If you’ve ever tried to use regular business bookkeeping rules for a medical practice, you know it’s like trying to fit a square peg in a round hole. It just doesn't work.

Medical practice bookkeeping isn't just about tracking money in and money out. It's a special way of handling finances built for the messy, delay-filled world of insurance claims, patient bills, and healthcare rules. Getting it right is the key to a healthy practice that can focus on what really matters: your patients.

What Makes Medical Practice Bookkeeping So Different

Imagine running a coffee shop. A customer orders a latte, pays you right away, and the whole thing is done in a minute. Simple and clean.

Now, picture a restaurant where a customer eats a meal, leaves, and tells you someone else—like their boss—will decide how much of the bill to pay, and then maybe send you a check in a few weeks or months. That's a lot closer to how money works in a medical practice.

This is why medical practice bookkeeping is its own thing. It’s less about simple math and more about solving a slow-moving money puzzle where a huge chunk of your income is always on its way to you.

Let's look at the main differences.

Medical Bookkeeping vs. Regular Business Bookkeeping

| Bookkeeping Task | A Regular Business (Simple) | A Medical Practice (Complex) |

|---|---|---|

| Getting Paid | You get cash or a card payment right away. | Payment arrives 30-90+ days after you see the patient, after insurance paperwork is done. |

| Money Owed to You (A/R) | A small list of late payments. | A huge, always-changing list of money owed by dozens of insurance companies and patients. |

| Adjusting Income | You handle simple returns or discounts. | You deal with confusing insurance adjustments, write-offs, and denials based on their rules. |

| Who Pays | One customer pays the full amount. | Multiple payers for one visit: the insurance company, maybe a second insurance, and the patient (copays). |

| The Bill | You create a simple invoice. | You use complex medical codes (like CPT, ICD-10) that decide how much you get paid. A tiny mistake can mean you get nothing. |

| The Rules | General business and tax rules. | You have to follow strict HIPAA rules for patient privacy and many other healthcare laws. |

As you can see, it’s not even close. A simple mistake in a shop might upset a customer. In a medical practice, a simple mistake can mean a payment is delayed for months or never comes at all.

The Constant Wait for Payment

In almost any other business, money comes in when you do the work. For a doctor, the path from treating a patient to getting paid is a long one. A claim has to be coded right, sent to insurance, reviewed, approved (hopefully), and only then is the money sent.

This whole process creates a big lag in your cash flow. While the goal is to get paid in about 30-45 days, many practices struggle to keep it under 60. Every day a claim sits unpaid is a day your practice is giving an interest-free loan to a giant insurance company.

The heart of medical bookkeeping isn’t just writing down what you’ve earned; it's about actively chasing the money you are owed.

Why Every Dollar Needs to Be Watched

Because you're never sure when you'll get paid, keeping clean and accurate books is a must. Without a solid system, it's scary easy to lose track of which insurance claims are paid, denied, or just floating around somewhere.

This is where practices lose money without even knowing it. Good bookkeeping is like your financial control center, giving you a clear, real-time view of:

- Who owes you: Tracking every last dollar from both patients and insurance companies.

- Your real income: Seeing how much you actually collect after all the insurance discounts and write-offs.

- Your practice's health: Knowing if your cash flow can actually cover important bills like payroll and rent.

This is totally different from standard bookkeeping, which often just looks at the big picture. Here, the small details matter most. To learn more, check out our complete guide on accounting for medical practices.

In the end, learning the basics of medical practice bookkeeping is the first step to building a practice that is stable, makes a profit, and is a lot less stressful to run.

The Unique Financial Hurdles Every Practice Faces

Running a medical practice means you're not just a doctor; you're also a business owner dealing with some very specific money headaches. Unlike a shop where money comes in right away, your cash is tangled up in insurance rules, payment delays, and confusing codes. These aren't just small problems—they're the big challenges that can make or break your practice.

Let’s be honest, these are the issues that keep practice owners up at night. The good news is, every practice faces them. Once you understand them, you can start to get them under control. We'll break down the three biggest headaches: the insurance maze, the long wait for payments, and the high-stakes game of medical coding.

The Ever-Changing Insurance Puzzle

Dealing with insurance companies can feel like solving a puzzle where the pieces keep changing. You provide a service, send in a claim, and then you wait. Each insurance company has its own set of rules, payment rates, and policies. A procedure that one company covers might be denied by another or paid at a totally different price.

This means you never really know exactly how much you'll get paid for a service until long after the claim is processed. This is why medical practice bookkeeping is so focused on tracking claims and payments from dozens of different sources, each with its own quirks. It's less about simple accounting and more about managing financial chaos.

Waiting for Your Money: The Reality of Accounts Receivable

In the medical world, you need to get used to the term Accounts Receivable, or A/R. This is just the money owed to you for work you've already done. For a medical practice, your A/R is a huge, constantly moving list of unpaid insurance claims and patient bills.

Imagine doing your job today but not getting paid for it for 30, 60, or even 90 days. That's the daily reality for a doctor.

This delay isn't just annoying; it's a major strain on your cash flow. While you wait for insurance companies to pay you, you still have to pay your own bills like payroll, rent, and medical supplies right away.

This is where so many practices get into trouble. I once worked with a small pediatric practice that was always struggling for cash. They were busy all the time but the bank account was always low. After we looked at their books, we found over $50,000 in claims that were more than 90 days old. Some were denied for tiny errors, and others were just forgotten. By organizing their A/R and making a plan to follow up, they collected most of that money and finally got stable.

How Tiny Coding Mistakes Cost Thousands

Every service you provide is turned into a set of codes before it's sent to an insurance company. These codes are the language insurance speaks—they tell the company exactly what you did. A small mistake here can cause big problems.

Think of it like ordering a pizza online. If you accidentally type in the wrong code for pepperoni, your pizza shows up with anchovies. You don't get what you wanted, and the pizza place doesn't get paid right.

It’s the same in medical billing. If a routine office visit is coded wrong, the insurance company might deny the whole claim or pay a lot less.

- Wrong Code: Using a code for a simple procedure when a more complex one was done means you get paid less.

- Missing Code: Forgetting to add a code for something extra you did means you won't get paid for it at all.

- Old Code: Using a code that isn't valid anymore will get your claim rejected instantly.

These aren't rare mistakes. A single wrong number can cause a claim to be denied, forcing your staff to spend time fixing and resubmitting it, which delays payment even more. When this happens over and over, the lost money adds up fast, quietly hurting your practice. Getting codes right isn't just paperwork; it's a key part of your financial plan.

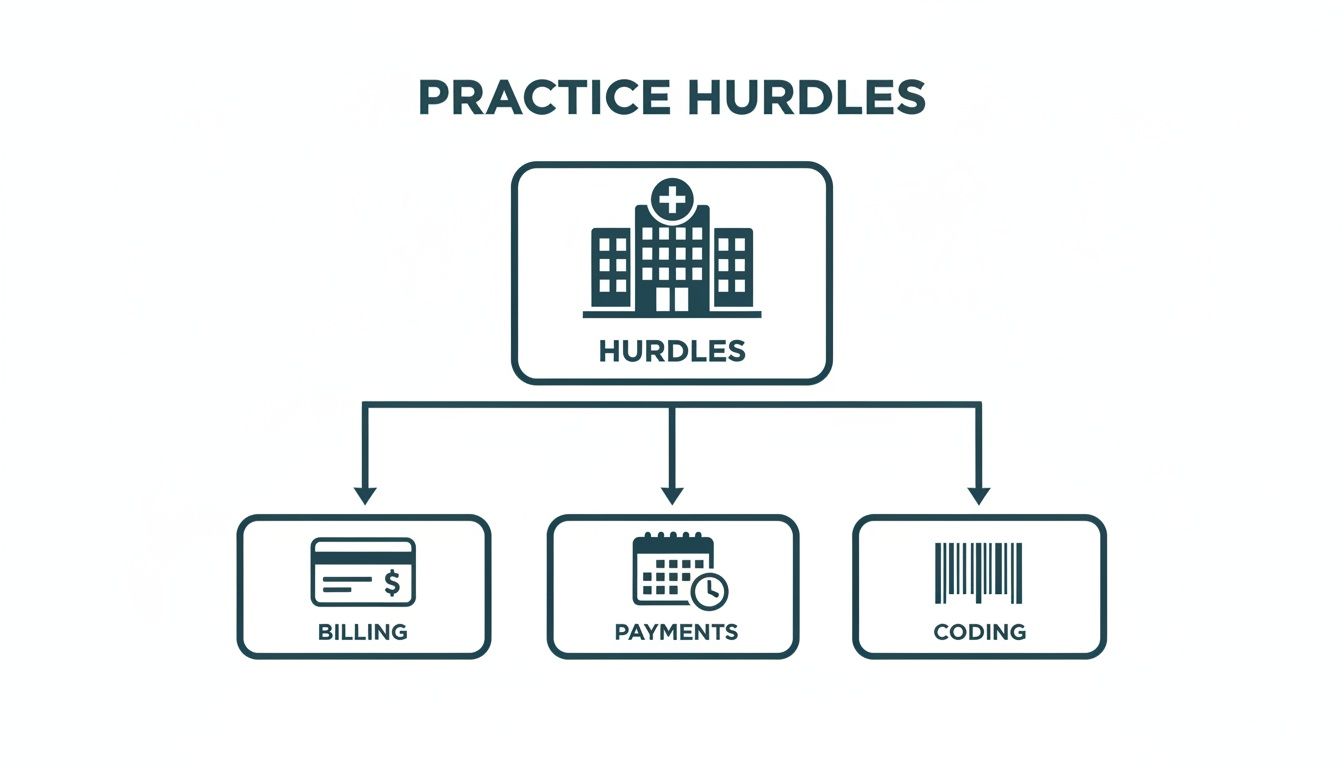

Core Bookkeeping Tasks Your Practice Needs

Think of your practice’s finances like a patient's chart. To keep it healthy, you need regular check-ups and consistent care. Good medical practice bookkeeping isn’t about one big effort; it’s about simple, repeatable habits that keep your money organized and moving.

Putting these systems in place brings order to the chaos. It stops money from slipping through the cracks and gives you a clear, real-time picture of where your practice stands.

Let's walk through the key tasks—daily, weekly, and monthly—that form the backbone of a financially strong practice.

The visual below shows the common money hurdles that these bookkeeping tasks are designed to fix.

As you can see, billing problems, payment delays, and coding mistakes are the biggest roadblocks. A structured bookkeeping routine is your best defense against them.

Your Daily Financial Habits

These are the small, must-do tasks that stop problems from piling up. They should only take a few minutes each day but make a huge difference to your cash flow.

Record All Payments Right Away: Every payment that comes in—whether it's a check from an insurance company or a patient's copay—needs to be recorded the day you get it. This keeps your records perfectly accurate.

Enter Bills and Expenses: Did you get a bill from your medical supply company? Did you buy lunch for the staff? Enter these bills and receipts into your accounting software immediately. Letting them pile up is how you end up with messy books and missed payments.

Your Weekly Financial Check-In

Once a week, set aside some time to look at the bigger picture and make sure everything is on track. This is your chance to catch problems before they turn into serious issues.

- Review and Send Claims: Make sure all services from the past week have been billed. A week-old service that hasn't been billed is money you can't collect yet.

- Check on Unpaid Claims: Look at your accounts receivable. Are there any claims that are over 30 days old? A quick weekly check helps you spot and follow up on delayed payments before they get ancient.

- Run Payroll: If you pay your team weekly or bi-weekly, this is a key weekly task. Paying your staff correctly and on time is basic to running a smooth practice.

Think of bank reconciliation like balancing your checkbook at home. You're just making sure the money your records say you have matches what the bank says you have. It’s a key monthly step to catch errors, spot weird charges, and make sure all your payments have gone through.

Your Monthly Financial Review

At the end of each month, it's time to close the books and see how you did. This routine gives you the high-level view you need to make smart business decisions.

Key Monthly Tasks:

- Reconcile Bank and Credit Card Accounts: This is a must. Compare your own records against your bank statements to make sure every single transaction lines up.

- Review Your Financial Reports: Pull up a simple Profit & Loss (P&L) statement and a Balance Sheet. The P&L shows if you made or lost money that month. The Balance Sheet gives you a snapshot of your overall financial health.

- Pay Your Bills: Pay off all outstanding bills to your suppliers to keep good relationships and avoid late fees.

Finally, a huge part of good medical practice bookkeeping is keeping clean records. You need a simple, organized way to store important papers like payroll files, employee records, receipts, and bank statements. Whether you do it digitally or with paper, keeping these files in order will save you a giant headache at tax time or if you ever get audited.

Key Numbers That Reveal Your Practice's Health

You don't need a finance degree to understand how your practice is doing. In fact, you can get a clear picture by just watching a few key numbers. Think of them as your practice’s vital signs—like a patient's blood pressure or heart rate, they tell you what’s working and what needs attention right away.

Good medical practice bookkeeping isn’t just about writing down numbers. It’s about turning all that data into simple information you can act on. By focusing on a few key performance indicators (KPIs), you can quickly see how healthy your finances are and start making smarter choices.

Days in Accounts Receivable (A/R)

This number answers a simple but important question: "How long does it take us to get paid?" It measures the average number of days between seeing a patient and having the money in your bank account.

Imagine you lend money to a friend. You’d want to know if they’ll pay you back in a week or three months, right? It's the same idea. A high Days in A/R means your cash is tied up for too long, which can make it hard to pay your own bills like salaries and rent.

Your goal should be to keep this number low. A good target for most practices is under 40 days. If you see it creeping up, that’s a big warning sign that something in your billing process is broken.

Net Collection Rate

Think of this as your practice’s report card for getting paid what you're owed. Your Net Collection Rate shows you what percentage of money you actually collect out of the total amount insurance allows you to be paid.

It’s a powerful way to measure how effective your billing team is. A low rate means money is slipping through the cracks, whether it's from billing mistakes, not fighting denials, or just poor follow-up.

A good Net Collection Rate should be 95% or higher. Anything less is like doing all the work but not getting your full paycheck. This number is key to understanding if your practice is truly making a profit.

Clean Claim Rate

This one is simple: What percentage of your insurance claims get accepted and paid on the very first try? That’s your Clean Claim Rate.

A high clean claim rate means your team is doing a great job with medical coding and billing. This is huge, because every denied claim costs you time and money to fix and resubmit. It also makes your Days in A/R worse, since fixing mistakes adds delays.

A strong clean claim rate is 95% or higher, and your denial rate should be below 5%.

The real value comes from using these numbers. Understanding them is the first step, but using them to guide your practice toward better financial health shows the necessity of business skills for healthcare leaders. Watching these few numbers turns bookkeeping from a chore into a powerful tool. It's the core of a strong healthcare revenue cycle management strategy, turning confusing data into a clear path forward.

How to Manage Rising Practice Costs

It feels like the cost of everything is going up, and that’s especially true when you’re running a medical practice. From staff salaries to the price of basic supplies, rising costs can quickly eat into your profits and create a lot of stress.

But feeling the squeeze doesn't mean you have to start cutting corners on patient care.

In fact, the most successful practices I’ve seen aren’t just cutting costs; they're getting smarter about them. They get a crystal-clear view of where their money is actually going and then find ways to be more efficient. It all starts with clean, clear books that show you the whole picture.

Finding Your Biggest Cost Drains

Before you can control your spending, you need to know exactly where your money is going. For most medical practices, the biggest costs usually fall into a few areas.

- Staffing Costs: This is almost always the biggest expense. It’s not just salaries, but also benefits, payroll taxes, and bonuses to keep great people.

- Medical Supplies and Equipment: The cost of everything from gloves and gauze to vaccines adds up fast. Without a tight system, it's easy to over-order or waste supplies.

- Technology and Software: Your practice relies on a lot of software—EHR, billing, payroll. Those monthly or yearly fees are a big, ongoing expense.

Recent numbers show just how serious this is. Operating costs for medical practices have jumped by about 11.1% in a year. The practices that kept their costs under control did so through better financial management. It’s a good reminder that control comes from clarity.

Smart Ways to Control Spending

Once you know where your money is going, you can start making smart changes. The goal isn't just to spend less—it’s to spend smarter. Here are a few real-world ideas that work.

1. Be Smart About Ordering Supplies

Instead of ordering supplies whenever someone notices you're low, create a system. Track how quickly you use things to avoid overstocking items that might expire. It’s also a great idea to put one person in charge of inventory and let them negotiate with suppliers for better prices on bigger orders.

2. Review Your Vendor Contracts

Don’t just let contracts for services like cleaning, IT support, or medical waste disposal renew automatically every year. Take time to review them and see if you can get better rates. You might be surprised by how much you can save just by shopping around or asking your current vendor for a better deal.

3. Make Smart Staffing Choices

Staffing is your biggest cost, but it's also your most important asset. Instead of cutting staff, focus on being more efficient. Cross-train your team so they can cover for each other, which reduces the need for expensive temp help. Also, make sure you have the right mix of clinical and office staff to support your patients without being overstaffed on slow days.

Tighter expense controls aren't about being cheap; they're about being intentional. Every dollar you save on unnecessary costs is a dollar you can put back into better patient care, new equipment, or rewarding your hardworking team.

To better manage rising costs, many practices are looking at cloud-based practice management solutions that help streamline tasks and make the office more efficient.

Ultimately, having accurate medical practice bookkeeping is the foundation for all of these strategies. It turns vague money worries into a clear plan.

When to Outsource Your Practice Bookkeeping

Let’s be honest. Trying to manage your practice’s books yourself, or asking your office manager to squeeze it in between a dozen other tasks, can only get you so far. At some point, most practice owners hit a wall. They're spending weekends buried in spreadsheets instead of with family, or they're constantly wondering if the numbers are even right.

It’s a common story. You became a doctor to care for people, not to become a part-time bookkeeper. Realizing when it’s time to bring in a professional isn’t a sign of failure—it’s a smart business move that gets you back to what you do best.

Telltale Signs You Need Help

So how do you know when you’ve hit that point? The signs are usually pretty clear. If you find yourself nodding along to any of these, it’s probably time to think about outsourcing.

- Financial tasks are stealing your time: Are you or your key staff spending hours each week on bookkeeping that could be spent on patients or growing the practice?

- You're always worried about cash flow: You know you're busy, but there never seems to be enough cash in the bank to feel safe.

- Your reports are confusing or late: You can't get a simple Profit & Loss statement when you need one, or you just don't trust the numbers.

- You feel like you're flying blind: You have no idea what your key financial numbers are, so you can't make good decisions about hiring, buying equipment, or expanding.

If this sounds familiar, it’s a strong sign that your current system is holding you back. This is especially true as the medical practice management industry grows. Revenue is expected to hit $210.4 billion in 2025, and with that growth comes more complexity. As practices get bigger, managing the finances becomes a full-time job. You can find more on this trend at IBISWorld.com.

More Than a Number-Cruncher

Outsourcing your medical practice bookkeeping isn’t just about hiring someone to enter numbers. It’s about getting a financial partner who understands the unique challenges of a healthcare business.

Think of it this way: a good outsourced bookkeeper doesn't just hand you reports. They help you understand what the numbers actually mean for your practice and guide you toward better financial health.

This partnership turns your finances from a source of stress into a tool for growth. You get clear, easy-to-understand reports that give you a real-time view of your practice's performance. They help you track the key numbers we talked about, like your Net Collection Rate, so you can spot problems before they get big. For a deeper dive, check out our guide on outsourced bookkeeping for small business.

Ultimately, bringing in an expert frees you and your team to focus on what’s important. By handing off the financial work, you get back valuable time and mental energy. This allows you to focus completely on providing great patient care, knowing that the money side of your practice is in good hands.

Common Questions About Medical Bookkeeping

Once you get the basics down, it’s normal to have more questions. The world of medical practice bookkeeping has its own quirks, and I find the same topics come up again and again. Here are some straightforward answers to the most common questions I hear.

What Is the Difference Between a Bookkeeper and an Accountant?

Let me give you an analogy I use all the time. Think of your bookkeeper as the nurse who takes your practice’s vital signs every day. They’re handling the daily financial tasks—recording payments, paying bills, and running payroll. Their job is to keep your financial records clean, accurate, and up to date.

An accountant is more like the doctor who looks at those vitals to give you a diagnosis of your practice's overall health. They take the clean records from the bookkeeper to do the big-picture work, like preparing tax returns, creating financial plans, and advising you on major business decisions. You really need both for a healthy practice.

A bookkeeper records the financial story of your practice day by day. An accountant reads that story to help you plan for a better future. Both jobs are essential, but they focus on different things.

What Software Do I Really Need for My Practice?

Most medical practices really need two different software systems working together. Don’t try to make one system do everything.

Practice Management (PM) System: This is your clinical workhorse. It handles all the healthcare tasks like patient scheduling, billing insurance, and tracking patient accounts.

Accounting Software: This is a general business tool like QuickBooks. It manages the rest of your business finances—payroll, rent, supply costs, and so on.

The most important part is making sure these two systems can "talk" to each other. You need a smooth way for the payment data from your PM system to get recorded correctly in your accounting software. A good medical practice bookkeeping partner can set this up so you get one complete financial picture without doing double the work.

How Much Does It Cost to Outsource Bookkeeping?

There isn't a simple, one-size-fits-all price for outsourced bookkeeping. The cost depends on the size of your practice, how many transactions you have each month, and what level of service you need.

Most firms will offer a few different options. This can range from basic bookkeeping and monthly reports all the way to more involved services that include advice on how to make your practice more profitable. Almost always, the cost is less than hiring a full-time financial employee, and you get access to a much higher level of expertise.

Are you ready to get a clear, accurate picture of your practice's financial health? The team at MyOfficeOps provides expert bookkeeping and advisory services designed specifically for medical practices. We handle the numbers so you can focus on your patients. Schedule your free discovery call today.