Imagine a client pays you $12,000 today for a full year of your company's service. Your bank account looks great, but let me ask you: have you actually earned that money?

From an accounting standpoint, the answer is no. This is the main idea behind deferred revenue, which is just money you've received for work you haven't done yet.

What Is Deferred Revenue in Simple Terms?

Let's stick with that $12,000 payment. It feels good seeing that cash in your account, but you've just made a promise. You owe your client a whole year of service, and until you deliver on that promise, month by month, the money isn't really yours to count as income.

Think of it like selling a gift card. A customer gives you $100 for a gift card. You have their money, but you haven't earned it. You still owe them $100 worth of products from your store. That $100 is a liability—a promise you must keep.

Deferred revenue works the same way. It's an obligation, not income yet.

A Promise on Your Balance Sheet

In accounting, this advance payment is called unearned revenue, and we record it as a liability on your balance sheet. This isn't a bad thing; it's just a way to show you have a promise to a customer.

This practice is a key part of the revenue recognition principle, a basic rule in accounting. The rule says you should only record revenue when you’ve earned it by delivering the goods or providing the services.

Getting this right gives you a true picture of your company’s financial health. You can see how this fits into the bigger picture in our guide on accrual accounting.

This table breaks down the difference between getting paid and counting the money as yours.

Cash Received vs Revenue Earned at a Glance

| Event | Impact on Cash | Impact on Revenue | What It Means for You |

|---|---|---|---|

| Client Pays Upfront | Increases | No Change | You have the money, but you also have an obligation. |

| You Deliver the Service | No Change | Increases | You've kept your promise and can now recognize the income. |

Understanding this difference is important. If you mix up cash and revenue, it's easy to think your business is more profitable than it really is.

Tracking deferred revenue keeps you from making decisions based on a full bank account. It helps you build your financial plan on an honest, accurate view of your business.

Why Managing Deferred Revenue Is So Important

If you get deferred revenue wrong, you can trick yourself into thinking your business is doing better than it is. That big check from a new client feels great—it can make you feel rich, leading to some risky spending decisions. You might think, "Wow, we can finally afford that new equipment or hire another person!"

But that cash comes with a promise—to do the work. If you treat it all as income right away, you're not seeing the real picture of your company's financial health. You’re spending money you haven’t earned yet, which can cause big problems later.

The Danger of a Misleading Bank Account

Imagine you're a contractor, and a client pays you a $50,000 deposit for a project that will take four months. Your bank account looks amazing, but that money has to cover all your materials, labor, and other costs over the whole project.

If you record that whole $50,000 as revenue on day one, you've created a false sense of security. It’s a common trap that hides future money problems and leads to a scramble when bills are due in month three and you’ve already spent the deposit. Getting this right prevents these kinds of bad decisions.

Managing advance payments gives you an honest look at your financial health and future commitments. It's the difference between flying blind and having a clear flight plan for your business.

A Clearer View of Your Business Health

When you handle your deferred revenue the right way, you get three big advantages:

- Honest Profitability: You see how much you’re actually earning each month, not just the cash you’ve collected. This gives you a true measure of your company’s performance.

- Smarter Budgeting: Knowing your real revenue helps you make better decisions about spending. You can invest in growth without risking overspending based on unearned cash.

- Predictable Cash Flow: You can map out your future promises and the revenue you’ll recognize from them. This helps you forecast your financial position more accurately, which is key for steady growth. To learn more, our guide on understanding cash flow statements is a great next step.

Ultimately, getting this right isn't just about following accounting rules. It's about building a solid business based on reality, not a temporarily full bank account. It helps you plan for the future with confidence because you have a clear, accurate picture of your commitments and what you're truly earning.

Real-World Examples of Deferred Revenue in Action

Okay, the term “deferred revenue” might sound like accounting homework, but I promise, you see it in action every day. Let's look at a few simple stories to make it real. Seeing how the money flows in real businesses makes it much easier to understand.

This isn't some strange rule, either. It’s a huge part of the economy, especially with so many subscription businesses. At one point, deferred revenue made up over 25% of current liabilities for major software companies. That shows you just how much cash is collected before the work is done.

Example 1: The Software Subscription

Let’s start with a classic. Imagine a small software company, "CodeCo," that sells an annual license for its project management tool. The price is $1,200, and on January 1st, a new customer pays for the whole year upfront.

Great news for CodeCo’s bank account, which now has $1,200 more. But here’s the catch: they haven’t earned that money yet. They owe the customer a full year of access and support.

On its books, CodeCo records the $1,200 cash and creates a matching liability called "Deferred Revenue." Each month, as they provide the service, they get to move $100 (1/12th of the total) from the deferred revenue liability over to the "Earned Revenue" line on their income statement. By the end of the year, the liability is gone and the full $12,000 has been properly counted as income.

Example 2: The Marketing Agency Retainer

Next, a marketing agency lands a new client for a three-month project. The client agrees to pay a $15,000 retainer upfront to secure their services for the quarter.

The agency has the cash, but it comes with a promise to deliver marketing campaigns and reports over the next three months. If they counted all $15,000 as revenue in the first month, their books would be very misleading.

Instead, they handle it the right way:

- Month 1: They do about one-third of the work and recognize $5,000 as revenue. The other $10,000 sits in the deferred revenue account.

- Month 2: Another month of work means they earn another $5,000. The liability is now down to $5,000.

- Month 3: They finish the project, earn the final $5,000, and the deferred revenue for this client hits zero.

This method gives a true picture of the agency's performance over time.

Example 3: The Construction Deposit

Finally, think about a construction firm hired to do a $100,000 kitchen remodel. The contract requires a 50% deposit—$50,000—before they start. This deposit is normal to lock in the job and cover the first costs for materials.

That $50,000 is pure deferred revenue. The firm has a promise to do the work, so none of that money is earned yet. It's a liability.

As the project hits key milestones—like demolition is done or cabinets are installed—the firm will recognize parts of that deposit as earned revenue. This approach makes sure their income statement accurately shows the value they’ve delivered, not just the cash they’ve collected. You can find similar real-world applications by looking at some church-focused deferred revenue income examples.

How Deferred Revenue Shows Up on Your Financials

Okay, we know deferred revenue is just a term for “money you've been paid but haven't earned yet.” But where does this promise actually show up on your books? You don't need an accounting degree to follow the money, so let's trace its path from when a customer pays you to when you finally count it as income.

Let's walk through a common situation. Say you sign a new client on a $12,000 annual retainer, and they pay you the whole thing upfront on day one. Here’s how that cash travels through your financial statements.

Step 1: When You Get Paid

The moment that $12,000 lands in your bank account, your books need to show it. First, your Cash account goes up by $12,000. But at the same time, an account called Deferred Revenue appears on your balance sheet, also for $12,000.

This is important. The Deferred Revenue account is a liability. It’s your company’s formal IOU, saying, "We have this cash, but we owe our client a full year of work before we can call it ours."

At this point, your income statement—the report that tracks your profit and loss—is untouched. Your bank balance looks great, but from an accounting view, you haven’t earned a single dollar of revenue from this deal yet.

Step 2: As You Do the Work

Now, let's jump forward one month. You’ve delivered the first month of service, so you've earned a piece of that contract. Since the agreement is for 12 months, you've earned one-twelfth of the total.

This is where the accounting happens. You’ll make an adjustment to move $1,000 (that’s $12,000 divided by 12 months) from the liability account over to your revenue account.

- Your Deferred Revenue liability on the balance sheet decreases by $1,000. It now sits at $11,000.

- Your Earned Revenue on the income statement increases by $1,000.

You repeat this exact step every month for the rest of the year. By the end of month 12, the Deferred Revenue liability will be $0, and you’ll have recognized the full $12,000 as earned income. This process is the heart of the revenue recognition principle.

For anyone running an online store, a seamless WooCommerce QuickBooks integration can handle all these monthly adjustments for you automatically, which saves time and prevents mistakes.

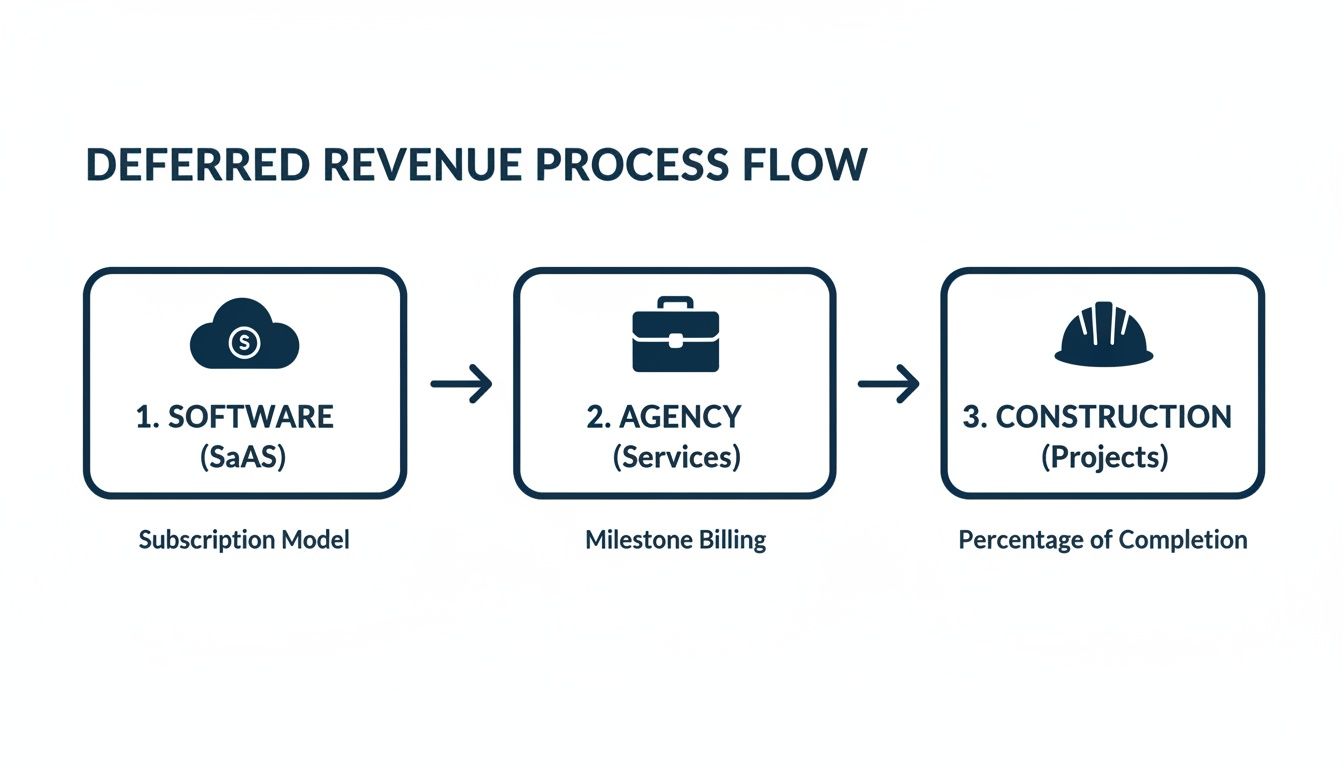

This revenue recognition flow works the same way across different businesses, as the picture below shows.

Whether you’re selling software, running an agency, or building homes, the core idea is the same: you only count revenue as you deliver the value you promised. Getting this right helps you read your own financials and trust what the numbers are telling you. You can learn more about these rules in our guide to the revenue recognition principle.

Common Deferred Revenue Mistakes and How to Avoid Them

Managing deferred revenue can feel complicated, but in my experience, most businesses run into the same few problems. Think of this as your guide for avoiding those common mistakes. If you get this right, you’ll build a financial foundation you can trust.

The single biggest mistake is also the simplest: counting all the cash you receive as immediate revenue. This is a huge mistake because it gives you a false picture of your company’s health. It creates “phantom profits” that can lead to bad spending decisions and money shortages down the road.

Another common error is forgetting to make the monthly adjustments. You might record the deferred revenue liability correctly when you get the cash, but then you get busy and don't move a portion over to earned revenue each month. This means your income statement is always understated, and your liability is always wrong.

Overpaying Taxes and Misleading Budgets

The results of these mistakes are real. If you report income before you've earned it, you could end up overpaying your taxes for that period. You’re handing over cash to the government for profits that don't exist yet.

Even worse, you might build your budget around these inflated numbers. You see a big income spike and decide it’s time to hire new staff or buy expensive equipment. Then you realize the cash you just spent was already promised for future services. It’s a classic recipe for financial stress.

The rules around this have become even more important since accounting standards like ASC 606 were introduced. The point is to make revenue reporting consistent and clear across all businesses.

How to Stay on Track

Avoiding these mistakes just comes down to having a clear process. Here are the simple, correct ways to handle your deferred revenue and keep your books clean.

Mistake: Booking upfront cash as instant revenue.

- The Fix: Always record advance payments as a liability first. Create a "Deferred Revenue" account on your balance sheet and park the money there. It doesn’t touch your income statement until you’ve done the work.

Mistake: Forgetting to recognize revenue each month.

- The Fix: Set a recurring calendar reminder or, even better, automate it. At the end of each month, make the journal entry to move the earned portion from your deferred revenue liability to your earned revenue account. Consistency is key here.

The entire landscape of deferred revenue accounting has been shaped by these global shifts. After standards like ASC 606 were implemented around 2018, U.S. public companies saw a 22% average increase in reported deferred revenue as they aligned with the new five-step model. You can read more about how these changes standardized revenue recognition on Bill.com.

Frequently Asked Questions About Deferred Revenue

Once business owners start to understand deferred revenue, a few common questions always pop up. Let's answer them so you can feel confident about what these numbers mean for your business.

Is Deferred Revenue a Good or Bad Sign?

In almost every case, it’s a great sign. A high deferred revenue balance means you have a line of future work that customers have already paid you for. Think of it as a signal of strong cash flow and predictable income you can count on in the coming months.

The only catch? You must have the team and resources ready to deliver on those promises. So, view it as a clear sign of business health, as long as you can do the work.

How Is Deferred Revenue Different from Accounts Receivable?

This is a great question, and I'm glad you asked. They are complete opposites, and it all comes down to who owes what to whom.

- Deferred Revenue: This is cash you've received for work you haven't done yet. On your books, it’s a liability because you owe your customer a service or product.

- Accounts Receivable: This is money owed to you for work you've already completed, but you haven't been paid for yet. It's an asset because your customer owes you cash.

Put simply: with deferred revenue, you owe the customer work. With accounts receivable, the customer owes you money.

What Happens If a Customer Cancels and Needs a Refund?

If a customer cancels a prepaid service and you owe them a refund, your accounting just reverses the first entry. You'll decrease your Deferred Revenue liability account and, of course, decrease your Cash account on the balance sheet.

Of course, this all depends on your contract. If you've already delivered part of the service, you'd only refund the amount for the work you haven't done yet.

How Can Software Help Manage Deferred Revenue?

Trying to track dozens of client payment schedules in a spreadsheet is a recipe for disaster. It’s not a question of if you’ll make a mistake, but when—and it will cost you hours to fix.

Using modern accounting software is a lifesaver here. Tools like QuickBooks Online let you create automated revenue recognition schedules. This automation saves you from manual work, reduces the risk of errors, and gives you a clear, accurate picture of your earned vs. unearned income each month without the headache. It’s one of the best moves you can make to get this right.

Navigating the rules around deferred revenue is crucial for building a financially healthy business. At MyOfficeOps, we take the guesswork out of your bookkeeping and provide CFO-level insights so you can focus on what you do best. If you're ready for clean books and a clear path to growth, schedule your free discovery call with us today.