Getting paid isn't the same thing as earning money. It’s a simple idea, but it’s one that trips up a lot of business owners.

At the heart of a healthy business is something called the revenue recognition principle. It’s a basic accounting rule that says you should only record money as "revenue" when you've actually earned it. That means you've delivered the product or finished the service—not just when the cash shows up in your bank account.

Why Getting Paid Is Not the Same As Earning Money

Let's say you run a small web design business. A new client loves your ideas and pays you $6,000 upfront for a six-month project. Your bank account looks great, but did you really "earn" all $6,000 on the first day?

Nope. Not even close. Thinking you did is a common trap. Right now, you just have their cash. You still owe the client six months of work. This is the exact problem the revenue recognition principle solves.

Getting a Real Look at Your Business Health

This principle is really all about being honest with your numbers. It makes you match the income you record on your books with the work you've actually done.

Let's go back to that $6,000 project. Instead of putting the whole amount down in the first month, you would record $1,000 of revenue each month for six months as you do the work. This gives you a much better picture of how your company is doing over time.

Key Takeaway: Revenue recognition helps you see if your business is actually healthy. It stops you from thinking a full bank account means you're profitable.

By spreading the revenue out, you avoid having a giant income one month and almost nothing the next. That kind of steady view is what helps you make smart decisions about hiring, spending, and growing.

How It Works in Real Life

So, what happens to the money you've been paid but haven't earned yet? It sits on your books in an account called deferred revenue or unearned revenue. The best way to think of this is as a debt—it’s a promise you still owe your client.

As you finish the work each month, you move a piece of that money from the deferred revenue account over to your earned revenue account. This simple step gives you a few big wins:

- You Know Your Real Profit: You can see how much you actually made each month.

- You Can Plan Better: It's much easier to guess future income and manage your cash.

- You Look More Trustworthy: Banks and investors see a stable, predictable business, not one with crazy ups and downs.

This also shows how important it is to track who owes you money. You can find helpful tools for this, like an accounts receivable aging report template. Knowing what you're owed is just as important as knowing what you've earned.

This simple shift in thinking—from "getting paid" to "earning money"—is the first real step toward building a stronger, more valuable company.

The Five Steps for Recording Revenue the Right Way

So, how do you actually do this? For a long time, the rules were a little confusing. To make things clearer, the people who make accounting rules came up with a single, clear standard called ASC 606.

Don't let the name scare you. It's just a simple, five-step recipe that tells any business how to record its income correctly. Think of it like a checklist to make sure you're recording revenue at the right time and for the right amount.

The big idea is simple: you record revenue when you deliver on your promises to a customer. This changes the focus from when you get paid to when you provide value.

Let's walk through the five steps. We’ll use an easy example: a software company that sells a $1,200 yearly subscription that also includes a one-time setup service.

Step 1: Find the Contract with the Customer

First, you need a contract. This doesn't always have to be a fancy, 50-page document.

A contract can be a written agreement, a verbal one, or even just implied by how you do business. The important thing is that both you and your customer have agreed to it, you both know your rights and payment terms, and it's a real deal.

- Example: A customer signs up for our software company's $1,200 yearly plan online. By clicking "I agree" and putting in their credit card, they've made a contract. Simple as that.

Step 2: List Your Promises

Next, you need to figure out exactly what you promised to deliver. In accounting, these promises are called performance obligations. It’s just a technical term for each separate thing you owe the customer.

Sometimes a contract has just one promise, like selling a t-shirt. Other times, it has several, like our software example. The trick is to identify each separate promise. A good question to ask is, "Could the customer use this thing on its own?"

Key Insight: A "performance obligation" is just a fancy term for a promise you made to your customer. The key is to list out each separate promise.

For our software company, we have two different promises:

- Promise 1: The one-time setup and training service.

- Promise 2: Access to the software for 12 months.

The customer gets value from the setup, and they get value from the software access. Since they are separate things, they are two separate promises.

Step 3: Figure Out the Price

This step is usually the easiest. The transaction price is just the total amount of money you expect to get from the customer for doing everything you promised.

In our example, the transaction price is $1,200. It's the total fee for the yearly plan, and it's stated clearly in the contract.

Step 4: Split the Price for Each Promise

Now for the important part. We need to split that $1,200 total price between the different promises we found in Step 2. You have to assign a value to the setup service and a value to the software access.

The goal is to split the price based on the standalone selling price of each item—what you would charge for each thing if you sold it separately. Let's say our software company normally charges $100 for the setup service and $1,100 a year for software access if you buy them on their own.

In this case, the total of the standalone prices is $1,200 ($100 + $1,100), which matches our deal price. So, the split is easy:

- Setup Service: $100

- Software Access: $1,100

This split is super important because it tells you how much revenue to record and, more importantly, when. For a more detailed guide on how to handle these numbers, you can explore our resource on mastering revenue recognition principles in Excel.

Step 5: Record Revenue as You Keep Each Promise

You’re at the final step: recording the revenue. This happens as you finish each promise. The timing depends on whether you deliver the value all at once (like the setup) or over a period of time (like the software access).

Let's finish our example:

Record Revenue for the Setup: The setup service happens once. After you finish the training in the first month, you've kept that promise completely. You can record the full $100 you assigned to it right away in that first month.

Record Revenue for Software Access: The software access, however, is delivered over 12 months. You haven't earned the full $1,100 on day one. Instead, you earn it evenly over the year.

This means you will record $91.67 per month ($1,100 / 12 months) for the software access.

So, in the first month, your total recorded revenue would be $191.67 ($100 from the setup + $91.67 from the first month of access). For the next 11 months, you would record just $91.67 each month. This way, your books show the value you've actually delivered, not just the cash you got.

A Simple Guide to the 5-Step Model

Feeling a little lost? Don't worry. It seems complicated at first, but it gets easier. To make it even clearer, here’s a simple table breaking down each step.

| Step | What It Means | Simple Example (For a Web Designer) |

|---|---|---|

| 1. Find the Contract | You have a clear agreement with your client. | A client signs your proposal for a $5,000 website. |

| 2. List Your Promises | List every separate thing you promised. | Promise 1: Design and build the website. Promise 2: Provide 12 months of hosting. |

| 3. Figure Out the Price | Find the total fee you'll be paid. | The total project fee is $5,000. |

| 4. Split the Price | Split the total fee between your promises. | You'd charge $4,400 for the build and $600 for hosting separately. So, you split the $5,000 fee that way. |

| 5. Record Revenue | Record the income as you finish each promise. | Record $4,400 when the site goes live. Record $50/month for hosting for the next 12 months. |

Following these five steps makes sure your books tell the true story of your business's performance, giving everyone a much more accurate picture of your financial health.

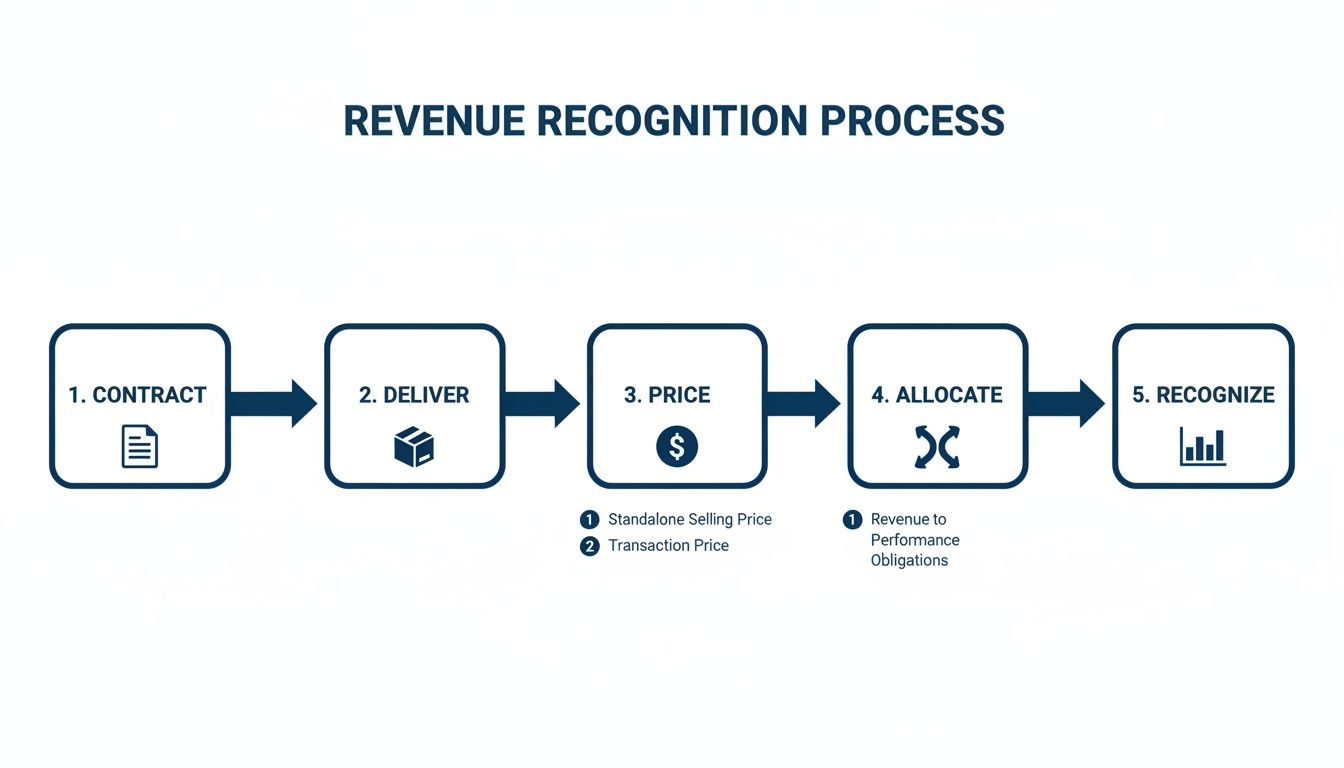

How Revenue Recognition Looks in the Real World

Theory is one thing, but seeing how this works in real life makes it all click. This isn’t just for giant companies; small businesses use it every day to get an honest look at their finances. Let’s walk through a few common examples you might run into.

This flowchart shows the five-step model that is the foundation of how we record revenue today.

As you can see, the process moves logically from finding the contract to finally recording the money you’ve earned. It’s all about tying revenue directly to when you deliver on your promises.

Example 1: The Marketing Agency Retainer

Imagine you run a marketing agency and sign a client on a $24,000, 12-month deal. Great! The client pays you the full amount upfront. It's really tempting to see that $24,000 in your bank account and count it all as revenue for that month.

But you haven't done 12 months of work yet. You've only been paid for it.

Using the revenue recognition principle, you can only record $2,000 of revenue each month ($24,000 / 12 months). The other $22,000 (after month one) sits on your books as deferred revenue. Think of it as a holding account for money you've been paid but haven't earned. Each month, as you do your marketing work, you’ll move $2,000 from deferred revenue over to earned revenue.

This gives you a stable, predictable picture of your monthly income instead of a huge spike in January and then nothing for the rest of the year from that client.

Example 2: The Construction Project

Now, think about a contractor building a large deck for a homeowner. The total project is $15,000, and the payments are tied to finishing specific parts of the job.

- $5,000 is paid upfront to start.

- $5,000 is paid after the foundation and frame are done.

- $5,000 is paid when the deck is completely finished.

In this case, the contractor records revenue as each stage is finished—that's when the value is delivered and "earned." When the client pays the first $5,000, it's just a deposit. No revenue is recorded yet because no work has been done.

Once the framing is done, the contractor has kept that promise and can record the first $5,000 of revenue. When the whole project is finished, the last $10,000 can be recorded. This approach perfectly matches revenue with the actual work being done. For a deeper dive, check out our complete guide on accounting for construction companies.

Key Idea: Deferred revenue is not your money to spend. It's a debt on your books that represents a promise you still owe your customer.

This stops the contractor from saying they made a bunch of money at the start of the project and gives a much better view of how profitable the job is at each stage.

Example 3: The Annual Software License

Software-as-a-Service (SaaS) companies live by this principle. Let's say a software business sells a yearly license for its product for $1,200. The customer pays the full amount on day one.

The software company is providing a service—access to its app—for the next 12 months. So, they can't record the full $1,200 as revenue in the first month.

Instead, they divide the total by the number of months. Each month, they will record $100 ($1,200 / 12 months) as earned revenue. The rest of the cash sits in that deferred revenue account and is slowly moved over each month as the service is provided.

This is super important for SaaS businesses. It allows them to accurately calculate things like Monthly Recurring Revenue (MRR), which is a key number investors and banks look at to see if a company is healthy and growing.

In all of these real-world situations, the ability to extract data from invoices is what makes it possible to do this correctly. Whether it's a retainer, a project payment, or a subscription fee, the invoice is where it all starts. These examples show that the revenue recognition principle isn't just a boring accounting rule—it's a tool for telling the true story of how your business is doing.

How This Principle Affects Your Business's Health and Value

The revenue recognition principle isn't just a stuffy accounting rule—it's how you get a real look at your business's performance. When you get it right, you give yourself, your banker, and potential investors a clear, honest picture of your company's stability and growth.

It’s the difference between guessing and knowing.

Using this principle helps you see the real story your numbers are telling. Instead of looking at a messy stream of cash deposits, you start to see smooth, predictable trends in your actual earnings. This is vital for tracking important numbers like Monthly Recurring Revenue (MRR) and your true profit.

A Real-World Example of Getting a Loan

I have a great story about this. One of our clients, a growing IT services company, needed a big business loan to buy new equipment and hire more staff. At first glance, their bank account looked healthy because they got big yearly payments from clients upfront. But their financial reports were a mess.

Their books showed huge income spikes in January, then looked like they fell off a cliff for the rest of the year. To a loan officer, this looked unstable and risky. The bank, not surprisingly, was nervous about lending them money.

We stepped in and cleaned up their books using proper revenue recognition. We took those big yearly payments and started recording the revenue monthly, as they actually provided their IT support. All of a sudden, their income statement showed steady, reliable earnings every single month.

The Result: The bank could now see a stable, profitable business with predictable revenue. They weren't just looking at random deposits anymore; they were seeing proof of real performance. The loan was approved right away.

This story makes it clear: clean financials aren't just for accountants. They build trust and open doors to the money you need to grow.

Why This Matters for Your Company's Future

Recording revenue the right way is key to building a valuable business, whether you plan to grow it, get funding, or sell it one day. Here’s why it's so important:

- It Builds Trust: Banks and investors love stability. Financials that show consistent, earned revenue are much more convincing than ones that just show when you got paid.

- It Helps You Make Better Decisions: When you have a clear picture of your monthly revenue and profit, you can make smarter, data-driven decisions about hiring, marketing, and other investments.

- It Increases Your Business's Value: If you ever decide to sell your company, a buyer will pay more for a business with clean, predictable, and well-documented earnings. Messy books are a huge red flag that can scare buyers off or lead to a much lower offer.

At the end of the day, understanding the revenue recognition principle is a key part of building a strong financial foundation. These practices are central to how you should prepare financial statements that show your business's true health. It turns your accounting from a chore into a tool for growth.

Common Revenue Recognition Mistakes to Avoid

Putting this principle into practice can feel a bit weird at first. It’s a big change from just looking at your bank account, and it’s normal for business owners to make a few mistakes.

The good news? Most of these mistakes are easy to spot and fix once you know what to look for. Let’s go through the most common slip-ups so you can keep your financial reports accurate and trustworthy.

Mistake 1: Recording an Entire Contract Upfront

This is the biggest and most common mistake. A client pays you $12,000 for a year-long service contract. The money hits your bank account, and it feels like a huge win. The temptation is to book all $12,000 as revenue in the first month.

This creates a dangerously wrong picture of your business. It makes one month look incredibly profitable while the next eleven months look like you earned nothing from that client. It also pumps up your short-term profits, which can lead to bad spending decisions.

- How to Fix It: Remember, you only earn the money as you do the work. Divide the total contract value by the number of months. In this case, you should record $1,000 of revenue each month for 12 months. The rest of the cash sits in a "deferred revenue" account until you've actually earned it.

Mistake 2: Treating an Invoice as Earned Revenue

Sending an invoice is an important step, but it doesn't automatically mean you've earned the money. An invoice is just a request for payment. Revenue is only earned when you've done the work or delivered the product.

For example, you might send a bill for a three-month project at the very beginning. You’ve sent the invoice, but you haven't done any of the work yet. Recording that full amount as revenue right away would be wrong and give you a false picture of your performance.

- How to Fix It: Think of invoicing and revenue recognition as two separate things. Send invoices when your contract says to, but only record the revenue in your accounting system as you complete the work.

Simple Rule of Thumb: An invoice asks for the money. Doing the work earns the money. Only record revenue when it's earned.

Mistake 3: Not Adjusting for Changes

Business is always changing. Clients might ask for extra services, or the scope of a project might shrink. These changes, or contract modifications, affect the total price and what you’ve promised to do. A common mistake is forgetting to update your revenue schedule when these changes happen.

Imagine you’re halfway through a project and the client adds a new feature that costs an extra $2,000. If you don't adjust your accounting, you’ll fail to record this extra revenue correctly over the rest of the project, and your financials will be wrong.

- How to Fix It: Whenever a contract changes, go back to the five-step model. You need to find any new promises, figure out the new total price, and re-split it across all the remaining work. This makes sure your books always show the latest version of your agreement.

Avoiding these common mistakes is what the revenue recognition principle is all about—creating a true, reliable story of your company's performance over time.

Making Sense of It All Without the Headache

If all this talk of performance obligations and deferred revenue has your head spinning, you’re not alone. The good news is you don’t have to become an accountant overnight to get this right.

In fact, trying to manage all of this on your own can quickly turn into a full-time job. It’s a huge distraction that pulls you away from what you do best—running your business.

This is where a good bookkeeping and advisory partner comes in. Instead of you getting lost in spreadsheets, an expert partner sets up your accounting systems to handle all of this automatically. They program your software to correctly track multi-month contracts, split payments between earned and deferred revenue, and create reports that actually make sense.

From Confusion to Clarity

Think of it this way: your partner builds the engine and the dashboard for your business's finances.

The engine (your accounting system) runs smoothly in the background, applying the revenue recognition principle correctly to every single sale. All you have to do is look at the dashboard—the simple, clear reports they give you each month.

These reports show you your true monthly revenue, your actual profit trends, and how much cash you’ve been paid for work you still owe your clients. This turns your financial data from a source of stress into a powerful tool for making good decisions.

Instead of just seeing a bank balance and guessing, you see the real story of your business's health. This is what helps you make smarter decisions about everything from hiring to new investments.

A Partnership for Smarter Growth

Working with a financial partner does more than just take boring tasks off your plate. It gives you a real strategic advantage. A good firm doesn't just "do the books"—they help you understand what the numbers mean for your future.

They help you answer the big questions that might be keeping you up at night:

- How much recurring revenue can we count on next quarter?

- Do we actually have the cash to hire a new person?

- Are our prices high enough to be profitable in the long run?

Ultimately, this kind of support allows you to step away from the financial details and focus on the big picture. You get the confidence that your books are accurate and the insight to steer your company toward growth, all without the accounting headaches.

Got Questions About Revenue Recognition? We've Got Answers

We get it—this stuff can seem a little confusing at first. To help, here are a few of the most common questions we hear from business owners every day.

How Is This Different from Just Tracking My Bank Account?

Looking only at your bank balance is called cash-basis accounting. It's simple: money comes in, you record income. Money goes out, you record an expense. It’s a snapshot of your cash right now.

The revenue recognition principle is part of accrual-basis accounting, which is more like watching a movie of your business’s performance. It records revenue when you earn it by doing the work, not just when you get paid. This gives you a much truer picture of your profitability over time.

Do I Really Need to Bother With This If My Business Is Small?

Yes, you definitely should. It might feel like too much work when you're just starting out, but it’s one of the best financial habits you can build early on.

Even for a small business, recording revenue correctly helps you understand your real financial health. It stops you from making bad spending decisions just because a big client paid you upfront. More importantly, if you ever want a business loan, an investor, or want to sell your company, they will demand financials prepared this way.

Starting now saves you huge headaches and expensive clean-up projects later on.

The real question isn’t if you need it, but when you’ll wish you had started sooner. Getting this right from day one builds a strong foundation for any growth you have planned.

What Exactly Is Deferred Revenue?

"Deferred revenue" sounds like a complicated accounting term, but the idea is actually simple. It’s cash you’ve received from a customer for work you haven't done yet. You’re holding their money, but you haven’t earned it.

Imagine a client pays you $5,000 upfront for a three-month project. The moment you get that cash, the entire $5,000 is deferred revenue. It sits on your books as a liability—basically, a promise you owe the client. It’s not yours to count as "earned" yet.

As you do the work each month, you'll move a piece of that money from the deferred revenue account over to the earned revenue on your income statement.

Feeling a bit overwhelmed by the details? You don't have to manage this alone. The team at MyOfficeOps can set up your systems to handle revenue recognition automatically, giving you crystal-clear reports without the headache. Schedule a discovery call with us today to see how we can help.