You open your budget report, look at the Budget column, then the Actual column, and your stomach drops a little.

Payroll is different than expected. Marketing came in higher. Supplies came in lower. Revenue missed in one area and beat the plan in another. Now you’re left with the question most owners ask: Should I be worried, or is this normal?

It’s normal.

Every small business budget ends up with gaps between the plan and what really happened. The problem isn’t that the numbers differ. The problem is when nobody can explain why they differ and what decision should come next.

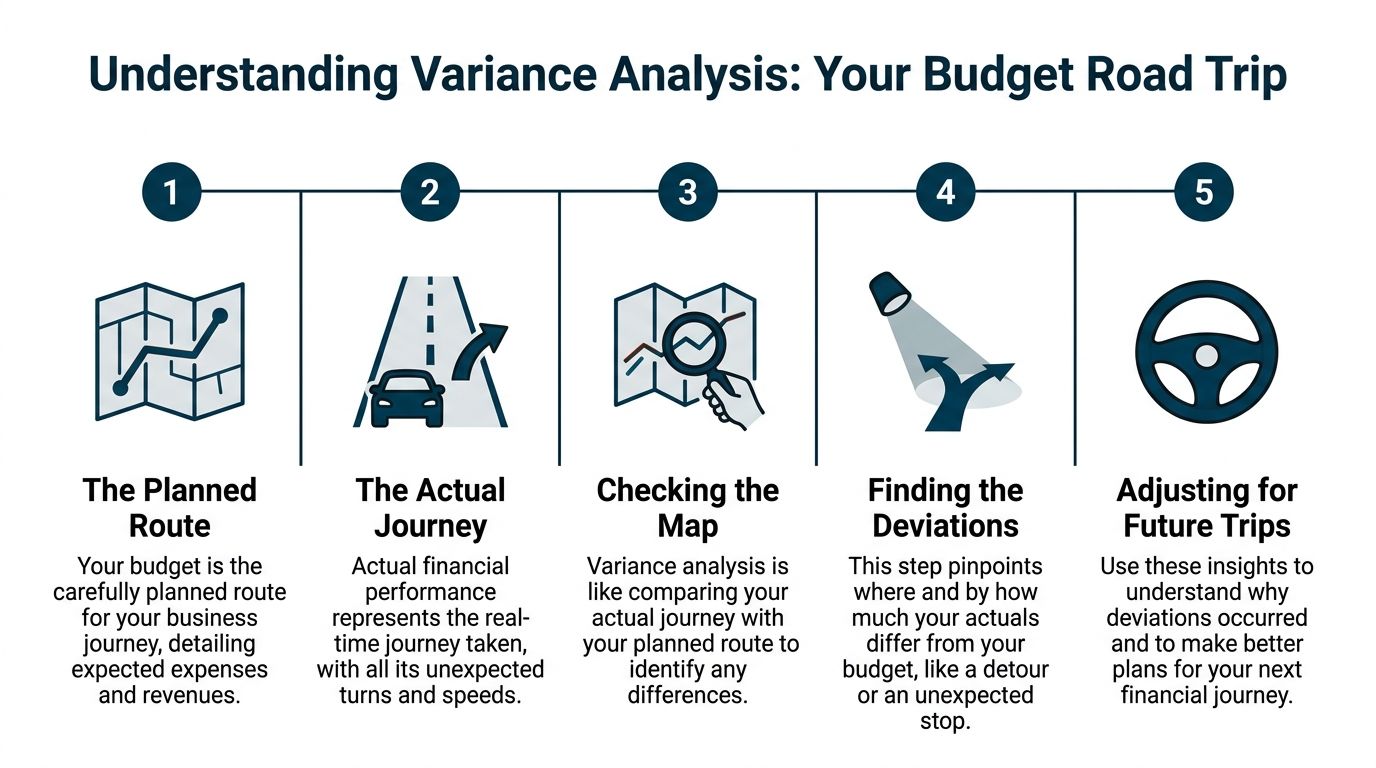

That’s where what is variance analysis in budgeting becomes a useful question, not just an accounting term. Variance analysis is the practice of comparing what you planned to what occurred, then figuring out what the difference means. It turns a confusing report into something you can use.

If you run a contractor business, that might mean spotting profit leaks on a job before the whole project goes sideways. If you own a clinic, it might mean seeing that payroll “savings” aren’t really savings because open roles are slowing patient flow. If you run a consulting firm, it might mean realizing the issue isn’t overhead at all. It’s that your fixed-fee projects are eating too many billable hours.

A budget isn’t just numbers on paper. It’s a set of expectations about hiring, pricing, workload, cash flow, and growth. Variance analysis helps you check whether those expectations match real life.

Your Budget Is Telling a Story Are You Listening

A lot of owners treat the monthly budget report like a school report card. Green must be good. Red must be bad. If expenses are over, someone must have messed up. If expenses are under, everyone can relax.

Real life doesn’t work that neatly.

Say you run a small HVAC company near West Chester. You budgeted for labor, trucks, materials, and sales. At month end, labor is under budget, fuel is over, and revenue is a little behind. On the surface, that sounds like a mixed bag. But the story behind it could be very clear once you look closer.

Maybe labor is under budget because you still haven’t filled an open technician role. That sounds “good” until you realize your team is stretched thin, jobs are getting pushed back, and you’re losing work you could have billed. Maybe fuel is over because your crews are driving farther for higher-margin work. That might be a smart trade. Maybe revenue is behind because several completed jobs haven’t been invoiced yet. Again, the story matters.

Numbers don’t speak for themselves. Someone has to ask what caused them.

That’s the heart of variance analysis. It helps you move from “these numbers don’t match” to “here’s what happened in the business.”

Why owners get stuck

The math isn't usually the sticking point. Interpretation is.

A report might show a line item that’s off by a certain amount, but that alone doesn’t tell you what to do. Should you cut spending? Raise prices? Hire sooner? Hold off? Dig into one customer? Rework one service line? Without context, you’re guessing.

What the story helps you decide

When you understand the variance, you can make a real decision:

- Hiring decisions based on whether labor variance reflects efficiency or understaffing

- Pricing decisions based on whether margins are shrinking job by job

- Cash flow decisions based on whether the timing of revenue is the issue

- Operational decisions based on whether a project, team, or client is causing the gap

That’s why good owners don’t just review whether the budget was hit. They ask what the budget is trying to tell them.

What Variance Analysis Actually Is and Is Not

You sit down at month end, open the budget report, and see payroll under budget, fuel over budget, and revenue a little light. That mix can mean three very different things. You may be running lean and burning out your team. You may be spending more to serve better jobs. Or you may be waiting on invoices to go out.

Variance analysis is the process of sorting that out.

The simple definition

At the basic level, variance analysis compares what you planned to what happened, then asks why the gap exists.

There are two parts to it:

- Measure the difference

- Explain the cause

The math starts simple. Dollar variance is usually Actual minus Budgeted.

If a clinic budgeted more patient revenue than it collected, or a contractor spent more on labor than planned, the first job is to measure the size of that gap. Then you figure out whether the issue came from price, volume, timing, staffing, efficiency, or a decision you made on purpose.

That second part is where this becomes useful for an owner.

A consultant with lower revenue might have a sales problem. Or they might have the same amount of work and just delayed billing. A contractor with higher labor cost might have a productivity problem. Or they may have added overtime to finish a profitable job faster. The number is the signal. The cause is what guides the decision.

Why the percentage matters

A dollar gap on its own can be misleading.

A $5,000 overrun means one thing in a small monthly office expense line and something very different in a large project budget. Percentage variance helps you judge scale, not just dollars. It answers the question, “Is this small noise, or something that needs attention?”

That matters in real life. If a clinic’s medical supplies come in above budget by a modest percentage, you may monitor it and move on. If a consulting firm’s subcontractor cost jumps by a large percentage, you may need to revisit pricing on active proposals right away.

Practical rule: Review both the dollar variance and the percentage variance. One shows size. The other shows significance.

If you want to tighten this process over time, it helps to pair your budget review with a clear financial forecasting process for small businesses. Forecasting updates the plan. Variance analysis explains the gap.

What variance analysis is and what owners often confuse it with

Owners sometimes treat variance analysis like a scorecard with green lights and red lights. That misses the point.

Variance analysis is a decision tool. It helps you separate problems that need action from differences that need context. As the Corporate Finance Institute explains in its guide to variance analysis, the goal is to compare planned and actual results so management can identify what drove performance.

In a small business, those drivers often fall into three buckets:

- The budget was off. You estimated too low, too high, or used old assumptions.

- Operations were off. The team used more hours, materials, or discounts than planned.

- You chose a different path. You spent more, hired sooner, or took lower-margin work for a reason.

That last one trips people up all the time.

Say a West Chester contractor budgets one technician, then hires sooner because demand is building and response times are slipping. Payroll goes unfavorable. From a report view, that looks like a miss. From an ownership view, it may be the move that protects customer retention and opens room for more billable work next month.

The same logic applies in a service business. A consulting firm may show an unfavorable labor variance because senior staff spent extra time onboarding a new client. If that client becomes a long-term account, the short-term variance may be money well spent.

What variance analysis does not do

It does not hand you the answer by itself.

A report can show that lab costs were high in a clinic, direct labor ran over on a remodeling job, or software expense climbed at a consulting firm. The report does not know whether that happened because of waste, growth, seasonality, delayed vendor increases, or a smart strategic choice. Someone has to connect the numbers to what happened on the ground.

That is why regular review matters. The Association for Financial Professionals notes in its budgeting and forecasting resources that comparing results to plan helps organizations adjust assumptions and respond sooner when performance shifts (AFP budgeting and forecasting resources).

Used well, variance analysis helps you find hidden profit leaks in project-based and service-based businesses. It can show that a contractor is underbidding labor on one type of job, that a clinic is losing margin to payer mix changes, or that a consultant is discounting too often to win work. Those are not accounting trivia points. They are hiring, pricing, and capacity decisions.

The Building Blocks of Variance Analysis

A budget variance report gets useful when you break it into parts. Otherwise, it is like seeing that your truck is making a strange noise but having no idea whether the problem is the engine, the brakes, or a loose tool in the back.

For a small business owner, the goal is simple. Find out whether profit slipped because you charged less, sold less, paid more, or used more labor and overhead than planned. Once you know which part moved, you can make a real decision about pricing, staffing, scheduling, or purchasing.

Start with total variance

Start wide, then narrow.

Compare the budgeted amount to the actual amount. That first comparison tells you how far off you were overall.

If you budgeted $50,000 for quarterly marketing and spent $55,000, your variance is 10% unfavorable using this formula: ((Actual – Budgeted) / Budgeted) × 100. If you budgeted $100,000 in revenue and brought in $75,000, your revenue variance is 25% unfavorable.

That number is only the headline. It tells you where to look first.

Break revenue into price and volume

Revenue usually changes for one of two reasons. You charged a different price than planned, or you sold a different amount than planned.

Price variance

Price variance asks whether your actual selling price matched your budgeted price.

This matters a lot in service and project-based work because price changes often hide in small decisions. A consultant offers a discount to win a retainer. A clinic accepts a different payer mix than expected. A contractor trims a bid to stay competitive.

On the surface, each choice may look minor. Over a month or a quarter, those choices can pull down margin.

If your price variance is off, the business question is not just, “Why is revenue lower?” The better question is, “Are we discounting too often, underbidding certain jobs, or accepting work at rates that do not cover labor?”

Volume variance

Volume variance asks whether you sold as much work as you expected to sell.

A contractor may have fewer signed jobs than planned. A clinic may see fewer patient visits. A consulting firm may have open capacity because billable hours came in light.

That leads to a different decision. If volume is the issue, you may need better scheduling, stronger follow-up on proposals, a referral push, or more sales activity. Cutting prices further may only shrink margin without fixing the actual problem.

Here is a simple way to separate the two:

| Question | What it helps you diagnose |

|---|---|

| Did we charge what we expected? | Discounting, bid strategy, payer mix, pricing discipline |

| Did we sell as much as we expected? | Demand, utilization, scheduling, sales execution |

Break costs into rate and usage

Expenses also have two common drivers. You paid a different rate than expected, or you used more of something than expected.

That distinction matters because the fix is different.

Input or supply cost variance

This variance shows up when the cost of materials, supplies, software, or subcontractors comes in higher or lower than planned.

For a contractor, that may be lumber, concrete, fixtures, or subcontractor bids. For a clinic, it may be medical supplies or lab-related costs. For a consulting firm, it may be software subscriptions, contractor support, or research tools.

If the rate changed, you may need to revisit vendor contracts, update estimates, or raise prices on future work. If you are still bidding jobs using old cost assumptions, you can stay busy and still lose money.

Labor variance

Labor variance is where many service businesses uncover the underlying profit leak.

You may be paying a higher hourly rate than planned, using more hours than planned, or both. A remodeling job can run over because the crew needed extra site visits. A clinic can lose margin when staff time per patient rises. A consulting project can look profitable until senior people spend far more time on revisions than the proposal assumed.

That is why labor variance should be tied back to operations, not just payroll totals. If one project type always runs long, you may need to change your pricing, tighten scope, or stop taking that kind of work at the current rate.

A job can hit its revenue target and still disappoint on profit because it consumed too much time.

Understand overhead without overcomplicating it

Overhead includes the support costs that keep the business running. Rent, admin payroll, insurance, software, utilities, and similar expenses usually sit here.

Owners sometimes ignore overhead variance because it feels less tied to one client or one job. That is a mistake. For many small businesses, overhead creeps up slowly and squeezes profit month after month.

OneStream’s variance analysis overview explains that fixed overhead can be analyzed in two useful ways. One asks whether fixed costs themselves were higher than budgeted. The other asks whether those fixed costs were spread over less activity than expected.

The technical terms matter less than the business lesson.

If your clinic carries the same front-desk staff and facility costs but patient visits fall, overhead per visit rises. If your consulting firm keeps the same salaried team but billable utilization drops, overhead per project rises. If your crews and equipment are underused, a contractor feels the same pressure.

In plain English, overhead variance answers two questions:

- Did our support costs increase?

- Did we have enough work to absorb those costs efficiently?

Those answers affect hiring plans, capacity targets, and the minimum pricing you need to protect margin.

Set a threshold so you focus on what matters

You do not need to investigate every small miss.

A practical variance process needs a filter. Otherwise, you spend your time chasing minor fluctuations instead of the few items that can change the month.

Many businesses use a percentage threshold, a dollar threshold, or both. The exact cutoff depends on your size and risk. A contractor may review any labor overrun on a job because one bad project can erase the profit from several good ones. A clinic may watch supply costs and provider productivity more closely than office supplies. A consultant may flag discounting and write-offs before anything else.

The point is to pick rules that help you act early.

Clean records make this much easier. If your budget assumptions still feel shaky, this guide to financial forecasting for small businesses can help you build a plan that gives your variance review something solid to measure against.

Favorable vs Unfavorable Is Not Good vs Bad

A variance report can fool you if you read it like a scoreboard.

On paper, a favorable variance usually means revenue was higher than planned or expenses were lower than planned. An unfavorable variance usually means revenue missed budget or costs came in higher. That part is straightforward. The mistake happens when an owner treats favorable as healthy and unfavorable as a problem without asking what caused the number.

In a service business, the reason behind the variance matters more than the label.

A favorable variance can hide a profit leak

Say a clinic’s payroll comes in under budget for the month. At first glance, that looks like good cost control. But if the underlying reason is an open provider or admin role that stayed unfilled, the savings may come with slower scheduling, longer wait times, and fewer completed visits.

The same pattern shows up in other businesses. A consulting firm may spend less on contractor support because it delayed bringing in help, then miss deadlines or burn out senior staff. A contractor may come in under budget on equipment maintenance because service was postponed, then lose time on the job when a machine breaks down.

The report says you spent less. The business may be paying for it somewhere else.

An unfavorable variance can be a smart choice

Now look at the other side.

A contractor may run over labor budget because a project moved faster by adding a crew at the right time. A clinic may spend more on recruiting because patient demand is strong and another provider will relieve schedule pressure. A consulting firm may exceed its software budget after buying a tool that cuts admin time and frees billable hours.

Those are unfavorable variances in accounting terms. They are not automatically bad decisions.

A useful question is simpler: Did this variance hurt the business, or did it support a better result later?

Read the reason before you react to the label.

Use the variance to ask better business questions

Variance analysis works like comparing your estimate for a job to the final invoice. The gap matters, but the primary value comes from learning why the gap happened and what you should change next time.

Instead of sorting each line into good or bad, review it through an owner’s lens:

- Was this intentional? If you chose to spend more, what result were you trying to get?

- Is it a timing issue? Some expenses move between months and make one report look better or worse than reality.

- Did it affect capacity? Lower spending can mean fewer people, fewer hours, or slower work.

- Did it protect or hurt margin? Extra spending that supports pricing, output, or retention may be worth it.

Here is what that looks like in practice:

| Variance | Quick reaction | Better question |

|---|---|---|

| Payroll under budget | Great, we saved money | Are we short-staffed and risking delays or lost revenue? |

| Marketing over budget | We overspent | Did the extra spend bring in the right leads or booked work? |

| Training under budget | Nice, lower costs | Did we postpone something that would improve speed or quality? |

| Recruiting over budget | Problem | Did we hire ahead of demand to avoid turning work away? |

The label matters less than the pattern

One month by itself can be misleading. If a favorable variance shows up once, it may just be timing. If it shows up three months in a row in payroll, marketing, or maintenance, you may be looking at underinvestment rather than efficiency.

That is where hidden profit leaks show up for project-based and service-based companies. A contractor may keep celebrating labor savings while jobs fall behind. A clinic may hold staffing costs down while providers lose appointment capacity. A consultant may keep travel and support expenses low while client delivery slows and write-offs rise.

The number is only the starting point. The decision comes from the story behind it.

Variance Analysis in Your Industry

A contractor finishes the month with sales close to plan, but cash feels tight. A clinic keeps payroll below budget, yet appointment slots sit empty because the right roles are not filled at the right times. A consulting firm hits its revenue target and still wonders why owner profit keeps coming in light.

Those are industry-specific variance problems.

Variance analysis gets useful when you stop viewing the business as one lump sum and start reviewing the place where money is made or lost. For project-based and service-based companies, that usually means by job, client, provider, service line, property, or location. That is how owners find hidden profit leaks that a company-wide budget can miss.

Construction and trades

For contractors, the budget on paper is only the starting bid on reality. The true test happens inside each active job.

A project can look healthy from 30,000 feet because total revenue is on track. Then you open the job file and see the margin leak. Labor hours ran over estimate. Material prices changed after the bid. A change order was approved in the field but never billed. A crew spent extra time fixing work that was not priced into the original job.

That kind of variance analysis helps a contractor make decisions while there is still time to act. You can tighten change-order tracking, compare actual job costs to your estimate, spot where crews are burning too many hours, and use that information to price the next job more accurately.

For a small contractor, that matters in plain-English terms. If labor keeps running over on kitchen remodels, you may need to raise pricing, change the scope process, or assign a different foreman. If every job with one supplier comes in high on materials, you may need a new purchasing plan.

Healthcare clinics

Clinics usually have a different profit leak. It often sits in the relationship between staffing, scheduling, payer mix, and visit volume.

Say payroll comes in under budget. At first glance, that looks like a win. But if a provider schedule has open gaps, front-desk coverage is thin, or one open medical assistant role is limiting patient flow, the clinic may be giving up revenue to save on wages. In that case, the favorable payroll variance is pointing to an operational problem, not efficiency.

Supply costs can work the same way. Higher-than-planned medical supplies might mean waste. It could also mean the clinic saw more high-value procedures or a different mix of patients than expected. The number only becomes useful when you compare it to visits, reimbursements, and provider capacity.

For clinic owners, the practical question is simple. Did staffing and scheduling support the volume and type of care you wanted to deliver? That answer affects hiring, hours, and even whether you should add another provider.

Professional services and consulting

For consultants, agencies, and other service firms, revenue often hides the problem.

A fixed-fee project may bill exactly as planned and still earn less than expected. Hours drift up. Scope expands in small ways. A senior team member jumps in to rescue delivery. Internal revisions pile up. None of that shows clearly if you only review invoiced revenue against budget.

The better comparison is budgeted hours versus actual hours, by client or by project. Once you see that gap, the decisions get clearer. You may need to reprice a service, tighten scope control, change who does the work, or stop offering a package that looks good in sales meetings but eats margin during delivery.

Service firms feel this all the time. The owner says, "We are busy, so why is profit flat?" Variance analysis helps answer that with specifics instead of guesswork.

One of the most useful questions in a consulting business is whether the job went over because the team worked inefficiently or because the original price assumed too little work. Those lead to very different decisions.

Real estate and related businesses

In real estate businesses, variance often makes the most sense below the company level. You may need to review by property, deal, service line, or office.

One property may be dragging maintenance expense above plan while another is performing well. Leasing costs may be rising in one segment but not another. Admin payroll may look fine overall, yet one line of business may be using far more staff time than it earns back.

That kind of review helps with resource allocation. You can decide which properties need attention, which services deserve more investment, and which parts of the business are using time without producing enough return.

The takeaway by industry

The pattern changes by industry, but the purpose stays the same. Review variance where decisions happen.

| Industry | Where variance often hides | Best decision it supports |

|---|---|---|

| Construction | Job costs, labor hours, materials, and change orders | Better bidding, tighter job control, and faster correction on active work |

| Clinics | Staffing levels, provider schedules, visit volume, and patient mix | Better hiring, scheduling, and capacity planning |

| Consulting | Billable hours, scope drift, write-offs, and project staffing | Better pricing and project management |

| Real estate | Property, deal, location, or service-line performance | Better resource allocation and operating focus |

If your budget is still too broad to answer those questions, start by tightening the assumptions behind it. This guide on how to create a business budget that matches how your company actually operates is a good place to begin.

A Simple Plan to Start Using Variance Analysis

Say you finish the month and profit is lighter than expected. Revenue looked close enough. Cash is still moving. But something feels off.

For a contractor, that leak might be labor hours running long on two active jobs. For a clinic, it might be overtime at the front desk because the schedule keeps bunching up on certain days. For a consultant, it might be write-offs on work that was never priced correctly in the first place. Variance analysis helps you find that leak before it turns into a pattern.

You do not need a large finance team to make this useful. You need a monthly routine that is simple enough to keep using.

Step 1 Build a budget that matches how the business runs

Variance analysis starts with a budget you can trust. If the budget is built on rough guesses, every comparison after that gets weaker.

Your budget should reflect the drivers behind the business. A contractor may need job volume, crew hours, materials, subcontractors, and equipment costs. A clinic may need provider schedules, visit volume, payer mix, and staffing by role. A consultant may need billable hours, utilization, project mix, and contractor support.

If those assumptions still feel too broad, start with a guide on how to create a business budget that matches your operations.

Step 2 Clean up the actual numbers

This step trips up a lot of owners.

If payroll lands in the wrong category, project costs sit in overhead, or vendor bills get posted late, the report will point you toward the wrong problem. What looks like a pricing issue may be a coding issue. What looks like an overhead spike may belong to one client, one job, or one provider.

Good variance analysis depends on clean bookkeeping because clean bookkeeping shows where the work and the money really went.

Step 3 Compare budget to actual in dollars and percentages

Use both views every month.

Dollar variance shows size. Percentage variance shows scale. A $2,000 overrun may be minor in one account and a big warning sign in another.

That matters in real decisions. If materials are $4,000 over budget on a $400,000 construction job, you may monitor it. If admin payroll is $4,000 over budget every month in a small clinic, you may need to revisit staffing or scheduling. The same number can call for very different action.

Step 4 Set rules for what gets reviewed

Without a threshold, every report becomes a scavenger hunt.

Pick a rule that fits the business. You might review any line that is over a set dollar amount, over a set percentage, or both. You can also flag repeat variances even when each month looks small on its own. That helps you catch slow leaks, which are often the ones that hurt margins most in service businesses.

A simple rule set might look like this:

- Review right away if a line is over your dollar or percentage threshold

- Review trends if the same line misses budget for two or three months in a row

- Leave it alone if the amount is small and does not affect hiring, pricing, scheduling, or cash flow

Step 5 Find the cause before choosing the fix

A variance is a signal, not a conclusion.

Start by asking a few plain questions. Did volume change. Did prices change. Did the team use more hours than planned. Did scope expand without approval. Did timing shift from one month to another. Was the variance intentional because you chose to invest in growth or fill a needed role.

This part works a lot like diagnosing a leak in your building. The water stain tells you where the problem showed up. It does not tell you whether the source is the roof, the pipe, or the window. In the same way, an unfavorable variance tells you where to look, but not what to blame.

If you want a clearer view of patterns across revenue, expenses, and job performance, tools like the Financial Insights Dashboard can make those signals easier to spot.

Step 6 End with one decision

Every monthly review should lead to action.

One action is enough. Raise the price on a service that keeps producing write-offs. Add approval steps for project extras. Adjust staffing on slow clinic days. Rework a bid template if labor keeps coming in high. Update next quarter’s forecast if demand has clearly changed.

That is where variance analysis becomes practical. It helps you decide whether to hire, reprice, reschedule, tighten scope, or leave a healthy part of the business alone.

A good monthly habit: End each review with one owner decision, one person responsible, and one follow-up date.

Keep the report short and decision-focused

The best owner report is usually brief. It should help you answer, “What changed, why did it change, and what do we do now?”

A simple format works well:

| Line item or segment | Budget | Actual | Variance | Action |

|---|---|---|---|---|

| Revenue or service line | ||||

| Labor or payroll | ||||

| Key project or client | ||||

| One major overhead line |

If the report helps you make a better call on pricing, hiring, job control, or scheduling, it is doing its job.

Turn Your Numbers into a Roadmap with MyOfficeOps

Most owners don’t need more spreadsheets. They need clear answers.

That’s the value of variance analysis. It takes budget-to-actual reports that feel backward-looking and turns them into something useful for the next decision. Instead of staring at a mismatch and wondering what happened, you can see whether the issue is pricing, labor, job control, staffing, or planning.

That kind of clarity depends on three things.

First, your books need to be clean enough to trust the actual numbers. Second, someone has to translate those numbers into plain-English insights. Third, the business needs guidance on what to do next, whether that means adjusting hiring, revising pricing, improving cash flow planning, or tightening project controls.

For owners who want a stronger reporting layer, tools that visualize trends can help. A platform like Ekipa AI’s Financial Insights Dashboard can be useful for seeing budget and performance signals more clearly, especially when you’re trying to spot issues before they grow.

For many small and midsize businesses, though, the hard part isn’t getting more charts. It’s having someone connect the chart to an actual business choice.

That’s where advisory support matters. If you’re weighing outsourced finance leadership, this overview of CFO services for small businesses gives a good sense of how owners use financial reporting to make decisions about growth, profitability, and cash flow.

The best setup is one where the numbers don’t just get recorded. They get explained. Then they get used.

When that happens, your budget stops being a static document you built once and forgot. It becomes a working roadmap.

If you want help turning confusing reports into clear decisions, MyOfficeOps can help. Their team supports small and midsize businesses with clean bookkeeping, practical reporting, and CFO-level guidance that helps owners make smarter calls on pricing, hiring, cash flow, and profitability.