A general ledger is the main financial record for your business. Think of it like a big book where every single dollar you earn, spend, own, or owe is written down.

It’s the complete, official story of your company's money.

Your Business's Financial Filing Cabinet

Imagine you have a big filing cabinet for all your business's money stuff. This cabinet has five main drawers, and each one is for a different type of financial activity.

Every time money moves in your business—you send an invoice, a customer pays you, you buy a new computer—the details of that transaction go into one of these drawers.

This system turns what could be a messy pile of receipts and bills into a clear picture of your finances. When you buy that new computer, the record goes into the "Assets" drawer. When you pay your monthly rent, it goes into the "Expenses" drawer. Every dollar has a home.

The Five Core Account Types

To really get it, you need to know about the five main "drawers" in this financial filing cabinet. Every single thing you do with money will fit into one of these five groups.

Here’s a simple breakdown of what they are.

The Five Building Blocks of Your General Ledger

| Account Type | What It Means in Simple Terms | Real-World Example |

|---|---|---|

| Assets | Stuff your business owns that has value. | Cash in the bank, company vehicles, or computers. |

| Liabilities | What your business owes to other people. | Business loans, credit card balances, or unpaid bills. |

| Equity | The owner's stake in the company. | What's left over if you sold all assets and paid all debts. |

| Revenue | Money your business earns from its activities. | Sales from products, fees for services, or subscription income. |

| Expenses | Money your business spends to operate. | Rent, employee salaries, and marketing costs. |

Understanding these five categories is the first step to knowing how your business is really doing.

Keeping a central record of money isn't a new idea. Archaeologists have found clay tablets from over 5,000 years ago in Mesopotamia. People used them to keep track of things like grain and taxes, just like we use a general ledger today.

To keep these categories organized, you need a list of all your specific accounts, which we call a Chart of Accounts. This is like the blueprint that tells you how to file everything in your general ledger.

To get the full picture, it's a good idea to understand your Chart of Accounts first. You can also read our guide on what a chart of accounts is to build a solid foundation.

How Every Transaction Tells a Two-Sided Story

Think of your business finances like a seesaw. To keep it balanced, whatever you put on one side, you have to put something of equal weight on the other. In accounting, we call this double-entry bookkeeping, and it's the rule that makes the general ledger work.

Every single financial event has two sides. Money never just appears out of nowhere or disappears into thin air. If you spend cash, for example, your cash account goes down, but something else—like an asset you just bought—must go up.

A Bakery Buys a New Oven

Let's imagine you run a small bakery and buy a fancy new oven for $5,000. You pay for it straight from your business bank account.

This one purchase creates two entries in your general ledger:

- Your Cash account (an Asset) goes down by $5,000. That's the money leaving your bank.

- Your Equipment account (also an Asset) goes up by $5,000. You now own a new piece of equipment.

See how the seesaw stays level? One asset (cash) went down, but another asset (the oven) went up by the exact same amount. The total value of your business didn't change at that moment—you just swapped one type of asset for another.

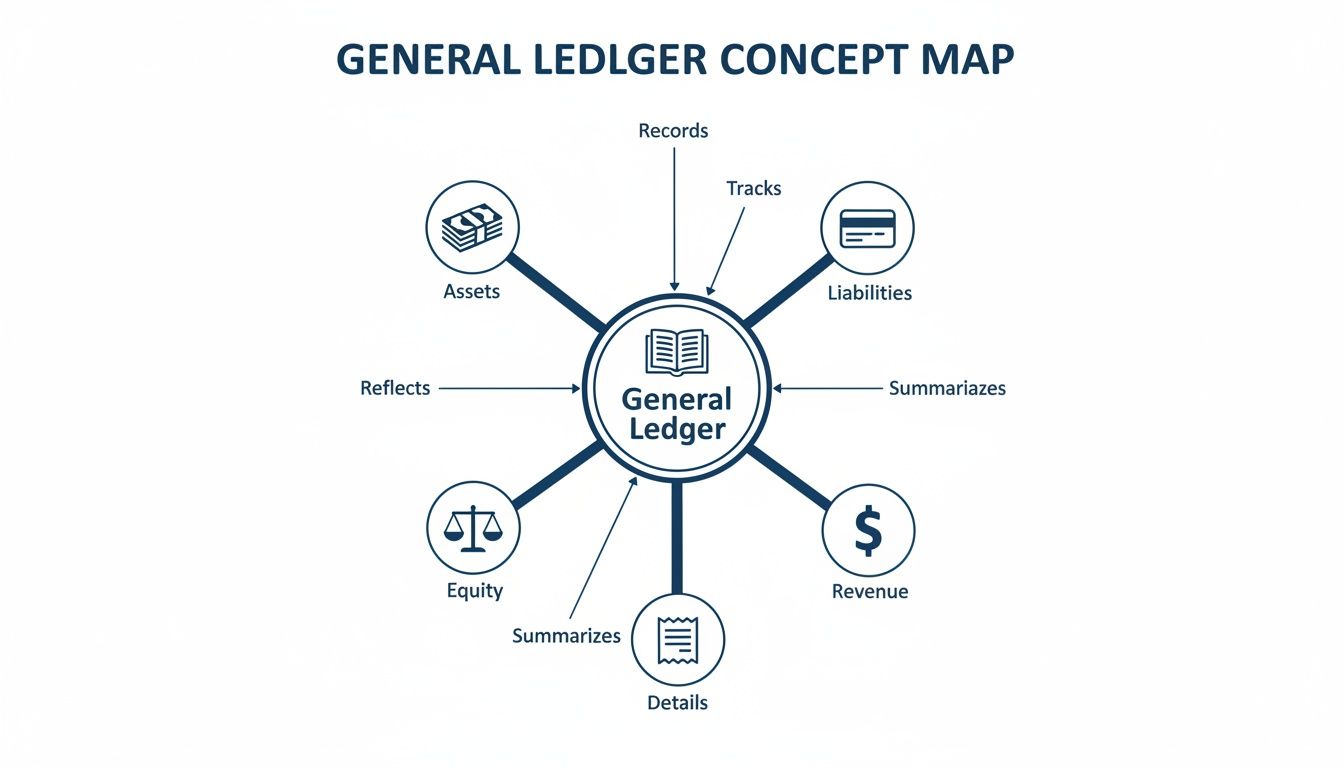

This concept map shows how the general ledger is at the center of everything, connecting the five main account types.

This picture helps show that every transaction has to touch at least two of these accounts to keep the whole system in balance.

Debits and Credits: The Balancing Act

This two-sided system is managed using debits and credits. Don't let these words scare you. They're just labels accountants use to show which way the money is moving. A debit in one account always needs an equal credit in another.

In modern accounting, a general ledger is the backbone of financial reporting, because every transaction must “hit” at least two accounts under the double‑entry system. For example, a $150 customer payment increases cash with a $150 debit and decreases accounts receivable with a $150 credit; the debits and credits must always net to zero, or there is likely an error or fraud risk. You can explore more about the evolution of this core concept and its importance on Digits.com.

This constant balancing act is why a clean general ledger is so important. It's a built-in checking system that makes sure every single penny is accounted for. When the books are balanced, you know you can trust the numbers.

Why a Clean General Ledger Is Your Business Compass

It's easy to dismiss the general ledger as just another boring accounting task. But that's a big mistake. Your general ledger is the most important financial compass your business has.

It tells you where you’ve been, where you are now, and helps you figure out where to go next. Without an accurate ledger, you’re basically flying blind.

A well-kept ledger is where you find the answers to the big questions. Are you actually making a profit on that last project? Can you afford to hire a new person right now? Should you invest in that expensive new software?

The answers are already in your financial data. Your general ledger is the key to unlocking them.

From Ledger to Loan Approval

This isn't just about making better daily decisions. Your general ledger is the source for creating the most important reports in your business: your financial statements. These are the documents that banks, investors, and potential buyers look at to judge how healthy your company is.

The two most important financial statements are:

- The Income Statement: This report shows if your business was profitable over a certain time, like a month or a year. It adds up your revenue and subtracts your expenses to show your final profit or loss.

- The Balance Sheet: This gives you a snapshot of your company's finances at one specific moment. It lists your assets, liabilities, and equity to show what you own versus what you owe.

Without a good general ledger, creating these statements is impossible. If you ever want to get a business loan, find investors, or sell your company, you’ll need clean financials. And that all starts with a well-kept ledger.

Making Smarter Decisions, Faster

In the past, business owners had to wait for their bookkeeper to "close the books" at the end of the month just to see how they did. Not anymore. Modern accounting tools can give you an updated picture of your finances almost in real-time.

This means you can see your revenue, expenses, and cash flow in minutes, not days. For any business, that kind of speed is a game-changer. You can find more insights on how modern ledgers power real-time finance at sdk.finance.

A clean ledger gives you the confidence to act. It turns gut feelings into decisions backed by real data, helping you manage your money and grow your company.

Keeping your general ledger clean isn't just a chore for tax season. It's one of the best habits you can build as a business owner. It gives you the clear, reliable information you need to make smart moves and guide your business toward its goals.

Common General Ledger Mistakes to Avoid

Keeping your general ledger clean is like doing basic maintenance on your car. If you ignore the little things, they can turn into big, expensive problems later. Even a small mistake in your ledger can create a mess that takes hours of work to fix.

The good news is that most of these mistakes are easy to avoid once you know what they are. By spotting these common problems early, you can keep your finances running smoothly and trust the numbers you're looking at.

The goal isn't to become a perfect accountant overnight. It's about building good habits to stop small errors from becoming big headaches.

Mixing Business with Pleasure

This is the number one mistake I see new business owners make. You're out to dinner with a friend, you pick up the tab, and you pay with your business credit card. It seems harmless, but it creates a real problem in your books.

Every time this happens, someone has to figure out how to deal with a personal expense in your company's records. It makes it hard to see how profitable your business actually is. The fix is simple: get a separate bank account and credit card for your business and only use them for business spending.

Forgetting to Reconcile Your Accounts

Your general ledger should match your bank account perfectly, but it doesn't happen by itself. You have to check it. Reconciliation is just the process of comparing every transaction in your ledger to your bank statement to make sure they match.

Skipping this step is asking for trouble. Small data entry mistakes, missed transactions, or even bank fees you didn't know about can throw your numbers off.

Not reconciling is like trying to sail a boat without a compass. You might think you're going in the right direction, but you could be way off course without even knowing it. Checking your accounts every month makes sure your ledger reflects reality.

This simple habit catches mistakes early and gives you confidence that your financial reports are accurate. To learn more about these routines, you can review the basics of small business bookkeeping.

Simple Data Entry Errors

Hey, we're all human. Typos happen. Mixing up two numbers (like writing $89 instead of $98) or putting a decimal in the wrong place might seem small, but it can throw your whole ledger out of balance.

These little errors can be a real pain to find later on. The best way to prevent them is to use good accounting software, which often flags these kinds of mistakes for you. But even then, just taking an extra second to double-check your numbers before you hit "save" can save you a lot of time and frustration.

Choosing the Right Tools to Manage Your Ledger

Trying to manage a general ledger with a spreadsheet is like trying to build a house with only a hammer. You might get it done, but it’s going to be slow, frustrating, and you’ll probably make mistakes. Honestly, it’s time to move past spreadsheets.

Modern accounting software like QuickBooks or Xero is a huge step up. These tools are designed to do the hard work for you. They connect to your business bank accounts and automatically pull in your transactions. This saves you tons of time and helps cut down on human error.

A Simple System That Works

Creating a good system doesn't have to be complicated. Once you have the right software, the monthly process is much easier to handle.

A simple, repeatable workflow looks like this:

- Categorize Your Transactions: Go through the transactions the software brought in and put them in the right accounts (like "Office Supplies" or "Sales").

- Match Everything to Your Statements: This is the reconciliation step. You'll match the transactions in your software to your bank and credit card statements to make sure it all lines up.

- Review the Reports: With one click, the software creates your financial reports. Take a few minutes to look them over and see what they tell you about your business.

This simple routine turns bookkeeping from a headache into a powerful business habit. Many tools also help automate this process even more. You can learn about the benefits by exploring financial reporting automation.

Choosing the right tool isn’t just about saving time; it's about getting clarity. It's about having numbers you can trust so you can make smarter decisions about your business.

If managing software still sounds like too much, there’s an even better way. Working with an outsourced bookkeeping firm like MyOfficeOps lets you use all these best practices without taking time away from running your business. An expert team can set up your system, manage it for you, and give you the clear reports you need to grow. When choosing tools, also consider the benefits of integrating accounting software like Xero with your payment systems to automate transaction recording and keep everything in sync.

Answering Your Top General Ledger Questions

Even after you learn the basics, a few questions always seem to come up. Here are straight answers to the things I hear most often from business owners about the general ledger.

How Often Should I Review My General Ledger?

For most small businesses, you should do a full review at least once a month. This is called reconciliation, where you match your ledger to your bank and credit card statements.

Doing this every month is a must. It helps you catch errors, duplicate charges, or even fraud right away, not months later when it’s a bigger problem. It’s also a great habit to check your cash accounts once a week just to keep an eye on your daily spending.

What's the Difference Between a General Ledger and a Chart of Accounts?

Let's use a simple analogy: think of your finances as a book.

The Chart of Accounts is the table of contents. It's a neat list of every financial category you use, like "Sales Revenue," "Office Supplies," or "Payroll." It tells you where to find everything.

The General Ledger is the book itself. It has all the pages with the full story of every single transaction that happened in each of those categories. It’s where all the financial details live.

Can I Manage My Own General Ledger, or Do I Need an Accountant?

You can definitely manage your own ledger, especially when you're just starting. Using good accounting software like QuickBooks Online makes it pretty simple and is a great way to learn how your business's money works.

But as your business grows, things get more complicated. You'll have more transactions, new ways of making money, and more rules to follow. Many owners find that the time they spend on bookkeeping is time they aren't spending on finding new customers or making their product better.

Working with a professional saves more than just time. It gives you an expert set of eyes to make sure your books are clean and ready for anything—from tax season to a sudden opportunity to grow.

An expert makes sure your financial records are always right. More importantly, they can give you insights that help you make smarter, more confident decisions for your business.

Ready to stop worrying about your books and start focusing on growth? The team at MyOfficeOps can build and maintain a clean, accurate general ledger for you, giving you the financial clarity you need to succeed. Get in touch with us today.