Job costing is direct materials + direct labor + applied overhead. It's a way to track the actual cost and profitability of each job, project, or client instead of blending everything together.

If you're a business owner, you've probably felt this problem already. Work is coming in. The bank account moves up and down. Your team stays busy. But when you ask a simple question, “Which jobs make us money?” the answer gets fuzzy fast.

That's where job costing matters. It isn't just an accounting formula. It's a decision tool. It helps you see whether a custom kitchen remodel, a website project, a legal matter, or a consulting engagement is earning a healthy return or draining your margin.

A simple way to think about it is this. If you bake a custom wedding cake, you need to know the exact ingredients, the baker's time, and part of the kitchen's operating cost for that one cake. If you bake trays of identical cookies all day, you can average the cost across batches. What is job costing? It's the method built for the cake, not the cookies.

Why Some Profitable Businesses Still Go Broke

A lot of owners confuse being busy with being profitable.

A contractor can have a full calendar and still lose money on the jobs that look biggest from the outside. An agency can land a dream client and still watch margin disappear through extra revisions, rushed deadlines, and too many senior staff hours. A law firm can bill heavily and still underprice certain case types because nobody tracked the labor and support cost by matter.

Revenue can hide bad jobs

Here's the trap. Most businesses look at company-wide totals first. Total sales. Total payroll. Total expenses. That tells you whether the business as a whole is up or down. It does not tell you which specific jobs are carrying the business and which ones are dragging it down.

A big client can make you feel safe while steadily eating time, materials, and overhead. Smaller jobs can look less exciting but produce cleaner profit because the work is tighter and easier to manage.

The businesses that get into trouble usually don't fail because they had no sales. They fail because they couldn't see where their margin was leaking.

That's why job costing became such an important part of managerial accounting as business moved from simple craft work into more customized industrial work. The method is used when each order, project, or client job consumes labor, materials, and overhead differently, rather than following one uniform production flow, as explained in Saylor's overview of job costing in managerial accounting.

The real question owners are asking

Most owners aren't asking for an accounting lecture. They're asking practical questions:

- Which jobs should I do more of

- Which customers are profitable

- Where did this project go off track

- Do my prices reflect the actual cost of delivery

- Is detailed tracking worth the effort for my business

That last question matters. Job costing can create extra admin work. If your work is highly custom, that effort often pays for itself in better pricing and better decisions. If your work is standardized, the admin burden may outweigh the benefit.

That trade-off is the heart of the issue. Job costing works best when you use it to manage the business, not just close the books.

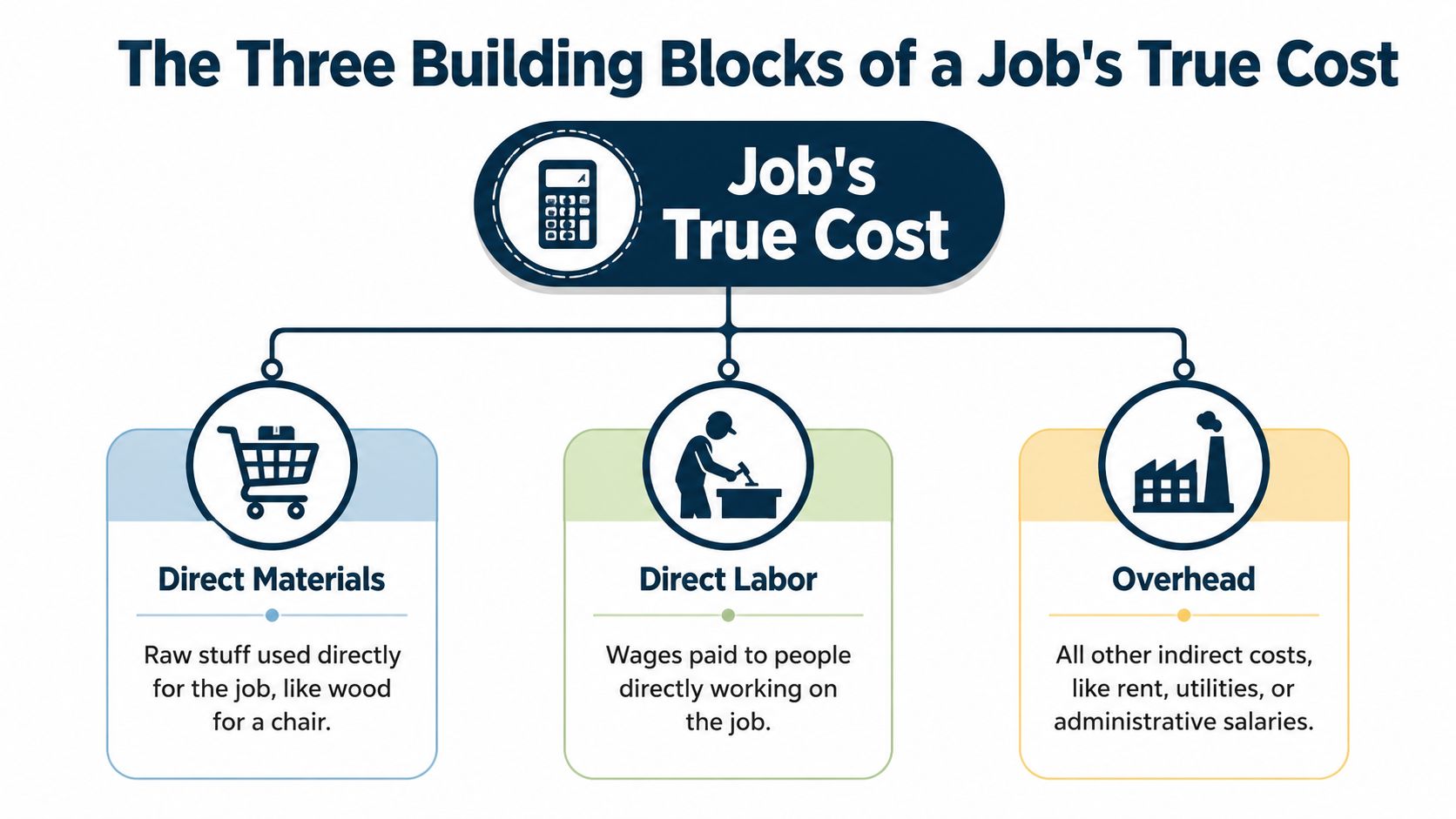

The Three Building Blocks of a Job's True Cost

Most owners make job costing harder than it needs to be. In practice, you're sorting costs into three buckets: direct materials, direct labor, and overhead. That basic structure is the core of job costing, and breaking estimates into those buckets helps you see where overruns happen later, as described in NetSuite's guide to job costing.

Here's the visual version.

Direct materials

These are the raw things that go into the job itself.

If you build a custom bookshelf, direct materials are the wood, screws, stain, and hardware. If you run a marketing agency, they might be stock photos, a paid plugin, or printing for a client event. If you're a contractor, direct materials are whatever you bought for that specific job site.

This category is usually the easiest one for owners to understand because it feels tangible. You bought it for that job. It belongs to that job.

Direct labor

This is the time your people spend doing the work.

For a bakery making a custom wedding cake, direct labor is the baker decorating the cake and the staff member assembling it. For a law firm, it's attorney and paralegal time on a specific matter. For a remodeler, it's crew hours on demolition, framing, and finish work.

A lot of small businesses undercount labor because they only look at wages in a broad way. Job costing forces you to ask, “How much time did this exact project consume?”

Practical rule: If a person worked directly on delivering the job, their time probably belongs in direct labor.

Overhead

This is the bucket owners often miss.

Overhead is the cost of keeping the business running when that cost can't be traced neatly to one single job. Think rent, utilities, office software, admin support, insurance, or the portion of supervision that supports many jobs at once. In job costing, overhead is commonly allocated using a predetermined rate tied to something like labor hours or machine hours, not guessed at after the fact. If you want a cleaner system around receipts, vendor charges, and categorization, a good primer on small business expense tracking can help tighten the basics before you layer on job costing.

For many owners, overhead is where “profitable” jobs stop looking so profitable. A project may cover labor and materials just fine, but once you assign its fair share of indirect costs, the margin shrinks.

A related concept that often confuses people is cost of goods sold. If you want the broader accounting context, this guide on what cost of goods sold means for a business is a useful companion.

Why these buckets matter

When you separate costs this way, you stop arguing in generalities.

Instead of saying, “That job just felt expensive,” you can say:

- Labor ran long

- Materials cost more than estimated

- Overhead allocation was too light

- The price was wrong from the start

That's the point. Clarity beats gut feel.

Job Costing in Action A Simple Project Example

Job costing clicks when you see it on one real project.

Take a small creative agency building a website for a local café. This is a custom job, so the agency shouldn't blend its cost into monthly company totals. It should trace the cost to that one project. That's what job costing is for.

Here's a simple example.

The first estimate

The agency scopes a website for “Fresh Eats” Café and builds the expected cost like this:

Direct materials

Software licenses, stock photos, and premium plugins. $300Direct labor

Designer's time at 20 hours @ $50/hr and project manager's time at 5 hours @ $60/hr. $1300Allocated overhead

A share of office rent, utilities, and admin expenses. $400Total job cost

$2000

If the client pays more than the full cost, the job should be profitable. If the client pays less, or if the actual cost rises above the estimate, margin gets squeezed.

This example also shows why job costing is a project-level accumulation method. Costs are traced to a single job, and the basic equation is direct materials + direct labor + applied overhead, as outlined in MRPeasy's explanation of job costing.

What goes wrong in real life

Now let's make it realistic.

The client asks for extra page revisions. The team spends more time in meetings than expected. A plugin issue slows down implementation. Nobody panics because each issue feels small on its own.

That's how profit leaks happen.

By the end of the project, the agency compares the original estimate with the actual job cost sheet. It may find that labor, not materials, caused the overrun. Or it may find that the overhead allocation base was too weak, so the project looked healthy during delivery but wasn't carrying its full share of business costs.

A job rarely goes bad all at once. It usually slips through a series of small decisions that no one measures in time.

What a smart owner does with that information

The point isn't to admire the spreadsheet after the project is done. The point is to improve the next decision.

A business that reviews estimate versus actual can do things like:

- Tighten scope so revisions are limited

- Price similar jobs differently because the labor pattern is now clearer

- Use a better overhead allocation base if the current one hides true costs

- Train project managers to flag change requests earlier

If you want a deeper look at variance thinking, this guide to effective project cost management gives a practical view of how planned cost and actual cost can drift apart.

The owner who uses job costing well isn't just doing accounting. They're building a pricing memory for the business.

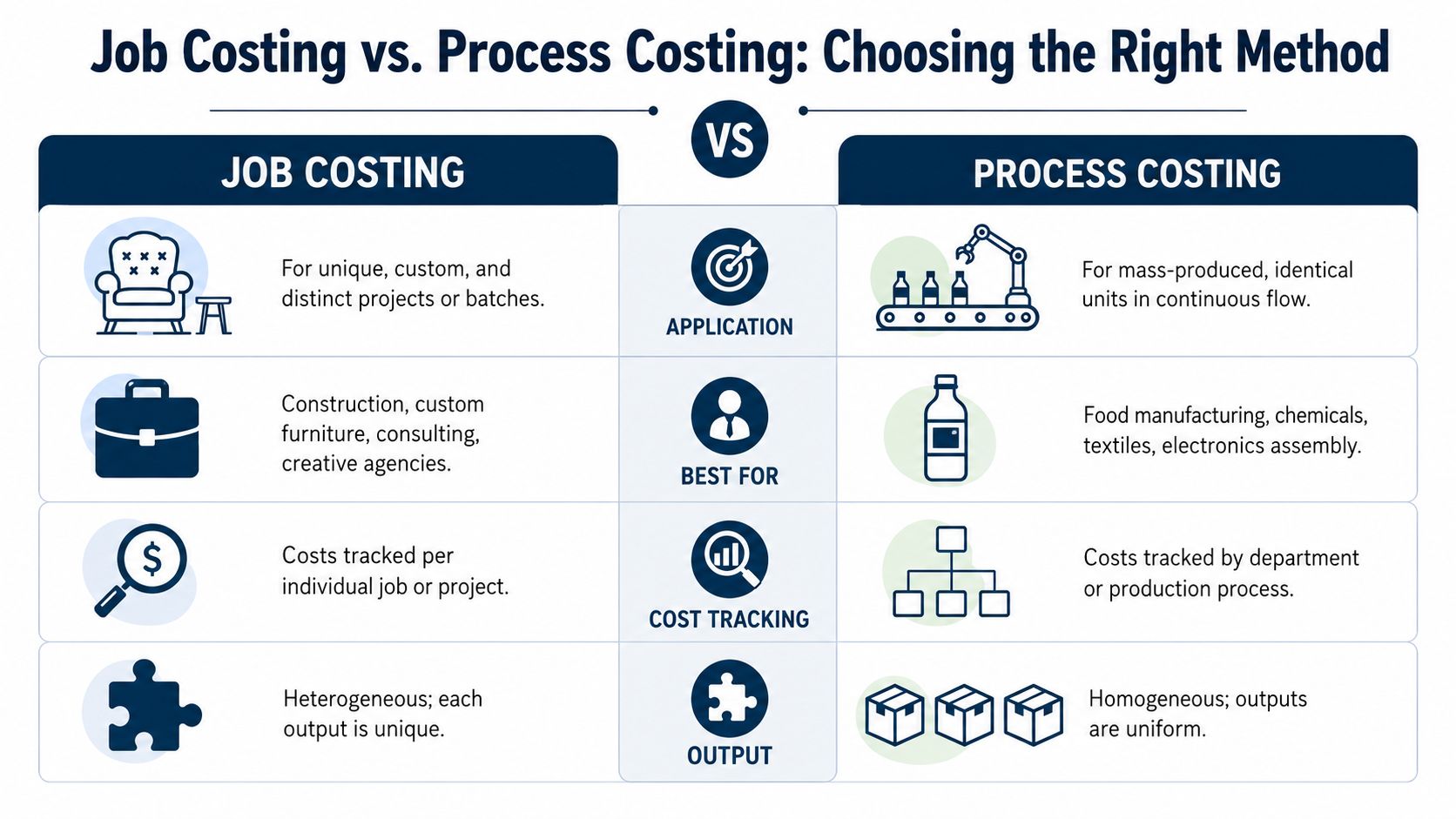

Job Costing vs Process Costing Which Is Right for You

Not every business needs job costing.

That's important because some owners hear “track everything by job” and start building a complicated system they'll never maintain. If your work is custom and each project consumes labor, materials, and overhead differently, job costing usually makes sense. If your work is repetitive and standardized, process costing is often the better fit.

That distinction matters because accounting guidance is clear that job costing is best for custom, order-specific work, while high-volume, standardized operations usually fit process costing better, as explained in Principles of Accounting's discussion of job costing.

The simple analogy

Think of a custom home builder versus a soda bottling plant.

The home builder works on projects that differ by customer, design, site conditions, labor mix, and material choices. Each house is its own financial story. That's job costing.

The soda plant makes large volumes of the same product again and again. It makes more sense to average costs across the production process. That's process costing.

Job costing vs process costing at a glance

| Attribute | Job Costing | Process Costing |

|---|---|---|

| Type of work | Custom, distinct, order-specific | Repetitive, standardized, continuous |

| Best for | Construction, consulting, agencies, legal work, custom manufacturing | Food production, chemicals, textiles, high-volume assembly |

| How costs are tracked | By individual job or project | By department or production process |

| Output | Each job can differ | Units are generally uniform |

| Main benefit | Shows profitability by project | Simplifies costing for identical output |

| Main drawback | More admin work | Less useful for unique jobs |

A quick test for owners

Ask yourself these questions:

- Does each client job look different from the last one

- Do labor hours vary a lot from project to project

- Do materials or outside purchases change by job

- Would one bad estimate hurt margin in a noticeable way

- Do you need to know which types of projects to price higher, avoid, or sell more often

If you're answering yes to most of those, job costing is probably worth the effort.

If your operation mostly produces the same thing in the same way, over and over, a detailed job-cost system may create more paperwork than value.

The right system is the one your team will actually use consistently. A perfect method that nobody updates is worse than a simpler method that stays current.

The trade-off nobody should ignore

Job costing creates administrative burden. That's not a flaw. It's the cost of getting better visibility.

For some businesses, the payoff is obvious because one bad project can wipe out the profit from several good ones. For others, especially standardized operations, detailed job tracking won't change many decisions.

That's why the question isn't “Is job costing good?” It's “Does my business make enough custom decisions that job-level visibility will improve pricing, staffing, and scope control?”

How Job Costing Looks in Your Industry

Job costing means different things depending on the business. The idea stays the same, but the blind spots change.

Construction

In construction, owners often know materials are expensive but underestimate how much money gets lost in labor drift, subcontractor coordination, and poor cost coding. A kitchen remodel can look fine from the top line until extra site visits, cleanup time, and change orders pile up.

A workable system usually tracks costs in near real time through job codes, time sheets, purchase orders, and general ledger reconciliation. Construction teams often break costs into jobs, phases, cost codes, and classes so they can see profitability at a more detailed level, as explained in this guide to construction job costing.

A contractor who only reviews cost after completion is late. A contractor who sees overruns by phase still has options.

Professional services

For agencies, consultants, IT firms, and law offices, the biggest issue is usually labor.

A project may be sold on a clean scope and a nice fee. Then senior people spend too much time on calls, revisions, internal reviews, and client hand-holding. None of that feels dramatic in the moment. Added together, it changes the economics of the job.

Good job costing in a service business often answers questions like:

- Which client types require the most unplanned time

- Which service packages are easy to deliver

- Which managers keep projects tight

- Where fixed fees are too low for the actual effort involved

That's how a service firm moves from “we're busy” to “we know what busy is worth.”

Healthcare

Healthcare owners don't always think in terms of job costing, but the logic still applies when work can be tied to a specific service line, case type, or procedure.

A clinic might want to understand the labor, supplies, and support burden behind a specific service. The challenge is that some costs are direct and visible, while others sit in shared staff, admin support, scheduling, and facility overhead. Without a disciplined method, one service can appear stronger than it really is.

This matters when you're deciding what to expand, what to price differently, or where staffing is out of sync with demand.

In every industry, the blind spot is the same. Owners see effort. Job costing shows whether that effort produced margin.

Real estate and property services

This also shows up in property management, maintenance, and specialty field services.

One property may seem easy because the monthly fee looks solid. But if tenant issues, service coordination, emergency calls, and admin time are constantly higher than expected, the account can become a low-margin drain. Job-level or property-level costing gives owners a cleaner basis for pricing and staffing.

The pattern repeats across industries. When work is custom, mixed, or service-heavy, broad averages hide the truth.

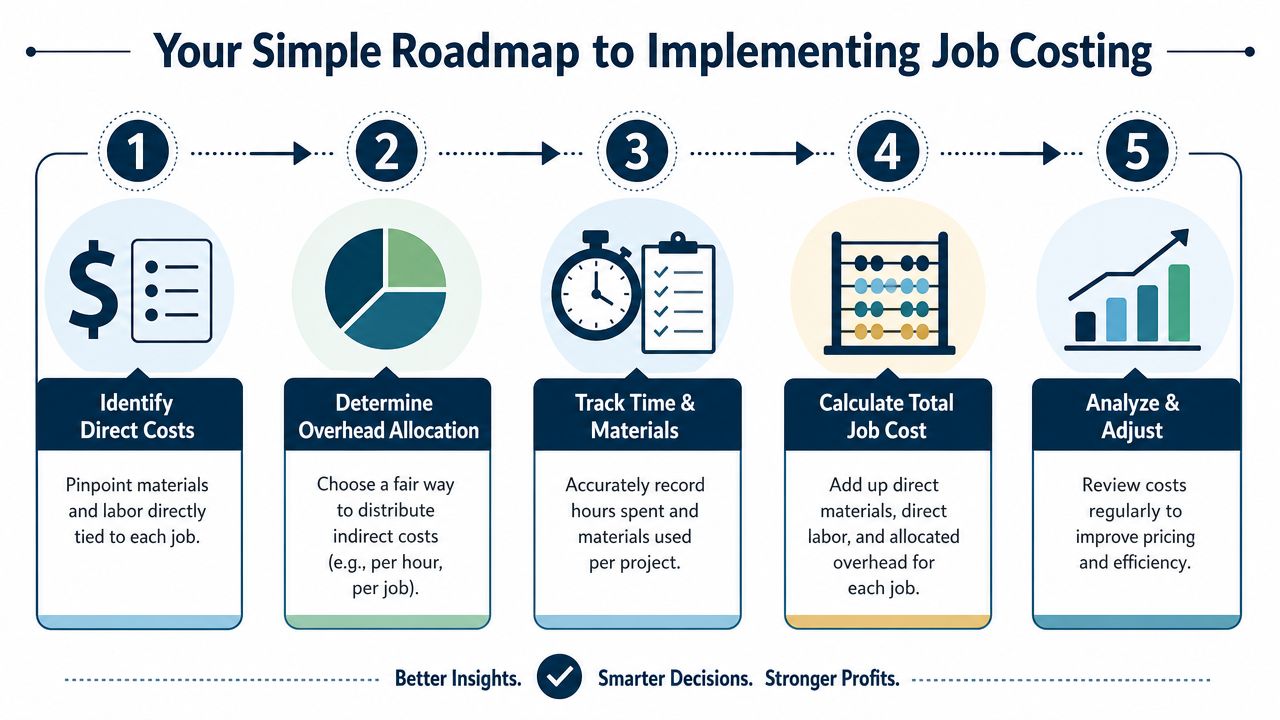

A Simple Plan to Start Job Costing in Your Business

Most small businesses don't need a giant software rollout to start. They need a usable process.

A functional job-cost system depends on recording costs in near real time using job codes, time sheets, and purchase orders. That level of detail lets you analyze profitability and take corrective action before a loss becomes irreversible, according to Foundation Software's guide to construction job costing.

Start with a simple structure

You don't need dozens of cost codes on day one.

Start with a few clear categories that match how your business operates:

- Labor for time spent delivering the work

- Materials for purchases tied directly to a job

- Subcontractors or outside services if that's common in your model

- Overhead allocation based on a rule you can apply consistently

If you're a contractor, you can get more detailed over time by adding phases or trade-specific codes. If you're an agency or consulting firm, start with clients, project names, and labor categories.

Pick one way to allocate overhead

Many owners freeze at this point. Don't.

Choose one fair method you can explain and repeat. Labor hours are common because they often reflect how much support and business infrastructure a job consumes. The exact method matters less than using it consistently and reviewing whether it still makes sense.

If you're in remodeling or trades, looking at a basement remodel cost estimate can be a helpful reminder of how many separate cost inputs a single project can carry before overhead is even considered.

Build the habit before you build complexity

A simple system works if your team uses it every week.

That usually means:

Create a job code before work starts

Every job needs a place for costs to land.Require time entry against that code

If labor isn't captured, the whole picture is off.Tag purchases and invoices to the same job

Materials and outside costs need the same discipline.Review estimate versus actual regularly

Don't wait until year-end.

Small businesses usually fail at job costing for process reasons, not math reasons.

Use tools that match your size

A spreadsheet can work if the business is still simple and someone owns the process. Basic accounting software plus disciplined coding can also work. As jobs, teams, and reporting needs grow, owners often move toward more integrated systems or outside support.

What matters most at the start is clean inputs. Messy data produces bad decisions, even in expensive software.

From Data Entry to Smarter Decisions with MyOfficeOps

Collecting job-cost data is only the first step. The payoff comes when that data changes what you do while the job is still active.

That's where many businesses fall short. They record costs, close the month, and file the report away. By then, the chance to protect margin may already be gone. Job costing is most useful when it informs decisions during the project, such as repricing change orders, adjusting staffing, or catching scope creep before the damage sticks, as noted in Deltek's discussion of job costing as a live management tool.

What smart use looks like

A useful job-cost process helps an owner answer questions like:

- Should we approve this extra work at the current price

- Is this project manager keeping labor under control

- Did we underbid this type of job

- Should we stop selling this service package

- Which clients are worth keeping at the current fee

Those are operating decisions, not bookkeeping trivia.

Where owners usually get stuck

The weak points are usually simple:

- Data comes in late

- Time isn't coded consistently

- Materials sit in broad expense accounts

- Nobody reviews estimate versus actual until the job is over

- Reports exist, but nobody ties them to decisions

That's why some owners bring in outside accounting and advisory support. A firm like MyOfficeOps can help set up the coding structure, clean reporting flow, and review rhythm so job costing becomes part of management, not just data entry. If you're also trying to connect cost reporting to broader decision support, this overview of analytics consulting for growing businesses gives the bigger picture.

Used well, job costing changes how you price, hire, schedule, and choose work. Used poorly, it becomes one more spreadsheet nobody trusts.

The difference isn't the formula. It's whether the business uses the information in time to act.

If you want help turning job costing into something practical, MyOfficeOps works with small and midsize businesses on bookkeeping, reporting, profitability analysis, and CFO-level decision support. For owners who need cleaner books and clearer answers on pricing, staffing, cash flow, and project profit, that kind of support can make job costing usable instead of overwhelming.