It’s a feeling every business owner knows. You check your bank account after a busy month, expecting it to be full. Instead, the number you see makes your stomach drop.

This isn’t just bad luck. It’s a classic cash flow problem, where the money coming in can’t keep up with the money going out.

Why Your Business Bank Account Is Always Low

If you've ever looked at your sales report, then your bank balance, and wondered where the money went, you're not alone. It’s one of the most stressful parts of running a company. You're working hard, your customers seem happy, but there’s never enough cash left over to feel safe, let alone grow.

This gap between making sales and having money in the bank is the heart of most cash flow issues. The problem usually isn’t that your business is failing; it's that the timing of your money is off.

The Slow Pain of Late Payments

One of the biggest culprits? Customers who pay late. You do the work, send the invoice, and then… you wait. And wait. Meanwhile, your own bills for rent, payroll, and supplies are due now. Soon, you're paying business expenses with your own money or using a credit card, all while waiting for clients to pay for work you finished weeks ago.

This is more than just annoying; it stops you from growing. Imagine you run a small marketing agency in Philadelphia. You're juggling projects, but your bank account is shrinking because your invoices are just sitting there, unpaid.

For many businesses, waiting for customer payments now takes about 28 days, up from 24 days in 2022. That slow trickle of money makes it really hard to pay your daily bills. You can learn more about this in a report from Peak Advisers on the top cash flow challenges facing businesses.

This creates a cycle of stress. You can't hire the extra person you need or buy new equipment because you’re always just trying to plug holes in your finances.

When Your Costs Quietly Creep Up

Another thing that can drain your cash is rising expenses. The cost of everything, from software to supplies, goes up over time. If you don't raise your own prices to match, your profit gets smaller and smaller until it's gone.

Let’s say you run a small construction company. A few years ago, the price of wood was stable. Now, it can change a lot from one month to the next. If you gave a quote based on old prices, you could lose money on a job you thought would be a big win. It’s like trying to fill a bucket with a hole in it—you pour money in the top, but it leaks right out the bottom.

The main idea is simple: Profit on paper is not the same as cash in the bank. A business can look profitable but still fail because it runs out of money to pay its bills.

Spotting The Trouble Before It’s Too Late

The key to avoiding a big cash crisis is to see the warning signs early. If these things are happening in your business, it’s time to stop and figure out what’s going on. Don’t just hope things will get better next month.

Here's a quick checklist to help you spot cash flow trouble. If more than one of these sounds familiar, you need to act.

| Top 4 Cash Flow Warning Signs |

|---|

| Description: A simple checklist to help you spot cash flow trouble early. If you recognize more than one of these, it’s time to take action. |

| Warning Sign |

| Bill Anxiety |

| Paying Yourself Last (or Not at All) |

| Growing Credit Card Balances |

| "Can't Afford to Grow" Syndrome |

These aren't just numbers on a page; they are real problems that can stop a good business from succeeding.

Getting a clear picture of where your money is going is the first and most important step to taking back control.

Your Immediate Cash Flow Rescue Plan

When your bank balance is low and payroll is next week, you don't have time for a big plan. You need cash, and you need it now. This is your emergency guide—a plan with quick, simple actions to get more cash in the next 30 to 60 days.

This isn’t about changing your whole business. Think of it like first aid for your money. It's about stopping the bleeding so you have some breathing room to fix the bigger issues. We’ll start with the easiest ways to bring cash in, then look at how to slow the cash going out.

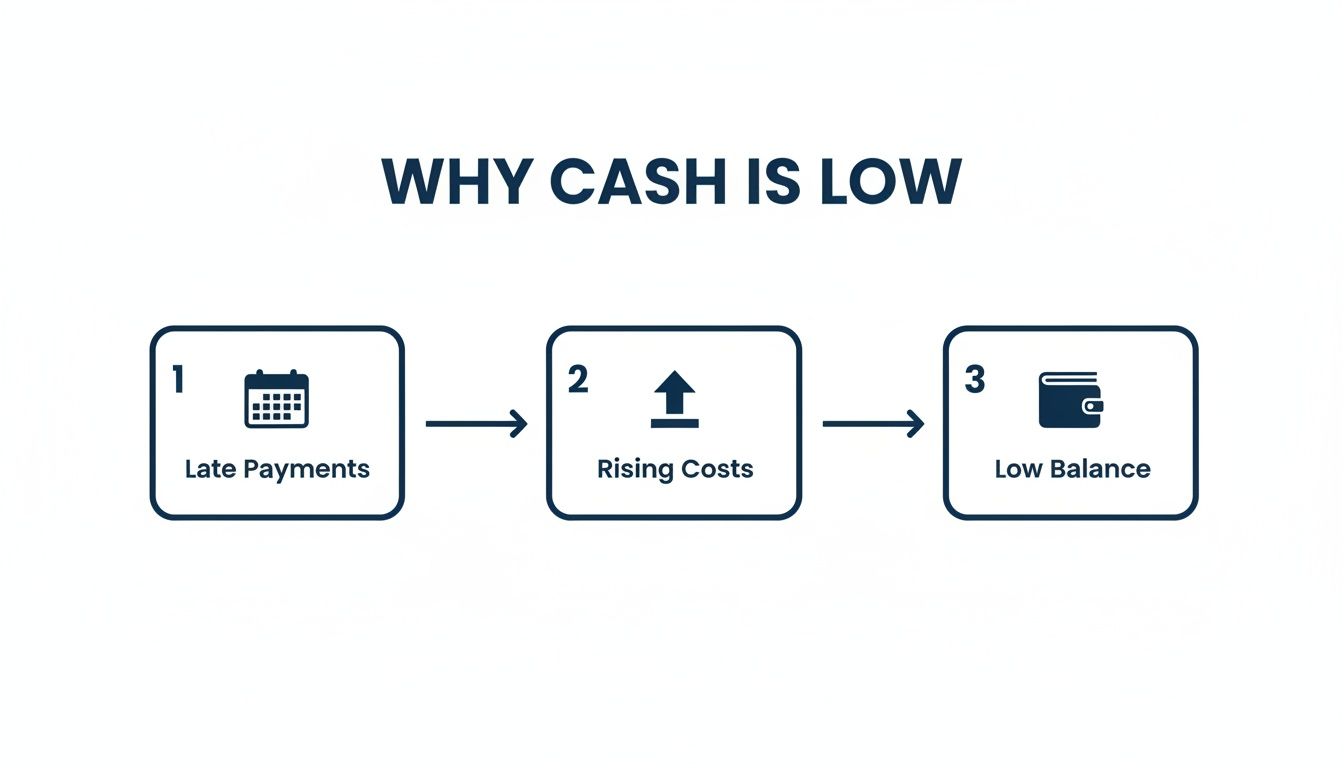

This simple flowchart shows how late payments and rising costs lead to a low balance in your business bank account.

The key takeaway here is that small delays and cost increases have a direct, painful effect on the cash you have to run your business.

Get Your Customers to Pay You Faster

The fastest way to get more cash is to collect the money you’re already owed. Every unpaid invoice is like a free loan you're giving to your customers. It’s time to ask for that money back, nicely but firmly.

Don't be afraid to pick up the phone. An email is easy to ignore, but a friendly call is harder to brush off. You don't need a complicated script.

Here's a simple, human way to say it:

"Hi [Client Name], it's [Your Name]. I'm calling about invoice #123 that was due last week. I wanted to make sure you got it and see if you needed anything from me to get it paid. When do you think that might be?"

This approach is helpful, not pushy. It gives them a chance to tell you if there’s a problem, and it makes it clear you expect to be paid. To keep track of this, you need to be organized. You can find a great tool to help with that in our accounts receivable aging report template.

Another smart move is to offer a small discount for paying early. Offering a 2% discount if an invoice is paid within 10 days (known as "2/10, net 30") can work like magic. You give up a tiny bit of money, but you get your cash weeks sooner, which is much more valuable when you're in a tight spot.

Put Your Spending on a "Can This Wait?" Diet

Now that you have a plan to get paid faster, it's time to slow down the money going out. This means looking at every single expense and asking one simple question: "Can this wait?"

Go through your bank and credit card statements from the last 90 days, one line at a time. Be tough.

- Software Subscriptions: Are you paying for tools you signed up for but don't use? That project management tool you tried for a week can go. Cancel it now.

- Marketing Campaigns: Look at your ad spending. Is it bringing in sales right now? If not, pause it. Focus only on ads that get immediate results.

- Unnecessary Perks: Things like free lunches or fancy office supplies are nice, but they are extras. Cut them until your cash flow is healthy again.

- Talk to Your Suppliers: Call the companies you buy from. You'd be surprised how many will let you pay in 45 or 60 days instead of 30, especially if you're a good customer. This simple call can give you a few extra weeks of breathing room.

This isn't about cutting your budget forever. It's a short-term diet to stop the cash from flowing out while you work on getting healthier. For more ideas, check out these 8 cash flow improvement tips. They have real advice that can make a difference fast.

By focusing on these two things—getting paid faster and spending slower—you create a temporary cash buffer. This gives you the space to move beyond panic mode and start fixing the real problems for good.

Fixing Operations to Prevent Future Cash Crunches

The quick fixes are like putting a bandage on a wound. They stop the bleeding, but you can't run your business in crisis mode all the time.

To really solve your cash flow problems, you have to make lasting changes to how you run your business.

This is about shifting from reacting to problems to planning for them. It’s about building a business where cash flow is steady, not a rollercoaster that makes you sick. And that starts with knowing your numbers inside and out, especially your costs.

Know Your True Job Costs

If you don't know exactly how much it costs to do a job or sell a product, you're just guessing. You might feel busy and think you're making money, but you could be losing a little on every sale. This is a big deal for contractors, consultants, and anyone who gives quotes for their work.

For example, a contractor in West Chester, PA, needs to know the exact cost of a job before they send a quote. This isn't just about the price of materials and paying their team.

They also need to include:

- Overhead: These are the costs that aren't for one specific job, like office rent, insurance, and truck payments.

- Hidden Labor Costs: This is more than just the hourly pay. It includes payroll taxes and workers' comp insurance.

- A Buffer: What if a delivery is late or a tool breaks? Smart business owners add a little extra to their costs for surprises.

You don't need a fancy degree to do this. The idea is simple: add up all the direct costs for a job, then add a percentage to cover your overhead. If you don’t, your overhead will eat up any profit you thought you had.

The Silent Threat of Rising Costs

Even when you're busy, rising costs can sink your business without you noticing. It's a big problem for everyone. In fact, 75% of businesses say rising costs for goods and services are their number one money headache.

The Federal Reserve found that over half also have trouble paying their regular operating expenses (56%) and dealing with unpredictable cash flow (51%). You can see more about this in the full report on employer firms.

This isn't just a boring economic fact; it has real effects.

Let's look at a real-world example. Think of a small doctor's office in the Philadelphia suburbs. They were doing great, with a full schedule of patients. But over the last year, their profit started to shrink, and cash got tight.

The problem? The cost of basic medical supplies—gloves, masks, and sanitizer—had jumped nearly 30%. Because they hadn't raised their prices, that entire cost increase came straight out of their profit. They were working just as hard but making less money on every patient.

This is a classic operations problem. The clinic was so focused on patients that they weren't watching their supply costs. A simple monthly check of their main expenses could have caught the problem early, letting them find new suppliers or adjust their prices.

Build a Leaner Operation

Once you know your true costs, the next step is to make your business more efficient. This isn't about cutting corners; it's about getting rid of waste so more of every dollar you earn stays in your bank account.

Start by looking at your biggest expenses besides payroll. For most businesses, this means things like inventory, software, and rent.

Here are a few areas to focus on:

- Manage Your Inventory Better: If you sell physical products, extra inventory is just money sitting on a shelf. Try a "just-in-time" system where you order supplies as you need them instead of keeping a huge stockpile. This can free up a lot of cash.

- Review Your Technology: Most businesses pay for software they don't really use. Do a yearly check of all your subscriptions. If a tool isn't essential or isn't helping you make money, cancel it.

- Improve Your Processes: Where are the slowdowns in your business? Does it take too long to send an invoice after a job is done? Do you spend hours on boring data entry that a computer could do? Fixing these small things adds up and saves you time and money.

Making these changes means you have to think differently. You have to move from just working in your business to working on your business. By understanding your costs and running a smarter operation, you build a stronger company that can handle money problems without always being on the edge of a crisis.

How to Build a Simple Cash Flow Forecast

The words “cash flow forecast” might sound complicated, but it’s simpler than you think. It's like using a map for your business’s money. It shows you where cash is coming from, where it’s going, and when, so you can see what’s ahead instead of just guessing.

Building this money map is one of the best things you can do to stop reacting to cash flow problems and start preventing them. It turns worry into confidence. A forecast isn’t about being perfect; it’s about making a good guess so you aren’t surprised by an empty bank account.

This is super important because so many businesses are always playing catch-up. Unpredictable cash flow is a major headache for 51% of small businesses. And it’s a serious issue: a shocking 82% of small businesses that fail do so because of money management problems. This shows that not planning ahead can have big consequences.

Start with What You Know

The easiest way to predict the future is to look at the past. You don’t need special software for this. Just grab your bank statements from the last six to twelve months.

Your goal is to get a feel for the rhythm of your business. Every business has one. A landscaping company in Pennsylvania is super busy in the spring and summer but slows down in the winter. A gift shop has a huge December but might have a slow February.

Look for these patterns in your own numbers. Your past results are your best guide for what will likely happen next.

Listing Your Cash Inflows

Now, let's map out the money coming in. This is the fun part. Be realistic, not too hopeful. It's better to plan for a normal month and be happy if you do better, than to plan for a record month and fall short.

Your cash inflows might include:

- Sales Revenue: Look at your average monthly sales. If a busy season is coming, you can estimate a higher number. If a slow period is ahead, estimate lower.

- Customer Payments: This is different from sales! If you send invoices and clients pay 30 days later, you need to predict when the cash will actually arrive, not when you made the sale.

- Other Income: Do you have any other money coming in? This could be a loan, a tax refund, or rent from a property you own.

Tracking Your Cash Outflows

Next, list all the money going out. This is where you need to be honest and list everything. It's easy to forget small expenses, but they add up.

Go through your bank statements and put everything into categories. Your cash outflows will fit into a few buckets.

Key Takeaway: A cash flow forecast is not a profit and loss statement. It only tracks actual money moving in and out of your bank. It ignores things like depreciation and focuses only on what you can spend.

Here’s a simple way to break down your expenses:

- Fixed Costs: These are the bills you pay every month, no matter what. They are easy to predict. Think rent, insurance, loan payments, and salaries.

- Variable Costs: These costs change with your sales. If you own a coffee shop, this would be coffee beans and milk. For a contractor, it’s the wood for a specific job.

- One-Time Expenses: Do you plan to buy a new computer next month? Or pay for a booth at a trade show? These aren’t regular costs, but they will affect your cash, so you need to include them.

Once you have your lists of cash in and cash out, you can put it all together. The math is very simple:

(Starting Cash) + (Cash In) – (Cash Out) = Ending Cash

By doing this for the next three to six months, you’ll create a timeline that shows your future bank balance. This lets you spot a potential cash shortage weeks or even months away. And when you can see a problem coming, you have time to do something about it.

For a head start, you can download our easy-to-use cash flow forecasting template and put in your own numbers. It does the hard work for you.

Knowing When to Get Professional Help

As a business owner, you do a lot. You’re the boss, the salesperson, the marketing expert, and often, the bookkeeper. But trying to do everything yourself, especially the numbers, is a quick way to get burned out.

Sometimes, the smartest—and most profitable—thing you can do is admit you need help.

Fixing cash flow isn't just about numbers on a spreadsheet; it’s about having the clear mind to make good decisions. If you’re always worried about making payroll, you can't focus on what you do best—serving your customers and growing your company.

Getting professional help isn't a sign of failure. It’s a sign that you’re serious about building a business that lasts.

Clear Signs You Need an Expert

It can be hard to know when to bring someone in. You might think it's an expense you can't afford, but the cost of not getting help is almost always higher. We’re talking lost time, missed chances to grow, and expensive mistakes that can hurt your business.

Here are a few signs that it’s time to call a professional:

- You spend more than a few hours a week on your books. Your time is valuable. If you’re spending half a day every week sorting transactions or chasing invoices, that’s time you’re not spending on sales or strategy.

- You look at financial reports and feel confused. Do you get a profit and loss statement and have no idea what it really means? A good financial partner explains those numbers in plain English you can actually use.

- You’re always surprised by your tax bill. A big, unexpected tax bill is a classic sign you're not planning your finances well during the year. It means you’re just reacting to problems.

- You're making big decisions based on a "gut feeling." Wondering if you can afford to hire someone new? Guessing is a bad strategy, and it’s what you have to do without clear data.

The goal is to get you out of the messy details so you can get back to leading the company. A financial expert handles the hard stuff and gives you the simple, clear information you need to make smart moves.

What Kind of Help Do You Need?

"Professional help" can mean different things. Depending on your situation, you might need someone for the daily details or someone for big-picture advice.

An outsourced bookkeeper is your first line of defense. They are the ones who will:

- Keep your daily transactions neat and organized.

- Manage who you owe and who owes you.

- Make sure your payroll runs without problems.

- Give you accurate financial reports each month.

Think of them as the foundation. Without clean books, you can’t make any other good financial decisions. It's that simple.

A fractional CFO or financial advisor is your strategic partner. Once your books are clean, they help you use that information to grow. They’ll work with you on things like:

- Building a cash flow forecast you can count on.

- Setting the right prices to make sure you're profitable.

- Creating a budget and a real plan for growth.

- Helping you understand your business's key numbers and what they mean.

For businesses facing big money problems because of taxes, it's also important to know all your options. This can include programs like the IRS currently not collectible status, which is something to look into with a professional's help.

Ultimately, bringing in an expert frees you up. It replaces confusion with confidence and lets you make decisions based on real information, not just hope. If you’re wondering what kind of support is right for you, check out our guide on when to hire a CFO.

Frequently Asked Questions About Cash Flow

When you're dealing with a cash flow problem, the questions can keep you up at night. Getting simple, straight answers is the first step to feeling in control again. Here are a few of the most common questions we hear, explained in plain English.

Is Profit the Same as Cash Flow?

No, and this is maybe the most important thing to understand in business finance. Profit is what’s left on paper after you take away your expenses from your sales. Cash flow is the actual money moving in and out of your bank account.

Think of it this way: you could send an invoice for a huge project in January, and your report will show a nice, big "profit." But if that client doesn't pay you until April, you have zero cash from that sale to pay your rent in February.

A profitable business can absolutely go bankrupt if it runs out of cash.

How Can I Have a Cash Flow Problem If My Sales Are Growing?

This is a very common—and painful—trap. The hard truth is that fast growth uses up cash. When your sales go up, you have to spend money before you get paid for those new sales.

Imagine you own a small construction company and you get a huge new contract. Great, right? But now you suddenly need to buy way more materials and maybe hire more people. You have to pay for all of that now, but you might not get the money from that big job for 60 or 90 days.

This gap between spending money and getting paid is what causes the cash problem, even when business is great.

Remember this: The faster you grow, the more cash you need to pay for that growth. It sounds backward, but it's a key part of managing your money.

What Is the Fastest Way to Fix a Cash Flow Problem?

When you need cash now, the quickest fix is usually your accounts receivable. That's just the fancy term for the money your customers already owe you.

Start by getting on the phone.

- Call overdue clients: A friendly, personal phone call works much better than another automatic email reminder.

- Offer a small discount for early payment: Giving a 2% discount for paying in 10 days instead of 30 can bring cash in weeks sooner.

- Send invoices immediately: Don't wait until the end of the month. The second a job is finished, send the invoice. The countdown for payment doesn't start until they have the bill.

When Should I Consider Getting a Loan for Cash Flow?

A loan can be a great tool, but only if you use it for the right reasons. Taking on debt to hide bigger business problems—like your prices are too low or you spend too much—is like putting a bandage on a deep cut. You're not fixing the real issue.

A loan makes sense for specific, smart reasons, such as:

- Covering a predictable slow season: Perfect for a landscaping company that has slow winters but knows a busy spring is coming.

- Paying for a large, profitable project: To cover the upfront costs for a big job you know will pay off well.

- Investing in equipment: For a purchase that will make your business more efficient and profitable in the long run.

Before you ever sign for a loan, make sure you have a solid plan for how you'll use the money and, more importantly, how you'll pay it back.

Managing your business finances can feel like a lot, but you don't have to do it alone. The team at MyOfficeOps provides the clear financial reporting and expert advice you need to move from guessing to knowing. If you’re ready to gain confidence in your numbers and solve your cash flow problems for good, schedule a discovery call with us today.