You're probably in one of these two spots right now.

Sales look decent, customers seem happy, and the phone keeps ringing. But every Friday, you still stare at the bank balance and wonder if payroll, rent, supplier payments, and taxes are all going to clear without drama.

Or maybe business is flat-out busy, which somehow feels worse. More jobs, more invoices, more materials, more people to pay, and still not enough cash sitting in the account when you need it.

That's the trap. A lot of Philly-area owners are profitable on paper and stressed in real life. Construction firms live it when they finish work before they bill. Clinics feel it when claims, billing, and payables move at different speeds. Service businesses feel it when they let clients drag payments out while payroll hits right on time.

Working capital optimization matters. Not as accounting jargon. As survival. As sleep. As the difference between funding your own growth and begging a bank for breathing room.

Why Your Cash Disappears and How to Find It

Working capital is the cash your business has available to run day to day. It's what pays your team, buys materials, covers software, and keeps the lights on while you wait to get paid.

A lot of owners think they have a sales problem when they really have a timing problem.

The profitable but broke problem

I've seen this with small contractors around Philadelphia and West Chester more times than I can count. Jobs are moving. Revenue is coming. But cash is missing because money gets trapped in three places. Receivables, payables, and inventory or work in progress.

If your customers take too long to pay, your vendors want money now, and you've got cash tied up in stock or half-finished jobs, your bank account gets squeezed even when the business looks healthy.

That's why I push owners to treat working capital optimization like an operating system, not a finance side project. A comprehensive approach focused on those three levers can generate 15 to 30% improvements in cash flow without requiring additional sales volume, according to HighRadius on working capital optimization strategies.

Practical rule: Revenue doesn't pay bills. Collected cash does.

Stop calling it a bookkeeping issue

This isn't just your bookkeeper's problem. Sales affects it. Purchasing affects it. Operations affects it. If one team chases volume while another team stretches vendors and nobody watches the full cash cycle, you get chaos.

Small business owners usually feel the pain first in simple ways:

- Payroll pressure: You made sales this month, but payroll lands before customers pay.

- Vendor stress: A supplier puts you on tighter terms because your payments are slipping.

- Owner withdrawals: You stop paying yourself consistently because the business is always “almost fine.”

- Growth strain: More work creates more cash pressure, not less.

If that sounds familiar, it helps to get grounded in simple cash flow thinking. This Australian small business cash flow guide does a good job explaining the common patterns owners run into when cash gets tight.

You also need to understand what your reports are telling you. If your cash flow statement feels like background noise, read this plain-English guide on how to read a cash flow statement.

Cash problems usually hide in plain sight

Owners often look for a dramatic fix. A bigger credit line. A new lender. A short-term loan. Sometimes that helps, but usually the first move is simpler. Find where cash is getting stuck and remove friction.

The good news is most small businesses don't need fancy financial engineering. They need tighter billing, cleaner collections, smarter purchasing, and a better rhythm for reviewing cash every week.

That's where the numbers come in.

Finding Your Starting Line with Key Numbers

If you don't know how long cash stays trapped in your business, you're guessing.

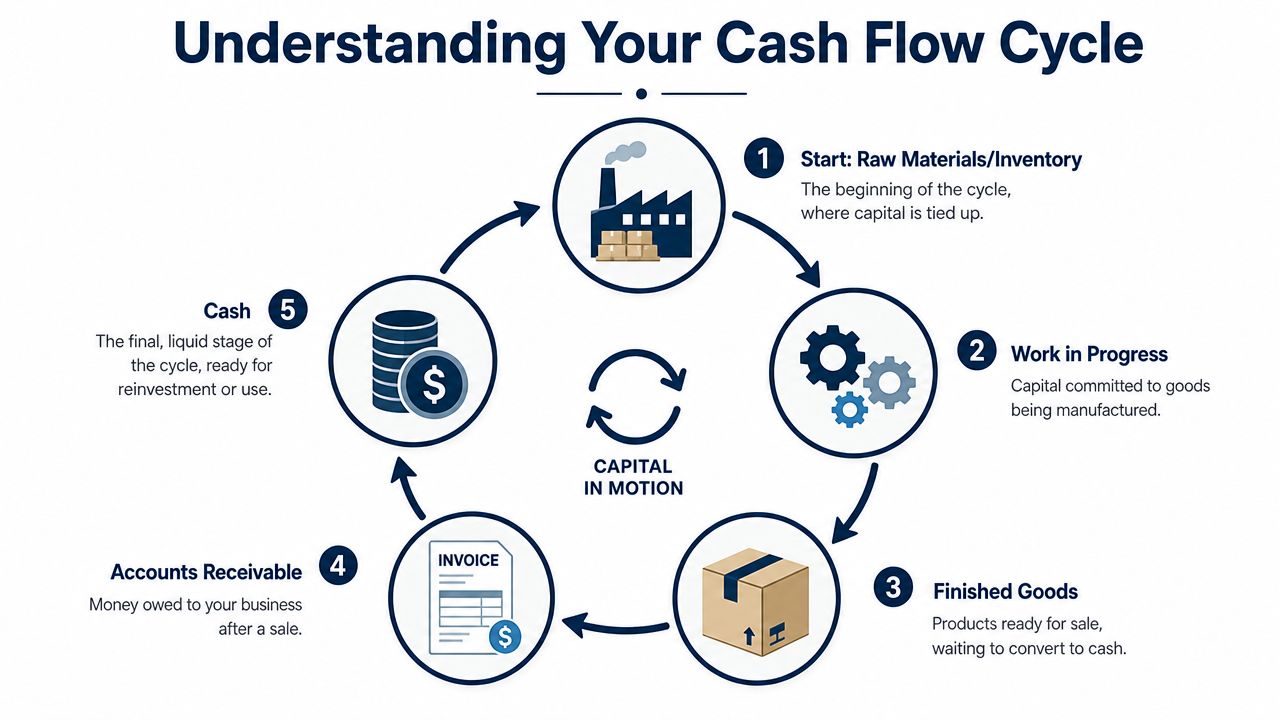

The key number is the Cash Conversion Cycle, or CCC. In plain English, it tells you how long it takes for a dollar you spend to come back into your bank account.

The process resembles planting a seed. You spend money on materials, labor, or inventory first. Then time passes. Then you sell the work. Then you invoice. Then you wait again. Finally, the cash shows up.

That waiting period is what hurts.

The formula that matters

The formula is simple. CCC = DSO + DIO – DPO, as outlined by Growth Operators on working capital and cash flow.

Here's the plain version:

- DSO is how long customers take to pay you.

- DIO is how long inventory sits before it turns into sales.

- DPO is how long you take to pay your own bills.

A lower cycle is better. It means cash comes back faster.

Here's the visual version.

What those numbers look like in real life

For a contractor, DSO might be the lag between finishing a job and getting paid. If you wait to send invoices, accept messy billing backup, or don't follow up fast, that number climbs.

For a clinic, DIO may not be traditional inventory in the retail sense, but the same logic applies to supplies, delayed claim processing, and work that's done but not yet converted into cash. Money sits in the system instead of the bank.

For almost any small business, DPO is where owners get nervous. They either pay too fast because they hate owing people money, or they pay too slow and annoy suppliers. The point isn't to play games. The point is to use agreed terms well and preserve cash without damaging relationships.

Start with a 13 week forecast

If you only look at monthly financials, you're driving by staring in the rearview mirror.

A rolling 13-week cash flow forecast is the tool I'd make mandatory for almost every small business owner. The same Growth Operators source notes that this forecast is critical, and that improving DSO by 10 to 15 days directly frees up cash when companies reduce their cycle systematically.

Cash gets tight weeks before owners admit it. A weekly forecast forces the truth into the room.

Your first version does not need to be fancy. It needs to answer a few hard questions:

- What cash is coming in each week

- What must go out each week

- Which customers are late

- Which payments can wait under normal terms

- Where a shortfall is likely to hit

If you want a cleaner way to track the numbers that drive decisions, this overview of key performance indicators for small business is a useful starting point.

Don't overcomplicate the baseline

You do not need perfect data to begin. You need honest data.

Use your accounting system. Pull your aged receivables. Review your payables list. Look at open jobs or inventory on hand. Then measure the lag between spending cash and collecting it back.

Once you know your starting line, you can go after fast wins.

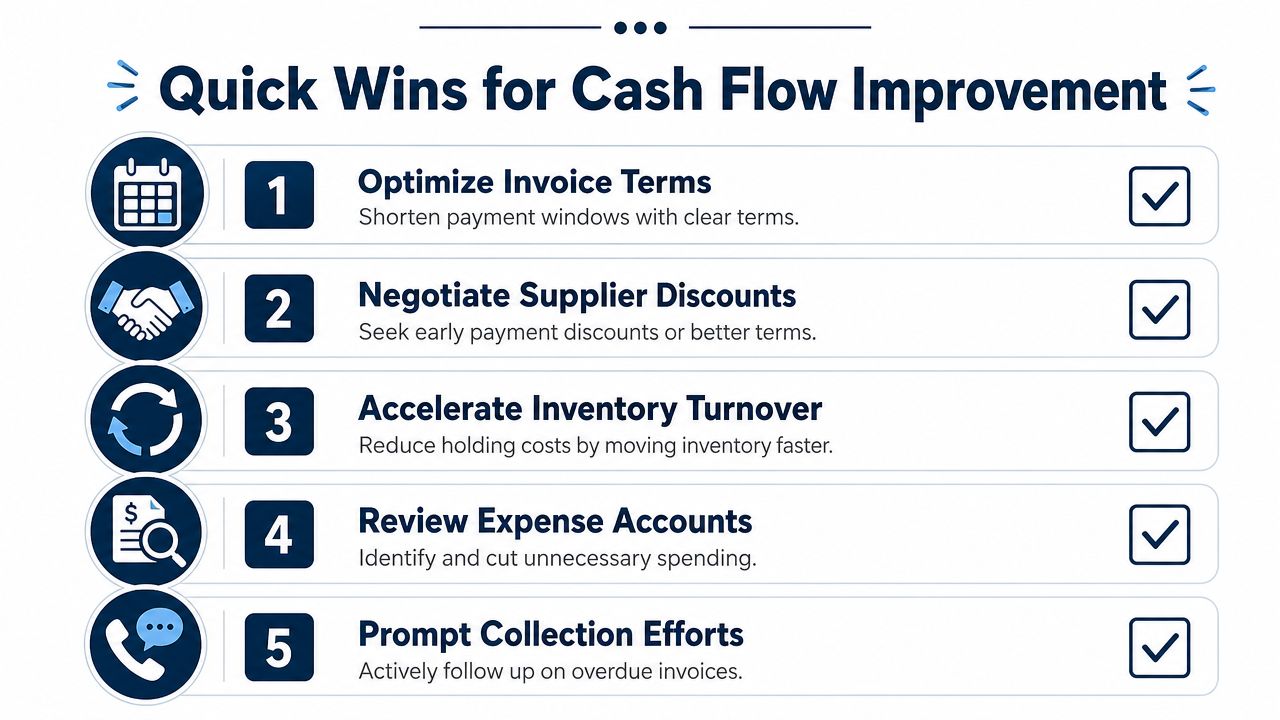

Fast Cash Wins You Can Implement This Month

If cash is tight, don't start with a twelve-month transformation plan. Start with moves that put money in the bank faster.

Most owners already know what they should do. They just haven't committed to it.

Get paid faster

The easiest money to find is usually in receivables.

A small construction firm in Philadelphia changed one habit. It started sending invoices by email and text instead of relying only on mail, and that cut average payment time from 45 days to 28 days, according to Billtrust's working capital optimization example.

That result makes sense. People pay what they see.

Here's what I'd put in place this month:

- Invoice same day: If the job is done, bill it that day. Not next Friday. Not when someone “gets around to it.”

- Use the customer's preferred channel: Email, text, portal. Match how they handle bills.

- Clean up invoice errors: Missing job numbers, missing approvals, and wrong contacts slow payments for stupid reasons.

- Follow up early: Don't wait until an invoice is significantly overdue. Make collections part of the normal process.

Pay smarter, not slower

Stretching payables blindly is lazy management.

Good payables management means knowing which vendors matter, which terms are standard, and where you have room to negotiate. If a supplier is strategic, protect that relationship. If terms are unclear, fix them before there's a cash issue.

A few practical moves:

- Use agreed terms fully: If you have net terms, don't pay on day one out of habit.

- Group payment runs: Random payments kill visibility. Scheduled runs create control.

- Ask for structure: Some vendors will work with staged or cleaner payment terms if you communicate early.

- Protect key suppliers: Don't squeeze the vendor you depend on to keep jobs moving.

Owners get into trouble when they treat every bill the same. Some vendors can wait. Some absolutely can't.

Hold less cash in stuff

Inventory, supplies, and work in progress can subtly drain cash.

You don't need a warehouse problem to have an inventory problem. Service firms do this too. They overbuy software seats, supplies, materials, or labor capacity because they're planning around hope instead of actual demand.

A blunt checklist:

- Review slow-moving items: If it hasn't moved in a while, ask why you're still carrying it.

- Buy based on demand, not fear: “Just in case” gets expensive fast.

- Finish work faster: Half-done jobs often mean half-trapped cash.

- Align purchasing with collections: Don't load up on materials for work that won't bill soon.

These are low-hanging changes. They aren't glamorous. They work because they reduce delay, and delay is what starves small businesses.

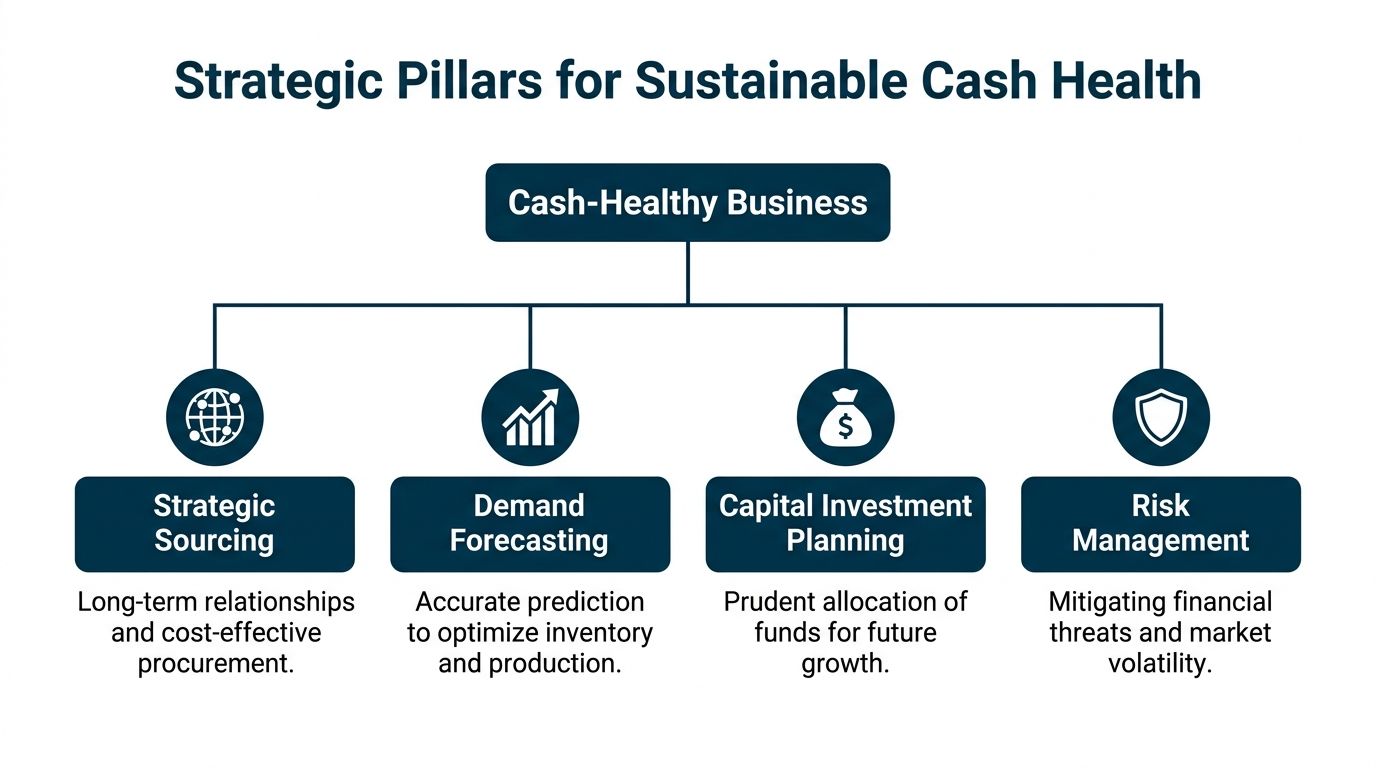

Building a Cash-Healthy Business for the Long Haul

Quick wins help. Systems keep you out of trouble.

A business becomes cash-healthy when pricing, vendor management, and forecasting support each other. If one of those breaks, the others have to carry too much weight.

Fix pricing that ignores time

A lot of owners price jobs as if payment shows up instantly. It doesn't.

If you wait a long time to get paid, that delay has a cost. You're funding labor, materials, overhead, and risk while the customer holds the cash. If your pricing doesn't account for that, fast growth can make the business weaker.

Ask yourself:

- Are we charging enough for slow-paying customers

- Do our payment terms fit the type of work

- Are deposits, progress billing, or milestone billing appropriate

- Do rush jobs and change orders get billed with the same discipline as core work

Those aren't accounting questions. They're operating questions with cash consequences.

Build vendor relationships like an adult

Good vendors are not your enemy. They're part of your financing chain.

That means you should talk to them before there's a problem. Ask for terms that fit your operating cycle. Be clear about volume, seasonality, and payment habits. Suppliers usually respond better to honesty and consistency than to surprise silence.

This matters a lot in transportation, logistics, and field service businesses where invoicing can get messy. If you want a practical example of how teams streamline transport invoicing, it helps show how billing process design affects cash timing in practice.

Here's a local example that gets to the point. A healthcare clinic in Greater Philadelphia automated its billing and payables, lowering overhead costs by 15% and freeing up $20,000 in working capital in just 6 months without needing a line of credit, based on Priority Commerce's working capital optimization example.

That didn't happen because someone found magic money. It happened because the clinic removed delays and manual friction.

Forecasting is what keeps you out of panic mode

Most small business cash problems aren't surprises. They're missed signals.

Process and tools matter. You need one place to review expected cash in, expected cash out, overdue receivables, upcoming payroll, and known large purchases. Some owners handle this inside their accounting software. Others use a dedicated spreadsheet. Others work with outside support to keep the process current. For example, MyOfficeOps provides bookkeeping, forecasting, KPI dashboards, and CFO-level advisory for small and midsize businesses that need tighter visibility without building a full internal finance team.

The point is not the tool. The point is the habit.

If you review cash weekly, adjust purchasing based on demand, and price work with payment timing in mind, your business gets sturdier. Not perfect. Sturdier.

Your Roadmap and Dashboard to Stay on Track

Owners fail at working capital optimization when they try to fix everything at once.

You need a short roadmap and a small dashboard. That's it. A few actions. A few numbers. Reviewed often.

A simple rollout that sticks

Start with the next 30 days. Tighten billing, clean up old receivables, map vendor terms, and build a weekly cash forecast. Don't delegate all of this without oversight. If cash is a pain point, the owner has to be in the room.

Then use the next quarter to lock in process. Standard invoice timing. Clear collection rules. Purchasing review. Better job or client profitability visibility. Fewer one-off payment decisions.

After that, the work becomes rhythm. Weekly review. Monthly trends. Quarterly changes to terms, pricing, and forecasting assumptions.

If a process depends on memory, it will break when the business gets busy.

The dashboard I'd want on one screen

You do not need twenty metrics. You need the handful that reveal where cash is getting stuck.

| KPI | What It Measures | Goal for Optimization |

|---|---|---|

| Cash Conversion Cycle | How long cash stays tied up from spend to collection | Shorten the cycle over time |

| Days Sales Outstanding | How quickly customers pay invoices | Reduce collection lag |

| Days Payable Outstanding | How long you take to pay vendors under agreed terms | Use terms fully without harming suppliers |

| Inventory or Work in Progress Review | How much cash is sitting in materials, stock, or unfinished work | Reduce idle cash and slow-moving items |

| 13 Week Cash Forecast Accuracy | Whether your short-term cash view matches reality closely enough to guide decisions | Improve visibility and reduce surprises |

That's your command center.

If you need a plain-English reference for organizing this visually, take a look at what a KPI dashboard is and how to use one.

What good discipline looks like

Good owners don't just review reports. They make decisions from them.

That means asking specific questions every week:

- Which invoices need action now

- Which purchases can wait

- Which jobs are consuming cash faster than planned

- Which customers deserve tighter terms

- Which vendor relationships need a conversation before tension builds

The dashboard should change behavior. If it doesn't, it's decoration.

And if your team runs different goals that fight each other, fix that fast. Sales should care about collection quality. Operations should care about billing readiness. Purchasing should care about timing, not just price. Cash discipline is cross-functional, even in a small company.

Avoiding Pitfalls and Taking the Next Step

The biggest mistake owners make is trying to optimize one corner of the business while ignoring the rest.

You can't fix cash by hammering collections if inventory is bloated. You can't fix it by stretching vendors if billing is sloppy. You can't fix it by cutting purchases if your forecast is wrong.

A common pitfall is focusing too narrowly on one area, when the key is synchronizing payables, receivables, and inventory. Inaccurate cash forecasting and poor real-time visibility are also common failures, as discussed in this CFO forum conversation on working capital management.

The excuses that keep owners stuck

I hear the same ones all the time.

- Our customers just pay slowly: Some do. That doesn't excuse late invoices, weak follow-up, or unclear terms.

- We're too busy to build a forecast: If cash is tight, you're too busy not to.

- I don't want to upset vendors: Fair. Then communicate early and use structure instead of avoidance.

- Our team already knows what to do: If cash still keeps getting tight, they either don't know or aren't doing it consistently.

Balance beats brute force

Bad working capital management isn't always obvious. Sometimes it looks responsible. Paying bills too fast can feel responsible. Holding too much stock can feel safe. Avoiding hard collection calls can feel polite.

But cash discipline requires balance. Push too hard on one side and something else breaks.

The right move is usually steady, boring, and repeatable. Bill faster. Collect earlier. buy smarter. Forecast weekly. Keep terms clear. Review a short dashboard. Fix process gaps before they turn into financing problems.

If you want help putting that into practice, get support from people who can clean up the books, tighten reporting, and turn the numbers into decisions.

If you're tired of feeling busy but cash-poor, MyOfficeOps can help you build a practical working capital plan, set up forecasting, clean up reporting, and create a dashboard you'll consistently use. That means fewer surprises, better decisions, and more cash staying where it belongs, in your business bank account.