You finish a full clinic day, glance at the bank balance, and think, “We're busy, so why does cash still feel tight?”

That question shows up in medical practices all the time. The schedule looks full. Claims are going out. Patients are being seen. But when it's time to decide whether to hire, add a provider, replace equipment, or open another location, the numbers feel foggy.

That's where bookkeeping for medical practices has to do more than keep records tidy. It has to tell you what's going on between the exam room and your bank account. If the books only show money in and money out, but not why cash is late or where revenue is getting stuck, you're making decisions with half the story.

A good bookkeeping system works like a monitor in an exam room. It doesn't treat the problem by itself, but it shows the vital signs early enough for you to act. When the setup is right, you can see whether the practice is healthy, where the pressure is building, and what needs attention before it turns into a bigger mess.

Your Practice's Financial Health Is on the Line

A lot of owners live in the same loop.

You see patients all week. Your front desk collects copays. Insurance payments hit the account. Bills get paid. Payroll runs. On paper, the practice looks active and productive. But then a simple question comes up, like whether you can afford another MA or whether a service line is making money, and nobody can answer quickly.

That's not because you're bad at business. It's because healthcare money moves in a way that hides the truth unless the books are built for it.

One practice owner described it to me like this: “We're collecting money every week, but I still don't know what I can trust.” That's the right way to put it. The problem usually isn't effort. It's visibility.

Busy doesn't always mean profitable

Medical practices can look strong from the outside while cash slips through the cracks inside. A claim gets denied and sits too long. A payment posts to the wrong bucket. Billing totals and accounting records stop matching. A provider seems productive, but the service mix and reimbursement pattern tell a different story.

Clean books don't just show what happened. They show whether the practice can make the next decision safely.

When owners don't have that clarity, they start managing by instinct. Sometimes instinct is useful. It just shouldn't be your only financial system.

What a healthier setup feels like

Once bookkeeping for medical practices is tied to the revenue cycle, the questions get easier to answer:

- Can we afford this hire: You can see cash flow trends and whether collections support added payroll.

- Which payer is slowing us down: You can spot where receivables are aging.

- Are we growing or just getting busier: You can separate volume from real profitability.

- Why is cash inconsistent: You can trace delays back to billing, denials, posting, or patient balances.

That's the shift. You stop treating the finances like a pile of reports and start reading them like a chart.

Why Your Practice Needs More Than Basic Bookkeeping

A patient is seen on Tuesday. Staff submit the claim on Wednesday. The money may not hit your bank account for weeks, and part of it may never arrive without rework. That gap is why a medical practice cannot rely on basic bookkeeping built for simpler businesses.

In a retail business, the sale and the payment usually happen at the same time. In a medical practice, revenue moves through a cycle with handoffs, delays, write-offs, denials, and partial payments. If the books only record bank deposits and monthly expenses, they miss the part of the engine that determines cash flow.

A better setup ties bookkeeping to the revenue cycle. It shows not just what was deposited, but what is still pending, what is aging, and where reimbursement is slowing down.

Timing changes what the books need to do

Healthcare revenue has a lag built into it. Services are provided first. Payment depends on claim submission, payer processing, contract terms, patient responsibility, and follow-up. That creates a bookkeeping problem basic systems do not solve well.

If deposits are entered without matching them back to claims activity, the books can look clean while cash performance keeps getting worse. The practice sees money coming in, but cannot tell whether collections are keeping pace with production, whether receivables are drifting older, or whether posting issues are masking a billing problem.

That is the difference between bookkeeping that records history and bookkeeping that helps manage the business.

High fixed costs make delay expensive

Medical practices carry heavy ongoing costs. Payroll keeps running. Rent is due. Supplies are ordered before insurers pay. A few slow weeks in collections can tighten cash fast, even when the schedule is full.

That is why a generic setup breaks down in predictable ways:

- Deposits get treated as revenue truth: The practice loses sight of what is still sitting in A/R.

- Insurance and patient payments get blended together: It becomes harder to spot whether payer performance or patient collections are causing the slowdown.

- Adjustments and write-offs stay too broad: Contractual adjustments, refunds, and bad debt start to blur together.

- Billing problems stay outside the books: Owners hear that cash is slow, but cannot trace whether the cause is coding, denials, credentialing, or posting delays.

I see this often. The practice owner reviews the P&L, sees revenue posted, and still cannot answer a simple question: is cash late because the practice is under-collecting, or because the revenue cycle is clogged?

Specialized bookkeeping gives you control points

Good bookkeeping for medical practices mirrors how money moves through the practice. It needs to track receivables in a way that supports decisions, not just tax prep.

That usually includes:

- A/R by payer and aging band: So slow-paying insurers stand out early.

- Patient versus insurance collections: So front-desk collection issues do not get buried inside total income.

- Adjustments by type: So normal contractual write-downs are separated from avoidable losses.

- Collections tied to provider, location, or service line: So growth is measured against reimbursement quality, not visit volume alone.

If your current bookkeeping cannot support that level of visibility, the problem may start with structure. A practice-specific chart of accounts for clearer reporting gives the books the categories they need to reflect the revenue cycle instead of flattening everything into one revenue number.

Practical rule: If the books cannot show where cash is delayed, they are incomplete for a medical practice.

Basic bookkeeping keeps score. Medical bookkeeping helps protect margin, spot reimbursement problems sooner, and give the owner a clearer read on whether the practice is getting healthier or just staying busy.

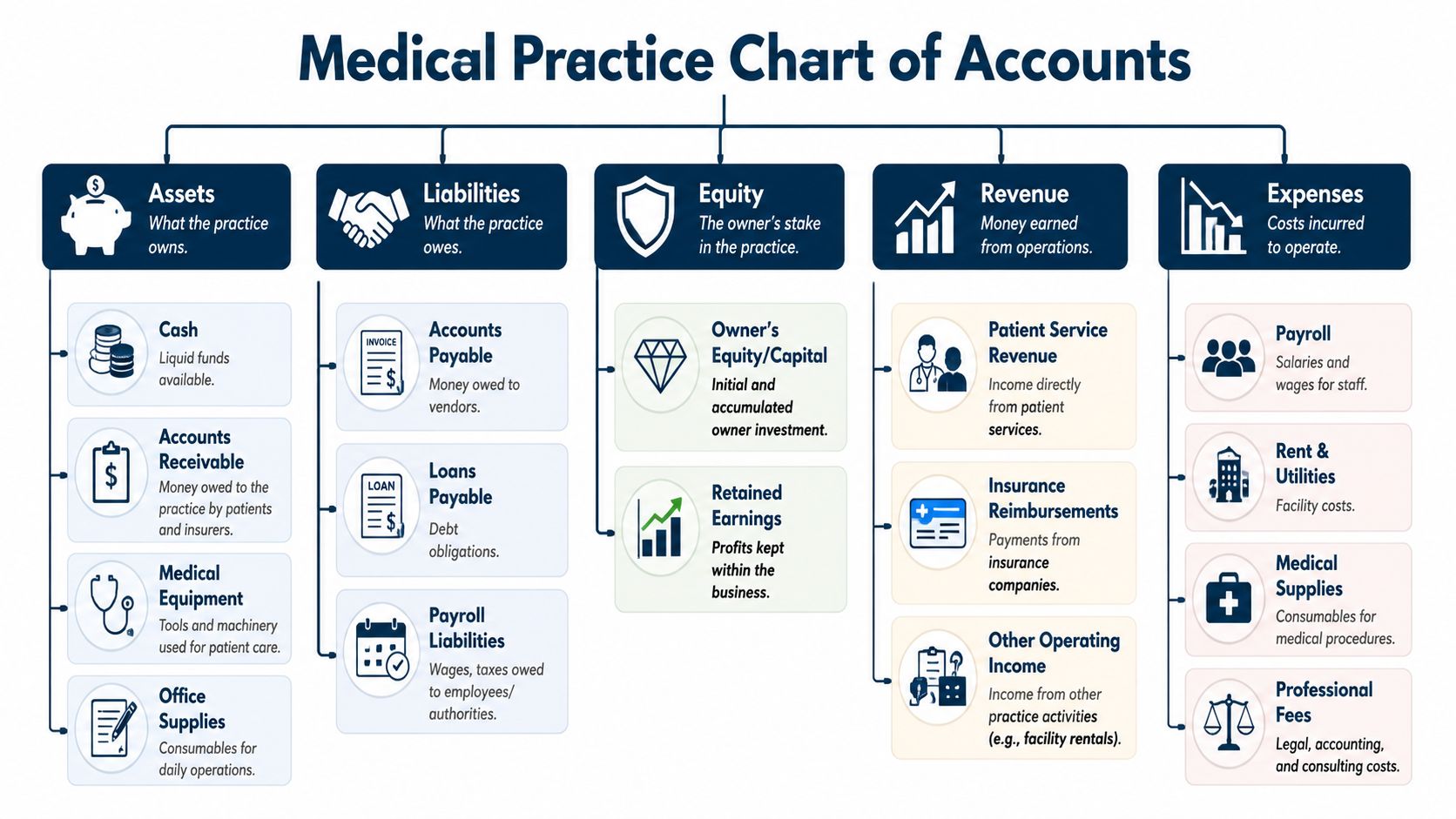

Setting Up Your Medical Chart of Accounts

Your chart of accounts is your filing cabinet. If the drawers are labeled badly, every report that comes out later will be blurry.

A generic chart of accounts gives you broad folders like income, expenses, and liabilities. That's not enough for a medical practice. You need categories that match how you get paid and how you spend.

Build the cabinet around how the practice runs

Industry guidance recommends separating income and expense categories for different service types, insurance payments, and patient payments, because that makes profitability by location, provider, or service line visible in a way a generic P&L never can, as noted in this guidance on healthcare bookkeeping structure.

That separation matters more than most owners think.

If all income lands in one top-level bucket called “medical revenue,” you can't easily answer basic questions. Are self-pay collections improving? Are insurer payments lagging? Is ancillary income helping margin or distracting from the core practice?

A cleaner setup starts with a chart of accounts that reflects reality. If you want a plain-English overview of the framework itself, this short guide on what a chart of accounts is is a useful reference.

A simple example that works

You don't need a giant account list. You need the right one.

A practical setup often includes categories like these:

- Revenue from insurance payments: Keep insurer reimbursements separate from patient-paid amounts.

- Revenue from patient payments: Copays, deductibles, self-pay visits, and other direct patient collections should stand on their own.

- Other operating income: Use a separate category for things that aren't standard clinical reimbursement.

- Clinical supplies and medical consumables: Don't bury these inside general office expenses.

- Payroll by role: Provider pay, clinical staff pay, and admin payroll are easier to analyze when they aren't mixed together.

- Facility costs: Rent, utilities, and occupancy costs should be grouped clearly.

What not to do

The biggest chart-of-accounts mistake is over-compressing the books. Owners often think a shorter P&L means a simpler business. It usually means the detail got buried.

Another common mistake is overbuilding the chart with too many tiny categories no one uses consistently. When that happens, staff guess. Guessing creates misclassification, and misclassification leads to bad decisions.

If one provider, one location, or one revenue stream is carrying the practice, your chart of accounts should make that visible without a detective story.

A good chart of accounts is boring in the best way. It makes monthly reporting easier, cleaner, and much more useful.

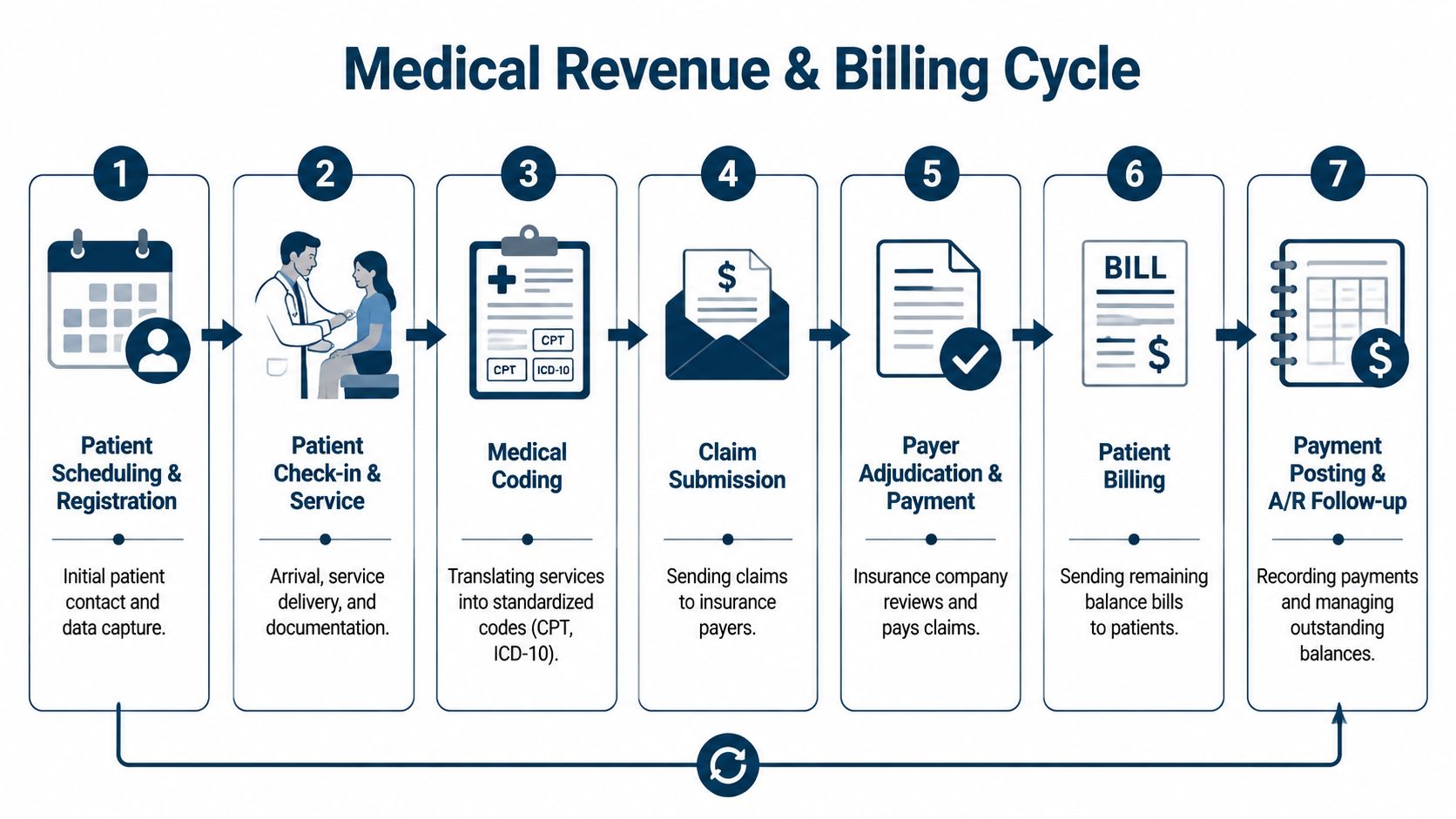

Navigating the Medical Revenue and Billing Cycle

Friday afternoon is a common moment for this problem to show up. The schedule was full all week, providers were busy, and the bank balance still feels thinner than it should. In a medical practice, that gap usually starts inside the revenue cycle, not in the appointment book.

A patient is seen. Charges are entered. A claim is submitted. The payer processes it, reduces part of it under the contract, pays what it approves, and shifts the rest to patient responsibility. Your books need to follow that whole chain. If they only capture the visit and the deposit, they miss the full story about cash flow.

Follow one visit from care to cash

Take one routine visit. The provider sees the patient on Tuesday, but the money may arrive in pieces over several weeks. Insurance pays first, or denies and asks for more work. The patient balance may sit longer, especially if the first statement goes ignored.

That timing difference matters. Medical revenue does not move in a straight line from appointment to cash. It moves through a system of claims, adjudication, adjustments, rework, payment posting, and patient collections. A clear healthcare revenue cycle management process helps the practice track where each dollar stands instead of treating every unpaid balance like the same problem.

Bookkeeping has to mirror that reality. Otherwise, owners see production on one report, receivables on another, and cash in the bank telling a different story.

Where practices lose money without noticing

Revenue rarely disappears because of one dramatic breakdown. It leaks out through routine errors and slow follow-up.

A front-desk mistake can send a claim out with bad insurance information. A coding error can push a clean claim into rework. A contractual adjustment posted to the wrong account can make receivables look collectible when they are not. A denial left untouched for three weeks turns into an aging problem. Small patient balances pile up when statements go out but no one owns collection follow-up.

These are billing problems on the surface. They are bookkeeping problems too, because each one changes what should be recorded as revenue, what still belongs in accounts receivable, and what is realistically going to convert to cash.

Reconciliation is where the practice gets the truth

The monthly close should force three records to agree. The practice management or billing system shows what was charged and how claims moved. The accounting system shows what was recorded. The bank account shows what came in.

When those records do not line up, the issue usually falls into one of a few buckets. Deposits were posted incorrectly. ERA payments were applied to the wrong date or wrong payer. Contractual adjustments were overstated or missed. Patient payments hit the bank but never cleared the receivables report. Sometimes the books look clean while aging, denials, or unapplied cash say otherwise.

That is why reconciliation matters so much in a medical practice. It closes the gap between activity and cash.

Reconciliation is the point where production, billing, and bookkeeping have to agree on the same version of events.

Done well, this process shows where the revenue cycle is healthy and where it is dragging down cash flow. Done poorly, it creates false confidence. The practice keeps working hard, but the books hide delayed payments, weak collections, and profit that exists on paper only.

The Few Financial KPIs That Actually Matter

A practice can look busy all month and still end up short on cash. The usual reason is simple. Owners are reviewing reports that describe activity, not reports that show whether the revenue cycle is turning work into money.

The right KPI dashboard works like an instrument panel. It should tell you, in a minute or two, whether claims are moving cleanly, receivables are aging too long, and patient balances are being collected before they become harder to recover.

The starter dashboard

For many small and midsize practices, five metrics give a clear view of financial performance: net collection rate, days in accounts receivable, claim denial rate, first-pass resolution rate, and point-of-service collections. This medical practice revenue-cycle dashboard guide is a useful reference for that core set.

If I had to start with one, I would start with net collection rate because it ties billing performance to cash in the bank. A healthy rate usually means the practice is collecting the reimbursement it was entitled to collect after contractual adjustments. A weak rate usually means revenue is leaking somewhere between charge entry, claim submission, follow-up, and patient collections.

What each KPI is showing you

Each number answers a different question.

- Net collection rate: How much collectible revenue became cash.

- Days in A/R: How long the practice waits to get paid.

- Claim denial rate: How often claims are rejected, delayed, or sent back for correction.

- First-pass resolution rate: How often claims are paid without rework.

- Point-of-service collections: How much patient responsibility is collected before the patient leaves.

That set is small on purpose. A medical practice does not need fifty metrics to run well. It needs a short list tied to decisions.

Read the dashboard as one financial system

One KPI in isolation can give false comfort.

Collections can look fine because older claims finally cleared, while current claims are being denied at a higher rate. Days in A/R can stay in range while front-desk collections slip, which means more balances move to statements and more staff time gets pulled into follow-up. First-pass resolution can weaken before the income statement shows a problem, because the cash impact usually arrives later.

That is why bookkeeping and revenue cycle reporting have to connect. Clean books show the result. These KPIs show where the result is being created or lost.

A useful KPI leads to a decision. If a number does not change what your team reviews, fixes, or follows up on, it does not belong on the dashboard.

One more point matters here. The systems used to track claims, payments, and patient balances need secure access controls and protection against avoidable risk. If your billing and finance workflows touch patient data, comprehensive cyber protection supports the operational side of financial management too.

For many owners, this short dashboard is enough. It catches slow cash, preventable denials, weak front-desk collection habits, and the early signs that profitability on paper is not turning into usable cash.

Managing Payroll and PHI Compliance Safely

Payroll and patient data protection usually sit in different mental buckets. In a medical practice, they overlap more than people think.

Payroll touches provider compensation, staff wages, bonuses, taxes, benefits, and access to sensitive records. At the same time, many finance workflows include patient names, balances, claim details, or supporting documents. That means a sloppy process can create both tax problems and privacy problems.

Payroll errors spread fast

When payroll is handled loosely, the damage doesn't stay in one place. It affects trust, taxes, and reporting.

The biggest issue is often classification. If a practice treats someone like an independent contractor while managing them like an employee, that can create tax and compliance trouble. The same goes for unclear bonus structures or provider compensation that isn't mapped cleanly in the books.

A safer setup usually includes:

- Defined compensation rules: Put salary, bonus, and benefit treatment in writing before payroll runs.

- Consistent account mapping: Provider pay, payroll taxes, benefits, and reimbursements should land in the right accounts every month.

- Clear approval flow: Someone should review payroll changes before they hit the system.

PHI changes how your finance stack should be built

A normal small business might email invoices around casually. A medical practice can't assume that kind of workflow is safe.

If your bookkeeper, payroll provider, document storage, or communication tools touch protected health information, your process needs to reflect that. Use systems designed for healthcare sensitivity, limit access to what people need, and make sure vendors understand their role.

One practical place to start is with broader comprehensive cyber protection, especially if your finance and admin systems connect across billing, email, file sharing, and remote access. Medical practices don't just need convenience. They need controls.

Treat compliance like operating equipment

Owners sometimes see payroll compliance and PHI protection as admin overhead. It's better to think of them like sterilization procedures. They may not generate revenue directly, but skipping them creates a risk no serious practice should accept.

A safe process usually includes:

- Vendor review: Confirm who can access payroll records and patient-related financial data.

- Access limits: Front desk, billing, HR, and outside advisors should not all see the same information by default.

- Written agreements: If a third party handles sensitive healthcare-related data, the relationship should be documented properly.

- Routine review: Check permissions, workflows, and storage habits before a problem forces the review.

This is not optional. Good bookkeeping for medical practices has to protect the data it organizes.

When to Outsource Bookkeeping or Hire a CFO

A common breaking point looks like this. The schedule is full, collections look strong on paper, and the bank balance still feels tighter than it should. That usually means the practice does not have a bookkeeping problem alone. It has a revenue-cycle-to-cash-flow visibility problem.

At that stage, keeping everything in-house often costs more than it saves. Claims lag, deposits are hard to trace, provider compensation gets messy, and the monthly financials arrive too late to guide decisions. Clean tax-ready books are useful, but a medical practice needs books that explain why cash is late, where margin is slipping, and which revenue streams carry the business.

Outsourced bookkeeper versus CFO support

An outsourced bookkeeper handles the financial recordkeeping. That includes coding transactions correctly, reconciling bank activity, closing the month, and organizing reports so the numbers can be trusted.

A CFO-level advisor works one layer higher. The job is to turn those reports into decisions about hiring, pricing, expansion, owner pay, debt, and reserves. For a practice with insurance payments, patient balances, write-offs, memberships, and direct-pay services, that distinction matters. The books have to reflect how money moves through the revenue cycle, not just where it landed in the bank.

That is why some owners outgrow basic bookkeeping even when the bookkeeping itself is competent. They need help connecting collections delays, payer mix shifts, and rising overhead to actual profitability. If you want a clearer picture of what strategic finance support looks like, CFO services for small business is a useful reference point.

What to prepare before outsourcing

Outsourcing goes better when the incoming team can see both the accounting records and the operational reports behind them.

| Item to Prepare | Why It Matters in a Medical Practice |

|---|---|

| Access to accounting software | Gives the bookkeeping partner the full ledger, prior reconciliations, and the current setup for provider pay, expenses, and owner draws |

| Billing and practice management reports | Connects revenue on the books to claims activity, such as A/R aging by payer, denial reports, payment posting, refunds, and collection trends |

| Bank and merchant statements | Confirms whether insurance deposits, patient card payments, and other cash receipts match what was recorded |

| Payroll reports and provider comp details | Helps map wages, bonuses, payroll taxes, and provider compensation formulas correctly |

| Existing chart of accounts | Shows whether the practice can track lab income, ancillary services, procedure revenue, software costs, and outsourced billing separately |

| Vendor list and recurring payments | Surfaces duplicate tools, missed accruals, auto-drafts, and expenses that should be grouped differently for management reporting |

| User access list | Identifies who can view financial records, patient-related payment workflows, and connected admin systems |

When a CFO is the better next step

A CFO is usually the right addition when the owner keeps asking questions the monthly close cannot answer.

That often happens when the practice is adding a provider, opening another location, changing compensation plans, or trying to understand whether a service line is profitable after billing delays and overhead allocation. It also comes up before a sale, partner buy-in, or lender review, because those situations require more than tidy books. They require a financial story that holds together under scrutiny.

In medical practices, timing matters as much as totals. A profit and loss statement can look acceptable while cash is strained by slow payer reimbursement, rising patient A/R, or inconsistent follow-up on denials. A CFO helps model those pressure points before they become payroll stress or forced borrowing.

If outside support will touch records or workflows connected to protected information, review your process carefully. FaxZen's HIPAA compliance guide is a practical resource for tightening document handling before you hand off finance work.

Some firms cover both bookkeeping and advisory. MyOfficeOps is one example. The point is not the brand name. The point is getting support that matches the complexity of your practice and gives you a clearer line from revenue cycle performance to real cash flow.