You're trying to make a normal business decision. Maybe it's hiring another project manager, buying equipment, or finally raising prices. You open QuickBooks or Xero and the numbers don't answer the question.

Revenue looks busy, but cash feels tight. One service line seems profitable, but you're not sure if payroll, software, and overhead are sitting in the right place. You have data everywhere and confidence nowhere.

That's the problem the month-end close is supposed to solve.

A lot of owners think of it as bookkeeping cleanup. It isn't. It's the process that turns a month of receipts, invoices, payroll runs, bill payments, and bank activity into financial statements you can trust. When the close is weak, you're driving with a foggy windshield. When it's done well, you can see what happened, what changed, and what needs attention next.

More Than Just Closing the Books

I see the same pattern all the time with small and midsize businesses. The owner works hard, sales are moving, customers are paying, and the company looks healthy from the outside. Then a simple question comes up, like “Can we afford this hire?” and nobody can answer it cleanly.

The issue usually isn't effort. It's that the books haven't been fully closed for the month, so the numbers are still half raw and half guessed.

A construction company might have cash going out for materials, payroll, fuel, and subcontractors, but not all vendor bills are entered yet. A medical practice may have deposits in the bank, but insurance receivables haven't been tied out. A professional services firm may show strong revenue, but payroll accruals and prepaid software costs haven't been adjusted yet. On paper, each business has “financials.” In practice, they have drafts.

What owners are really asking for

Most owners don't wake up asking, “Has the balance sheet been reconciled?”

They ask things like:

- Can I hire now or should I wait

- Why is profit up but cash is down

- Which customer or service line is making money

- Are we clean enough to show these numbers to a bank or buyer

Those are fair questions. But you can't get solid answers from messy books.

A good month-end close doesn't just organize the past month. It gives management a clean starting point for the next decision.

According to Ramp's explanation of the month-end close process, the close is foundational because it turns raw transactions into the three core financial statements after reconciling bank, AR, AP, payroll, and balance-sheet accounts and posting adjustments like accruals and depreciation. That documented cutoff between periods is what lets management rely on the numbers.

Why this feels harder than it should

Small businesses often don't have a full accounting department. One person may handle billing, payables, payroll support, and reporting. That's why the close often gets pushed aside until the end of the month, then the end of the next month, then “we'll clean it up at quarter end.”

That approach works right up until it doesn't.

If you want accurate reporting, stronger cash control, and a business that's easier to finance or sell, month-end close isn't optional. It's the habit that makes the rest of your financial reporting useful.

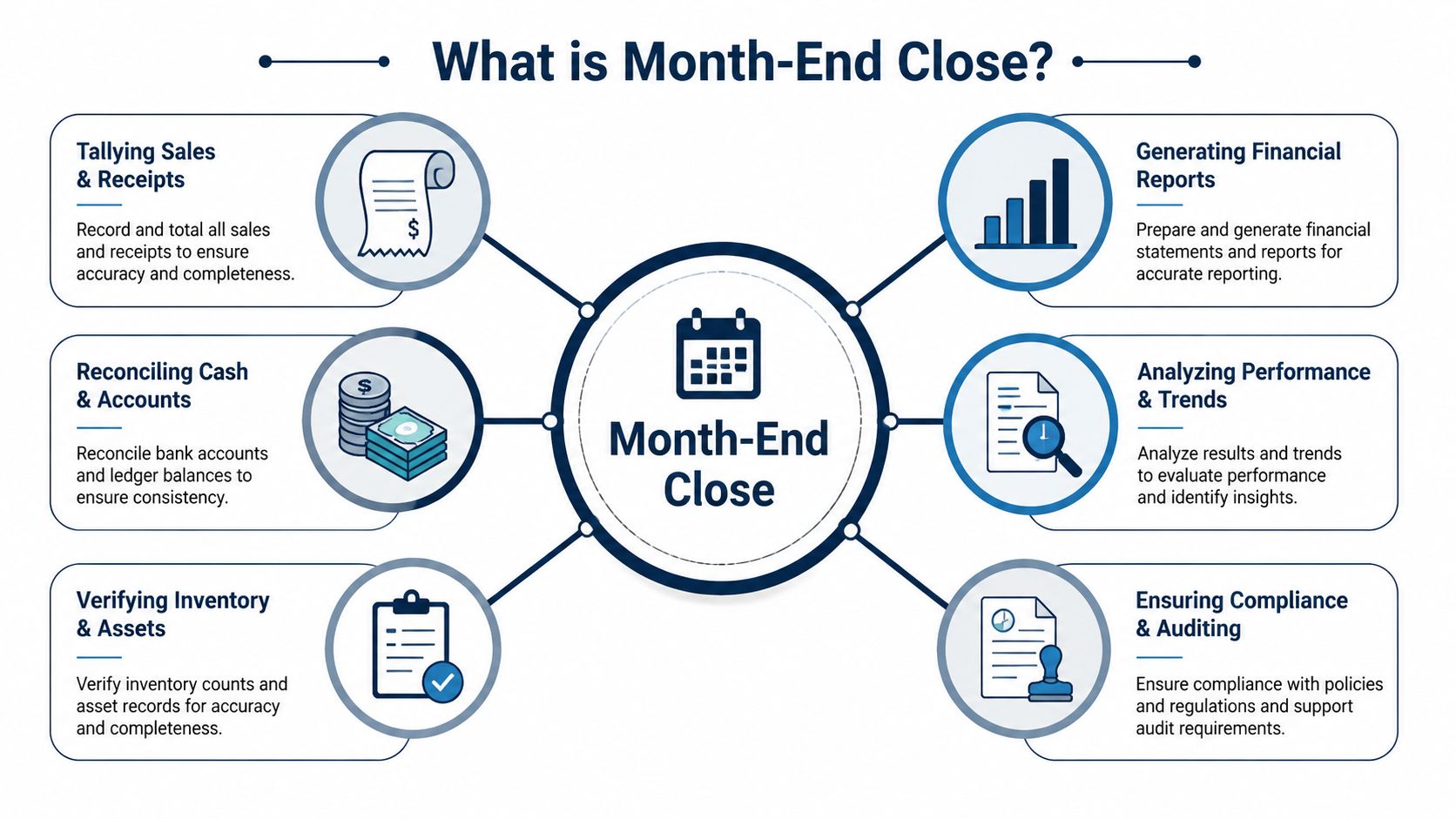

So What Is a Month End Close Really

Think of your business like a restaurant kitchen at the end of the night. Nobody just turns off the lights and leaves. The team counts receipts, checks the cash drawer, sees what inventory was used, throws out what doesn't belong, and resets the station for tomorrow.

Your accounting team has to do the same thing each month.

The month-end close is the process of reviewing, verifying, and finalizing the prior month's financial activity so your books reflect what happened in that period and nothing else.

What comes out of the close

If someone asks what is month end close, the simplest answer is this. It's the work required to produce three reports you can trust:

- Income statement. Did the business make money that month?

- Balance sheet. What does the business own and owe at month end?

- Cash flow statement. Where did the cash come from and where did it go?

Those reports only matter if the underlying records are complete. That means reconciling bank accounts, reviewing accounts receivable and accounts payable, recording payroll correctly, and posting adjustments like accruals and depreciation.

If you need a more technical walk-through of the sequence, this overview of financial closing procedures is a helpful reference because it shows how the pieces fit together in a practical close cycle.

Why the cutoff matters

A clean close creates a hard line between one month and the next. Without that line, expenses drift into the wrong month, late invoices pollute current results, and your reports stop being comparable.

That's also why accrual accounting matters here. If you're still sorting out the basics, this plain-English guide to what accrual accounting means helps connect the idea. The close depends on recording activity when it belongs, not just when cash moves.

Practical rule: If one month's activity is leaking into the next, your reports may look polished, but they're not decision-grade.

HighRadius describes the close as a control point in the accounting cycle, where finance teams collect, verify, reconcile, and then lock transactions from the prior month so the general ledger can support accurate statements and management reporting. Their summary of the month-end close process gets that point right. The close is where raw activity becomes a final snapshot of performance.

What it is not

Month-end close is not just checking whether the bank balance matches the ledger.

It's also not a rushed PDF package sent to the owner with no review, no commentary, and no confidence behind it.

A real close ends with management review and sign-off. That tells everyone in the business, “This month is complete. We can use these numbers.”

Why a Clean Close Process Is Your Secret Weapon

Most owners treat the close like compliance. Something the accountant wants. Something the bank may ask for. Something that has to be done before tax season gets annoying.

That mindset leaves a lot of value on the table.

A clean close gives you reliable information for pricing, hiring, spending, and cash planning. More importantly, it tells outside parties that your business is under control.

Better decisions start with trusted numbers

Owners usually know when the books feel off. They hesitate before making commitments. They keep extra cash in reserve because they don't fully trust the reports. They delay decisions because they're waiting for “clean numbers.”

That hesitation is expensive.

When the close is disciplined, your financial statements stop being historical clutter and start becoming a management tool. You can compare one month to the last one. You can spot gross margin shifts. You can see whether higher sales improved cash or just created more receivables.

Buyers and investors look for this fast

A sloppy close doesn't stay hidden for long. It shows up during due diligence.

According to a 2025 report discussed by MyOfficeOps on choosing the right accountant in Philadelphia, 42% of failed due diligence processes for small business sales were attributed to close process inconsistencies or unreconciled period-end data that obscured true cash flow. The same source notes that buyers in the Greater Philadelphia market, especially in professional services and healthcare, increasingly want clean-close audits as a condition for 30-50% higher acquisition multiples.

That gets to the core point. A month-end close is not only an accounting exercise. It's part of your valuation story.

If a buyer can't trust your monthly numbers, they won't trust your earnings. If they won't trust your earnings, they won't pay full value.

Where the real trade-off sits

Some owners want speed. Others want accuracy. The right answer is both, but accuracy comes first.

A fast close with weak reconciliations just means you made mistakes quickly. On the other hand, a close that drags on for weeks loses most of its management value because the numbers arrive too late to guide anything.

A clean close helps in three ways:

- Operationally. You can make monthly decisions with less guessing.

- Financially. You get a clearer view of profit, obligations, and cash pressure.

- Strategically. You're far more prepared for financing, diligence, and eventual sale discussions.

That's why I call it a secret weapon. It doesn't look exciting from the outside. But it profoundly affects how you run the company and what the company is worth.

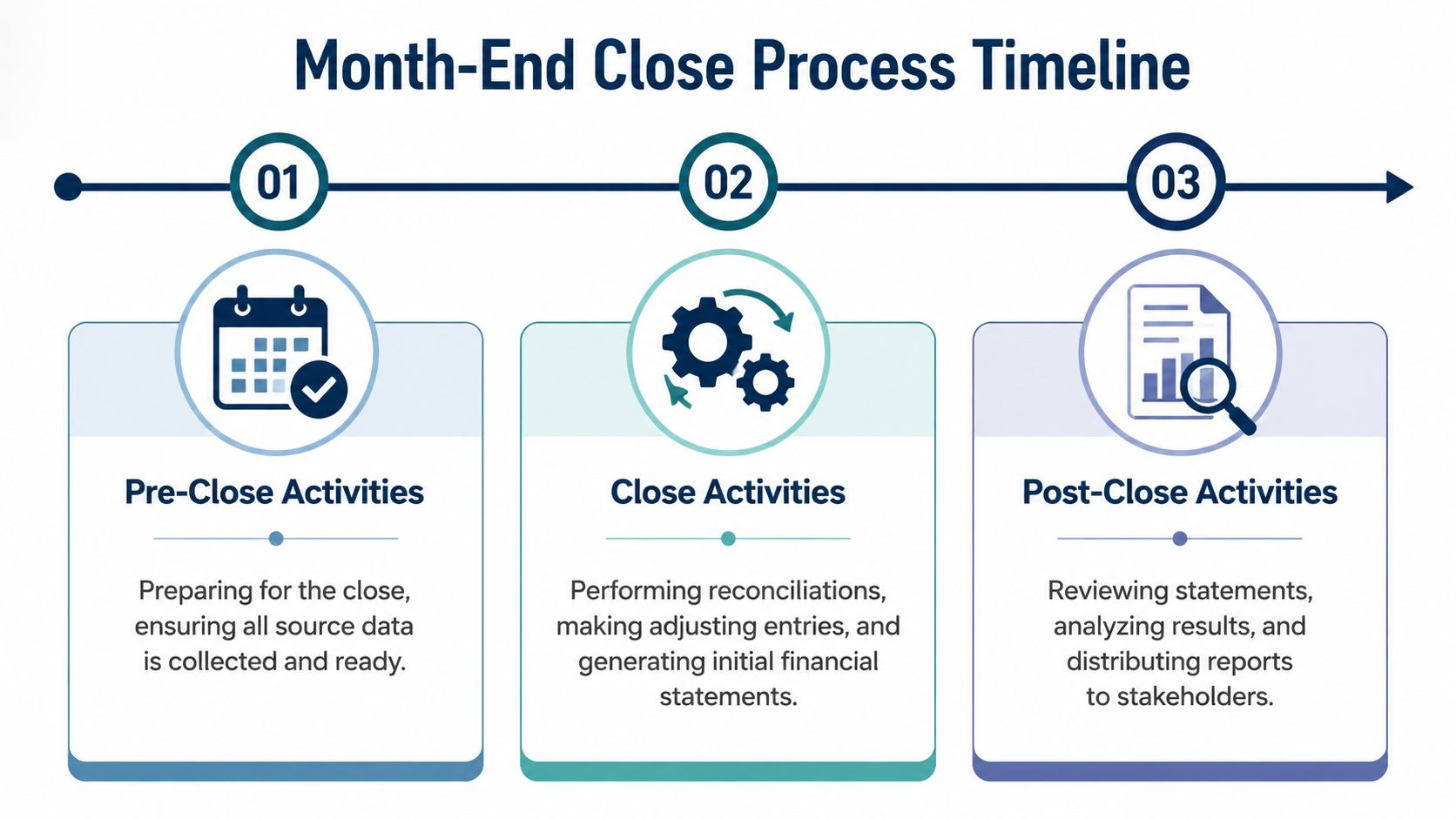

A Practical Month End Close Process Timeline

Owners often picture the close as something that happens on the last day of the month. That's not how it works in practice. A good close follows a sequence.

The exact timing varies by business, but the pattern is usually the same. First, clean up the high-volume accounts. Then post the adjustments. Then review, lock, and report.

Days 1 to 3 clean the transaction flow

The team closes the sub-ledgers and makes sure the basic transaction activity is complete.

That usually includes:

- Cash activity. Record all bank and credit card transactions, then reconcile each account to the statement.

- Accounts receivable. Confirm invoices were issued properly, payments were posted, and open balances make sense.

- Accounts payable. Enter vendor bills, match payments, and review what is still owed.

- Payroll and related items. Make sure payroll entries hit the ledger correctly and benefit-related items are captured.

For many businesses, this phase tells you whether the close will be smooth or painful. If the bank rec is off, AR is stale, or AP is missing bills, every step after this gets harder.

Days 4 to 7 post the real accounting entries

This is the part many owners don't see, but it matters a lot.

Accounting isn't just recording what cleared the bank. It also means recognizing what belongs in the month even if cash didn't move yet. That's where adjusting entries come in.

Common examples include:

- Accrued expenses for costs incurred but not yet billed

- Prepaid expenses that need to be spread across months

- Depreciation on equipment, vehicles, furniture, or other fixed assets

- Corrections or reclasses when items landed in the wrong account

This is also where closing entries and lock controls matter. FloQast explains in its overview of the month-end close process that temporary accounts such as revenue and expenses are closed out and reset for the next period, while permanent accounts carry forward. The same source notes that systems can lock AR, AP, and then the general ledger in sequence, which helps stop compounding errors later.

Weak period locks create a false sense of completion. If anyone can keep changing last month after reports go out, the close wasn't really finished.

Days 8 to 10 review and use the numbers

Once the books are finalized, the work shifts from accounting to management.

This is when you generate the statements, compare actual results to budget or prior months, and ask the basic questions that matter:

- Why did gross margin move?

- Why is cash lower even though sales were strong?

- Are expenses rising in a normal way or are they drifting?

- Did the business perform the way management expected?

This is the part owners usually care about most, and rightly so. But it only works if the earlier phases were done carefully.

A practical close timeline is less about speed than rhythm. The more consistent the sequence, the easier it is to spot delays, assign ownership, and improve each month.

Your Month End Close Checklist and Common Pitfalls

A checklist sounds simple, but it solves a real problem. It takes the close out of people's heads and puts it into a repeatable system.

That matters because close failures usually aren't caused by obscure accounting rules. They come from missed steps, unclear ownership, late information, and small errors nobody resolved when they first appeared.

Sample month-end close checklist

| Task Area | Specific Action | Typical Owner |

|---|---|---|

| Cash | Reconcile all bank accounts and credit cards to statements | Bookkeeper or staff accountant |

| Accounts Receivable | Review open invoices, unapplied payments, and aging issues | AR specialist or bookkeeper |

| Accounts Payable | Enter remaining vendor bills and review unpaid balances | AP specialist or bookkeeper |

| Payroll | Confirm payroll entries, taxes, and benefits posted correctly | Payroll admin or accountant |

| Accruals | Record unpaid expenses that belong in the month | Accountant or controller |

| Prepaids | Adjust items paid in advance to the proper monthly amount | Accountant |

| Fixed Assets | Record depreciation and review additions or disposals | Accountant or controller |

| Balance Sheet | Reconcile key asset, liability, and equity accounts | Accountant or controller |

| Review | Compare current month to prior month and budget | Controller, CFO, or owner |

| Finalize | Lock the period and archive support for reconciliations and entries | Controller or accounting lead |

The mistakes that slow everything down

The most common problems are usually process problems.

- Waiting until month end to start. If bank recs, invoice reviews, and bill entry all wait until the final days, the team creates its own bottleneck.

- Ignoring small differences. A minor unreconciled item today turns into a messy balance sheet next quarter.

- No clear owner. When everyone is “kind of” responsible, nobody is actually responsible.

- Spreadsheet dependence. Spreadsheets are useful, but outdated manual trackers often become error factories.

- No review layer. If nobody checks the entries and reconciliations before reports go out, bad data gets approved by default.

What works better

The best close processes are boring in a good way. Same sequence. Same owners. Same deadlines. Same review points.

A few habits make a big difference:

- Do recurring tasks during the month instead of piling them into a short window.

- Set a close calendar so every person knows what's due and when.

- Require support for material entries so nobody has to guess later.

- Review the balance sheet, not just the P&L because that's where hidden issues often sit.

Clean closes are built before month end. They are not rescued after month end.

If your close feels chaotic every month, don't assume your business is too complex. Most of the time, the process is just too loose.

KPIs Software and Tools for a Smoother Close

If you want to improve the close, measure it. Otherwise every month feels “busy,” but nobody knows whether the process is getting better.

The first KPI I watch is days to close. It tells you how long it takes to finalize the books after month end. The second is post-close adjustments. If you keep changing the numbers after reports go out, your process has a control problem.

What to track without overcomplicating it

A small business doesn't need a giant finance scorecard to manage the close.

Start with a short list:

- Days to close. How long until the books are finalized and reviewed?

- Number of post-close entries. How often do you reopen a period to fix missed items?

- Reconciliation completion. Were key balance sheet accounts tied out?

- Reporting timeliness. Did leadership receive usable reports while they still mattered?

If you want a cleaner way to organize financial reporting metrics, a simple KPI dashboard guide for small businesses can help you decide what to track and how to present it without drowning in data.

For industry-specific examples, restaurant operators often track a tighter set of operating and profit measures. This roundup of essential restaurant metrics for profit is a good reminder that financial reporting works best when it connects to day-to-day operations.

The real software choice for SMBs

A lot of small businesses think they have two options. Stay manual forever, or buy a huge enterprise system they don't need and can't afford.

That's not true anymore.

According to a 2025 SMB Technology Survey covered by MyOfficeOps, 68% of SMBs in the Philadelphia construction and trade sectors fail to close their books within 7 days due to manual data entry, while 74% say they cannot afford the $50,000+ implementation costs of traditional enterprise automations. The same source points to the rise of low-code, API-first accounting connectors that tie together platforms like QuickBooks and Xero at a fraction of the cost.

That middle ground is where many growing companies should look first.

What usually works

For most SMBs, the stack is not fancy. It's practical.

- Core ledger. QuickBooks Online or Xero

- Payroll platform integrated to the ledger

- Bank and credit card feeds connected correctly

- Bill pay and expense tools that reduce manual entry

- Close tracking and reporting tools that make ownership visible

One practical option in that mix is MyOfficeOps, which handles bookkeeping, reporting, payroll integration, analytics, and CFO-level advisory for small and midsize businesses that need a cleaner monthly close without building a full in-house finance team.

What usually does not work is trying to patch a broken process with more spreadsheets. Software helps when it removes manual re-entry, improves visibility, and enforces review. It doesn't help when it adds complexity without fixing ownership.

When to Do It Yourself vs Hiring a Partner

For a very small business with a low transaction count, DIY can work. If you have simple operations, one bank account, limited accruals, and enough time to review the books carefully each month, you may be able to manage the close internally.

But growth changes the math fast.

More customers, more vendors, more payroll complexity, and more systems mean the close starts pulling real time away from sales, operations, and leadership. At that point, the question isn't whether you can do it yourself. It's whether you should.

A simple way to decide

DIY is usually still reasonable when:

- Transactions are limited

- You understand your reports

- The books are current

- You're not preparing for financing, diligence, or a sale

A partner makes more sense when:

- The close keeps slipping

- Cash surprises are becoming common

- You need cleaner reporting for lenders, investors, or buyers

- You want analysis, not just data entry

Hiring internally can solve the problem, but a full-time controller or senior accounting hire is expensive and still needs process design, tools, and oversight. That's why many owners use outsourced support instead. If you're weighing that route, this guide on the advantages of outsourcing bookkeeping services gives a practical view of when it makes sense.

There's also a broader point here. Once your books are clean and your close is reliable, you can make better use of specialized advisors in other areas too. For example, companies doing product or technical development may also look at Expert R&D tax claim advisors when they want support beyond day-to-day accounting.

The right partner shouldn't just close your books. They should help you trust the numbers, explain what changed, and make the reporting usable for decisions.

If your month-end close still feels like a scramble, MyOfficeOps can help you build a process that's clear, consistent, and useful. The team supports small and midsize businesses with bookkeeping, payroll integration, financial reporting, KPI dashboards, and CFO-level guidance so you can stop guessing and start managing from clean numbers.