You bought the rental. The lease is signed. Rent should hit your account soon. For a minute, it feels simple.

Then the paper starts to pile up.

A locksmith invoice lands in your email. The plumber texts a receipt photo. You paid for smoke detectors on your personal card because it was faster. The tenant sent the security deposit and first month's rent in one payment. Now you're staring at a spreadsheet called “rental stuff” and asking the question most new owners ask a little later than they should.

Is this property making money?

That's where accounting for real estate investors stops being a tax chore and starts becoming a decision tool. If you can't clearly track rent, repairs, deposits, loan interest, and bigger upgrades, you don't really know what you own. You just know money is moving.

Your First Property Is Just the Beginning

A first rental usually starts with optimism and ends its first month with confusion.

One owner might collect rent on time, pay for a small leak repair, cover a lawn bill, and replace a broken garbage disposal. On paper, it feels like progress. In practice, those transactions often get spread across a personal checking account, a credit card, a few email threads, and maybe a note on a phone. By tax time, nothing is clean.

The biggest problem isn't bookkeeping itself. It's the false sense that you can “sort it out later.” Later is when receipts are missing, categories are fuzzy, and nobody remembers whether that hardware store charge was for a tenant turnover or your own house.

Good real estate accounting answers basic questions fast. What came in, what went out, what belongs to this property, and what doesn't.

A rental property is a business unit. Even if you own one duplex and still work a full-time job, you need records that show the property's own story. That means you should be able to look at one address and know whether rent covered the actual cost of holding it.

Some owners learn this when they try to refinance. Others learn it when a CPA asks for support behind deductions. A few learn it when a “profitable” property turns out to be draining cash because large expenses were never tracked properly.

What new investors usually miss

- Profit isn't the same as cash in your bank account. Rent may come in, but that doesn't mean the asset is performing well.

- Small messes get expensive. One mixed account turns into miscategorized expenses, weak reports, and tax cleanup.

- Every property needs its own trail. If you can't trace an expense back to a specific property, you're already behind.

Think of your records like the property's medical chart. If they're incomplete, you can't diagnose problems early. You also can't make smart calls on rent increases, repairs, refinancing, or whether to keep the asset at all.

That's why the first property matters so much. It's where your habits get built. Clean habits scale. Sloppy ones follow you into every new deal.

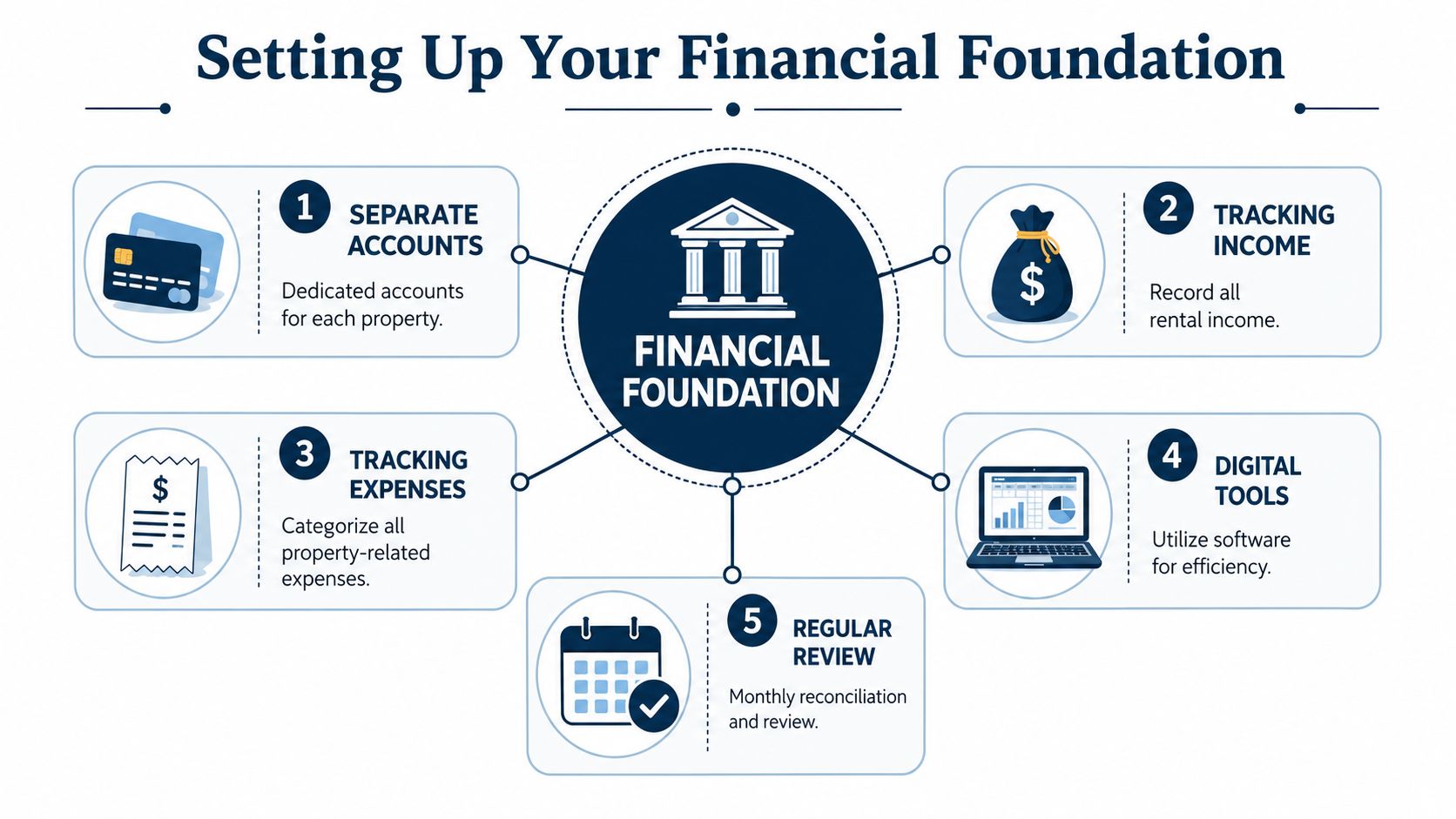

Setting Up Your Financial Foundation

The setup is where most accounting problems start, or get prevented.

If you do one thing right early, do this. Give each property or legal entity its own bank account. The cleanest version is one account per property. At minimum, use separate accounts for each LLC or legal entity. When money for one property shares space with another property or your personal spending, the records stop being trustworthy.

According to Devine Consulting's real estate accounting guide, each property needs separate income and expense accounts within the chart of accounts, such as rental income and mortgage interest, so you can track individual performance, avoid mixed personal and business spending, and improve cash flow visibility and KPI reporting.

Think of your chart of accounts like a filing cabinet

“Chart of accounts” sounds bigger than it is. It's just your list of labeled folders.

You need folders for the money coming in, the money going out, and the balance sheet items that shouldn't be treated like normal expenses. If you've ever used manila folders for taxes, it's the same idea in digital form.

A simple starter setup might look like this:

| Account type | Example |

|---|---|

| Income | Rental Income, Late Fees |

| Operating expenses | Repairs, Insurance, Property Taxes, Mortgage Interest |

| Admin | Bank Fees, Software, Professional Fees |

| Balance sheet | Security Deposits Held, Loan Balance |

| Asset tracking | Capital Improvements |

The property label matters just as much as the category. “Repairs” by itself isn't enough if you own more than one unit. “Repairs, 123 Maple Street” tells you something useful.

The setup that works in real life

Most investors don't need a fancy system on day one. They need a consistent one.

- Open dedicated accounts: One account structure per property or entity keeps the money trail clear.

- Name accounts clearly: Don't use vague labels like “miscellaneous housing.”

- Store documents right away: Save leases, invoices, tax notices, and loan statements in cloud folders the same day you receive them.

- Reconcile monthly: Compare the bank activity to your records every month, not at year-end.

If you're still learning how to judge deal quality from the numbers, a good rental property financial analysis guide can help you connect your bookkeeping setup to actual investment decisions.

Practical rule: If a stranger couldn't look at your records and tell which property earned or spent the money, the foundation isn't set up well enough.

That sounds strict, but it saves people over and over. Good accounting for real estate investors starts before tax season. It starts with how the first dollar gets deposited.

How to Track Your Day to Day Activity

Once the foundation is clean, daily tracking gets much easier. Every transaction usually fits into one of three buckets. Income, operating expenses, or capital expenditures. If you get those right, your books start making sense.

Income you should record right away

Rent is the obvious one, but it's rarely the only one.

A rental can also bring in late fees, pet fees, application fees, or other tenant charges. Record each item clearly, and tie it to the property and tenant when possible. That makes it easier to sort out disputes and easier to explain your records later.

If you're choosing tools, this roundup of the best real estate accounting software is useful for comparing platforms built for rent collection, categorization, and reporting. If you want a second list with a bookkeeping angle, this guide to accounting software for real estate investors can help narrow down what fits a smaller portfolio.

Operating expenses that keep the property running

These are the regular costs of owning and operating the rental.

Examples include mortgage interest, insurance, utilities you pay, property management fees, lawn care, small maintenance items, and ordinary repairs. A leaking faucet fix belongs here. A service call to reset a tripped system likely belongs here too.

The mistake I see often is overusing one category called “maintenance.” That hides patterns. If the HVAC keeps needing service, or turnover costs are rising, you want that to show up.

Capital expenditures need their own log

Many new owners often encounter difficulties at this stage.

According to A.COBLOOM's accounting best practices for investors, effective accounting requires dedicated bank accounts for each property, separate handling of security deposits from operating cash, and a dedicated capital expenditure log for major improvements like roofs or HVAC systems because those items matter for depreciation and resale planning.

A quick example helps. If a water heater gets one small part replaced and keeps working, that's usually a repair. If the entire unit is replaced with a new one, that's usually a capital improvement. One keeps the property going. The other creates or extends value over time.

Track capital items with details like:

- What was done: “Replaced full water heater” is better than “plumbing.”

- When it was placed in service: That date matters later.

- Which property it belongs to: Never leave this open to guesswork.

- Supporting documents: Invoice, contractor receipt, and payment proof.

Security deposits are not operating cash

This is one of the easiest ways to create a legal and accounting problem.

Security deposits don't belong in the same pool as rent you can spend. In many states, they need to sit in a dedicated trust account. Even where the rule feels routine, sloppy handling creates tenant issues fast.

Keep tenant deposits in their own lane. If you treat deposit money like normal rent, your books stop matching reality.

A landlord can feel cash-rich for a moment by mixing deposits into operating funds. Then move-out happens, deductions need support, or a refund is due, and the record falls apart. Good day-to-day tracking prevents that kind of scramble.

Understanding Real Estate Taxes and Depreciation

Taxes are where many investors either gain clarity or get overwhelmed. The good news is the basic ideas are simpler than they sound.

Start with depreciation. It's a tax concept that lets you deduct part of a property's value over time. You didn't write a fresh check for that deduction each year, so many owners call it a paper expense. That's why it can feel powerful once you understand it.

A simple way to think about depreciation

Think about a car. Over time, it wears down and loses value. Real estate works differently in the market, but for tax purposes, the IRS still allows owners to recover certain costs over a set schedule.

That doesn't mean you guess. There's a formal system behind it.

According to J.M. Co.’s overview of real estate investment accounting, real estate investors often need to understand two reporting systems, a GAAP-based accrual system for outside stakeholders and a tax-basis cash system for IRS compliance. The same source notes that tax reporting requires following MACRS depreciation conventions, including mid-month, half-year, or mid-quarter start rules, with bonus depreciation and Section 179 available for qualified assets.

If you want a plain-English companion to that topic, INTELLI's guide to depreciation does a nice job walking through the moving parts. For an even simpler accounting primer, this explanation of what depreciation means in accounting can help if the term still feels abstract.

Why cash basis and accrual both exist

Investors often get confused, and for good reason. The same business can speak two accounting languages.

Cash basis records income and expenses when money changes hands. That's often easier for smaller investors to understand because it lines up with the bank account. Accrual basis records income when earned and expenses when incurred, even if the cash moves later. Banks, partners, and outside stakeholders may care more about that view because it shows performance across periods.

You're not choosing between right and wrong. You're choosing which reporting view fits the decision in front of you.

A single rental owner may mostly live on cash-basis reports. A growing portfolio with outside investors or more formal reporting needs may also need accrual reporting. That's normal. What matters is keeping your underlying records clean enough to support both.

Why this matters beyond tax season

Depreciation isn't just a CPA topic. It affects how you evaluate upgrades, hold periods, and exit planning.

If you replace major components and never track them properly, you make depreciation harder. You also make your own portfolio harder to understand. Accounting for real estate investors gets more valuable when the records support tax planning and real decision-making at the same time.

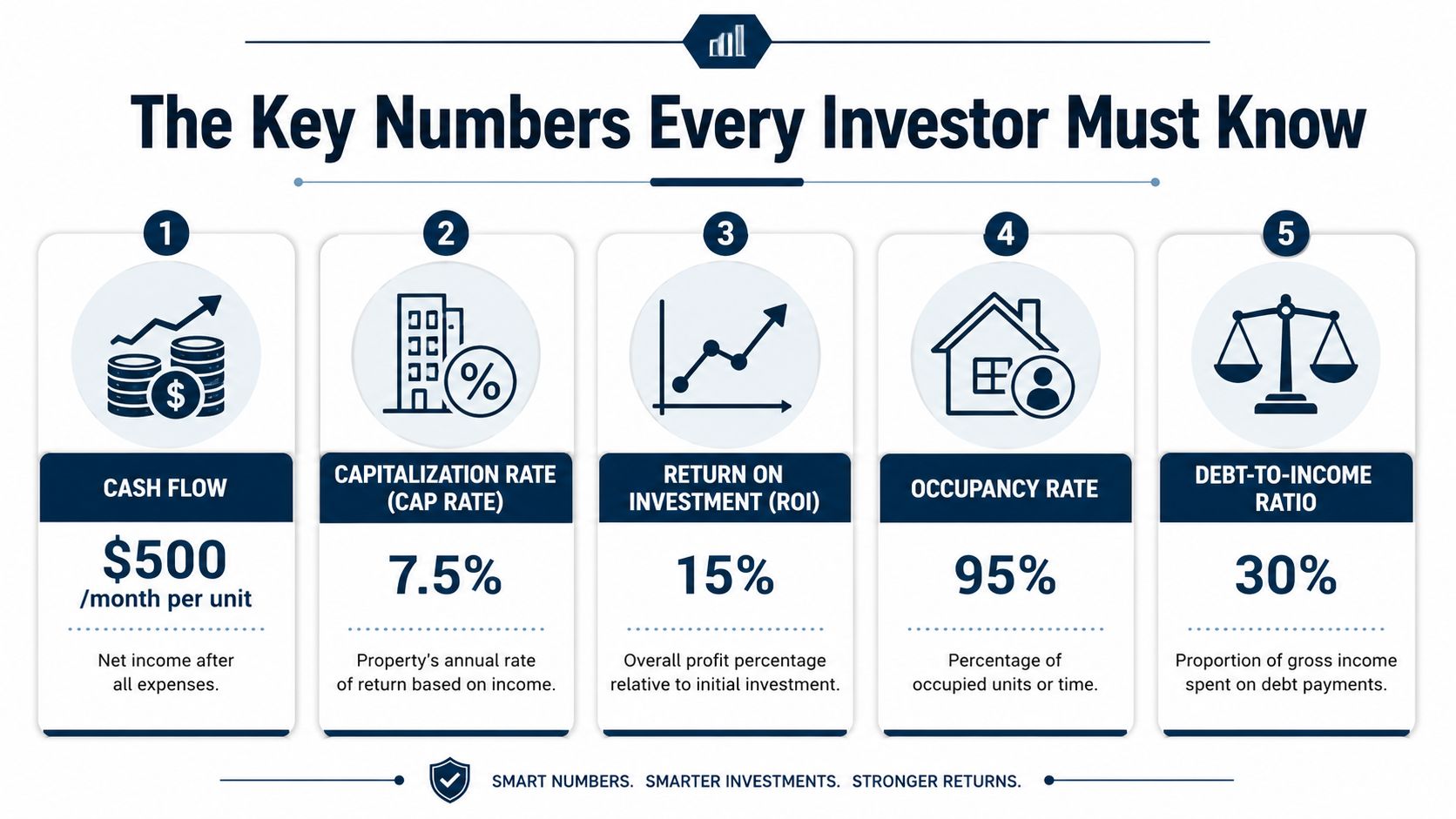

The Key Numbers Every Investor Must Know

A property can feel busy and still perform poorly. That's why serious investors look at a small set of numbers that cut through noise.

The point isn't to build a Wall Street model. The point is to answer practical questions. Is this property healthy on its own? Is my cash working hard enough? How does this deal compare with another one across town?

According to Sage's real estate accounting overview, astute investors track KPIs such as Net Operating Income, Cash-on-Cash Return, and Capitalization Rate. The same source explains that NOI is calculated by subtracting operating expenses from gross rental income, and Cap Rate is found by dividing NOI by current market value.

Start with the property's own performance

NOI is one of the clearest numbers in real estate. It tells you what the property produces before debt and certain owner-level items get involved.

If rent comes in and the building has ordinary operating costs, NOI shows the health of the asset itself. That matters because a weak property can look acceptable for a while if the owner keeps covering shortfalls out of pocket.

Here's the plain version:

| KPI | Simple formula | What it tells you |

|---|---|---|

| NOI | Gross rental income minus operating expenses | Whether the property itself is producing income |

| Cash-on-Cash Return | Annual cash flow compared with cash invested | How hard your actual invested money is working |

| Cap Rate | NOI divided by property market value | How this asset compares with other opportunities |

What these numbers sound like in plain English

NOI answers, “Is the building doing its job?”

Cash-on-cash return answers, “Was this a good use of my cash?”

Cap rate answers, “How does this deal compare with other deals if I strip out financing differences?”

Those are different questions. Investors get into trouble when they treat one metric like it answers everything.

For example, a property can show solid NOI but still create stress if the debt payments are too heavy. Another property may look less exciting on cap rate but produce better real cash flow because of financing or lower operating headaches.

Why most smaller investors like cash basis first

A lot of smaller portfolios start with cash-basis accounting because it's simple and close to everyday reality. Money came in or it didn't. A bill got paid or it didn't. That makes tax prep and day-to-day review easier for many owners.

As complexity grows, you may need accrual views for cleaner reporting over time. However, investors don't need complexity for its own sake. They need clean numbers they'll review every month.

A good monthly review is short and honest

Don't turn reporting into a ritual you avoid. Sit down and review a few items:

- Income trend: Did rent hit on time, and are there gaps?

- Expense drift: Are repairs, utilities, or management costs moving the wrong way?

- Property comparison: Which unit or address is carrying the portfolio, and which one is lagging?

- Cash position: Are you setting aside enough for the next major hit?

A KPI isn't useful because it sounds sophisticated. It's useful if it changes a decision.

That's the standard. If the number helps you price rent, budget repairs, refinance, hold, or sell, keep it on your dashboard. If it doesn't, it's just decoration.

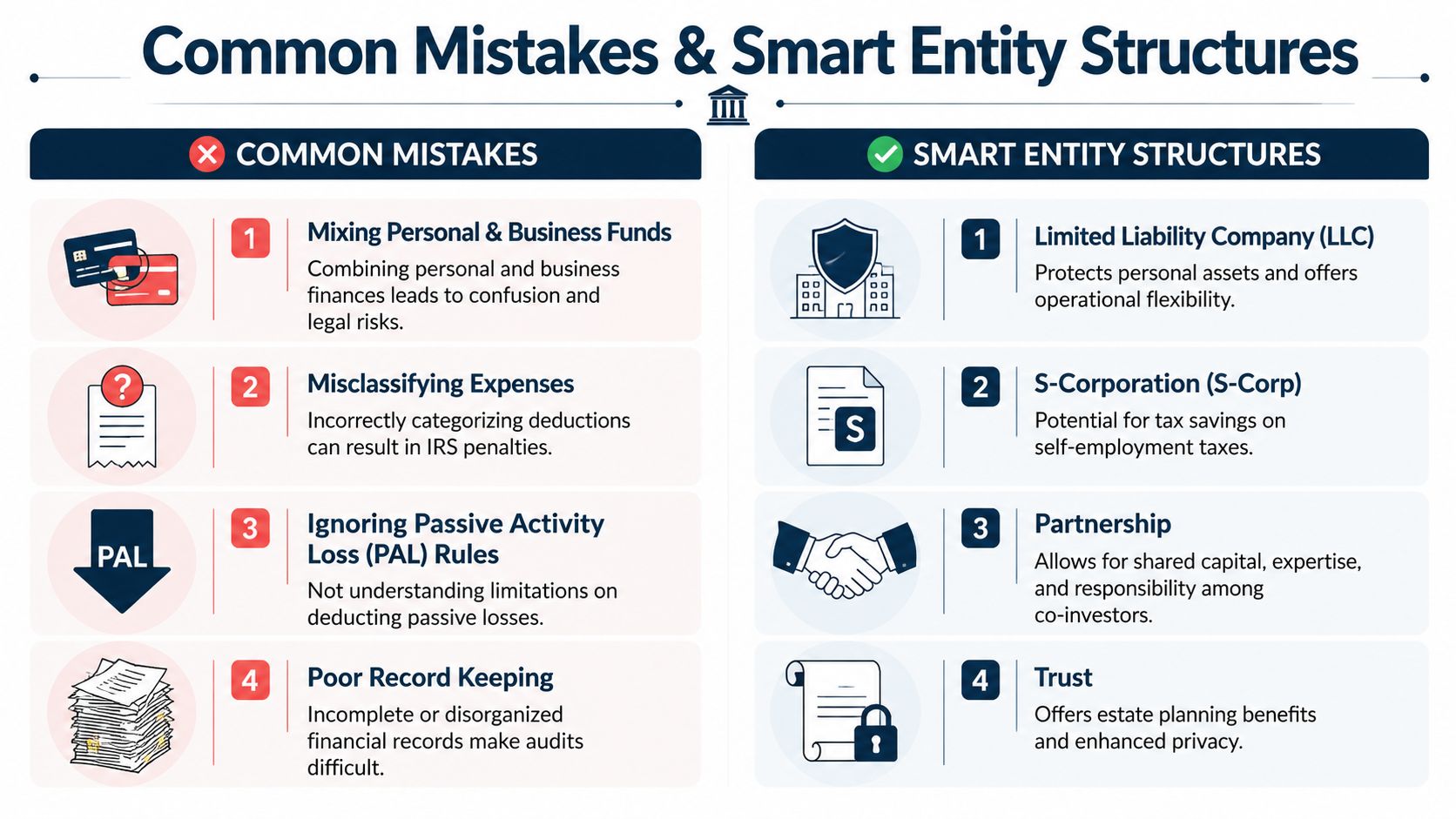

Common Mistakes and Smart Entity Structures

The expensive mistakes usually don't look dramatic at first. They look convenient.

Paying for a contractor on your personal card feels harmless. Dumping several property costs into one category feels efficient. Running losses through the wrong structure feels like something the tax preparer will “handle later.” Then the records get messy, deductions get weaker, and strategy turns reactive.

The mistakes that keep showing up

- Mixing personal and property spending: This is the fastest way to blur what belongs where.

- Calling everything a repair: That can create trouble when a cost should be tracked differently.

- Ignoring entity differences: An LLC, sole proprietorship, or other structure can change how you manage records and planning.

- Treating losses casually: Rental losses come with rules, not assumptions.

Passive activity loss rules are where many investors slip

This topic gets glossed over far too often.

According to REI Hub's accounting resource for investors, a key nuance is allocating expenses properly to maximize the $25,000 passive loss deduction under IRS Section 469, especially across mixed-entity portfolios like LLCs and sole proprietorships. The same source notes that many guides mention the strategy but don't explain the tracking needed to allocate losses correctly.

That last part matters. If you own rentals across different entities, sloppy records can distort how losses should be assigned. This isn't only a tax filing issue. It affects planning all year.

Entity structure is more than a legal form

A lot of owners choose an entity for liability reasons and stop thinking there. That's incomplete.

Your structure can affect how you track transactions, separate activity, and work with your CPA on passive losses and deductions. If you're weighing business entity options more broadly, this plain-English look at C corp vs S corp is helpful for understanding how structure choices can shape taxes and operations.

A simple example: if one property is held one way and another sits in a different entity, your accounting has to reflect that from the start. You can't patch it together cleanly after months of mixed spending.

The wrong structure doesn't always create an immediate crisis. More often, it quietly limits what you can do well later.

That's why smart investors review structure before the portfolio gets complicated, not after.

When to Call for Professional Help

A lot of investors wait too long to get help because they think hiring support means they failed at managing their own business. It doesn't. It usually means the business is growing past a simple DIY setup.

For a small portfolio, software and a disciplined process may be enough. If you have a few units, consistent rent, and straightforward expenses, you can often stay on top of it with monthly reconciliations and organized records. But there's a difference between “I can post transactions” and “I can trust the numbers enough to make big decisions.”

The point where a bookkeeper becomes worth it

Bring in a bookkeeper when the volume starts causing delays, missed categorizations, or cleanup work every month. Clean books save time, but that's not the main win. The true win is confidence.

A good bookkeeper helps you keep property-level records accurate, reconcile accounts on time, and maintain support for deposits, repairs, and larger improvements. That gives your CPA better data and gives you fewer surprises.

When a CPA or tax strategist should step in

Once you're dealing with multiple properties, mixed entities, depreciation schedules, or more complicated deductions, tax advice can't be an afterthought.

That's when a CPA or tax strategist earns their seat. They help you think ahead instead of reacting in March or April. They can also help you sort out whether your current reporting process supports the tax treatment you're expecting.

When you need CFO-level advice

There comes a stage where bookkeeping and tax prep still aren't enough.

If you're comparing refinance options, deciding whether to sell one property to fund another, planning for a partner, or trying to understand which assets deserve more capital, you're in advisory territory. That's where CFO-level help matters. The work shifts from recording history to guiding decisions.

A useful way to think about the progression is this:

| Stage | Main need |

|---|---|

| Early ownership | Clean process and monthly bookkeeping |

| Growing portfolio | Tax planning and entity coordination |

| Scaling or exit planning | Forecasting, capital decisions, and portfolio strategy |

The best investors I know don't hire help because they can't learn accounting. They hire help because they know their time is better spent finding deals, managing assets, and making better decisions with cleaner numbers.

If your books feel behind, unclear, or too reactive, MyOfficeOps can help you build a cleaner system and turn the numbers into something useful. Their team supports bookkeeping, reporting, and CFO-level advisory in plain English, so you can spend less time sorting transactions and more time making smart portfolio decisions.