Let’s be honest: just because you made a lot of sales doesn't mean your bank account is full. If you've ever looked at a big revenue number and wondered where all the money went, the answer is often found in something called contribution margin.

In simple terms, contribution margin is the money you have left from a sale after you pay for the costs of making that one sale. Think of it as the cash each sale "contributes" to paying your big bills—like rent and salaries—before you can take any profit.

So, What Is Contribution Margin?

Imagine you have a lemonade stand. It's a simple business, but the numbers are important.

You sell each cup for $3.00. But to make that one cup, you spent $1.00 on lemons, sugar, and the cup itself. The $2.00 left over is your contribution margin for that cup. It’s the money from the sale that helps you pay for the stand’s permit fee and the sign you painted.

To get this, you need to split your costs into two types:

- Variable Costs: These costs change with how much you sell. For the lemonade stand, it's the cost of lemons and cups. Sell more, and these costs go up. Sell less, and they go down.

- Fixed Costs: These are costs that stay the same no matter how much you sell. Think of your stand permit, the table you use, or the rent for your storefront. You pay these whether you sell one cup or a hundred.

Once you understand this split, you can see how profitable your business really is. It helps you see how much cash each product or service brings in to keep the lights on and build your profit. You can start asking better questions, like, "How many products do I need to sell just to cover my rent this month?"

This isn't just theory. When I work with service businesses, this is a real game-changer. We've seen small companies improve their profits by an average of 25% in a year, often just by using contribution margin to find which services were not making enough money.

The main idea is simple: Not all sales are equal. Contribution margin shows you which sales are working hardest for your business by covering your fixed costs and building your profit.

Understanding this helps you make smarter money decisions—a skill that goes hand-in-hand with knowing how to read an income statement. If you want to get better at managing your finances, looking into outsourced finance and accounting services can give you the expert help you need to improve your business.

The Three Simple Formulas You Need

Don't let the word 'formula' worry you. These aren't hard math problems—they're simple tools that give you a clear look at your business. You don't need to be an accountant to use them, but they’ll help you think like one.

Let's use a real example. Imagine you own a small coffee shop. You sell a latte for $5.00. The variable costs to make one—the milk, coffee, cup, and lid—add up to $1.50. Let's use these numbers to see the formulas work.

1. The Per Unit Contribution Margin

This is your starting point. It tells you exactly how much cash you make from selling just one item. It's the best way to figure out if a single product is worth selling.

The Formula:

Sales Price Per Unit – Variable Cost Per Unit = Contribution Margin Per Unit

For our coffee shop, the math is easy:

- $5.00 (Latte Price) – $1.50 (Milk, Coffee, Cup) = $3.50

That $3.50 is the contribution margin for one latte. It’s the cash that one sale makes to help pay for your rent, salaries, and other fixed costs before you can think about profit.

2. The Total Contribution Margin

This formula zooms out to give you the big picture. It adds up the contribution from all your sales to show how much total cash your business made over a time period, like a month or a quarter, to cover its fixed costs.

The Formula:

Total Sales – Total Variable Costs = Total Contribution Margin

Let’s say our coffee shop sold 1,000 lattes in a month. Here’s how that works out:

- Total Sales: 1,000 lattes x $5.00 = $5,000

- Total Variable Costs: 1,000 lattes x $1.50 = $1,500

- Total Contribution Margin: $5,000 – $1,500 = $3,500

This $3,500 is the total money the shop has to pay its monthly rent, employee wages, and utilities. Anything left after that is profit.

3. The Contribution Margin Ratio (Percentage)

This last one is very helpful because it turns your contribution margin into a percentage. The ratio is great for comparing how profitable different products are. Is a latte more profitable than a muffin, even if their prices and costs are different? The ratio gives you a direct, apples-to-apples answer.

The Formula:

(Contribution Margin / Sales Price) x 100 = Contribution Margin Ratio

Let's look at our single latte again:

- ($3.50 / $5.00) x 100 = 70%

This means that for every dollar in latte sales, 70 cents can be used to pay for fixed costs and, later, profit. You could do this same quick math for a muffin or a sandwich and immediately see which item makes more money for your business.

For a deeper look at the details, especially for businesses with more complex product costs, check out this guide on how to calculate contribution margin.

People mix these two up all the time, but the difference is simple—and very important for making smart business decisions. Both contribution margin and gross margin tell you something about your business's profit, but they tell two different stories.

Think of it like this: gross margin looks at what's left after paying for the product itself. Contribution margin, on the other hand, looks at what’s left after paying for all the costs that change when you make a sale.

Let's use a T-shirt business as an example.

- Gross Margin tells you the profit left after paying for the T-shirt fabric and the ink. These direct product costs are your cost of goods sold.

- Contribution Margin tells you the profit after paying for those same costs plus any other variable costs, like the $2 commission you pay a salesperson for each shirt they sell.

The difference seems small, but it gives you a much clearer view of your profit. Gross margin tells you if your product is profitable. Contribution margin tells you if your entire sales process is efficient and actually adding money to your bank account.

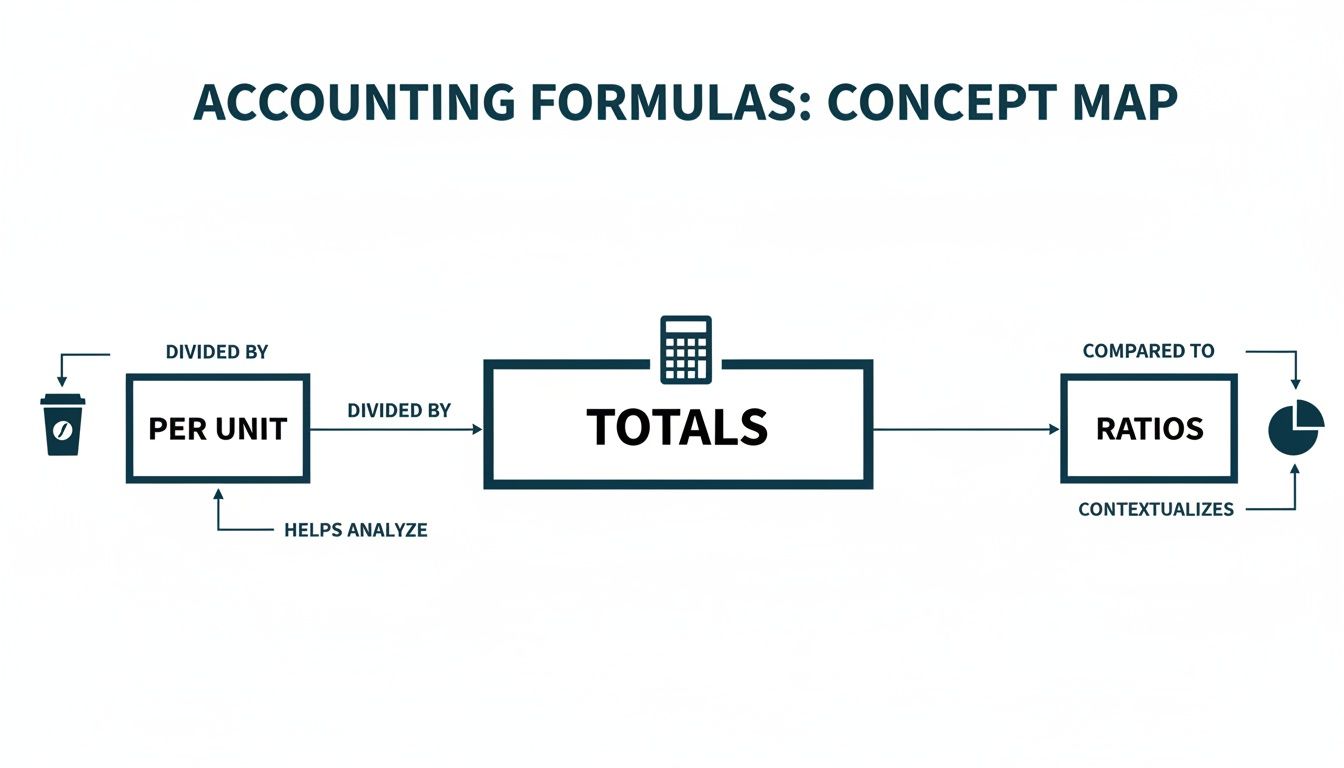

This picture shows how the different ways of looking at contribution margin—by unit, in total, or as a ratio—all work together to give you a complete picture.

Each formula gives you a different view, from the total big picture down to the profit of a single item or a percentage you can compare.

Contribution Margin vs. Gross Margin

This table shows the key differences between the two numbers side-by-side.

| Aspect | Contribution Margin | Gross Margin |

|---|---|---|

| Purpose | Shows how much money from a sale is left to cover fixed costs and make a profit. | Shows the profit of the product itself, before other business expenses. |

| Formula | Revenue – All Variable Costs | Revenue – Cost of Goods Sold (COGS) |

| Costs Subtracted | Includes COGS plus other variable costs like sales commissions and shipping supplies. | Only includes direct costs of making a product or delivering a service (COGS). |

| Focus | Making decisions (pricing, break-even, which products to sell). | Financial reports and product-level profit. |

| Key Question | "How much does each sale help pay my rent and salaries?" | "Is this product priced right compared to what it costs to make?" |

While both are useful, I find that business owners use contribution margin most for making daily decisions. It shows you the real cash you get from each sale.

A Construction Business Example

Let’s see how this works in the real world. Imagine a local construction business gets a $50,000 job to remodel a kitchen.

Here’s the job breakdown:

- Total Revenue: $50,000

- Materials (Lumber, Cabinets): $20,000

- Subcontractor Labor (Variable): $15,000

- Sales Commission (Variable): $2,500

Now, let's calculate the two margins for this job.

Gross Margin Calculation:

$50,000 (Revenue) – $35,000 (Materials & Sub Labor) = $15,000 Gross ProfitContribution Margin Calculation:

$50,000 (Revenue) – $37,500 (Materials, Sub Labor, & Commission) = $12,500 Contribution Margin

See the difference? That $12,500 contribution margin gives a better picture of the actual cash this job brings in to pay the company's fixed costs, like office rent, insurance, and salaried project managers.

This isn't just a math exercise. This is how smart businesses succeed. Companies that track contribution margin often see big improvements. By using this number to find and drop their least profitable clients, some firms have increased their overall gross margins by an average of 12%. Understanding contribution margin helps you focus on what really makes you money.

How to Use Contribution Margin for Smarter Decisions

Okay, so you have the numbers. Now what? This is where understanding contribution margin stops being a math problem and starts making you money. It’s more than a number for your accountant—it’s a tool for running a smarter, more profitable business.

Think of it as your guide. It points you toward the most profitable decisions and away from choices that secretly lose you money. Let’s walk through four ways you can use it to make better choices every day.

1. Set Smarter Prices

For most business owners, pricing can feel like guesswork. Should you charge more? Less? Contribution margin takes the guessing out of it and gives you a solid reason for your pricing.

It shows you the lowest price you can possibly set. Your price must cover your variable costs for that product or service. If it doesn’t, you are literally paying a customer to buy your product.

Key takeaway: A positive contribution margin means every sale helps you pay down your fixed costs like rent and salaries. The bigger the margin, the faster you get to real profit.

2. Find Your Break-Even Point

The break-even point is one of the most important numbers a business owner can know. It’s the exact amount of sales you need to cover all your costs—both fixed and variable. You aren’t making a profit yet, but you aren’t losing money either.

Contribution margin is the key to finding this number. The formula is simple:

- Break-Even Point (in Units) = Total Fixed Costs / Contribution Margin Per Unit

Once you know you need to sell 500 items this month just to cover your costs, you have a clear goal. It changes a vague goal like "make more money" into a clear, real mission. You can learn more about this calculation in our guide on how to calculate your breakeven point.

3. Decide on Special Orders

Imagine a new customer offers you a big, one-time project, but they want a discount. Your first thought might be "no," but contribution margin gives you the real answer.

As long as the discounted price is still higher than your variable costs for that job, taking the project brings in a positive contribution margin. That means it’s adding cash to your business that can go toward your fixed costs. If you have the time and it won’t mess up your other work, accepting that special order is often a smart move.

4. Find Your Most Profitable Products and Services

Not all of your sales are the same. Some of your products or services are big money-makers, while others are just taking up space. A contribution margin analysis is how you tell the difference.

By regularly calculating the contribution margin for each product, you can make smart decisions that have a huge impact on your profit:

- Promote: Put your marketing money on the products with a high margin.

- Reprice: Can you change the price on lower-margin items to make them more profitable?

- Bundle: Could you sell a low-margin item with a high-margin one?

- Drop: Is it time to stop selling products or services that barely make any money?

This is especially important for service businesses, like the healthcare practices I work with. For them, just calculating the contribution margin for each procedure led to an average profit increase of 22%. They found that routine visits often had a contribution margin ratio of 45%, which showed them exactly where to focus their efforts to grow.

Using contribution margin this way changes your financial data from a report card on the past to a map for future growth.

Theory is fine, but let’s talk about what this really looks like. This isn’t a high-level idea only for big companies. It’s a tool I see small business owners use every day to make smarter decisions.

Let's look at three different businesses. You'll see how one simple calculation can change how they see their own business.

A Marketing Agency Finds Its Best Clients

Imagine a small marketing agency with five clients. On paper, the one with the biggest monthly fee—let's call them Client A—looks like the best one. But is that the whole story? The owner decides to check the contribution margin for each client.

First, she has to find her variable costs. These aren't the fixed costs like her office rent or software. They're the costs that change directly because of the work she does for a specific client.

- Hours billed by her freelance graphic designer for Client A's projects.

- The ad budget she manages for Client B.

- Sales commissions paid to the person who got Client C.

After checking the numbers, the owner is surprised. Client A, even with their big fee, needs so much freelance work that their contribution margin is the lowest of all. Meanwhile, a smaller client, Client D, needs very little extra help and has a great contribution margin.

This one discovery is a game-changer. The owner realizes Client A looks good on paper but doesn't really help pay the bills. She decides to talk to Client A about changing their contract to match the real cost of the work. She also tells her team to find more clients like Client D.

A Construction Contractor Bidding on a Job

Now, picture a local contractor. For them, job profit is everything, especially when material and labor costs change all the time. Just adding a standard markup to every bid can be a mistake.

Instead, they use contribution margin to bid on a new home extension project. The client’s budget is $100,000. The contractor calculates all the variable costs for this specific job:

- Lumber, drywall, and other materials

- Wages for the hourly construction crew

- Fees for subcontractors like plumbers and electricians

The total variable costs add up to $65,000.

The Calculation:

$100,000 (Total Revenue) – $65,000 (Total Variable Costs) = $35,000 Contribution Margin

This $35,000 (or a 35% contribution margin ratio) is what this job will give the company to help pay for its fixed costs—things like insurance, truck payments, and office staff salaries. This is common, as construction firms in my area often use this same thinking to manage their profits when costs change. You can learn more about how different businesses handle this by reading about contribution margin for various industries.

With this number, the contractor knows exactly how much "room" he has. It helps him bid against others while making sure the job is worth his time.

A Healthcare Practice Considering a New Service

Finally, let's look at a physical therapy practice. The owners are thinking about adding a new service: sports injury assessments. Before they spend money on marketing and training, they want to know if it's a smart financial move.

They estimate the revenue and variable costs for one assessment:

- Price to Patient: $250

- Variable Costs:

- $75 for the therapist’s time (direct labor).

- $25 for supplies used once.

- Total Variable Cost per Assessment: $100

The contribution margin for each new assessment is $150 ($250 – $100). This tells them that for every patient who gets this service, they’ll make $150 to help cover the clinic's fixed costs and, eventually, add to their profit.

Now they can easily figure out how many assessments they need to do each month to make the new service worthwhile. It’s no longer a gut feeling; it’s a decision backed by simple, real math.

Common Mistakes and How to Avoid Them

Contribution margin is a great tool, but like any tool, it’s only useful if you use it right. I’ve seen business owners get excited about their numbers, only to make bad decisions because they made a few common mistakes.

Let’s go over the most common mistakes so you can avoid them and use your numbers to make good decisions.

Mixing Up Fixed and Variable Costs

The single biggest mistake I see is not sorting costs correctly. If you accidentally call a fixed cost (like your office rent) a variable one, your contribution margin will look lower than it is. This can make a good product look like a bad one, leading you to stop selling it for no good reason.

The fix is simple. For every cost, ask yourself this question: “If I sell one more item, does this cost go up?”

- If the answer is yes—like the cost of materials or a sales commission—it’s a variable cost.

- If the answer is no—like your monthly insurance bill or a manager's salary—it’s a fixed cost.

Getting this right is the most important step. Everything else depends on it.

Another common mistake is focusing only on the margin and forgetting the big picture. For example, a low-margin product might be your best marketing tool. It could be a "loss leader" that brings new customers in the door who then buy your more profitable items.

Finally, always remember what contribution margin is for: short-term, daily decisions. It's perfect for pricing a special order or deciding if a job is worth taking. For long-term plans, though, it has limits because it doesn't include all your fixed costs.

Frequently Asked Questions

Still have a few questions? You're not alone. Once business owners start to understand contribution margin, a few common questions always come up. Let's answer them.

Can a Business Have a Negative Contribution Margin?

Yes, and it’s a huge red flag for your business.

Imagine you sell handmade birdhouses for $20. But the wood, nails, and paint for each one cost you $22. You have a negative contribution margin of $2.

This means you are losing money on every single sale. Each birdhouse you sell puts you in a deeper hole, and that’s before you even pay for your workshop rent or your own salary. This is a problem that must be fixed right away, either by raising prices or finding a way to lower those direct costs.

How Often Should I Calculate My Contribution Margin?

As a general rule, checking it monthly is a great habit to have. This gives you a regular look at your profitability without being too much work.

However, if your costs change a lot—like a contractor buying lumber or a baker whose flour prices change weekly—you should calculate it more often. For these businesses, checking the numbers for each project or even each week gives them the information they need to make smart pricing decisions before it's too late.

Is This Number Useful for a Service Business?

Absolutely. It’s just as important for service businesses as it is for companies selling physical products. The only tricky part is figuring out your variable costs, which aren't as obvious as a pile of materials.

For a service business, variable costs are often things like:

- The hours a consultant works on a specific client project.

- Commissions paid to a salesperson for getting a new client.

- Software costs that are billed per user and are tied directly to serving a client.

By calculating the margin for each service you offer or even each client you have, you can quickly see which services are your real money-makers and which ones are using up your time for very little return.

Feeling like it's a lot to connect these numbers to your own business? You don't have to do it alone. The team at MyOfficeOps is great at turning financial numbers into clear, simple advice for businesses like yours. Schedule your free discovery call today and start making decisions with confidence.