cards, move to software. Don't wait until the books are already a mess.

Software helps because it keeps your chart of accounts, bank activity, invoices, and reports in one place. It also gives you a cleaner trail when you need to answer basic questions like:

- Who still owes me money

- Which jobs or clients are profitable

- What did I spend last month

- Why cash is lower than expected

Even then, software is not autopilot. Bank feeds save time, but they don't think. If a charge gets coded to the wrong category, your reports still come out wrong. If you're comparing platforms, this bookkeeping software for small businesses resource is useful because it focuses on bookkeeping tasks like invoice tracking, payment matching, and bank activity.

Practical rule: If you need answers from your books more than once a month, a spreadsheet is usually too small for the job.

When to bring in a partner

There's a point where the issue isn't the tool. It's time.

If you're spending evenings fixing transactions, chasing receipts, and trying to remember what happened in the business, you're doing admin work instead of owner work. That's usually the point to bring in a professional.

This hits trades especially hard. Contractors have deposits, draws, job materials, vendor bills, equipment, and subcontractors all moving at once. If you're in that world, this Growth 4 Trades accounting guide gives a solid look at software considerations for contractor workflows.

My opinion is simple. Use a spreadsheet only while the business is still plain vanilla. Move to software as soon as the business has moving parts. Bring in a partner when you're making decisions on bad or delayed numbers, or when the books keep stealing your time.

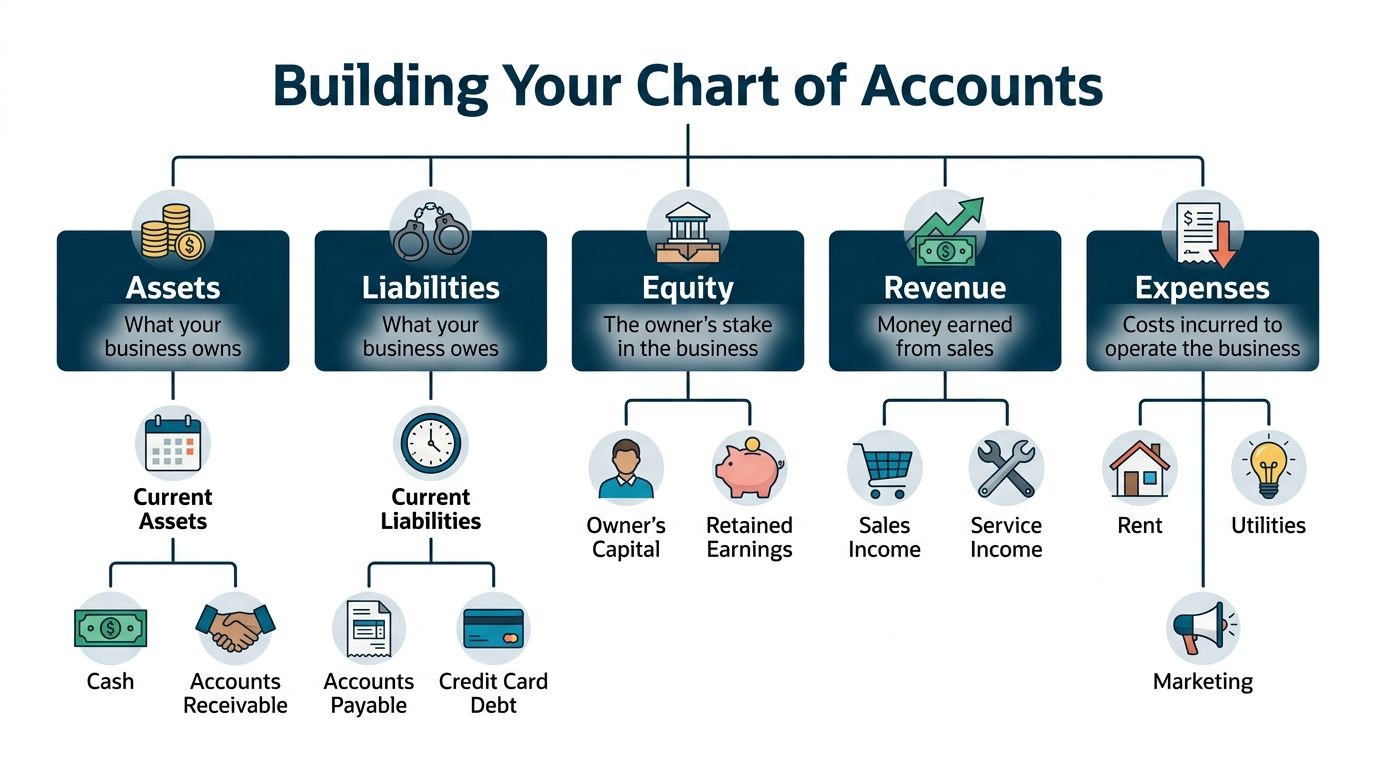

Building a Chart of Accounts That Tells a Story

“Chart of accounts” sounds bigger than it is. It's just a filing cabinet for your money. Every dollar that enters or leaves the business needs the right folder.

When the folders are set up well, your books tell a clear story. When they're sloppy, all you get is noise.

A solid bookkeeping format for small business usually sits on the double-entry system, where every transaction is recorded twice, once as a debit and once as a credit, so the books stay balanced. That structure supports the chart of accounts, general ledger, and core reports, as explained in this small business bookkeeping overview.

Start with the five big buckets

You don't need a giant list on day one. You need the right structure.

- Assets are what the business owns. Cash, accounts receivable, equipment.

- Liabilities are what the business owes. Credit cards, loans, bills.

- Equity is the owner's stake.

- Revenue is money earned.

- Expenses are the costs of running the business.

That's it. Most bookkeeping confusion starts when owners skip this basic setup and create random categories that don't help them later.

A simple starter template

Here's a clean starting point most small businesses can use:

| Main category | Starter accounts |

|---|---|

| Assets | Checking, savings, accounts receivable, prepaid expenses, equipment |

| Liabilities | Accounts payable, credit card payable, loan payable, payroll liabilities |

| Equity | Owner contributions, owner draws, retained earnings |

| Revenue | Service income, product sales, other income |

| Expenses | Rent, payroll, software, advertising, insurance, office supplies, meals, travel |

That's your base. Then you shape it to match how the business runs.

Build it around your decisions

The right categories should answer the questions you ask all the time.

If you run a service business, break revenue into meaningful lines. Consulting income. Retainer income. Project income. That helps you see which type of work is carrying the business.

If you run a healthcare practice, generic categories won't help much. You'll want accounts like patient co-pays, insurance reimbursements, medical supplies, lab fees, and provider payroll. That gives you a truer picture of collections and operating costs.

If you're in construction, you need more detail where the money leaks. Job materials, subcontractor costs, permits, equipment rental, fuel, and possibly revenue by project type. If all of that sits inside one big “job costs” bucket, you can't tell what's going wrong.

If you work in real estate, separate commission income, referral income, MLS fees, staging, marketing, and client-related expenses. Agents often think they know where the money goes. Then the books show how much gets eaten by deal support and lead generation.

Your chart of accounts should match the way you run the business, not the way a generic template labels it.

If you want a plain-English walkthrough of how these categories work, this guide to what a chart of accounts is is worth a look.

One warning. Don't overbuild it. A chart of accounts should be detailed enough to help you decide, but not so detailed that nobody uses it correctly. If your team can't tell the difference between two categories, merge them.

Your Rhythm for Recording and Reconciling

Good books come from rhythm, not heroics. If you wait until the end of the quarter and try to “catch up,” you'll forget details, miss receipts, and code things badly.

A better system looks boring. That's why it works.

What a normal week should look like

Say you run a small contracting company. On Tuesday, you buy materials at the supply house. That receipt should be captured right away, not left in the truck. On Thursday, you send an invoice for a progress payment. By Friday, you review the week's bank and card activity and code each item to the right account.

If you run a consulting firm, the rhythm is different but the idea is the same. Send invoices weekly. Record incoming payments weekly. Categorize software subscriptions, travel, meals, and contractor payments while they're still fresh in your mind.

The goal isn't perfection every day. The goal is staying close to real time.

The weekly and monthly cadence

A practical bookkeeping format for small business uses a monthly close workflow built around a customized chart of accounts, transaction coding, bank and credit-card reconciliation, and scheduled report review. Expert guidance recommends recording revenue weekly and reconciling monthly so errors are caught before they compound, which is laid out clearly in this monthly bookkeeping workflow guide.

Here's the rhythm I recommend:

Daily habit

Snap a photo of every receipt. Save bills when they arrive. Don't trust your memory.Weekly money check

Send invoices, record payments, review uncategorized transactions, and follow up on overdue customer balances.Monthly close

Reconcile bank accounts and credit cards, review loans and payroll-related items, then look at the month-end reports.

Reconciliation is just matching your book to your bank so you can catch missing entries, duplicates, and bad coding before they spread.

What reconciliation really does

Owners often hear “reconcile” and think it's accountant language. It isn't. It's a simple comparison.

Your books say the checking account has one balance. The bank says it has another. Reconciliation is the process of lining those up and explaining every difference. Maybe a payment was recorded twice. Maybe a bank fee never got entered. Maybe a customer payment landed in the bank but wasn't attached to the invoice.

That's why monthly reconciliation matters. It's quality control.

For healthcare, that might mean matching deposits to patient payments and insurer payments. For construction, it might mean making sure card purchases hit the right job cost bucket. For real estate, it might mean checking that every commission deposit and marketing expense landed in the right place.

If you stay current weekly, monthly close is manageable. If you ignore the books for months, monthly close turns into detective work.

Making Sense of the Numbers Your Business Generates

Once the bookkeeping is clean, the reports stop feeling like homework. They start acting like a dashboard.

A lot of owners never got comfortable with financial reports. That's normal. In fact, 42% of small business owners surveyed said they had limited or no financial literacy before starting their businesses, according to this small business bookkeeping article from Coursera. That's exactly why your bookkeeping format for small business needs to produce reports you can use.

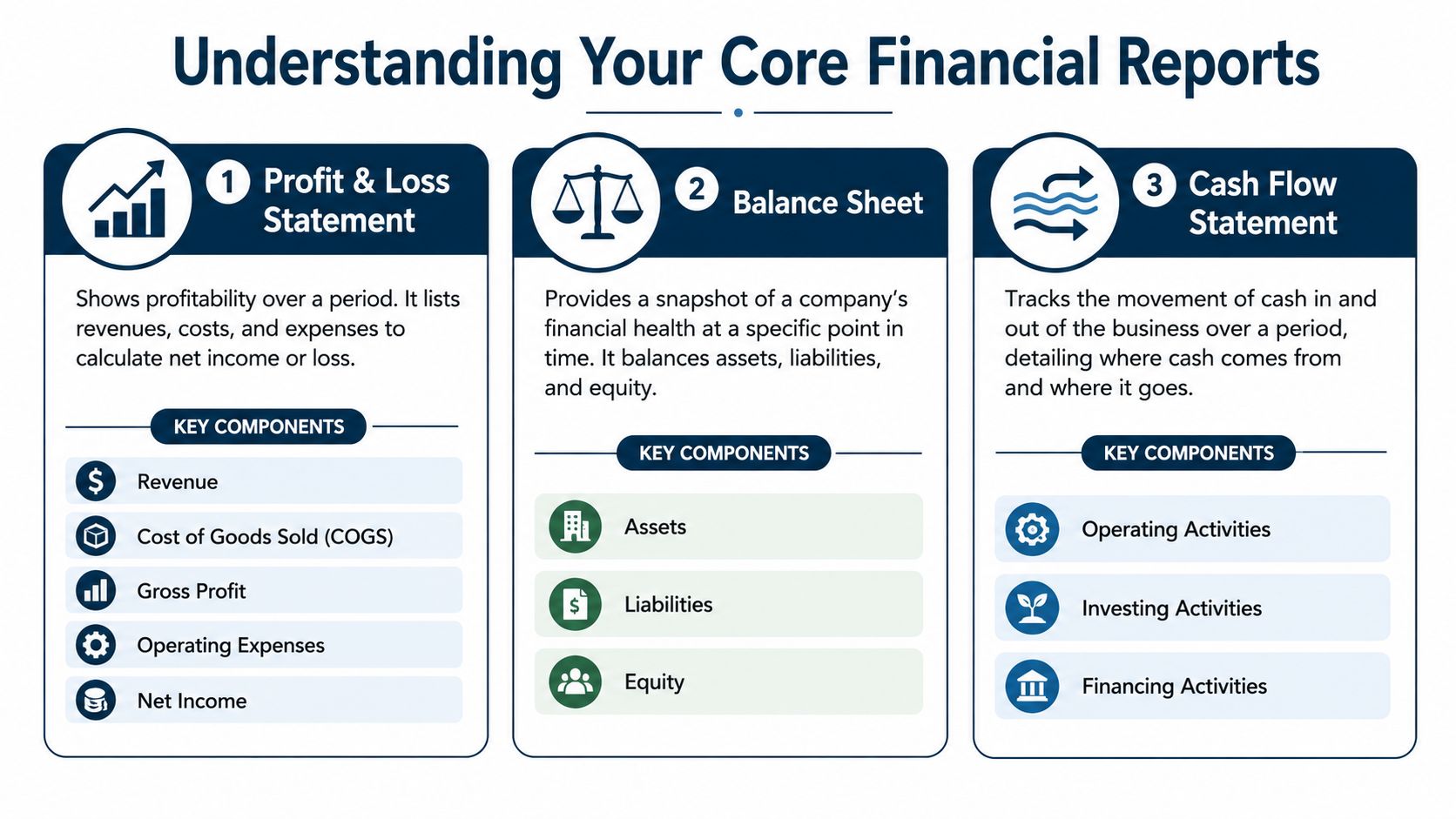

The three reports that matter most

Each report answers a different question.

| Report | What it tells you |

|---|---|

| Profit and Loss statement | Did the business make money over a period? |

| Balance Sheet | What does the business own, owe, and retain right now? |

| Cash Flow statement | Where did cash come from, and where did it go? |

Start there. Don't try to become an accountant overnight.

How to read them like an owner

The Profit and Loss statement tells you if the month was worth the effort. Revenue comes in at the top. Expenses sit below. What's left is profit or loss. For a marketing agency or IT firm, I like to break this down further by service line or client group if the system allows it. That's how you spot the work that looks busy but pays poorly.

The Balance Sheet is a snapshot. It shows cash, receivables, debt, credit card balances, and owner equity. If profit looks fine but receivables are bloated or card debt keeps climbing, the business may not be as healthy as the P&L suggests.

The Cash Flow statement is the reality check. A contractor can show profit on paper and still feel squeezed because cash is tied up in labor, materials, or slow-paying customers. A real estate team can have a strong month in commissions and still see uneven cash timing because closings bunch together.

Industry-specific questions to ask

Use the same reports differently depending on your business:

Professional services

Which clients produce the strongest margin? Are payroll and contractor costs lined up with revenue?Healthcare

Are collections keeping pace with provider and staffing costs? Are supply expenses creeping up?Construction

Is each job producing cash, or just revenue? Are subcontractor and materials costs eating the margin?Real estate

Are commission splits, marketing spend, and deal-related costs leaving enough profit per closing?

If you still get bank statements as PDFs and need cleaner raw data before review, a tool that can streamline bank statement data entry can save time on cleanup work.

Don't stare at reports asking, “What do these numbers mean?” Ask, “What decision do I need to make, and which report answers it?”

For a plain-English breakdown, this guide on how to read financial reports is a good next step.

Common Bookkeeping Mistakes That Cost Real Money

Small mistakes don't stay small. They turn into missed deductions, late invoices, bad pricing, and ugly surprises when cash gets tight.

The expensive part isn't the bookkeeping error itself. It's the decision you make because the books were wrong.

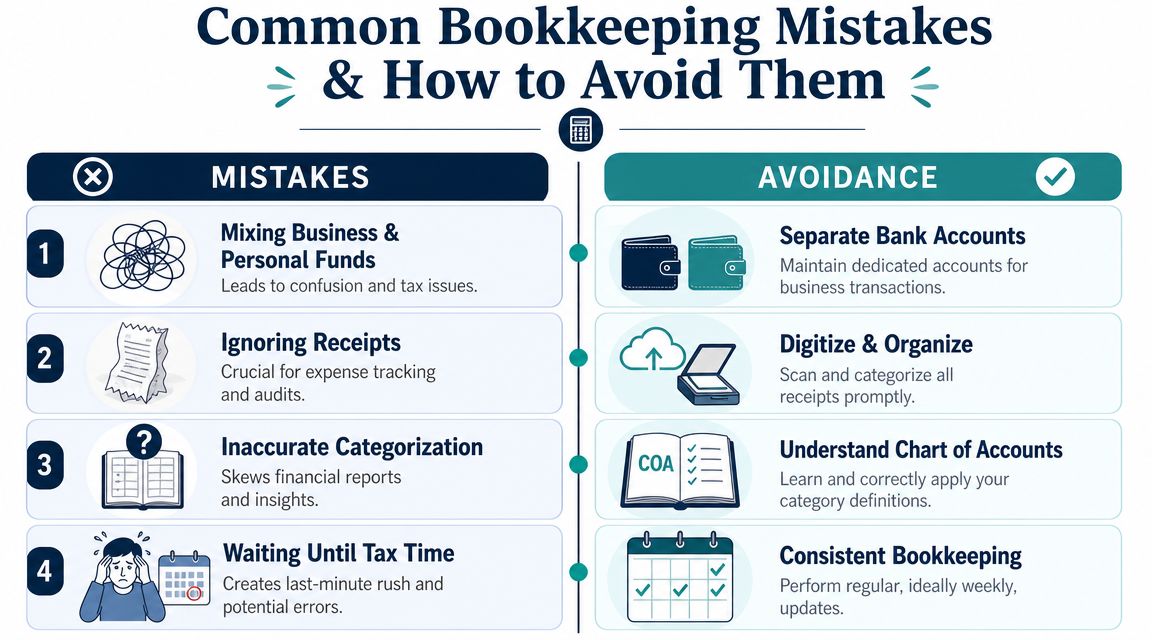

The mistakes I see most often

Mixing business and personal spending

This creates confusion fast. A meal, a gas purchase, a software charge, and now nobody knows what belongs to the company. Open separate accounts and keep them separate.Ignoring receipts and backup documents

If you can't support an expense, it becomes harder to trust the number. Digitize receipts right away and store them where your bookkeeper can find them.Coding expenses to random categories

If everything lands in “miscellaneous,” the reports become useless. Use your chart of accounts the same way every time.Waiting until tax time

Owners often find themselves in a painful situation. Catch-up bookkeeping is slower, sloppier, and more expensive than staying current.

The quiet leak nobody talks about enough

Owners also forget to bill small costs back to customers. That happens on projects all the time. Materials, permit fees, rush shipping, disposal fees, mileage. One missed item doesn't hurt much. A year of missed items does.

Then there's accounts receivable. If you don't stay on top of unpaid invoices, you're financing your customer's business with your cash. That's a terrible deal.

Clean books don't just help with taxes. They protect margin.

The fix is simple, even if it takes discipline:

- Separate accounts for business use only.

- Weekly review of new transactions and unpaid invoices.

- Monthly reconciliation so the reports are based on facts, not guesses.

- Clear ownership of the process, whether that's you, your office manager, or an outside partner.

If you're tired of carrying this yourself, MyOfficeOps works with small and midsize businesses that need bookkeeping, payroll integration, reporting, and advisory support without building a full in-house finance team.

If your books are late, messy, or too basic for the business you're running now, it's time to fix the format. MyOfficeOps helps owners clean up the records, build a bookkeeping system that fits their business model, and turn the numbers into something useful for pricing, cash flow, and growth decisions.