To understand a cash flow statement, you need to look at its three main parts: cash from operations, cash from investing, and cash from financing. Think of them as three different stories that, when put together, show you where your money is really coming from and where it’s going. This helps you know if your business has the cash to survive and grow.

What a Cash Flow Statement Actually Tells You

Forget about complicated accounting words for a second. Your cash flow statement is like a video replay of your business bank account. It shows you exactly how much money came in and how much went out over a certain time, like a month or a quarter. That's it.

This is very different from an income statement (also called a P&L). I've seen lots of business owners get confused because their income statement showed a big profit, but their bank account was almost empty. This can happen if you sell something to a customer who promises to pay you later. The sale counts as profit right away, but you don't have the cash until the customer actually pays you.

The cash flow statement shows you the real cash you have on hand.

Key Takeaway: There's an old saying in business: profit is an opinion, but cash is a fact. The cash flow statement is all about the facts—the actual cash moving in and out of your business.

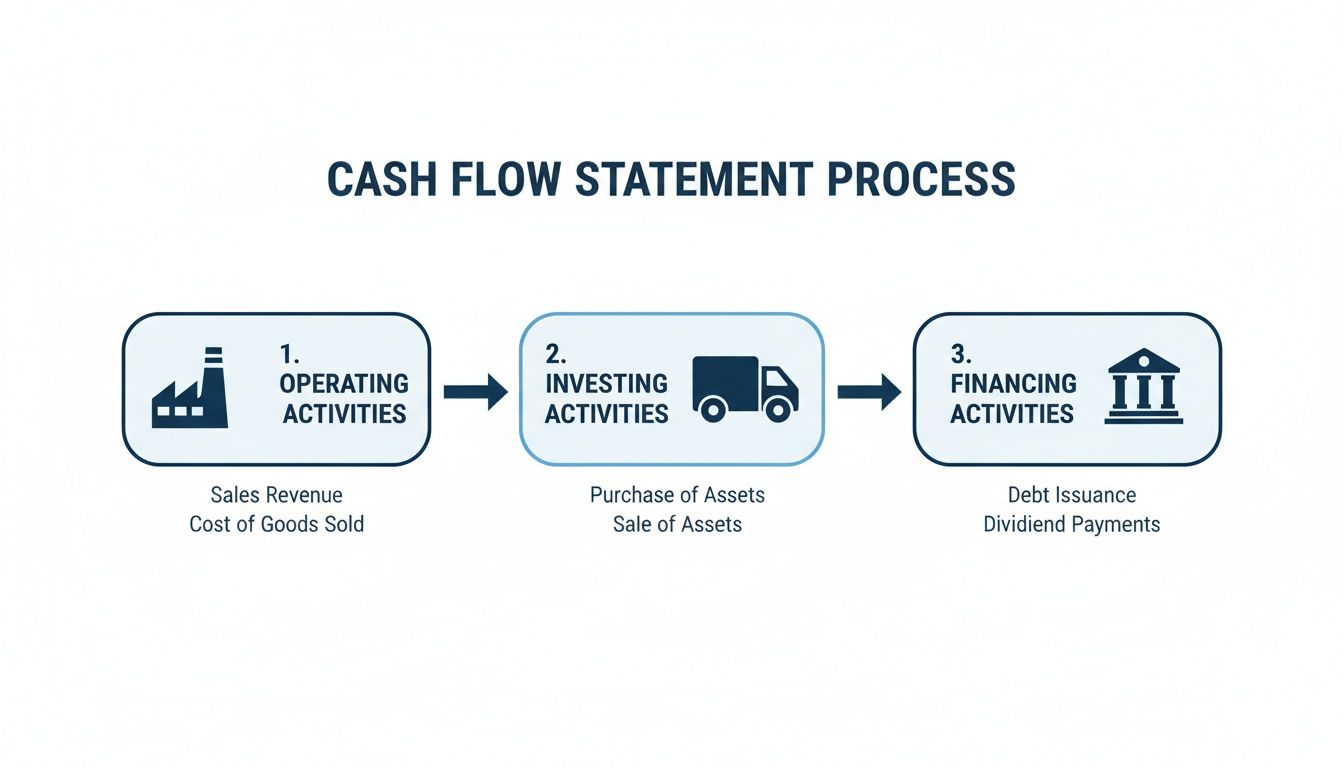

The Three Core Stories in Your Statement

Every cash flow statement is split into three sections. Each one tells a different, important story about your money. Understanding these three parts is the first step.

Here’s a quick look at what each section shows.

The Three Sections of a Cash Flow Statement

| Section | What It Shows You | A Simple Example |

|---|---|---|

| Operating Activities | Cash from your main business, like selling things or providing services. This is your business's engine. | Money you get from customers, minus money you pay for rent, employee salaries, and supplies. |

| Investing Activities | Cash you use to buy or sell big, long-lasting things for your business. This shows how you're planning for the future. | Buying a new computer or company car; selling an old piece of equipment. |

| Financing Activities | Cash from owners and banks. This shows how you get money for your business besides just selling things. | Getting a loan from a bank, an owner putting their own money into the business, or paying back a loan. |

Let's dive into what each of these really means.

H3: Operating Activities

This is the most important part. It shows if your main business can make enough cash on its own. If this number is positive, it’s a good sign that your business is healthy and can stand on its own two feet.

H3: Investing Activities

This section shows money you spent on or got from big, long-term items called assets. Did you buy a new delivery truck? Sell old furniture? You’ll see that here. It tells you how you're investing in your company's future.

H3: Financing Activities

This part covers money from owners or lenders like a bank. It includes things like getting a new loan, an owner adding more money to the business, or making loan payments. This shows how you're funding the company when your sales aren't enough or when you're getting ready to grow.

Together, these three sections give you a full picture of your cash. They work with other financial reports, which you can learn about in our guide on how to read a balance sheet. At the end of the day, this statement is a health check-up that shows if you have the cash to pay your bills, your team, and grow your business.

Unpacking Cash From Operating Activities

This is the most important section of your cash flow statement. Why? Because it tells you if your main business can actually make its own cash. I've seen companies look profitable on paper but go out of business because they couldn't pay their bills. This is where you see that problem first. It’s like the engine room of your business.

The calculation starts with net income, which is the "profit" from your income statement. Then, it makes some changes to connect that paper profit to the real cash in your bank. It's like translating a story from one language to another.

For a long time, this was a confusing part of financial reports. But in 1988, a new rule made companies show their cash flow more clearly. Even before that, smart companies were already focusing on cash. In 1980, only 10% of the biggest companies focused on cash, but by 1985, that number jumped to 70%.

This simple chart shows how the three main activities—operating, investing, and financing—fit together to tell your company's full cash story.

As you can see, operating activities are the base. They show the cash your everyday business makes before you even think about buying big things or getting loans.

Adjusting for Non-Cash Items

One of the first things you'll see is a change made for "non-cash expenses." The most common example is depreciation. Let’s say you bought a work truck for $30,000. Your accountant might say that the truck lost $6,000 of its value this year. That is depreciation.

This $6,000 lowers your profit on paper, which is good for taxes. But did you actually spend $6,000 in cash this year for depreciation? No. The cash was spent when you first bought the truck.

Because no cash went out for depreciation this year, we add that $6,000 back to the net income on the cash flow statement. It’s a paper expense, not a cash expense.

The Two Methods: Indirect vs. Direct

Most businesses—and probably yours too—use the indirect method for this section. This is what we've been talking about: you start with net income and make changes. It's popular because it's easier to create from your income statement and balance sheet.

The direct method, on the other hand, just lists all the cash that came in and went out from your operations.

- Cash from customers

- Cash paid to suppliers

- Cash paid for salaries

It’s more like looking at your bank statement. It's very clear, but it’s a lot more work to put together. That's why most companies use the indirect method.

My Personal Tip: Don't worry too much about which method is used. The final number—Net Cash From Operating Activities—is the same both ways. The indirect method is useful because it shows you why your profit and your cash are different, which is super helpful for a business owner.

Changes in Working Capital

This is where many business owners have a "lightbulb" moment. This part of the statement looks at changes in things like money customers owe you (accounts receivable), stuff you plan to sell (inventory), and bills you need to pay (accounts payable).

Good cash flow from operations is usually a sign that your business is running well. Learning how to streamline business processes can make a big difference to these numbers.

Let’s look at a real-life example.

Example: The Service Business Cash Crunch

Imagine you run a marketing company. You had a great quarter and sent bills to clients for $50,000. Your income statement shows a nice profit.

But here’s the problem: your clients have 60 days to pay you. That $50,000 is now called accounts receivable—it’s money customers owe you. It's your money, but it's not in your bank account yet.

- When your accounts receivable goes up, it means you made sales but haven't gotten the cash yet.

- On the cash flow statement, an increase in accounts receivable is shown as a decrease in cash.

This is how a "profitable" business can suddenly have no cash and struggle to pay its bills. The profit is on paper, but the cash isn't there. Your cash flow statement makes this problem impossible to miss.

Here’s another common one:

Inventory: The Cash Sitting on Your Shelf

If you run a store or a construction business, you have to buy stuff—like products or lumber—before you can sell it.

Let's say you spend $20,000 on new inventory. That cash is gone from your bank, but it's not an "expense" on your income statement until you sell those items. For now, that cash is just sitting on your shelves.

- An increase in inventory means you spent cash on goods that you haven't sold yet.

- On the cash flow statement, this shows up as a decrease in cash.

On the other hand, an increase in accounts payable (money you owe to your suppliers) actually increases your cash for that period. You got stuff but haven't paid for it yet, so you get to hold onto your cash a little longer. It’s like getting a short, interest-free loan from your suppliers.

Understanding these changes is the key to reading a cash flow statement. It clearly shows the important difference between making a sale and actually getting paid.

Making Sense of Investing and Financing Activities

Once you get how your operating cash flow works, the next two parts are much easier. These sections, investing and financing activities, tell the story of your business's big plans—how you're building for the future and how you're paying for it.

Think of it like this: operating activities are about the daily work. Investing and financing are about the big moves you make to grow or just get through a tough time.

Cash From Investing Activities: What It Really Means

This section is all about your long-term assets. It’s where you see the cash you spent on big things that will help your business for years. It’s also where you see cash you got from selling those same kinds of things.

Here are a few real-world examples of investing activities:

- Buying new equipment: Did your construction company just buy a new excavator for $80,000? That’s a cash outflow (a negative number) you'll see here.

- Purchasing a company vehicle: If your catering business bought a new delivery van, the cash you paid shows up here.

- Selling old assets: Did you sell old office computers for $1,500? That’s a cash inflow (a positive number) from investing.

A negative number here is not always bad. In fact, a negative number from investing often means you are putting money back into your business to grow. It shows you're buying the tools and technology you need to do more in the future.

My Personal Tip: If a business always has positive cash flow from investing, it might be in trouble. It could mean they are selling off their equipment just to get cash to pay for daily bills—a plan that won't work for long.

Cash From Financing Activities: Where the Money Comes From

The financing section is all about how you get money for your business besides what you earn from customers. It tracks cash between your business, its owners, and its lenders. For any small business owner, this is a key part of learning how to read a cash flow statement.

This section shows you how much you depend on outside money.

Cash Inflows From Financing

These are activities that bring cash into your business from other places.

- Taking out a bank loan: If you get a $50,000 business loan, you'll see a $50,000 cash inflow here.

- Owner contributions: When you, the owner, put $10,000 of your own money into the business, that's a financing inflow.

- Issuing stock: If your company sells shares to investors, the cash from those sales shows up here.

Cash Outflows From Financing

These are cash payments related to your funding.

- Repaying loan principal: The part of your loan payment that pays down the actual loan amount is a cash outflow here. (The interest part is an operating activity).

- Owner draws or dividends: When you take money out of the business for yourself, that cash withdrawal is a financing outflow.

- Share buybacks: If you use company cash to buy back shares from investors, that's also a cash-out activity.

Understanding this section helps you answer a key question: Is your business funded by debt, by its owners, or by its own success? A new startup might have a huge positive number here after getting money from investors. A stable business might have a negative number as it pays down its debts. Both can be healthy, depending on the company's goals.

How to Spot Financial Red Flags

Think of your cash flow statement as an early warning system. I've seen it many times: one bad month isn't a big deal, but patterns of bad numbers can signal trouble way before your profit and loss statement shows it. Learning to read your cash flow statement is really about learning to spot these warnings early.

Catching these problems early gives you time to fix them. That could mean calling customers who owe you money, not making a big purchase, or finding a better way to handle your loans.

Consistently Negative Operating Cash Flow

This is the big one. It's like a flashing red light. If your operating cash flow is negative month after month, it means your main business is spending more cash than it brings in.

Your business can't survive if its main job—selling things or services—is always losing cash.

Sure, you might have one bad month. Maybe you spent a lot on ads or bought extra inventory for a busy season. But if you see negative numbers for a whole quarter or more, it’s time to investigate. It's a clear sign that your business plan isn't working as it should.

High Profit but Low Operating Cash

This is a classic problem for business owners. Your income statement looks great, showing big profits, but your bank account is almost empty. What’s going on?

This almost always points to a problem with working capital. The profit is on paper, but the real cash is stuck somewhere else. The most common reasons are:

- Slow-paying customers (High Accounts Receivable): You made sales, and they look good on your P&L. But your customers haven't paid you yet. The cash flow statement shows the hard truth: the money isn't in your bank.

- Too much cash tied up in inventory: You spent real cash on products that are now just sitting on a shelf. That cash is gone, but it won't show up as an "expense" on your income statement until you sell the items.

If you see this difference between profit and cash, the first place to look is your accounts receivable. Are customers taking longer and longer to pay? It might be time to be more direct about collecting your money. From there, you'll want to explore ways to improve working capital in your whole business.

Relying on Financing to Cover Operations

Look at your financing activities section. Are you regularly taking out loans or using a line of credit (a positive financing cash flow) just to pay your employees and rent (a negative operating cash flow)? This is a huge red flag.

It’s like using a credit card to pay your mortgage. It fixes the problem for a moment, but it’s not a good long-term plan. You're just getting into more debt to cover your daily costs.

Key Insight: A healthy business pays its daily bills with cash from its customers, not from its lenders. You should use loans for big purchases that will help you grow, not to fix leaks in your day-to-day operations.

A brand-new startup will probably use financing to get started, and that's normal. But for a business that's been around for a while, this is a sign of a serious problem that needs to be fixed.

Selling Assets to Generate Cash

Do you see a pattern of positive cash flow from your investing activities? Getting cash might seem good, but if it happens too often, it can be a very bad sign.

This usually means the business is selling its long-term assets—like equipment, trucks, or property—just to get cash for today.

Why is this a problem? You might be selling the very tools you need to run your business and make money in the future. Selling one old, unused machine is fine. But if it becomes a regular thing, it’s like selling your furniture to pay the power bill. You’re giving up your future to survive today.

Here's a quick checklist to help you look for these red flags on your own statement.

Quick Red Flag Checklist

- Is Net Cash from Operating Activities negative again and again?

- Is your Net Income high while your operating cash is low or negative?

- Is the amount of money customers owe you (Accounts Receivable) growing much faster than your sales?

- Are you often using cash from Financing Activities (like new loans) while your operating cash is negative?

- Are you regularly getting cash by selling assets in the Investing Activities section?

Answering "yes" to any of these questions doesn't mean your business is failing. It means you've used the cash flow statement correctly: to find problems that need your attention. Now you know where to look and what to fix.

Connecting the Dots with Real Business Examples

Okay, talking about the ideas is one thing, but it really makes sense when you see how the numbers tell a story. Reading about operating, investing, and financing is fine, but seeing how they work in real businesses is where it all clicks.

I’ve found that going through a few common situations is the best way to get comfortable reading your own statement. We'll look at three different small businesses—a marketing agency, a medical practice, and a construction company—to see how their businesses create very different cash flow stories.

Example 1: The Marketing Agency and the Cash Flow Lag

Imagine you run a local marketing agency. Business is great. You just got a huge new client—a $60,000 project that will take three months. Your income statement looks amazing, showing a profit of $20,000 this month alone. You feel like you're on top of the world.

But when you get your cash flow statement, your stomach drops a little. The "Net Cash from Operating Activities" shows a negative number, a cash outflow of -$5,000.

How is that possible? You’re profitable!

This is the classic cash flow problem that trips up so many service businesses. The problem is hidden in your payment terms. Your big new client pays you in 90 days. So while you’ve earned the money, you haven’t received the cash.

Here’s a simple look at how this shows up on your cash flow statement (using the indirect method):

| Cash Flow from Operating Activities | Amount |

|---|---|

| Net Income | $20,000 |

| Adjustments: | |

| Increase in Accounts Receivable | ($25,000) |

| Net Cash from Operating Activities | ($5,000) |

That $25,000 increase in Accounts Receivable is the money you're waiting for. Since that cash isn't in your bank, we have to subtract it from your net income to see what really happened with your cash.

This one line tells an important story. Your business is healthy on paper, but you could have a cash problem soon if you don't manage your payments well. This is your sign to maybe offer a discount for paying early or start sending friendly reminders after 30 days, not 90.

Example 2: The Medical Practice and Strategic Investment

Now let's look at a small, growing medical practice. The doctors decide it's time to upgrade their tools by buying a new X-ray machine for $150,000. They don't have that much cash, so they get a loan from the bank to buy it.

This one decision affects two different parts of their cash flow statement.

First, under Investing Activities, you’ll see this:

- Purchase of Equipment: ($150,000)

This is a cash outflow. The business spent cash to buy a long-term asset that will help it make money for years. Seeing a big negative number here isn't always bad—it often means the business is investing in its future.

But where did that $150,000 come from? The answer is in the Financing Activities section:

- Proceeds from Long-Term Debt: $150,000

This is a cash inflow. The bank gave the practice the cash to buy the machine.

Key Takeaway: When you look at the whole statement, these two numbers cancel each other out for the total cash balance. The business spent $150,000 on the purchase (investing outflow) but got $150,000 from the loan (financing inflow). The real story is about the plan—using a loan to buy something that will help the business grow.

Example 3: The Construction Company and the Inventory Crunch

Finally, let’s look at a small construction company. It’s early spring, and they’re getting ready for a busy summer. They just got two big home-building jobs that will start next month. To get ready, they spend $75,000 on lumber, windows, and other materials.

They're all booked up and should be happy, but the owner is worried about paying his employees. The cash flow statement shows why.

Even though they haven't started getting paid for the big jobs yet, they've already spent a lot of cash. This shows up under Operating Activities.

A Look at the Contractor's Operations

- Increase in Inventory: ($75,000)

This is a huge cash outflow. That $75,000 is gone from their bank account. It's now sitting in a lumberyard and on their books as inventory. It won't be counted as a cost on the income statement until the jobs are started and the materials are used.

This creates a serious cash problem. They have to pay their employees and their regular bills for the next month before they get their first payment from the new jobs. This is a common problem for contractors, stores, and any business that has to buy things before selling them.

Seeing this on the cash flow statement is a signal. It might make the owner:

- Ask for better payment terms with his suppliers so he can pay them later.

- Ask for a deposit from his clients to pay for materials up front.

- Get a line of credit to help get through these temporary cash shortages.

These three examples show that learning how to read a cash flow statement isn't just for accountants. It’s a live look at your business's health, showing you the story behind the numbers and where you need to take action.

Answering Your Top Cash Flow Questions

Once you start getting used to your cash flow statement, you're going to have questions. This is a great sign! It means you're starting to think about what the numbers mean for your business.

Over the years, I've found that most business owners end up asking the same few questions. Getting these answers will help you take what you've learned and use it to make smart moves.

How Often Should I Review My Cash Flow Statement?

For most small businesses, looking at your cash flow statement monthly is perfect. It’s often enough to see new trends—like customers paying you more slowly—without getting lost in tiny, daily changes.

But there are times you might want to check it more often. If your business is seasonal, like a snow-plowing company, checking it weekly during your busy season is a good idea. The same goes for any business that is growing very fast. When things are moving that quickly, you need to watch your cash very closely.

Why Is My Profit High but My Cash Is Low?

This is the most common—and most important—question I get asked. It’s a familiar story: your income statement says you had a great, profitable month, but when you check your bank account, the balance is low.

The answer is almost always about timing. Your income statement counts money when you earn it, not when you actually get paid.

The Simple Explanation: If you sent out a lot of bills at the end of the month, your profit looks great on paper. But that cash is still in your customers' bank accounts, not yours. This money is called accounts receivable, and it’s the number one reason for the difference between profit and cash.

This gap can also happen if you spent a lot of cash on things that aren't counted as an expense right away, like buying a lot of inventory that you haven't sold yet.

What Should I Do First if I See a Problem?

If you see you’re losing cash from your main operations, the first step is to figure out why, not to panic. The very first place I tell business owners to look is their accounts receivable.

Are your customers taking longer to pay you? Your statement will show this as an "increase in accounts receivable." If that's the problem, it's time to be more active in collecting your money. You could try:

- Sending payment reminders sooner and more often.

- Offering a small discount (like 2%) for paying early.

- Making a phone call for large, late payments. A direct conversation often works best.

The goal is to shorten the time it takes to get cash in your hands after you make a sale. For a deeper look into planning for these situations, our cash flow forecasting template can be a big help. It’s all about seeing these problems coming before they become emergencies.

Feeling overwhelmed trying to connect the dots between your profit and your cash? You’re not alone. At MyOfficeOps, we help business owners move beyond the numbers and find the story they tell. We provide clear, jargon-free reports and CFO-level advice to help you manage your cash flow, improve profitability, and focus on growth. Schedule your free discovery call today.