Running a business can feel like trying to build something without instructions. You could just start putting pieces together and hope it works, or you could follow a clear plan. That's what this A to Z bookkeeping guide is all about.

Bookkeeping is that plan. It’s simply the job of keeping track of all the money that comes into your business and all the money that goes out.

Why Your Business Needs a Financial Map

It’s easy to think of bookkeeping as just a boring task for tax season. But it's so much more than that. Good bookkeeping gives you an honest look at how your business is really doing. Without it, you’re just guessing.

You might feel busy and see money coming in, but does that mean you're actually making a profit?

Let's say you run a small landscaping business. You just finished a big backyard project and the client paid you a nice chunk of money. Feels great, right? But once you subtract the cost of the plants, your crew's pay, and other expenses, you might find out you barely made any money. That’s the kind of tough—but important—truth that bookkeeping shows you.

Turning Data into Decisions

This financial map does more than just show you where your money went. It helps you decide where your money should go next. Knowing your numbers helps you answer the hard questions every business owner has:

- Can I afford to hire a new person?

- Is it a good time to buy that new truck?

- Which of my services are actually making me the most money?

- Do I have enough cash to pay my bills next month?

Answering these questions with real numbers instead of a gut feeling is how you grow a strong business. It lets you plan ahead instead of always reacting to problems. You can see a money shortage coming weeks away or feel confident raising your prices because you know exactly what things cost.

A business without bookkeeping is like a ship without a rudder. You're moving, but you have no control over where you're going. It gives you the clarity you need to steer toward your goals.

A Universal Language for Business

It doesn't matter if you run a dental office, a marketing agency, or a cleaning service—the language of money is the same for everyone. Clean, accurate financial records are a must if you want to get a loan, find investors, or just plan for the future.

Part of this is figuring out your Digital Marketing Budget Allocation to make sure your ad spending is actually helping you grow.

This guide will explain all the confusing money stuff in simple terms. We'll walk you through it, step-by-step, so you can start making smarter decisions for your business.

Learning the Language of Your Business Finances

Before you can understand your business’s financial story, you have to learn its language. Don't worry, it's not that hard. It’s just a few key ideas that make everything else make sense.

First are debits and credits. These words sound tricky, but the idea is simple. Think of your business finances having two sides that must always be equal. A debit is just an entry on the left side of your books, and a credit is an entry on the right. It’s a system designed to keep everything perfectly balanced.

This idea of balance is the core of bookkeeping. It makes sure every dollar is accounted for, which prevents mistakes and gives you a true picture of your money.

Cash vs. Accrual: Two Ways to Tell Time

Next, you need to decide when to record your money moves. You have two main options: cash and accrual.

Cash accounting is the simple way. It’s like looking at your bank account. You record money when it actually shows up in your account, and you record an expense when the money leaves. A client pays you today, so it’s income today. Easy.

Accrual accounting is a little more advanced. It records income when you earn it, even if you haven't been paid yet. For example, you finish a job and send the bill on Monday, but the client pays next week. With accrual accounting, that money is counted as income on Monday. This gives you a better picture of how your business is doing over time.

Most small businesses start with cash accounting because it’s easy. But as you grow, banks and investors will want to see accrual-based reports because they show your true profitability.

Organizing Your Money with a Chart of Accounts

So, where does all this information go? It gets sorted into something called a Chart of Accounts. It sounds fancy, but it’s just a list of categories for all your income and expenses. Think of it like making folders on your computer for your money.

Instead of one big messy pile, you have specific folders for things like 'Income from Projects,' 'Software Costs,' and 'Office Rent.' This simple setup is the foundation of your whole bookkeeping system, making it clear where every dollar comes from and where it goes. For more, check out this guide on how to set up a Chart of Accounts for your business.

Getting this right is important. The bookkeeping industry makes up 43.2% of the global accounting services market, which is expected to reach $688.17 billion by 2025. For businesses like professional services, healthcare, and construction, good books are essential—it's how they find money leaks and see if a project is actually making money.

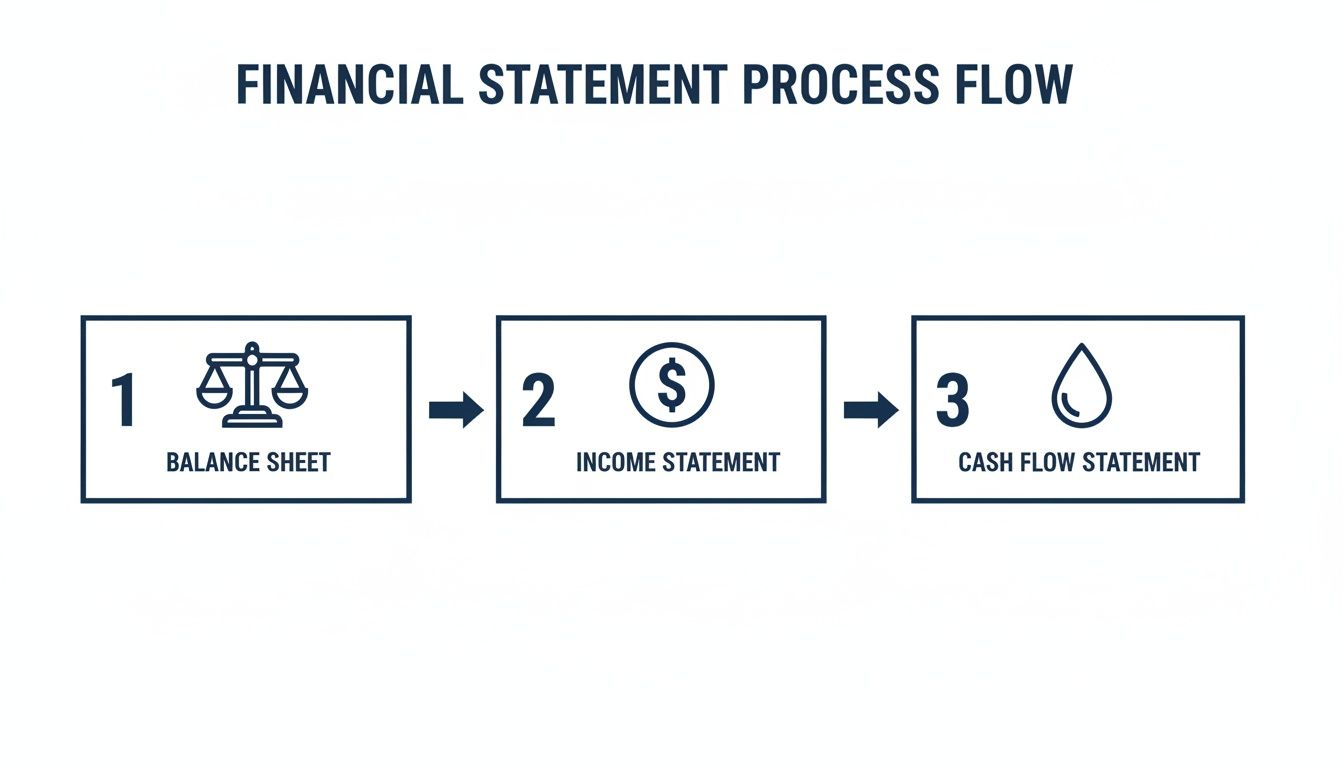

The Three Reports That Tell Your Story

Finally, all this organized data gets turned into three key financial reports. Think of these as the main chapters in your business's money story. Each one tells you something different and important.

Here’s a quick look at what each report tells you.

What Your Financial Statements Are Telling You

| Financial Statement | What It Shows | A Simple Analogy |

|---|---|---|

| Income Statement | If you made or lost money over a period (like a month). | A report card showing your grades for the semester. |

| Balance Sheet | What you own and what you owe at one specific moment. | A photo of your financial situation right now. |

| Cash Flow Statement | How cash moved in and out of your business over time. | Your bank statement, showing all deposits and withdrawals. |

These three reports work together to give you the full story. The income statement says if you made a profit, the balance sheet shows what you have, and the cash flow statement confirms you have the actual cash to run the business.

Your Simple Bookkeeping Routine

Knowing the ideas behind bookkeeping is one thing, but doing it regularly is what really matters. Good bookkeeping isn't a huge project you do once a year. It's a simple, steady habit—a routine that keeps your business healthy.

Think of it like an exercise plan. You don't go to the gym once a year and expect to be fit. You get results with small, regular workouts. We’re going to do the same thing with your finances using a simple checklist.

Your Daily Financial Check-In

Your daily tasks should be fast, taking about 15 minutes. The goal is to keep an eye on your cash and catch problems before they get big. It's like checking the gas gauge in your car before you drive.

Here’s what to do every day:

- Check Your Bank Balances: Look at your business checking and savings accounts. Knowing your exact cash helps you make smart spending choices.

- Record Daily Sales and Deposits: Did you make any sales? Write them down. Did a client payment come through? Record it. This keeps your income records current.

- Categorize New Expenses: Look at your bank account for any new spending. If you bought office supplies, put that expense in the right category right away. Doing this daily makes your monthly review much easier.

These small steps stop things from piling up. You’ll always know where you stand, which brings a lot of peace of mind.

Weekly Tasks to Stay on Track

Once a week, set aside about an hour for bigger tasks. This is when you manage the money moving between you, your customers, and your suppliers.

Your weekly routine should include:

- Pay Your Bills and Suppliers: Look at any bills that are due soon. Paying on time keeps your suppliers happy and your business in good standing.

- Send Out Invoices: Don't let finished work sit there without sending a bill. The sooner you send it, the sooner you get paid. This is key for good cash flow.

- Review Your Accounts Receivable: Check to see which clients have paid and which bills are still open. If an invoice is late, now is the time to send a friendly reminder.

- Process Payroll: If you have employees, make sure they get paid on time, every time. This includes figuring out hours, taxes, and other deductions.

These weekly tasks are all about managing the flow of money. Keeping track of who owes you and who you owe is a basic part of the whole a to z bookkeeping process.

Your Monthly Financial Review

At the end of each month, it's time to step back and look at the bigger picture. This is when you make sure your numbers are perfect and see how your business actually did. Set aside a few hours for this—it’s time well spent.

Reconciling your bank accounts is a must-do. It’s the process of matching the transactions in your books to your bank statement to make sure every single penny is accounted for.

Your key monthly tasks are:

- Bank and Credit Card Reconciliation: This is the most important step. You need to make sure your records match what the bank says. If they don't, you have to find out why and fix it.

- Review Financial Statements: Pull up your three main reports: the Income Statement, Balance Sheet, and Cash Flow Statement. This is where you see if you made a profit and how your financial health changed.

- Analyze Your Budget: Compare what you actually spent to what you planned to spend. Did you go over budget on marketing? Did that project cost more than you thought? This helps you adjust your plan for next month.

This monthly routine turns bookkeeping from just typing in numbers into a tool for making smart decisions. For a deeper look at managing spending, you can learn more about how to track business expenses.

This flow shows how all your work comes together in the key reports that tell your business's story.

As you can see, these reports are all connected. The information from your daily records flows into each one, giving you a full view of your company's health.

Choosing Your Bookkeeping Tools

You wouldn't try to build a house with just a hammer, right? The same idea applies to your business finances. Trying to manage your money with a shoebox full of receipts is a recipe for headaches and missed opportunities.

The right tools can make your bookkeeping process faster, easier, and more accurate. Think of modern bookkeeping software as a power drill for your finances. It does the hard work for you, saving you from hours of manual data entry.

This isn't just a small change; it's a huge one. The global bookkeeping market has already hit $20.5 billion and is growing at 7% each year, mostly because these tools have made good bookkeeping available to everyone. With cloud software use in this area jumping by 45% in just three years, it's clear that spreadsheets are on their way out. You can find more details on these bookkeeping industry trends on atidiv.com.

Why Software Is a Game Changer

There’s a reason tools like QuickBooks are so popular. They connect right to your business bank accounts and credit cards. When you buy something, the software sees it, adds it to your books, and often knows how to categorize it. That coffee you bought for a client? It gets labeled 'Meals & Entertainment' automatically.

This automation is the key to efficient bookkeeping. It lets you spend less time typing at a computer and more time running your business.

Good bookkeeping software doesn't just record what happened. It creates a central place for your entire financial world, giving you an up-to-the-minute look at your business's health.

A connected system also cuts down on human error. I've seen a simple typo in a spreadsheet mess up a whole month's reports, causing hours of work to find the mistake. Automation helps make sure your numbers are right from the start.

Creating a Connected Financial Hub

The real power of modern bookkeeping software is how it connects to other tools you use. This is a huge piece of building a complete a to z bookkeeping system.

Your bookkeeping software becomes the center, linking up with other apps to make information flow smoothly. No more typing the same thing into two or three different places.

Here’s how this works:

- Payroll Systems: When you run payroll through a service like Gusto or ADP, the pay and tax information goes right into your accounting records automatically.

- Invoicing and Payment Apps: A client pays your bill through Stripe or Square. That payment is instantly recorded as income in your books. Easy.

- Expense Tracking Tools: Your team uses an app to take pictures of receipts for gas or supplies. That information syncs with your accounting software, making expense reports simple.

By connecting these pieces, you create one single source of truth for your finances. You can log in anytime and see a real-time snapshot of how your company is doing. You’re no longer guessing; you’re looking at the real, current numbers.

Of course, with your financial data online, it's important to choose tools with strong security to keep your information safe.

Using Your Numbers to Make Smart Decisions

Once you have a steady routine and your books are in order, the real work begins. Bookkeeping isn’t just about recording the past. It’s about using that information to make better choices for the future.

Think of it this way: your bookkeeping records are a map of where you've been. Now, you get to use that map to find the best route forward. This is where you go from just doing the books to making the books work for you.

This side of bookkeeping is becoming more important every day. The global accounting services market is expected to grow from $682.69 billion in 2025 to over $986.50 billion by 2032. Accurate records that help businesses make smart moves are a big reason for that growth. You can see the full breakdown of the growth of accounting services on Fortune Business Insights.

Asking the Right Questions

Your financial reports have the answers to your biggest business questions. You just need to know where to look. Instead of going with a gut feeling, you can use real data to guide you.

This is how you move from just getting by to really succeeding. It means you're in control.

Key Metrics to Watch

You don't need to be a math expert to get useful information from your numbers. Start by tracking a few key numbers, often called Key Performance Indicators (KPIs). These are just specific numbers that give you a quick look at how your business is doing.

Here are a few examples of questions your numbers can answer:

- Which services make the most money? Looking at your profit margin for different jobs tells you which ones are your real winners. You might find that a service you thought was small is actually your most profitable.

- Do we have enough cash for next month? Your cash flow forecast helps you predict how much money will come in and go out. It’s like a weather forecast for your bank account, giving you time to prepare.

- Is our pricing right? Looking at your job costing reports shows you the true cost of doing a job or making a product. If your costs are going up, you have the proof you need to raise your prices.

Your financial data tells a story about your business. Learning to read it is like gaining a superpower. It lets you see what’s coming, spot problems early, and grab opportunities others might miss.

Imagine you own a small marketing agency. By looking at your profit margins, you realize that your web design projects barely make any money. At the same time, your monthly SEO services are very profitable. With this information, you can focus on getting more SEO clients.

This is the real power of a complete a to z bookkeeping system. It’s not just about tracking receipts; it’s about having a financial GPS that guides you toward success, one smart decision at a time.

Knowing When to Ask for Help

Sooner or later, most business owners hit a wall with their bookkeeping. At first, doing it yourself seems like a good way to save money. But as your business grows, the finances get more complicated. It’s a normal part of success.

You might find yourself spending nights catching up on paperwork instead of being with your family. Or maybe you're just staring at a financial report, and you have no idea what it means. This is a common and normal stage for a business to be in.

Realizing you need help isn't a sign of failure—it’s a sign that you've grown. It means you've reached a point where your time is better spent leading your team and serving your customers.

Signs It’s Time to Call a Professional

So how do you know when it’s time? The signs are usually pretty clear. It’s not one big thing, but a slow feeling that you're in over your head.

Here are a few signs I see all the time that tell you it's time to get help:

- You're Always Behind: Your books are always a month or two out of date. This makes it impossible to know where you stand financially.

- Tax Season is a Nightmare: The thought of taxes makes you stressed. You know it means weeks of scrambling to organize a year's worth of messy records.

- You're Wasting Too Much Time: You spend more than a few hours each week on bookkeeping. That’s time you could be using to make money.

- Your Decisions are Guesses: You're making big choices about hiring or pricing based on a "gut feeling" instead of real numbers.

- You Can't Answer Tough Questions: You don't know your profit margins. Your cash flow is always a surprise. You aren’t sure which services are actually making you money.

If any of these sound familiar, it’s probably time to look for a partner.

Getting professional bookkeeping help isn’t just about handing off tasks. It’s about gaining a partner who can turn your financial data from a source of stress into your best tool for growth.

More Than Just a Bookkeeper

Bringing in a pro does more than just clean up your records. It brings a new level of clarity to your business. A good bookkeeping partner doesn’t just record the past; they help you plan the future.

For example, a service like MyOfficeOps gives you a clear path that meets you where you are. It starts with getting the basics right—what we call Core Accounting. This makes sure your daily books are accurate and reliable. From there, we can move to Profit Optimization, where we use that clean data to find ways to improve cash flow and make you more money.

Ultimately, this all leads to planning for your Exit Strategy. Even if selling your business seems far away, building a company with strong finances is what creates real value. It’s about having an expert you can call who understands the whole journey, from the small details to your biggest goals.

You can learn more about the benefits of outsourced bookkeeping for your small business. This complete a to z bookkeeping approach makes sure nothing gets missed.

Your Bookkeeping Questions, Answered

Starting with bookkeeping can feel like learning a new skill, and it’s normal to have questions. To finish our A-to-Z guide, let’s answer some of the most common things business owners ask.

Can I Do My Own Bookkeeping?

Yes, you definitely can—especially when you’re just starting. Many business owners handle their own books for a while with easy-to-use software. The real question isn’t can you, but should you?

As your business grows, the finances get more complicated. You'll reach a point where the time you spend on bookkeeping is time taken away from selling and strategy. Once it starts to feel like a chore, it’s usually a smart move to hand it off.

How Much Does a Bookkeeper Cost?

The cost can be very different, depending on what you need. A freelance bookkeeper might charge by the hour, while a firm will probably have a monthly fee. The price depends on things like how many transactions you have, if you need payroll help, and how many bank accounts you have.

While it’s an expense, try to think of it as an investment. A good bookkeeper will often save you more than they cost by preventing mistakes, finding tax savings, and showing you ways to be more profitable.

A common mistake is seeing bookkeeping as just another cost. Really, it's the engine that powers smart business decisions. Paying for an expert is paying for clarity and peace of mind.

What's the Difference Between a Bookkeeper and an Accountant?

This is a great question. Think of a bookkeeper as the person who records the day-to-day financial story of your business. They handle tasks like categorizing expenses, checking bank accounts, and managing bills. Their job is to keep your financial records clean and up to date.

An accountant, on the other hand, looks at the bigger picture. They analyze the data your bookkeeper has organized. Accountants handle things like filing tax returns, making financial plans, and giving advice on your business's financial structure.

You really need both. The bookkeeper builds the solid foundation, and the accountant uses that foundation to help you build your future.

Ready to stop guessing and start knowing your numbers? MyOfficeOps provides the clear, reliable bookkeeping and expert advice you need to grow with confidence. Get in touch today for a custom plan.