A subsidiary ledger is the detailed record behind one summary account in your main books. It holds the transaction-by-transaction detail, like individual customer invoices that add up to your total Accounts Receivable in the general ledger.

If you've ever looked at your Profit & Loss or Balance Sheet and thought, “Okay, but what is this number made of?” you're already bumping into the reason subsidiary ledgers matter.

This comes up all the time with small business owners. The report says customers owe you money. Fine. But which customers? Which invoices are late? Did someone pay and the payment never get applied? Your main reports usually won't answer that on their own.

That's where the core work of bookkeeping starts. The summary reports tell you the score. The subsidiary ledger tells you the story behind it, and if that story is messy, the summary numbers can't be trusted.

Why Your Main Financial Reports Don't Tell the Whole Story

A business owner opens the monthly reports and sees a balance sitting in Accounts Receivable. It might look healthy. It might look worrying. Either way, the first question is usually the same. Who owes us that money?

The financial statements don't usually answer that question. They show totals. They are supposed to show totals. Historically, that was part of the whole design. The general ledger stayed organized as the main summary record, while the detailed records sat underneath it in subsidiary ledgers. That structure is still foundational now because the general ledger is used to prepare periodic financial statements, while subledgers hold the detail needed for audit trails and day-to-day review (Idealist Consulting on subsidiary ledgers).

The report gives you the total, not the trail

Think about a simple example. Your balance sheet shows an Accounts Receivable total. That tells you money is owed to the business. It doesn't tell you whether that balance is spread across many current invoices or tied up in a few old ones that nobody followed up on.

The same problem shows up in Accounts Payable. You may know what you owe in total, but not which vendor bill is due first, which one was entered twice, or whether a credit was missed.

Your reports can be technically complete and still not be useful enough to run the business.

Why owners get stuck here

Most owners don't need more accounting theory. They need to answer practical questions fast.

A subsidiary ledger helps with questions like these:

- Customer detail: Which client still owes for March's invoice?

- Vendor detail: Did we already enter that supplier bill?

- Asset detail: What equipment are we depreciating?

- Inventory detail: Which items make up the inventory balance on the books?

Without that detail, you end up guessing. And guessing with accounting numbers usually leads to one of two problems. Either you chase the wrong issue, or you miss the actual one.

The story behind the numbers

When people ask what is a subsidiary ledger, I usually explain it this way. It's the place where the summary number becomes understandable.

Your financial statements are still necessary. They're the clean version. But clean doesn't mean complete. If you want to know whether your books are reliable, you have to be able to trace a summary balance back to the underlying records that created it.

That's why the detail work matters so much. Clean books aren't just neat. They let you trust what you're looking at.

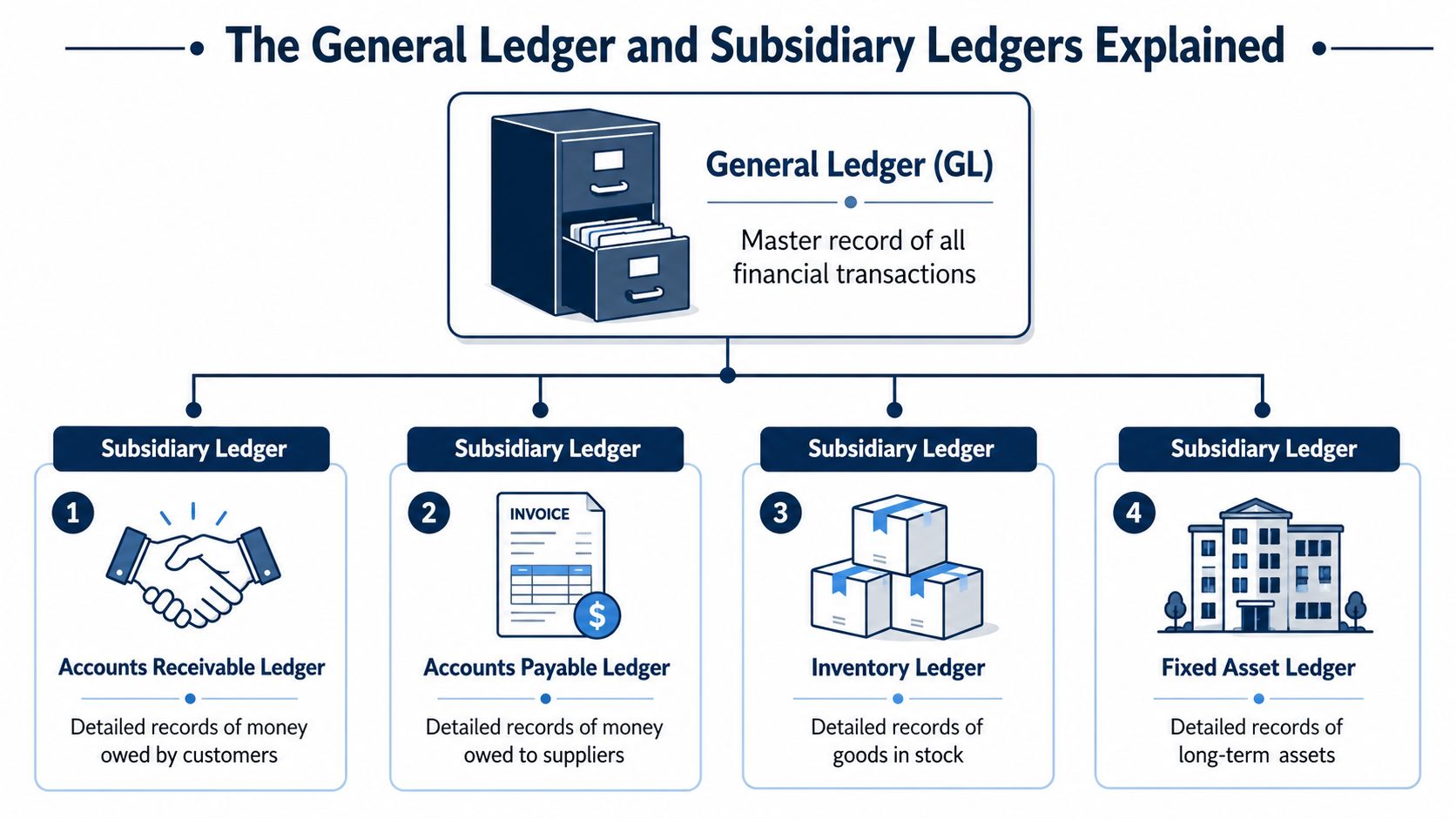

The General Ledger and Subsidiary Ledgers Explained

The easiest way to understand this is to picture a filing cabinet.

Your general ledger is the cabinet. It holds the main categories of your business records. Inside the cabinet are drawers for accounts like Accounts Receivable, Accounts Payable, Inventory, and Fixed Assets. If you want a refresher on the main record itself, this general ledger overview from MyOfficeOps is a useful starting point.

A subsidiary ledger is the set of folders inside one drawer. Instead of one total, it shows each individual item that makes up that total.

The cabinet, the drawers, and the folders

Here's the relationship in plain language:

| Record | What it does | Example |

|---|---|---|

| General ledger | Holds the summary balances used for financial statements | Accounts Receivable shows one total |

| Control account | The summary account in the general ledger tied to one detail area | The Accounts Receivable account |

| Subsidiary ledger | Holds the item-by-item detail behind that control account | One page or record for each customer |

A subsidiary ledger is a detailed record that supports one control account in the general ledger. The general ledger is the summarized system of record used to produce financial statements, while the subledger captures transaction-level detail for areas such as accounts receivable, accounts payable, fixed assets, or inventory. The subledger total must tie to the control account in the general ledger (HubiFi on general ledger vs subsidiary ledger).

Why this setup works

If every invoice, bill, stock movement, and asset update hit the main ledger as raw detail, the books would become hard to read fast. The summary structure keeps the main record usable.

The subledger does the opposite job. It preserves the detail so someone can investigate a number.

That division matters in real businesses because different people need different views:

- Owners usually want summary reports.

- Bookkeepers need the transaction detail.

- Collections or operations staff may need customer or vendor records, but not access to the full ledger.

- Accountants need both levels when reviewing balances.

Practical rule: If a balance matters enough to question, it matters enough to support with detail.

One control account, one detailed support file

A good way to check whether you're dealing with a real subledger is to ask one question. Does it support a single summary account in the general ledger?

If yes, you're likely looking at a subsidiary ledger. If it's just a random export with mixed transactions from all over the system, it's probably not.

That's an important distinction because the value of a subsidiary ledger isn't that it exists. Its value is that it supports one clean control account and can be checked against it.

Common Subsidiary Ledgers Your Business Will Use

Most small businesses don't need a long list of subledgers. They usually need a few core ones kept well.

The four that come up most often are Accounts Receivable, Accounts Payable, Inventory, and Fixed Assets. If those are sloppy, the reports built on top of them will be shaky too.

Accounts Receivable ledger

This is usually the first one owners recognize because it's tied directly to cash coming in.

Say you send invoices to ten clients each month. Your general ledger may show one Accounts Receivable total, but your receivables subledger shows each client, each invoice, each payment, and what's still open. For accounts receivable, the subsidiary ledger is often the source of truth for each customer's open balance, and the sum of those balances should tie to the Accounts Receivable control account in the general ledger. It also lets teams inspect invoice dates, remittances, discounts, and returns without exposing the full general ledger to every user (AccountingCoach on subsidiary ledgers and control accounts).

That's why a customer can call and ask, “Why do you say I owe this?” and a good bookkeeper can answer quickly.

Accounts Payable ledger

This one tracks what you owe vendors and suppliers.

A lot of small businesses think of payables as just “bills to pay.” But the detail matters. You want to know which invoice belongs to which vendor, when it's due, whether a credit memo exists, and whether someone accidentally entered the same bill twice.

If you're tightening up that process, especially if you handle a lot of contractor or supplier invoices, a practical resource on how to automate accounts payable for UK freelancers can help you think through workflow, approvals, and document handling.

Inventory ledger

If you sell products, inventory detail matters more than many owners expect.

Your balance sheet may show one inventory number. The inventory subledger tells you what items make up that number. It helps answer questions like which products are sitting too long, which items were received but not recorded properly, and where the stock value on the books came from.

When inventory is wrong, profit is often wrong too. That's why this subledger needs attention even in a smaller operation.

Fixed assets ledger

This is the record for long-term items like equipment, vehicles, furniture, or property improvements.

A fixed asset subledger usually tracks each asset separately. That makes it easier to see what you bought, what's still on the books, and whether something old is hanging around in the records even though you no longer use it.

I see this one get ignored a lot. Then at year-end, someone asks why a disposed asset is still sitting on the balance sheet.

A quick view of the common ones

| Subsidiary Ledger | What It Tracks | Key Question It Answers |

|---|---|---|

| Accounts Receivable | Customer invoices, payments, credits, open balances | Who owes us money right now? |

| Accounts Payable | Vendor bills, payments, credits, due dates | What do we owe, and when is it due? |

| Inventory | Item-level stock records and value details | What products make up the inventory balance? |

| Fixed Assets | Individual long-term assets and related records | What assets do we own and still carry on the books? |

Which one matters most

That depends on the business.

A service firm may live and die by Accounts Receivable because unpaid invoices squeeze cash. A contractor may focus hard on payables and job-cost detail. A retail or product business usually can't ignore inventory for long.

The right answer isn't “track everything in extreme detail.” The right answer is to keep detailed support where a summary number by itself isn't enough to manage the business.

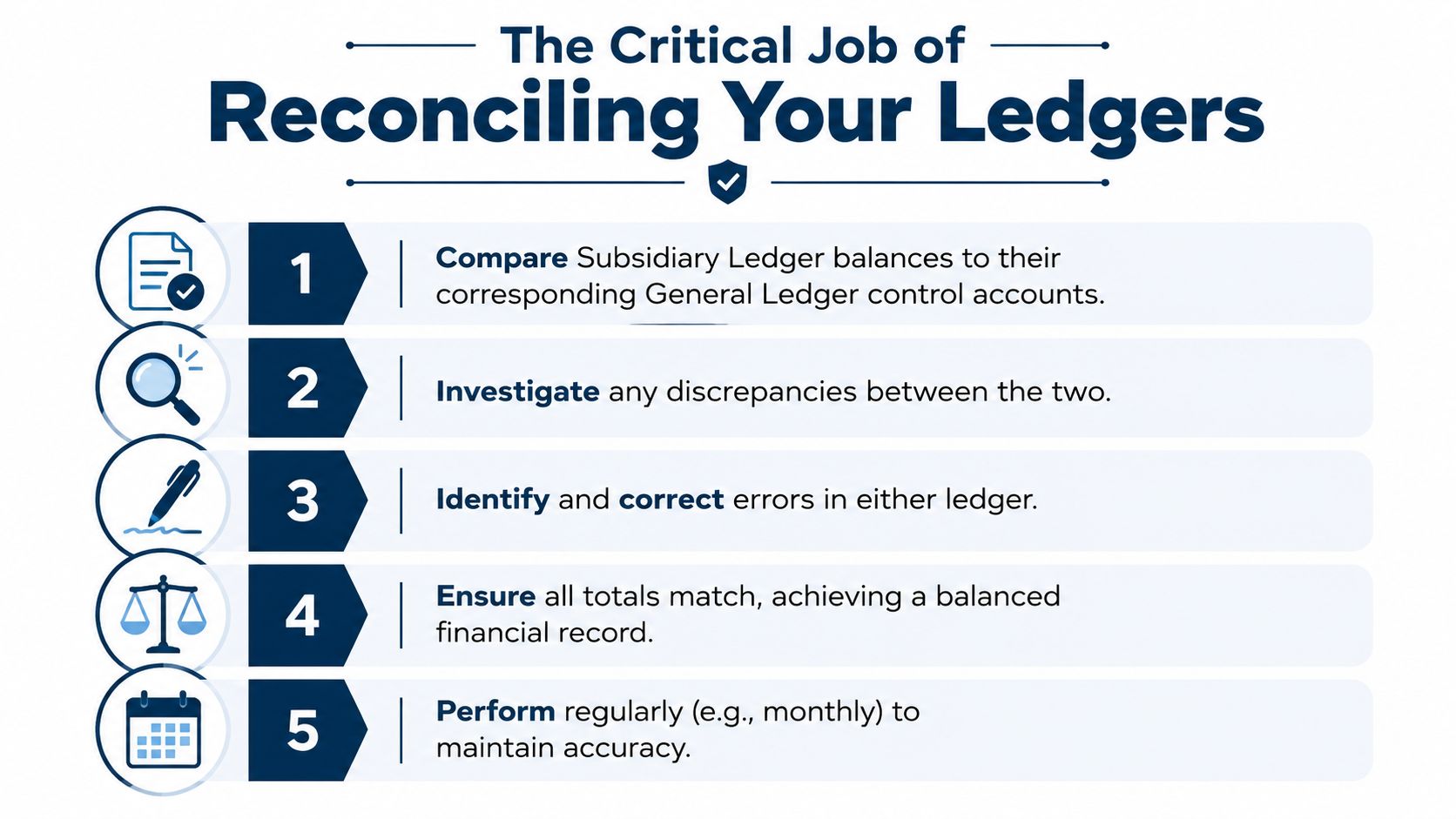

The Critical Job of Reconciling Your Ledgers

A subsidiary ledger doesn't help much if nobody checks it against the general ledger.

This is the part many guides rush past, but it's the part that keeps books honest. The value of a subsidiary ledger is not its existence, but whether teams can reconcile it monthly. During this monthly reconciliation, invoice-level errors, duplicate postings, and timing differences become visible before they distort cash flow reporting, and for small and midsize businesses this is the main operational issue, not a side note (Aico glossary entry on subsidiary ledgers).

What reconciliation actually means

In plain terms, reconciliation means making sure the detail equals the summary.

If your Accounts Receivable subledger says all customer balances together equal one amount, then the Accounts Receivable control account in the general ledger should show that same amount. If it doesn't, something is off.

Sometimes it's small. A payment hit the bank but wasn't applied to the customer account. A bill was entered in one place but not posted correctly in another. A duplicate invoice slipped in.

Sometimes it's bigger. A workflow changed, access controls were loose, or staff started using the software inconsistently.

What good reconciliation catches

Monthly reconciliation helps uncover issues like:

- Duplicate postings: The same bill or invoice entered twice

- Timing differences: A transaction recorded in one ledger but not fully posted to the other yet

- Misapplied cash: A customer paid, but the payment was attached to the wrong invoice or customer

- Old balances: Items sitting open that should have been cleared months ago

- Broken process steps: System imports or manual workarounds that stop the ledgers from lining up

If the subledger and the control account don't match, don't trust the summary until you know why.

Why monthly is the practical rhythm

Waiting until year-end is where small bookkeeping problems become expensive cleanup projects.

Monthly is usually the sweet spot because it gives you enough activity to review meaningfully, but not so much that the investigation becomes a scavenger hunt. If your team still does some work in spreadsheets, a guide for finance teams on Excel reconciliations can help standardize the review process so things don't live only in one person's head.

A lot of owners understand bank reconciliation but don't realize the same mindset applies here. This bank account reconciliation resource from MyOfficeOps is useful because the habit is similar. Compare records, find the difference, correct it, and document what happened.

What works and what doesn't

What works:

- Close on a schedule: Reconcile subledgers every month, not “when there's time.”

- Assign ownership: One person should know who reviews receivables, payables, and other detail ledgers.

- Keep support handy: Invoices, credits, payment records, and notes should be easy to pull.

- Fix root causes: If the same mismatch keeps happening, the process is broken.

What doesn't:

- Relying on software totals alone

- Posting manual adjustments without notes

- Letting old unmatched items pile up

- Assuming a small difference doesn't matter

Small differences often point to bigger process problems. That's why reconciliation isn't busywork. It's quality control for the numbers you use to make decisions.

Common Mistakes to Avoid with Subsidiary Ledgers

Most subledger problems aren't caused by hard accounting issues. They're caused by basic process mistakes repeated over time.

The good news is that these are fixable if you catch them early.

Duplicate names and duplicate records

A very common issue is setting up the same customer or vendor more than once.

That leads to split balances. One invoice sits under one name, the payment sits under another, and now the owner thinks a client hasn't paid when they have.

Fix: Clean up naming rules. Decide how customer and vendor records are created, and limit who can create new ones.

Posting detail inconsistently

This happens when transactions are entered in a way that doesn't flow cleanly into the control account.

Maybe someone posts an invoice in a customer module, but then someone else makes a manual journal entry to “fix” the balance without correcting the original issue. The reports can look patched together, but the underlying records won't make sense.

Fix: Enter transactions through the right workflow first. Use manual adjustments carefully and document why they were needed.

Watch for this: If your summary balance looks right but the detail report looks confusing, the books may be balanced in appearance only.

Falling behind on reconciliation

This is the one that hurts the most because it snowballs.

One skipped month turns into a quarter. Then nobody remembers why a transaction was posted a certain way, who approved a credit, or whether an old open invoice is real.

Fix: Put reconciliation on the close checklist and treat it like paying payroll. It has to happen.

Giving too much access

Not everyone needs the ability to edit customer balances, vendor records, or historical entries.

When too many people can change subledger detail, mistakes become hard to trace. In cloud systems, that can happen fast because several users may be working at once.

Fix: Limit access based on job role. Let people see what they need, not everything.

Keeping “temporary” workarounds forever

Some businesses start using side spreadsheets to track unpaid invoices, inventory corrections, or asset changes “just for now.”

Then the spreadsheet becomes the unofficial ledger, and nobody is sure which record is correct.

Fix: Use one primary system of record. If a spreadsheet supports the process, it should support it, not replace it.

A clean subsidiary ledger should answer questions quickly. If looking something up creates more confusion, that's a sign the setup or process needs attention.

When to Stop DIYing and Get Professional Help

There's a point where doing the books yourself stops saving money and starts costing you time, confidence, and sometimes sleep.

That point usually isn't dramatic. It sneaks up on you. You spend evenings trying to figure out why customer balances don't match. You delay sending reports because you don't trust them. You keep meaning to clean it up next month.

Signs you've hit the limit

A few red flags show up again and again:

- You can't get ledgers to tie out: The subledger and control account keep disagreeing.

- You avoid looking at reports: Not because you don't care, but because you don't trust the numbers.

- Bookkeeping spills into owner time: Nights, weekends, or catch-up sessions before tax deadlines.

- Your system has outgrown your process: More customers, more bills, more staff, and no tighter controls.

- You rely on memory: You know why something was done, but nothing is documented.

If two or three of those sound familiar, it may be time to hand the detail work to someone who does it every day.

What outside help should actually do

Good outsourced support shouldn't just produce reports. It should maintain the detail underneath the reports so the numbers hold up.

That can include keeping receivables and payables ledgers clean, reconciling them regularly, documenting adjustments, and making sure the financial statements reflect what's really happening in the business. For owners comparing options, this overview of the advantages of outsourcing bookkeeping services is a practical read.

One option in this space is MyOfficeOps, which provides bookkeeping, accounting support, payroll integration, reporting, and advisory services for small and midsize businesses. For a business owner, that usually means fewer loose ends in the books and a clearer handoff between daily bookkeeping and bigger financial decisions.

You don't need to know everything yourself

A lot of owners feel like they should be able to manage this alone because “it's just bookkeeping.”

It isn't simple once your business has real volume, multiple users, or messy carryover from past months. The goal isn't to become an expert in subsidiary ledgers. The goal is to have clean enough records that you can make decisions without second-guessing the numbers.

If your reports feel more confusing than helpful, MyOfficeOps can help you get the detail work under control. That includes keeping ledgers organized, reconciling balances, and turning messy accounting records into numbers you can use.