Bidding on a construction project comes down to three things: knowing your real costs, adding a fair profit, and presenting it clearly. That's it. But a lot of contractors lose bids not because their final price is wrong, but because the numbers they used to get there were just guesses. Winning jobs over and over is about knowing your business inside and out before you even look at the plans.

Why Many Bids Are Lost Before You Even Hit Send

It’s a tough feeling. You spend hours, maybe even days, looking at plans, getting quotes, and running the numbers, only to get a short email: "We've decided to go with another contractor." You might blame the other guy for bidding too low, but what if the problem wasn't the price? What if your bid was doomed from the start?

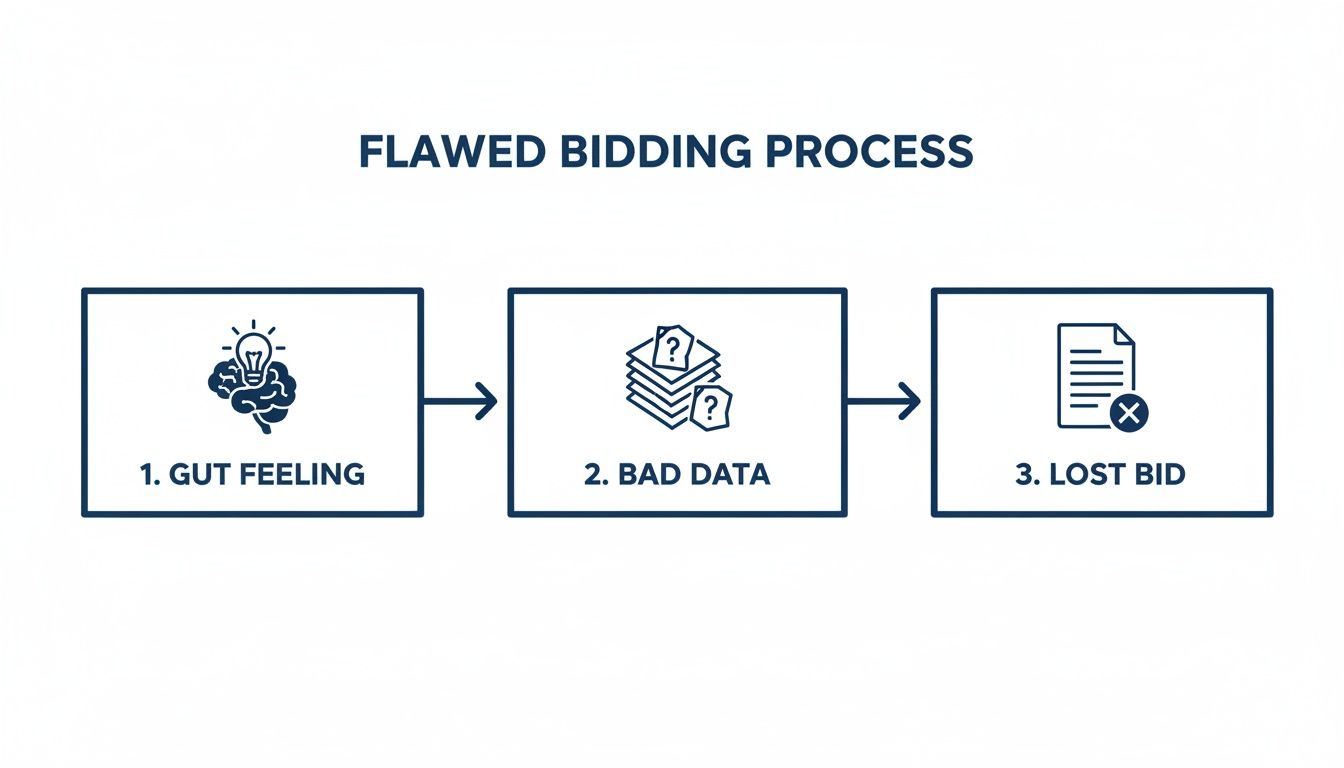

Too often, contractors build their bids on messy financial data. They go with a gut feeling or pull numbers from a totally different job. That's like trying to build a house without a level—it might look straight at first, but it's going to fall apart.

The Gut Feeling Trap

Bidding based on a "feeling" is a classic mistake. You look at a job and think, "This looks like that project we did last spring, so I'll just use those numbers." The problem is, you're forgetting that materials cost 10% more now, the job site is completely different, and you have a different crew.

I once knew a framing contractor who was amazing at his job. He won bids all the time and his crew was always working. The problem? He was barely making any money. He thought being the lowest bidder meant he was doing great, but without clean books, he had no idea what his real labor and overhead costs were. He was winning a race to the bottom, and it was hurting his business.

Your financial numbers aren't just for your accountant at tax time. Clean books and accurate job costing are the best bidding tools you have. They turn guesswork into confidence.

From Busy to Profitable

That framer eventually hit a breaking point. He was working harder than ever with nothing to show for it. He finally hired a bookkeeper who helped him set up proper job costing, which tracks every single dollar spent on materials, labor, and overhead for each specific project.

What he found was a huge surprise:

- He was undercharging for labor: He wasn't including payroll taxes and workers' comp in his labor rate. This simple mistake was costing him thousands.

- He forgot about overhead: He never added real-world costs like tool repairs, truck fuel, or his small office rent into his bids.

- Some jobs were losing him money: Those small, quick jobs he loved were actually costing him money because of all the hidden setup and teardown time.

Once he had clear, accurate numbers, everything changed. His bids got smarter. He started saying no to the low-profit jobs and focused on the ones he knew he could make money on. Sure, he won fewer bids, but his bank account finally started to grow. This is how you learn to bid on construction projects for the long term.

Laying the Groundwork for a Winning Bid

The best bids aren't won on the day you send them. They're won weeks, sometimes months, before you even see a request for a bid. Winning is all about being prepared and smart—choosing the right jobs, not just chasing every single one.

Successful contractors know exactly what a "good" job looks like for them. They know what their team can handle, what their financial sweet spot is, and what kind of projects they're best at. It's time to stop wasting time and money preparing bids for jobs you probably won't win or, even worse, jobs that won't make you any money.

Too many bids start with a gut feeling and bad data, which is a fast track to a lost bid.

This is a common trap. When you skip the prep work and just go with your gut, you're setting yourself up to lose from the start.

Create Your Bid/No-Bid Filter

Think of a Bid/No-Bid Checklist as your company’s bouncer. Its only job is to turn away the projects that aren't a good fit, so you can focus your energy on the ones you have the best shot at winning. This isn't just a to-do list; it’s a tool that forces you to be honest about each project.

Your checklist should be simple and help you answer a few key questions before you even start an estimate.

- Is this type of project one of our strengths? If you’re great at home remodels, taking on a huge commercial project might not be the best use of your time. Stick to what you're good at.

- Do we have the time and people? Look at your current workload. Can you honestly handle this job without your other projects suffering?

- Is the client a good fit? Have you worked with this owner or general contractor before? Do they pay on time? A difficult client can wipe out your profit.

- Can we make money on this? Based on a quick look, does the project seem like it will hit your profit goals? Don't get into a race to be the cheapest.

A good bid/no-bid process is the single best way to win more jobs. You’ll send out fewer bids but win more of the right ones, which is the key to growing your business.

Size Up the Competition and the Market

Once a project passes your first check, it’s time to see who you're up against. If the job needs a special skill and you know the top three companies in town are also bidding, you need to be realistic about your chances.

What are their strengths and weaknesses? Maybe they’re bigger but slower, or maybe they're known for being the cheapest. Knowing this helps you show why you are the better choice.

The market also plays a big part. Right now, with construction backlogs at their lowest point since 2022 and over 90% of contractors struggling to find workers, labor costs are a huge part of every bid. The most successful companies are winning about 30% of their bids because they're being picky and avoiding the low-profit jobs that other companies are forced to take.

For contractors in the building sector, this helpful guide to winning building construction tenders offers some great tips for getting this important prep work right.

Mastering Your Estimate And Takeoff

Once you've checked out the project and decided to go for it, the real work starts. This is where you turn a gut feeling into a hard number. A detailed estimate is the heart of a winning bid, and that all starts with a solid takeoff.

Think of the quantity takeoff as building the project on paper first. You go through the plans and spec sheets, counting every stud, measuring every pipe, and listing every single material needed to do the job. This isn't a quick look—it's a careful process that sets the foundation for all your costs.

Building Your Master List: Direct vs. Indirect Costs

Everything from your takeoff goes into your estimate, where you start putting prices next to each item. The easiest way to organize this is to split your costs into two groups: direct and indirect. Getting this right is a must.

Direct costs are the things you can see and touch in the final build. They are tied directly to the actual construction.

- Materials: Concrete, lumber, drywall, windows, paint—the obvious stuff.

- Labor: The wages for your crew on the job site.

- Equipment: Rental costs for a forklift, fuel for the excavator, etc.

- Subcontractors: The quotes from your plumbing, electrical, and HVAC partners.

Indirect costs are the "costs of doing business" for that specific job. They're just as real and just as important, but they aren't physically part of the finished building. Forgetting these is the fastest way to work for free. Think of things like the site fence, portable toilets, project manager salaries, and permit fees.

Imagine you're bidding a small office remodel. You might spend hours pricing out the new flooring and lights but completely forget to budget for the dumpster or the final cleanup. That’s a classic indirect cost that comes straight out of your own pocket.

The Devil Is In The Details

Being accurate here is everything. A small mistake in your takeoff can have a huge impact on your final number. Let's say you're off by just 10% on your lumber estimate for a custom home. That could easily be a $5,000 mistake you have to pay for.

This is why so many successful contractors have a second person check every takeoff. The time it takes to double-check is almost always less than the cost of a small mistake. Understanding your costs is key, which is something we cover in our guide on what job costing is in construction.

To give you an idea, here’s how these costs might look on a small commercial renovation.

Sample Direct vs Indirect Cost Breakdown

This simple table shows why it's so important to categorize every expense to protect your profit on a project.

| Cost Category | Example Item | Why It Matters |

|---|---|---|

| Direct Costs | Steel Studs | This is a main material. If you miscalculate how much you need, it directly hits your budget and can cause delays waiting for another delivery. |

| Indirect Costs | Project Manager Salary | This person isn't using a hammer, but without them, the job stops. Their time must be included as a real cost for the project. |

| Direct Costs | Subcontractor Quote (HVAC) | This is a hard cost from another company. Getting a firm, written quote is a must for an accurate bid and protects you from price changes. |

| Indirect Costs | General Liability Insurance | This protects your business during the project. The insurance cost for this specific job needs to be included in your estimate. |

Getting this balance right means you're covering all your costs and pricing the job for the real world, not just the materials you see on the plans.

Securing Reliable Quotes And Watching Trends

Your estimate is only as good as the prices you get from your suppliers and subs. This is where having good relationships helps. A supplier who knows you pay on time is more likely to give you their best price and hold it for you. Always get quotes in writing and check the expiration date—material prices change all the time.

Speaking of which, you have to pay attention to cost trends. According to the U.S. Bureau of Labor Statistics, the prices for 'inputs to construction industries' went up 1.7% over the last year, with big jumps in steel and fuel. This means the numbers you used on a job six months ago are already out of date.

The contractors who win the most are the ones who use current price data in their bids. In fact, companies that adjusted their bids based on local material and labor costs won 25% more jobs in 2024. Hard data beats a gut feeling every single time.

How to Price for Profit, Not Just to Cover Costs

You’ve done the hard work. You’ve listed every material, every hour of labor, and every permit. Now comes the part where a lot of good contractors get nervous. They look at their total cost and a little voice whispers, "Is that too high? Maybe I should cut it a little to win."

This is the most dangerous moment in the whole bidding process.

Knowing your costs is just the first step; the real goal is to make a profit. Cutting your numbers because you're scared is a fast way to become the busiest, most broke contractor around. The goal isn't just to stay busy; it's to be profitable.

First Things First: Calculate Your Overhead

Before you can even think about profit, you have to cover the cost of keeping your business running. This is your overhead—every expense that isn’t for a specific job. Think of it as the cost of unlocking your doors every morning, whether your crew is working or not.

These costs are real, they add up fast, and if you don't build them into every bid, you're paying for them out of your own pocket.

Here’s a quick list of what I’m talking about:

- Rent for your office or shop

- Utilities (power, internet, phone bills)

- Salaries for office staff (not your field crew)

- Business insurance (not project-specific policies)

- Truck payments and general fuel costs

- Marketing expenses

- Accountant and lawyer fees

Once you have your total annual overhead, you can figure out your overhead recovery rate. A simple way is to divide your total annual overhead by your total annual sales. If your overhead is $100,000 and you do $1,000,000 in sales, your overhead rate is 10%. That means you have to add 10% to the direct cost of every job just to break even.

Markup vs. Margin: Understanding the Million-Dollar Difference

Okay, let's talk about making money. This is where the words markup and margin come in, and I promise you, they are not the same thing. Mixing them up is one of the most common and costly mistakes I see.

Markup is what you add to your cost to get your sales price.

Margin is the profit you have left from your sales price.

Let's use a quick example. Say the total cost of a project—materials, labor, and your 10% overhead—is $10,000. You want to make a 20% profit.

If you use a 20% markup, you add $2,000 ($10,000 x 0.20) to your cost. Your final bid price is $12,000. Simple, right?

But what's your actual profit margin? It’s your profit ($2,000) divided by your sales price ($12,000), which is only 16.7%. You wanted 20% but got less because you used markup. If you really want to learn how to price construction jobs for a target profit margin, you need to do it differently.

The biggest mistake contractors make is mixing up markup and margin. If you want a 20% profit margin, you can't just mark up your costs by 20%. You’ll always end up with less profit than you planned for.

Hitting Your Target Profit Margin Every Time

So, what’s a good profit for the work you do? It depends on your trade, location, and the risks, but in today's market, every little bit counts. Tough competition is squeezing profits for everyone, with smaller commercial jobs averaging a 10.6% margin. According to recent global construction cost trends, contractors in busy areas like the Philadelphia suburbs have to be smart with their pricing to avoid losing money.

Let's go back to our $10,000 project cost. If you want to get a true 20% profit margin, here's the formula you need:

Sales Price = Total Costs / (1 – Target Margin Percentage)

- Sales Price = $10,000 / (1 – 0.20)

- Sales Price = $10,000 / 0.80

- Sales Price = $12,500

In this case, your profit is $2,500 ($12,500 – $10,000). Now, check your margin: $2,500 divided by $12,500. It's exactly 20%. That $500 difference is the money you lose every single time you mix up markup and margin.

Don’t Forget to Price in Surprises (Contingency)

Finally, remember that every project has surprises. It's not a matter of if, but when. A material delivery is late, you find a problem behind a wall, or bad weather shuts down the site for a day. If you haven't planned for this, these surprises eat right into your profit.

This is where contingency comes in.

It’s a specific amount of money you add to your bid to cover these unexpected problems. A typical contingency is between 5% and 10% of the total project cost, depending on how risky you think the job is.

Don't hide it. Many contracts let you list contingency as a separate line item. This shows the client you're a professional who plans for real-world problems, not someone who just hopes for the best.

Assembling a Bid Package That Stands Out

You’ve spent hours on the takeoff, sharpened your pencil on the estimate, and found the perfect price. Now for the final step: putting it all together. Your final bid is much more than just a number; it’s your sales pitch on paper. A messy, confusing proposal can make even the best price look risky to a client.

Think about it from their point of view. They might be looking at five different bids. If yours is hard to read, missing papers, or looks like it was thrown together in five minutes, what does that say about how you'll handle their project? A professional-looking bid shows you’re a professional contractor.

More Than Just a Price Tag

A winning bid tells the whole story. It shows the client that you don't just understand the numbers; you understand their project. Your bid package should be a complete folder that answers their questions before they even ask them. This is your chance to stand out.

Here’s what a great package should always have:

- A Detailed Scope of Work: Don't just write "office renovation." Clearly explain what is included and, just as importantly, what is not included. This prevents arguments later.

- A Proposed Schedule: Give them a realistic timeline with key dates. This shows you’ve thought about how to get the job done on time.

- Proof of Qualifications: Include your license, insurance, and bonding information. These papers are must-haves and build trust right away.

- Company Information: Briefly introduce your company. Who are you? What do you do best? A simple one-page summary can help a lot.

Including things that show you care about safety—like a good workplace safety policy template that wins tenders—can really set you apart. It's these details that show you're a serious professional.

Tailor Your Proposal to the Client

Every client is different. Some only care about the lowest price. Others care more about how fast you can finish. And some want the highest quality no matter what. Your bid should speak directly to what they care about most.

How do you know what that is? You listen. Pay close attention during the pre-bid meeting. What questions are they asking? What parts of the project do they seem most worried about?

Showing you understand what a client really wants is powerful. It proves you did more than just run the numbers; it proves you were actually listening to them.

For example, if the client keeps mentioning a hard deadline for a grand opening, your proposal should focus on your schedule and your history of finishing on time. If they talk about having quality problems on past projects, you should talk about your quality control process and maybe include a good review or two.

Your Final Review Checklist

Before you hit "send" or drop off that envelope, do one last check. Mistakes happen, but a simple typo or a missing paper can get your whole bid thrown out. A final check is the easiest way to protect all your hard work.

Use this checklist as a final check:

- Have you signed everything? Make sure all signature lines are signed.

- Are all papers included? Double-check the bid request for things like insurance certificates.

- Is the math right? Look over your final numbers one last time.

- Is the client's name spelled right? It’s a small detail that shows you care.

- Is the bid on time? Late is the same as never. Check the deadline and how they want it delivered.

This final five-minute review is the cheapest insurance you can buy for your bid. It catches small mistakes and makes sure your professional package looks exactly that—professional.

Learning from Every Bid, Win or Lose

The work isn’t over just because you sent the bid. What you do after the bid is sent can be just as important as all the prep work you did before.

Whether you get the job or not, every single bid is a chance to get smarter. This knowledge is what separates the contractors that last for decades from the ones that don't.

Think of each bid as a lesson. If you just shrug your shoulders when you lose and move on to the next one, you're throwing away a free education. You spent hours on that proposal; you owe it to yourself to learn something from that time, even if you don't get the contract.

What to Do When You Lose a Bid

Losing hurts. There's no doubt about it. But it's also your best chance to get some honest feedback.

Once you know they've made a decision, wait a day or two and then follow up with the owner or general contractor. Your goal isn't to argue or try to change their mind. You have one goal: to learn.

Keep the conversation short and respectful. A simple phone call or a short email asking for feedback can be very helpful.

Here are a few questions you could ask:

- "Could you share any feedback on what was good about our proposal and where we could improve?"

- "Was the decision mostly about price, or were other things like our timeline more important?"

- "Is there anything we could do to make our proposals better for future jobs with you?"

Most people are willing to give you a few tips. Maybe your price was 5% higher than the winner's. Or maybe they thought your schedule was too tight. This feedback is pure gold. It tells you exactly how people see your pricing and presentation, helping you get better for the next time.

Don't ever take a lost bid personally. See it as market research. The client is giving you a free, honest review of your company. Listen carefully, say thank you, and use that information to get smarter.

What to Do When You Win a Bid

Winning feels great, but now the real work starts. That winning bid isn't just a paper anymore—it’s now the budget for your project. This is where your financial discipline is really tested.

All those numbers you carefully figured out now have to survive the real world of a job site.

The key is to use job costing to track every dollar you spend against your original estimate. This means keeping a close eye on your actual costs for labor, materials, and subcontractors for the entire project.

This process creates a powerful learning loop. You're always comparing your estimated costs to your actual costs. Did you budget 100 hours for framing, but it really took 120? That's important information. Maybe your labor rate was too low, or maybe problems on site caused delays. Tracking these details is the only way to make your estimates better over time.

For a deeper look, check out our guide on how a company's financial statements can reveal its operational health.

This cycle—bidding, tracking your costs, and then reviewing the results—is what makes a construction company truly successful. You’re not just guessing anymore. You’re building a library of your own data that makes every future bid more accurate and more profitable than the last. You learn what types of jobs you’re best at and which ones make you less money.

This is how you stop just bidding on jobs and start building a smarter, stronger business.

At MyOfficeOps, we help contractors turn their financial data into their most powerful bidding tool. From setting up precise job costing to providing CFO-level insights, we give you the financial clarity you need to bid with confidence and win more profitable work. Get in touch to see how we can help you build a stronger bottom line.