Building business credit means showing your company can be trusted with money, totally separate from you. It’s like a report card for your business that banks and suppliers look at.

The whole point is to make your business look like a real, standalone company. You start with simple steps, like registering your business correctly. Then you open a business bank account and get small lines of credit from suppliers who report your payments.

A Simple Look at Building Business Credit

Think of business credit as your company's reputation. A good one gets you better loans, higher credit limits, and easier payment terms with suppliers. A bad one (or no credit at all) can really hold you back, forcing you to use your personal money and credit to grow.

A lot of business owners I talk to think this is a huge, confusing process. It's not. It's really just about creating a clean break between your finances and your business's finances. When a bank looks up your company, they want to see a professional business, not just another one of your personal accounts.

This separation is what keeps your personal stuff safe. If your business has its own good credit, you won’t have to personally promise to pay back every loan or credit card. That's a huge relief.

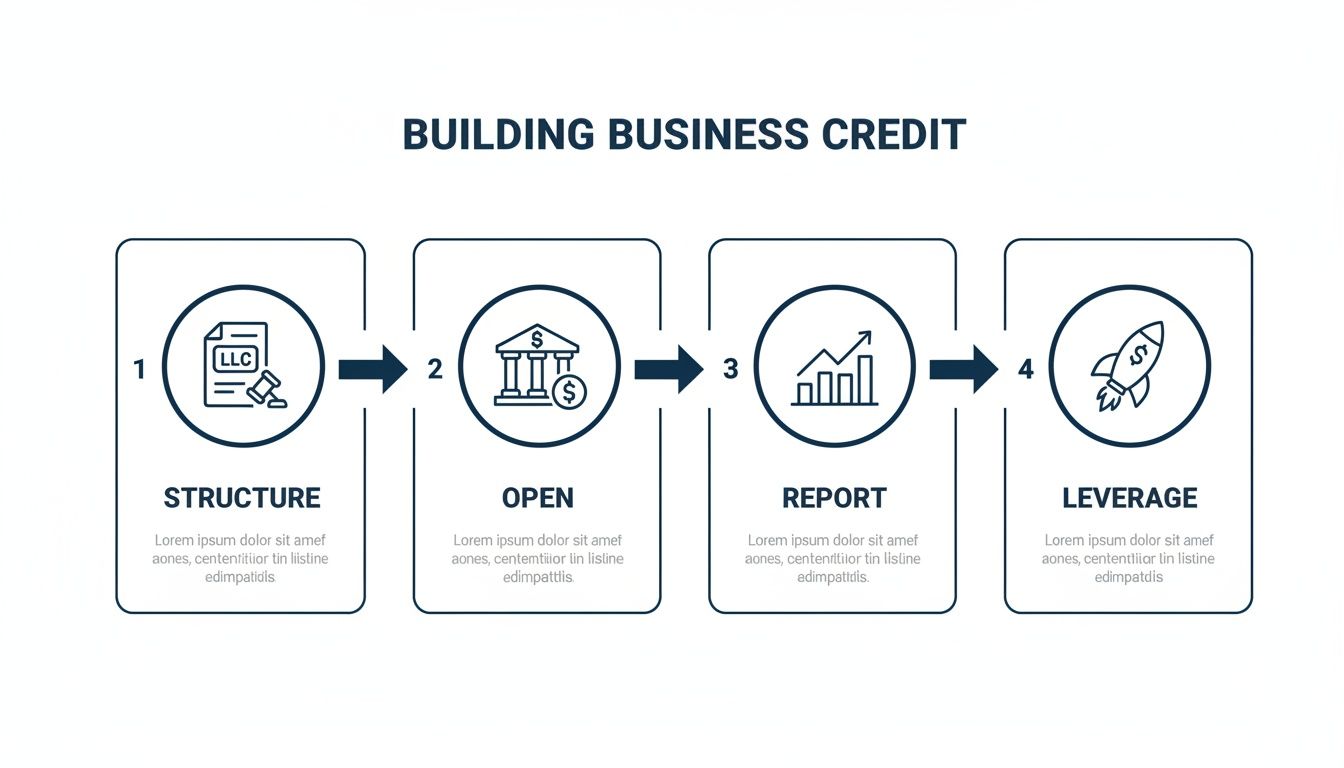

The Four Pillars of Business Credit

The whole process comes down to four main ideas. If you get these right, you’ll be on your way to building credit that helps you grow.

This picture breaks down the simple, four-step flow of building business credit from the start.

As you can see, you start by setting up your business the right way and then use its good financial standing to grow. Each step builds on the last. Now, let’s walk through exactly how to do each one.

Here’s a quick look at the main steps we’re about to cover.

Key Milestones for Building Business Credit

| Milestone | Why It Matters | Your First Action |

|---|---|---|

| Establish Your Business Identity | Lenders need to see a real, professional company. | Register your business as an LLC or corporation and get an EIN. |

| Open a Business Bank Account | This is the first step to separating business and personal money. | Take your business papers and EIN to a bank to open an account. |

| Secure Initial Vendor Credit | You need accounts that report your payment history. | Open accounts with suppliers who offer Net-30 terms and report payments. |

| Get Your Business Credit Files | This makes your business "visible" to credit bureaus. | Get a free DUNS Number from Dun & Bradstreet. |

Getting these first pieces in place is a must. They are the building blocks for everything else.

Building Your Business Foundation

Before anyone will lend your company money, they need to see it as a real, professional business. This isn’t just about having a great idea; it’s about creating an official identity that’s completely separate from you.

Think of it like building a house. You can't put up walls before you have a solid foundation. These next steps are that foundation. Banks and credit bureaus need to see clear signs that your business is legit. Without them, your business is basically invisible.

Make Your Business a Separate Legal Entity

First, you have to legally separate your business from yourself. If you’re just running things as a sole proprietor, the law sees you and your business as the same thing. This is a huge risk for you and stops you from building business credit.

Forming a Limited Liability Company (LLC) or a corporation creates that separation. It tells the world—and credit bureaus—that your business is its own legal "person." This is what protects your personal things, like your house or car, if the business gets into money trouble. For example, if someone sues your LLC, they can't come after your personal savings.

This isn't just a tip; it's the most important first step. Lenders won't give credit to a business that isn't set up formally because they can't tell where you stop and the business starts.

Setting up your business correctly is the real starting line. For a full rundown of what you need to do, you can check out a guide to starting your business. This will help make sure you do it right from the beginning.

Get Your Business an EIN

Once your business is legally set up, you need to get an Employer Identification Number (EIN) from the IRS. You can think of an EIN as a Social Security number for your company. It’s a unique nine-digit number that identifies your business.

Even if you don't have employees, you absolutely need one. You’ll use your EIN for almost everything:

- Opening a bank account: Banks need an EIN to open a business checking account.

- Applying for credit: When you apply for accounts with suppliers or for a business credit card, you’ll give them your EIN, not your personal Social Security number. This is key to keeping your credit separate.

- Filing taxes: It's how the IRS keeps track of your business.

Getting an EIN is free, and you can apply for it right on the IRS website. It’s a simple but big step in making your business's financial identity official.

Open a Dedicated Business Bank Account

Now that you have your business papers and your EIN, it's time to open a business bank account. This might sound simple, but a lot of new business owners skip it, and that’s a huge mistake.

Mixing personal and business spending is the fastest way to get a loan application denied. A separate account creates a clean record. It shows lenders you're organized. When they look at your bank statements, they'll see a clear history of your business's income and expenses, which helps them see if your company is healthy.

Keeping these records straight is super important. Learning some small business bookkeeping basics will make your life a lot easier.

Establish a Professional Business Presence

Finally, you need to look like a real business. This means having a few key things that lenders and suppliers check for.

- A Business Phone Number: Get a phone line just for your business. It can be an internet phone service or a separate cell phone, but it must be listed under your business's name.

- A Professional Business Address: Your business needs a physical address. A P.O. Box is okay for mail, but it doesn't look great to credit bureaus. A home address can work, but a real office address adds more credibility.

These small details matter. They show that you're serious about your business. With this foundation built, you're ready to start opening the accounts that will actually build your credit history.

Opening Your First Credit Accounts

Okay, your business foundation is set. Now it’s time to actually get your first lines of credit and start building a track record.

You can't just walk into a bank and ask for a big loan right away. It’s like learning to ride a bike—you need training wheels first. For business credit, those training wheels are accounts with your suppliers.

These are often called tradelines or Net-30 accounts. The idea is simple: you buy stuff your business needs, and the supplier gives you 30 days to pay the bill. It's a small, informal loan. Paying that bill on time is your first chance to prove your business is reliable.

Finding Starter-Friendly Vendor Accounts

Here's the key: you need to find suppliers that do two things. First, they have to approve new businesses without a long credit history. Second—and this is a must—they have to report your payments to the business credit bureaus. If they don't report your payments, it’s like they never happened.

A good goal is to open between three and five of these accounts. Paying several accounts on time sends a much stronger signal than just having one.

Here are a few classic examples that are known for working with new businesses:

- Quill: Great for office supplies like paper and ink. They are known for reporting to Dun & Bradstreet.

- Uline: If you ship products, you'll need boxes and tape. Uline is a popular choice that reports to the bureaus.

- Grainger: For tools, safety gear, or industrial supplies, Grainger is a solid option.

To get started, you’ll apply for an account online using your business name and EIN. Once approved, place a small order—you don't have to spend a lot. For example, you could buy a box of pens from Quill for $20. The most important part is paying that bill, preferably way before the 30-day deadline. Paying early is a pro move that can boost your score even faster.

Graduating to a Business Credit Card

Once you have a few supplier accounts reporting good payments for a few months, your next big step is getting a business credit card. This is a huge deal. Why? Because a credit card is seen as a more serious line of credit than a simple supplier account.

Unlike your personal credit card, a business credit card is tied to your company's EIN. This is what keeps your business spending separate and helps build that independent credit history you’re working for.

When you're starting out, you probably won't get a card with a huge limit or fancy rewards. That's fine. Your goal is to find a starter card made for new businesses.

Key Takeaway: When you apply, many card companies will still ask for a personal guarantee. This is normal. It just means you're personally promising to pay the bill if the business can't. As your business credit gets stronger, you'll be able to get cards without this.

This separation is the whole point. Globally, many small businesses struggle because they don't have formal credit. In fact, 40% of small and medium enterprises have a hard time getting credit. Building a separate credit profile for your business is the best way to get the funding you need without risking your personal finances. You can read updated global estimates to learn more about how business credit helps companies grow.

Using Your First Business Card Wisely

Once you get that first business credit card, how you use it is everything. This isn't the time to go on a spending spree. The best plan is to use it for small, regular business expenses you'd be making anyway.

Think about things like:

- Your monthly software subscriptions

- Gas for a company car

- Taking a client out for coffee

Then, here’s the most important rule: pay the balance in full every single month. Never carry a balance. Paying it off completely and on time sends the strongest possible signal that your business is responsible with money. This one habit will build a powerful credit history much faster than supplier accounts alone.

Getting to Know the Business Credit Bureaus

Paying your bills on time is great, but if nobody is keeping score, it does nothing for your business credit. You have to know who is tracking your payments.

Imagine you're an amazing basketball player, but you only practice in an empty gym. Sure, you played well, but if there's no referee, none of your points officially count.

In the world of business credit, there are three main referees: Dun & Bradstreet (D&B), Experian Business, and Equifax Business. These are the major credit bureaus that collect information on how businesses like yours pay their bills. Each one works a little differently, but their goal is the same: to create a financial report card for your company.

When a lender wants to know if you're a good risk, they pull a report from one of these bureaus. Understanding what they see is the key to building a strong profile.

The Big Three of Business Credit

You don't need to memorize a bunch of technical terms. You just need to know who these companies are and what they care about. While each one has its own scoring system, they all boil down to one simple question: does this business pay its bills on time?

- Dun & Bradstreet (D&B): This is the oldest and most well-known name in business credit. They’re famous for their D-U-N-S Number, a unique nine-digit ID for your company. Getting one is your first move.

- Experian Business: You've probably heard of Experian for personal credit, and their business side is just as important. They look at your payment history and also check public records for things like lawsuits or liens.

- Equifax Business: Like Experian, Equifax also has a big presence in business credit. They gather data from suppliers and public records to create their own risk scores.

These bureaus don't just magically get this information. Your suppliers have to report your payment data to them. This information is often sent using a standard format. If you're curious, you can learn about the Metro 2 format for credit reporting to see how banks and suppliers actually communicate your payment history to the bureaus.

The Main Business Credit Bureaus at a Glance

Let's break down the key differences. While they all measure how trustworthy you are with credit, they each have a main score with a slightly different focus.

| Bureau | Key Score Name | What It Really Measures |

|---|---|---|

| Dun & Bradstreet | PAYDEX Score | How quickly you pay your bills compared to when they are due. |

| Experian Business | Intelliscore Plus | The chance your business will pay a bill more than 90 days late in the next year. |

| Equifax Business | Business Credit Risk Score | How likely it is that your business will become seriously late on its bills. |

As you can see, D&B's PAYDEX is all about how you pay, while Experian and Equifax focus more on predicting if you'll pay late. You need to build a strong profile with all three.

Your First and Most Important Step: The D-U-N-S Number

Before you do anything else, you need to get a D-U-N-S Number from Dun & Bradstreet. Think of it as officially putting your business on the map for the credit world. Without it, D&B can't even start a credit file on you.

The good news is, getting a D-U-N-S Number is completely free. You can apply for one on the D&B website. Don't fall for services that try to charge you for this. It’s the first step to becoming "visible" to lenders.

Simply put, no D-U-N-S Number means no D&B credit file. It’s the ticket you need to get into the game. Make this your top priority.

Once you have your D-U-N-S Number, D&B can start building your credit file and calculate your most important score: the PAYDEX score.

Understanding the D&B PAYDEX Score

If there’s one score you really need to know, it's the D&B PAYDEX score. It’s very simple and powerful. It’s a number between 1 and 100 that measures just one thing: how quickly you pay your bills.

It’s not about how much money you have or how profitable you are. It’s all about your payment habits.

- A score of 80 means you pay on time.

- A score of 100 means you pay 30 days early.

- A score below 80 means you’re paying late.

The impact of this is huge. Having accounts that report to the bureaus is directly tied to getting better loans. In fact, global trends show that digital and bureau data now drive most new business loans. The digital lending market is expected to hit around US$590 billion in 2025, with over 50% of small-business loans in developed markets coming from online lenders. This means businesses with clean credit data are far more likely to get approved.

Your job is to check your reports, see who is reporting your payments, and make sure everything is correct. If you find a mistake, dispute it right away. Your credit report is your business's financial resume—make sure it looks its best.

Growing and Maintaining Your Credit Score

You’ve done the hard work of getting a few accounts reporting to the credit bureaus. Great start. But your job isn't over.

Think of your new business credit score like a small plant. You’ve planted the seed, and now you need to water it and give it sunlight so it can grow strong. This is a habit, not a one-time project.

The good news is that the habits you need are simple. By focusing on a few key practices, you can build a credit score that opens doors to better financing and bigger opportunities.

Let's look at the simple habits that keep your business credit strong.

Pay Your Bills Early, Not Just on Time

This is the single most important habit you can build. Everyone knows paying bills on time is important, but for business credit, paying early is the secret weapon. This is especially true for your D&B PAYDEX score, which is a simple 1-100 scale measuring how quickly you pay.

A PAYDEX score of 80 means you pay on time. That's good, but it's just the starting point. A score of 100 means you pay your bills 30 days before they are due.

Paying even 15-20 days early can seriously boost your score above 80. It sends a powerful signal to lenders that your business manages its cash well.

Imagine two businesses. One pays its bills on the due date. The other pays them two weeks early. To a lender, the second business looks much more stable and reliable. That's the advantage you're creating.

Set calendar reminders to pay your bills a week or two before the actual due date. This simple change can make a huge difference in how lenders see your company.

Keep Your Credit Utilization Low

Once you get a business credit card, you need to watch your credit utilization ratio. This is just a fancy term for how much of your available credit you're using. If you have a credit card with a $10,000 limit and a $1,000 balance, your utilization is 10%.

Keeping this number low is very important. A high utilization—say, over 30%—is a red flag for lenders. It might make them think your business is stretched too thin.

Even if you pay the balance in full each month, a high balance on your statement date can still hurt your score. For instance, if you charged $8,000 on a $10,000 limit card for a big equipment purchase, your utilization would be 80%, which looks risky.

- Best Practice: Aim to keep your credit utilization below 20%.

- Pro Tip: If you need to make a large purchase, try to pay down the balance before your statement closes. This way, a lower balance gets reported.

Managing your spending is key here. Having a clear plan is essential for controlling costs. If you need help, check out our guide on how to create a business budget.

Apply for New Credit Strategically

As your score grows, you'll be able to get better credit, like bigger loans. Be smart about it. Every time you apply for new credit, it can cause a "hard inquiry" on your report, which can temporarily lower your score.

A few inquiries are normal. But applying for five different loans in a week looks desperate to lenders. Instead, do your research first, find the best lender for you, and apply for one thing at a time.

Building business credit is a marathon, not a sprint. It helps you get money to grow. The global finance gap for small businesses is estimated at a huge US$5.7 trillion, showing just how many companies are held back by not having enough credit. By building a formal credit history, your business can get the financing it needs.

Common Questions About Building Business Credit

When you're first getting into business credit, it's easy to feel a little lost. I get it. There are a lot of new terms, but the ideas behind them are pretty simple.

Let's walk through some of the most common questions I hear from business owners. The answers are more straightforward than you might think.

How Long Does It Take to Build Good Business Credit?

This is the big one. You can actually see a basic credit profile show up in as little as 60 to 90 days after your first few payments get reported. It’s surprisingly quick to get on the board.

But getting a "good" score—one that lenders really respect—is a different story. You should plan on at least 6 to 12 months of consistent, on-time (or early!) payments. This is about building a track record that proves your business is trustworthy.

Here’s how that timeline usually works:

- First, you get your D-U-N-S Number from Dun & Bradstreet.

- Next, you open three to five accounts with suppliers that report your payments.

- As you pay those bills, they report your good behavior to the credit bureaus.

- After a couple of months, a basic credit file and score will show up.

The key word here is consistency. That first year is your chance to show lenders you’re reliable.

Can I Build Business Credit Using Only My EIN?

Yes, and that’s the whole point! Using your Employer Identification Number (EIN) is how you create a financial identity for your business that is separate from your personal Social Security Number. When you apply for a business account or credit, you should always use your EIN.

This makes sure all your good payment history gets tied to your company’s credit file, not your personal one.

However, there’s a common catch at the beginning. For your first business credit card, most banks will require a personal guarantee. Don't worry; this is normal. It just means you're personally "co-signing" and agree to pay the debt if the business can't.

Think of it as a stepping stone. As you build a stronger business credit history, you'll start qualifying for credit based on your business alone, with no personal guarantee needed.

What Are the Easiest Starter Accounts to Get?

The easiest place to start is with Net-30 vendor accounts. They are perfect for new businesses because they often have very easy approval requirements. The best part? You're just buying things your business already needs.

Look for companies that are well-known for reporting to the business credit bureaus. A few of the classics that have helped many businesses get started are:

- Uline: For shipping and packaging supplies.

- Quill: A popular choice for office supplies like paper and pens.

- Grainger: For industrial supplies, safety gear, and tools.

The process is simple. You apply for a credit account online, place a small order (around $50 is usually enough to start), and they’ll send you a bill. Your only job is to pay that bill—and remember our pro tip: pay it early! Paying 15 days before the due date sends a much stronger signal than paying right on time. Getting three to five of these accounts reporting is the best first step you can take.

What Is the Biggest Mistake to Avoid?

The single biggest mistake new owners make is mixing their personal and business finances. It’s a huge error that can undo all your hard work.

When you pay for business expenses with a personal card, you get zero credit for it. To the credit bureaus, that payment might as well have never happened.

It also creates a massive bookkeeping headache and can even put your personal assets at risk if your business gets sued. Lenders want to see a clean, professional financial history that belongs to the business alone. I once worked with a client who couldn't get a loan for his growing landscaping business because he'd been paying for all his new mowers and equipment with his personal credit card. The bank couldn't see any of that positive history under his business's name.

The fix is simple: keep everything separate from day one. Open a dedicated business bank account and get a business debit card. All money should flow through those accounts. This discipline is the foundation of a strong, fundable company. As things get more complex, that's often a sign of when to hire a CFO to help you keep things clear.