You're probably feeling this right now.

A job looks good on paper. The margin seems fine. The owner or GC says payment is coming. Meanwhile, payroll hits on Friday, your supplier wants to be paid, a sub is calling twice a day, and your checking account looks nothing like your P&L.

I see this all the time. Good contractors don't usually fail because they can't build. They get squeezed because money shows up later than costs do. That's why construction cash flow forecasting matters so much. Not the fake version based on contract language, but the version reflecting how money moves in your business.

Most advice on this topic misses the point. It tells you to plug contract terms into a spreadsheet and call it a forecast. That's not a forecast. That's wishful thinking with rows and columns.

Why Profitable Construction Projects Go Broke

A contractor wins a solid project. The job starts well. Crews are moving, materials are on site, and billings are going out. If you look at the job report, it shows profit.

Then the pain starts.

Payroll comes first because it always does. Materials get paid because suppliers don't like excuses. Subcontractors want their draw. The client payment is still “processing.” Retainage is being held back. A change order is approved in the field but hasn't made it into accounting. On paper, the project is healthy. In the bank, it's starving.

Profit isn't cash

This is the first thing I want you to get straight. Profit and cash are not the same thing.

Profit tells you whether the work should make money overall. Cash tells you whether you can survive long enough to collect it. In construction, timing is the whole game.

That's why profitable projects still go broke. You can earn money on a job and still run into a liquidity crisis if cash isn't available when payroll, vendors, and subs need to be paid. That's the core issue behind a lot of project stress, and it's one reason owners who want a better grip on operations should also spend time understanding paving project risks, because cash problems rarely show up alone.

Practical rule: If your team looks at profit first and cash second, you're managing construction backward.

Spreadsheets make this worse when they're built on hope

A lot of contractors are trying to manage this with spreadsheets stitched together from job costing, WIP, AR, AP, and somebody's memory. That setup breaks fast.

Industry data reveals that 94% of business spreadsheets contain critical errors. In construction, this is amplified because many firms fail to model retainage (typically 5% to 10% of every draw) as a separate line item, mistakenly treating non-cash withholdings as available cash according to this cash flow forecasting analysis.

That one mistake causes a lot of pain. The cash isn't in your account, but your forecast acts like it is. Then you hit the classic year-end wall. Jobs are active, receivables look decent, but there's not enough usable cash to carry labor and subs.

Here's the simple test:

| What your report says | What your bank says |

|---|---|

| Job is profitable | Cash is tight |

| Invoice was sent | Payment hasn't arrived |

| Revenue is earned | Retainage is trapped |

| Change order exists | Money still isn't collected |

If your current process doesn't clearly show that difference, it's not a forecast. It's a rearview mirror.

If you want a cleaner baseline before building your own model, this guide on construction cash flow management is worth reading because it frames cash as an operating issue, not just an accounting task.

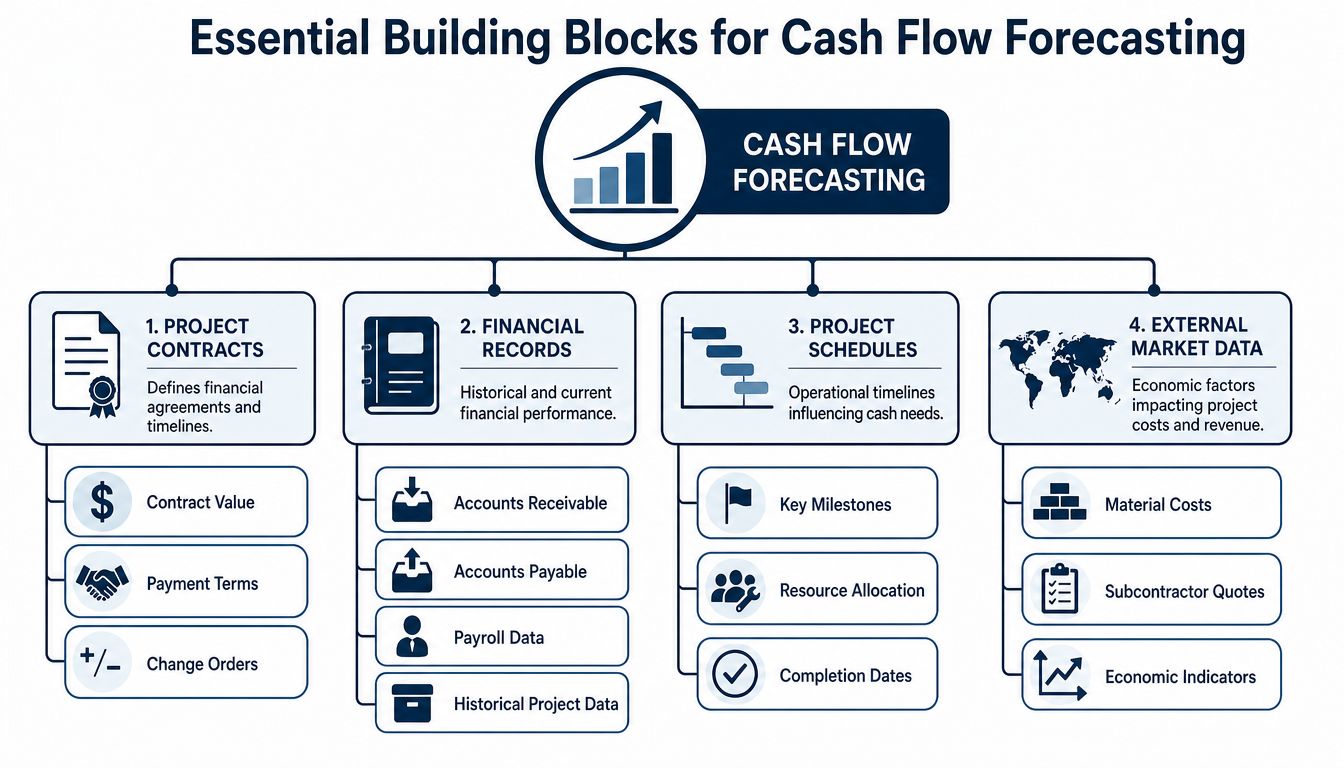

Gathering Your Essential Building Blocks

Before you build a forecast, you need the right inputs. Not just a bank balance. Not just last month's P&L. You need the operating facts that control when cash comes in and when it leaves.

Most bad forecasts fail at this stage. The math isn't the problem. The assumptions are.

Start with the real payment cycle

The biggest mistake I see is simple. Owners forecast off the contractual payment cycle instead of the real payment cycle.

Those are not the same thing.

Actual cash inflows often lag 30–60 days beyond contract terms due to retention deductions and subcontractor cycling. Data shows that forecast accuracy only reaches a 50% confidence level (P50) when these real-world cycles, not idealized terms, are used based on this industry breakdown.

That means if your contract says net terms are one thing, but your customer usually pays much later, your forecast has to reflect the later date. Always.

If a client always pays late, “late” is no longer an exception. It's your normal.

What you need on your desk

I'd gather these inputs before touching a spreadsheet:

- Project contracts: Contract value, billing terms, retainage terms, approved change orders, and any pay-when-paid language.

- Schedule of Values: Your billing cadence begins here. If the SOV is sloppy, the forecast will be sloppy too.

- Project schedule: Key milestones, start and finish timing, and any known schedule pressure.

- Accounts receivable detail: Not summary totals. I want invoice dates, expected collection dates, and notes on problem accounts.

- Accounts payable detail: Vendor terms, due dates, and which suppliers will enforce them.

- Payroll rhythm: Weekly payroll can crush a business that bills monthly.

- Subcontractor commitments: Payment timing, draw expectations, and whether they'll tolerate delay.

- Overhead costs: Rent, admin payroll, insurance, software, vehicles, and anything else that gets paid whether the job is smooth or not.

If your job costing isn't clean, fix that next. A forecast built on bad job data won't help you. This explainer on what job costing means in construction is a good refresher if your numbers don't currently tie back to the field.

Build for reality, not paperwork

I'd also keep a short “reality adjustment” list for every customer and major vendor.

For example:

- Customer A: Contract says one thing. Actual payment behavior is slower.

- Supplier B: Terms look flexible on paper, but they start calling the minute a bill is due.

- Sub C: Needs quick payment to stay loyal on your jobs.

- Owner rep: Holds up approvals unless backup is perfect.

That list matters more than most templates.

If collections are one of your weak spots, you don't need to overcomplicate it. Sometimes a simple system to streamline payment collections for your business can tighten up the inflow side enough to make the whole forecast more usable.

A simple checklist you can actually use

Here's the checklist I'd use each time:

- Pull live job data. Contracts, SOVs, schedules, change orders.

- Match each invoice to a realistic collection date. Not the legal due date. The likely date.

- Map fixed cash outflows. Payroll, rent, debt, insurance, software.

- Add project-specific outflows. Materials, subs, equipment, permits.

- Flag anything uncertain. Disputes, unsigned change orders, delayed approvals.

That gives you the raw material for a forecast that acts like a business tool instead of a monthly ritual.

Building Your First Cash Flow Forecast

Don't start with the whole company. Start with one project.

That keeps the process simple, and it forces you to think clearly about timing. Once you can forecast one job well, you can roll several jobs together and build a company-level view.

Build one project first

Take a single live job and lay it out by week.

I like weekly forecasting because construction moves fast. Monthly views are too slow when payroll and suppliers are moving every few days.

Use a basic structure like this:

| Week | Expected cash in | Expected cash out | Net cash movement | Ending cash impact |

|---|---|---|---|---|

| Week 1 | Client payment expected | Payroll, materials, subs | In minus out | Running balance |

| Week 2 | Retainage release or none | Payroll, equipment, AP | In minus out | Running balance |

| Week 3 | Progress billing collected or none | Labor, vendor bills | In minus out | Running balance |

You don't need fancy formulas at first. You need clear timing.

What goes into cash in

For inflows, only include money you have a reasonable path to collect.

That usually means:

- Approved billings: Tied to your SOV and expected collection timing

- Approved change orders: Only when they're approved and likely to bill

- Retention release: Only if you have a realistic date, not because you hope it comes soon

- Other receivables: Only if someone on your team owns the collection process

Be conservative. Construction forecasting breaks when optimism gets treated like cash.

What goes into cash out

Outflows need more honesty than most owners want to give them.

Include:

- Direct labor: Weekly payroll and related labor costs

- Materials: Deposit timing, delivery timing, and due dates

- Subcontractors: Draw timing and your real payment practice

- Equipment and rentals: Planned use, not just booked invoices

- Permits and project admin: Small items still hit the bank

- Company overhead: Admin payroll, office costs, software, vehicles, and recurring expenses

A project doesn't just need enough cash to build the work. It needs enough cash to carry the company while the work gets paid.

Then move to the company forecast

Once you've built one project forecast, stack all active jobs together and add overhead. Now you've got something useful.

The standard methodology for effective construction forecasting relies on a 13-week rolling cash flow forecast, which provides a one-quarter runway by layering billing cadence and retainage release against vendor payment terms according to this construction cash flow guide.

That 13-week view is the tool I'd want in front of me every Monday morning.

How the 13-week model should work

A good rolling forecast does three things:

- Shows this week's expected movement. What's supposed to hit and what's definitely leaving.

- Shows upcoming trouble early. You should see the cash dip before it arrives.

- Updates constantly. Every week, you drop the old week, add a new one, and adjust based on what happened.

If you're using a generic spreadsheet, that's fine. What matters is discipline. If you want a simpler starting point, this cash flow forecasting template can help you avoid building one from scratch.

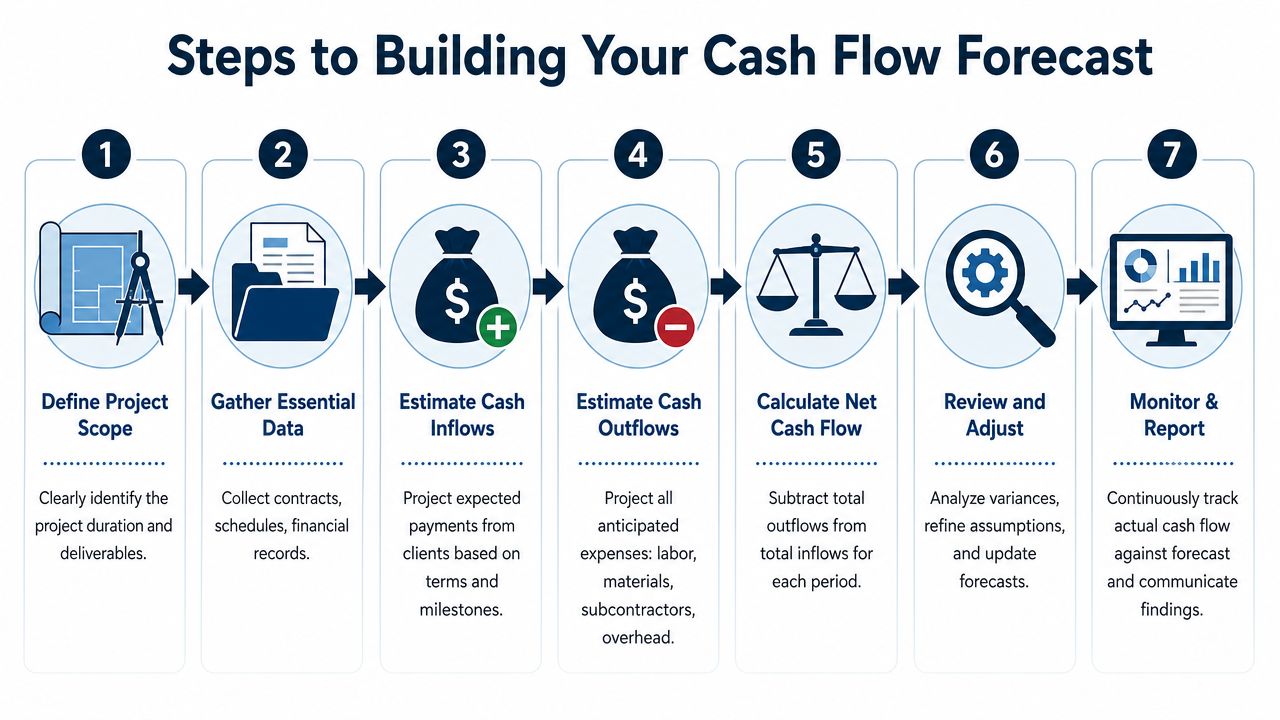

A plain-English process

Here's the version I use with owners who hate finance language:

Step 1

List every dollar you expect to collect in the next 13 weeks. Put each item in the week it will most likely arrive, not the week the contract says it should arrive.

Step 2

List every dollar you expect to pay in the next 13 weeks. Include payroll, materials, subcontractors, taxes, loan payments, and overhead.

Step 3

Subtract outflows from inflows each week. Then carry forward the running cash balance.

Step 4

Mark danger weeks. If a week goes negative or gets uncomfortably tight, flag it.

Step 5

Decide what action you'll take now. Speed up billing, push collections, slow spending, draw on a credit line, or move a project start.

That's what real construction cash flow forecasting is. Not a spreadsheet that makes you feel better. A weekly decision tool that tells you when you're about to get squeezed.

Timing Is Everything In Construction

In this business, the amount matters. The timing matters more.

A contractor can survive a thin margin longer than they can survive bad timing. If cash lands after labor, materials, and subcontractors need to be paid, you've got a funding gap. That gap is where stress, bad decisions, and expensive financing show up.

Retainage and payment chains create hidden gaps

Retainage is one of the easiest ways to fool yourself. The invoice is issued. Revenue is recorded. But part of that money is still out of reach.

Then add pay-when-paid language and the chain gets longer. Owner pays GC late. GC pays subcontractor late. Subcontractor delays their own obligations. Everyone down the line feels it.

If you finance projects with draws, it also helps to understand how the release of funds really works. This piece on a construction loan draw schedule is useful because draw timing affects when cash is available, not just when work is done.

Build a buffer before the job forces you to

A forecast without a reserve is fragile.

An important forecasting step involves setting a contingency reserve buffer of 5-10% of the total project cost to absorb unplanned expenses like weather delays, price increases, or change orders, and reviewing this living document weekly or monthly based on this construction forecasting guidance.

I agree with that. You need a buffer because construction never runs on a perfect script.

This is my approach:

| Timing issue | What it does to cash | What you should do |

|---|---|---|

| Slow billing approval | Pushes inflows later | Follow up faster and document backup |

| Retainage held back | Shrinks usable cash | Track it separately |

| Subcontractor draw due | Pulls cash out now | Match timing to expected receipts |

| Material price jump | Increases outflow | Use reserve, then reforecast |

Use a working capital lens

I also want you to stop looking only at project profit and start asking one harder question:

How much cash does this backlog require before it pays me back?

That's the working capital view. Some jobs need more carrying power than others. A project can look fine on margin and still put pressure on the whole company if it demands cash too early.

Good contractors get in trouble when they win work they can't comfortably carry.

That's why I'd review your forecast often. Weekly is best if things are moving fast. Monthly is the bare minimum if your project load is lighter. The minute a schedule slips or a payment drifts, your forecast needs to change.

Avoiding Common Forecasting Disasters

A bad forecast can do real damage because it gives you confidence you haven't earned. I've seen owners hire too early, start new jobs too fast, and relax collections because the spreadsheet looked healthy.

Then the cash crunch hits and everybody acts surprised.

Disaster one, siloed data

This is the biggest technical failure I see. Estimating has one version of the job. PMs have another. Accounting is working off something older. Nobody is wrong on purpose, but the forecast is still wrong.

The primary technical failure point in construction forecasting is siloed data across ERP, CRM, and project management tools, identified as the single biggest cause of inaccurate forecasts. The solution requires integrating change order tracking with live forecast updates according to this forecasting glossary.

If a PM knows about a cost increase on Tuesday and finance doesn't reflect it until next month, your forecast is fiction.

Fix: One owner for the forecast. Weekly update meeting. Change orders, schedule slips, and field issues get pushed into the model right away.

Disaster two, forgetting overhead

A lot of project forecasts only include field costs. That's a mistake.

Your office payroll, software, vehicles, rent, insurance, and debt service still need cash. If your forecast leaves those out, it will always look better than reality.

Fix: Add overhead as its own section every week. Don't bury it in a monthly total and pretend it's separate from project decisions.

Disaster three, trusting approval without collection

Approved doesn't mean paid. Submitted doesn't mean collectible. Verbal agreement doesn't mean anything.

The safest forecast is the one that assumes paperwork moves slower than you want.

Fix: Use stages. Pending, approved, billed, expected to collect. Only put likely collections into the inflow line.

Disaster four, not updating the forecast

A forecast loses value fast if nobody touches it. Construction changes every week. Your forecast should too.

Here's a simple pre-flight list:

- Check changes in the field: Scope changes, labor shifts, delays, rework

- Review AR weekly: Confirm which invoices are still on track and which are slipping

- Update vendor timing: Some suppliers wait. Others don't

- Revisit staffing decisions: Don't hire off old numbers

- Watch disputed items closely: If a payment is getting messy, stop treating it like clean cash

If your current model can't absorb new information quickly, it's too rigid to help you.

Making Your Forecast A Living Business Tool

The forecast should sit in the middle of your business, not in a folder nobody opens.

If you're only looking at it when cash gets tight, you're late. By then, your options are worse. You're reacting instead of choosing.

Use it to make decisions early

A living forecast helps you answer real questions before they turn into problems.

Can you start another job next month? Can you afford another crew? Should you hold off on equipment? Do you need to push harder on receivables this week instead of next week?

That's where scenario planning matters. Advanced forecasts use sensitivity scenarios to simulate billing milestones shifting out by 30, 60, or 90 days. This allows teams to activate contingency plans like drawing on credit facilities when the model shows a specific future cash gap, rather than waiting for it to happen as explained in this cash flow management article.

I like this because it forces honesty. If one owner payment slips, what happens? If two jobs bill later than planned, what happens? If a supplier won't extend terms, what happens?

Give the forecast a weekly rhythm

Here's the cadence I recommend:

- Every week: Update expected collections and disbursements

- After every material change: Revise for schedule slips, cost changes, and approved scope changes

- Before major decisions: Check the forecast before hiring, starting a project, or taking a distribution

One person should own the document. But operations, project management, and accounting all need to feed it.

A useful forecast changes behavior. If it doesn't affect decisions, it's just reporting.

The contractors who handle cash best aren't always the ones with the best margins. They're the ones who see trouble early and act before it hits the bank.

If you want help turning messy books, delayed reporting, and uneven cash visibility into something you can run the business on, MyOfficeOps can help. They work with construction and other service businesses that need clear numbers, better forecasting, and practical financial guidance without the big-firm nonsense.