You're probably in that frustrating middle ground right now. The business is moving. Clients are paying. Payroll goes out. You're working hard enough that friends assume you must be doing great. But when you sit down and ask, “Is this business really giving me a strong return on the money I've put into it?” the answer gets fuzzy fast.

That's a common owner problem. You can be busy, even profitable, and still not be using your money well. A full calendar doesn't prove the business is building wealth. A decent bank balance doesn't prove your investment is earning what it should.

That's where return on equity matters. It helps answer a blunt question. Is your business just keeping you occupied, or is it doing a good job turning owner money into profit?

Are You Working Hard or Is Your Money Working Hard

Let's use a simple example.

A business owner in West Chester runs a growing service company. The phone rings. The team is slammed. Revenue is up. She finally stopped worrying about whether there's enough cash to make payroll. From the outside, it looks like a win.

But then she asks a smarter question. “I put years of savings into this thing. I left a stable job. I've kept profits in the business instead of taking them home. Is that money pulling its weight?”

That's the question most owners avoid because they don't know where to look.

They watch sales. They watch the checking account. They watch tax bills with dread. Those matter, but none of them tell the full story of how hard your invested money is working. Return on equity does.

Think of it as the owner's scorecard. It tells you whether the money tied up in the business is generating a return that makes sense for the risk, time, and stress you're carrying. If you want a broader comparison between business returns and other uses of capital, this guide to calculating return on investment helps connect the dots.

Practical rule: If your business depends on your money, your time, and your personal risk, you need a clear way to judge whether that investment is paying off.

A lot of owners confuse movement with progress. Hiring people, buying software, adding space, or landing more work can feel like growth. Sometimes it is. Sometimes it's just a more expensive version of the same business.

Return on equity cuts through that noise. It asks one clean question. For every dollar the owners have left in the business, how much profit is the company producing?

That's why I like this metric. It doesn't care about your hustle story. It cares about results.

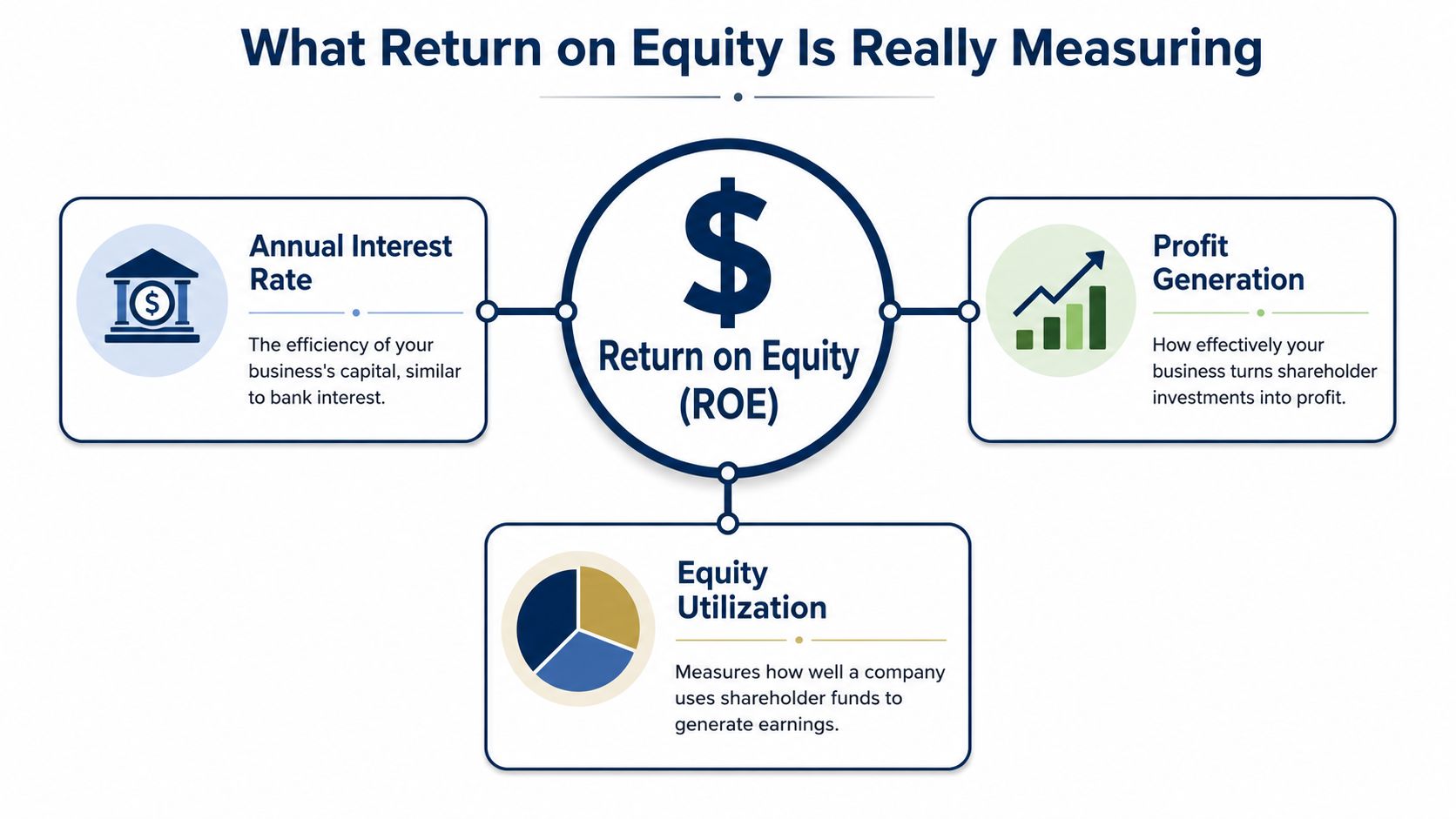

What Return on Equity Is Really Measuring

Textbook definitions tend to make this harder than it needs to be. Here's the plain-English version.

Return on equity measures how well your business turns the owners' stake into profit. If your business were a savings account, return on equity would be the interest rate your money earned for being parked there.

That's the main point. Not activity. Not vanity. Return.

The formula in normal language

The formula is simple:

ROE = Net Income / Shareholder's Equity

That's it. Two numbers.

- Net income is the profit left after you've paid expenses. Rent, payroll, software, insurance, taxes, interest, all of it. This is the bottom-line number on your profit and loss statement.

- Shareholder's equity is the owners' value in the business. In plain terms, it's what the business owns minus what it owes. If you need a refresher on where that lives, this balance sheet reading guide is worth your time.

If that sounds abstract, use this mental picture. Equity is the pile of owner money and retained profits sitting in the business. Net income is what that pile produced.

Why this number matters more than most owners think

A lot of small business owners look at profit and stop there. That's a mistake.

Profit alone doesn't tell you whether the business is efficient with owner capital. Two companies can both make money, but one may need far less owner investment to do it. That business is doing a better job with equity.

A strong return on equity usually means the business isn't just making money. It's making money without wasting the owners' capital.

This is also why return on equity matters when you make operating choices. Pricing affects profit. Hiring affects profit. Equipment purchases affect both profit and equity. Payroll structure, overhead, and debt all show up in this ratio sooner or later.

If you want another angle on how workforce structure can change profitability ratios, this guide on PEO financial impact is useful because it ties staffing decisions back to financial performance, not just HR convenience.

Think of it as a report card for your money

Here's the simplest way to remember it:

| What you're asking | What ROE tells you |

|---|---|

| “Is the business profitable?” | Not exactly. It goes deeper than that. |

| “Is my money invested well here?” | Yes. That's the real question ROE answers. |

| “Does growth mean I'm building value?” | Only if profit grows in a healthy way compared with owner equity. |

A business can feel successful and still post a weak return on equity. That usually means too much cash is trapped, margins are thin, assets are underused, or the company is carrying capital it isn't putting to work.

How to Calculate ROE for Your Business Step by Step

You don't need fancy software to calculate return on equity. You need clean books and the discipline to pull the right numbers from the right reports.

That second part matters. If your financials are messy, your ROE will be nonsense. I've seen owners make serious decisions off reports that were missing payroll adjustments, carrying old receivables, or lumping personal expenses into the business. Garbage in, garbage out.

Step one, pull your profit and loss

Let's stick with a local example. Say you run a small marketing agency in West Chester.

Open your profit and loss statement for the period you want to review. Annual is common because return on equity is easiest to understand over a full year. Go straight to the bottom line. You're looking for net income. If you want a quick refresher on the layout, this income statement reading guide shows where that number sits and what feeds into it.

Don't grab gross profit. Don't grab operating income unless that's the version you intentionally use for internal analysis. For a basic ROE calculation, use net income.

Step two, pull your balance sheet

Now open your balance sheet for the same date or period end.

You want total shareholder's equity or owner's equity, depending on how your accounting system labels it. This section usually includes owner contributions, retained earnings, and current-year earnings rolled into equity.

This number is not your bank balance. It's not the value of one asset. It's the ownership stake left after liabilities are taken out.

Step three, plug the numbers into the formula

Take net income and divide it by shareholder's equity.

That gives you your return on equity.

Here's the process in simple form:

- Run the profit and loss for the year.

- Find net income at the bottom.

- Run the balance sheet for the same period end.

- Find owner's or shareholder's equity in the equity section.

- Divide net income by equity to get ROE.

If you use QuickBooks Online, Xero, or another accounting platform, those reports are already there. The challenge usually isn't access. It's accuracy.

Reality check: If you haven't reconciled accounts, cleaned up payroll entries, and reviewed expenses, don't trust the ratio.

Step four, sanity-check the result

Before you celebrate or panic, ask a few basic questions.

- Was the year unusual? A one-time lawsuit, equipment sale, owner bonus, or cleanup entry can distort net income.

- Was equity unusually low or high? Large owner distributions or new capital injections can make the denominator jump around.

- Are your books current? Late bookkeeping turns ROE into old news.

This is why I tell owners not to treat return on equity like a one-and-done math problem. It's a management tool. You calculate it, then you ask why it looks the way it does.

Clean books are not optional

If your reports are sloppy, every conclusion after that is shaky. You might think pricing is the problem when the actual issue is job costing. You might think labor is too high when the books are classifying contractor payments incorrectly. You might think equity is strong when old liabilities haven't been recorded.

A clean monthly close matters because ROE sits on top of two reports that must be right: the profit and loss statement and the balance sheet.

That's why bookkeeping isn't back-office busywork. It's the foundation for good decisions.

Is Your ROE Good Bad or Just Average

Once you have your return on equity, the next question is obvious. Is it good?

The honest answer is that context matters more than the raw number. A service firm with low equipment needs usually looks different from a contractor that owns trucks, tools, and machines. A medical practice has a different cost structure from a marketing agency. Comparing them without context is a fast way to fool yourself.

Start with common-sense benchmarks

Many owners want a simple pass-or-fail line. I get it. But you're better off using rough context, not chasing one magic target.

In general, owners and investors usually want to see return on equity that shows the business is producing healthy profit from owner capital. Higher is better, but only if the number comes from a sound business and not from financial gymnastics.

To put it into practical terms:

| Industry | Typical ROE Range |

|---|---|

| Professional services | Often moderate to strong, especially when overhead stays lean |

| Healthcare practices | Often stable, but influenced heavily by staffing and reimbursement mix |

| Construction | Often more uneven because equipment, project timing, and debt can distort results |

That table is intentionally broad because industry, size, age of business, and capital needs change the picture fast. A mature law firm won't behave like a growing HVAC company. A solo consultant won't behave like a clinic with heavy payroll.

Compare against your own history first

The best first comparison is usually your own business over time.

If return on equity is improving year after year, that tells me management decisions are likely moving in the right direction. If it's flat while revenue rises, something is off. Maybe margin is slipping. Maybe you've tied up too much money in assets. Maybe cash is sitting idle.

A year-over-year trend can tell you more than a one-time benchmark chart.

Don't obsess over whether your ROE beats some generic standard. Ask whether your business is becoming more efficient with owner capital.

High ROE can hide a problem

Here's the part many owners miss. A very high return on equity is not always a victory lap.

Debt can inflate ROE. When a business borrows more, it can reduce the amount of equity needed to support operations. That can make the denominator smaller and the ratio look better, even if the underlying business hasn't become stronger.

Let's make that simple. If you buy equipment with a loan instead of owner cash, equity may stay lower than it otherwise would. If profits hold up, ROE can rise. On paper, that looks efficient. In real life, it may also mean more monthly pressure, more lender risk, and less room for error.

Watch for these warning signs

A strong-looking ROE deserves a second look if you also see:

- Heavy debt payments: The ratio may be relying on high debt rather than operating strength.

- Thin cash reserves: Good ROE won't save you if one bad month creates a cash crunch.

- Low owner equity: Past losses or aggressive distributions can make ROE look better than the business really is.

- Profit swings: One strong year doesn't prove the business model is solid.

That's why I never judge return on equity in isolation. Pair it with cash flow, debt levels, and profit trends. A healthy business earns solid returns without living on the edge.

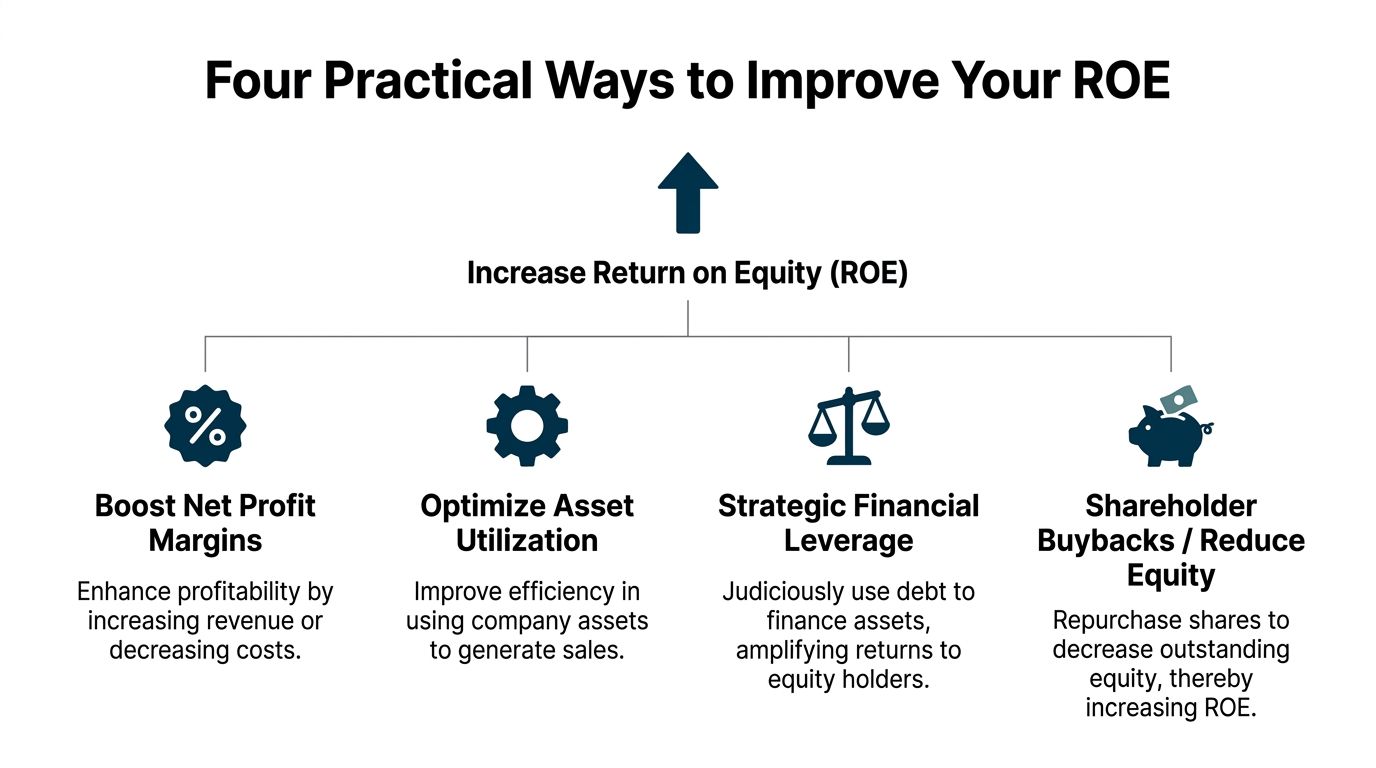

Four Practical Ways to Improve Your ROE

If return on equity is weak, don't jump straight to cutting staff or taking on debt. Start with the levers that effectively move the formula in a healthy way.

You improve ROE by increasing profit, using assets better, managing capital more tightly, and being smart about financing. Those are CFO decisions, but they show up in everyday choices like pricing a job, approving a hire, or replacing a machine.

Raise profit without fooling yourself

The cleanest way to improve return on equity is to raise net income.

That doesn't mean slashing costs blindly. It means finding the places where profit leaks out of the business every month and fixing them. A lot of owners underprice legacy clients, keep unprofitable service packages, or tolerate bloated software stacks because each monthly charge feels small.

Try this instead:

- Review pricing line by line: If you haven't raised prices in a while, odds are good you're training customers to expect more while your labor and vendor costs climb.

- Cut low-value spend: Open your expense detail and look at every recurring charge. If a tool isn't helping sales, delivery, or reporting, question it.

- Drop weak work: Some revenue is expensive revenue. If a service line causes rework, custom scope creep, or constant support headaches, it may be lowering ROE even while boosting top-line sales.

A small price increase on your best work often improves return on equity faster than chasing a pile of mediocre new clients.

Owner move: Before your next invoice cycle, identify one service that customers value and test a cleaner, firmer price.

Get more from the assets you already own

The next lever is asset use. If money is tied up in things that don't produce enough revenue or profit, return on equity suffers.

This shows up differently by business type. In construction, it might be equipment that sits too often. In healthcare, it could be underused provider schedules or too much front-desk overhead for current patient volume. In a professional services firm, it may be labor capacity that isn't being billed efficiently.

Look for these friction points:

- Idle equipment: Sell what you rarely use, rent when it makes more sense, or schedule jobs to increase utilization.

- Slow inventory: If products sit too long, cash gets trapped on shelves instead of supporting profit.

- Underbooked labor: A salaried employee with too much downtime is an expensive asset problem, not just a staffing issue.

If you run a medical practice, this strategies to increase practice profits article is useful because it focuses on operational choices that affect margin and resource use, which is exactly what pushes return on equity up or down.

Stop letting cash sit around doing nothing

Owners love having cash in the bank. I do too. But there's a difference between healthy reserves and lazy capital.

If your business is carrying more idle cash than it needs for operations, taxes, and a reasonable cushion, that money may be dragging on return on equity. It's owner capital sitting still.

That doesn't mean drain the account. It means be intentional.

Consider a few questions:

| Decision area | What to ask |

|---|---|

| Cash reserves | Do you have a true target, or are you just accumulating money with no plan? |

| Receivables | Are clients taking too long to pay because your billing process is weak? |

| Payables | Are you paying vendors faster than required while customers pay you late? |

Sometimes the answer is tightening invoicing. Sometimes it's collecting deposits sooner. Sometimes it's moving excess cash into growth uses that produce a better return, like a profitable hire, better equipment, or targeted business development.

Use debt carefully, not casually

Debt can help ROE. It can also wreck a good business.

The key is using financing where the borrowed money supports productive growth and where the payment terms fit your cash flow. Borrowing for equipment that increases capacity can be smart. Borrowing to patch losses month after month is a warning sign.

I'm opinionated on this. Small business owners often take on debt too emotionally. They either avoid it completely because they hate owing money, or they grab it too fast because a lender says yes.

A better approach looks like this:

- Match financing to purpose: Long-term assets deserve structured financing. Short-term working capital problems need operational fixes first.

- Stress-test the payment: If one slow month makes the loan feel scary, the debt load may already be too high.

- Protect flexibility: Leave yourself room to handle delays, bad quarters, or surprise repairs.

Good leverage supports a solid business. Bad leverage props up a weak one and makes the weakness more dangerous.

One more lever owners forget

There's also a technical way to improve ROE by reducing equity itself. In larger companies, that can happen through share buybacks. In small businesses, the rough equivalent is changing how much capital stays trapped in the company versus how much is distributed.

Be careful here. Pulling too much equity out can make the ratio look better while making the business more fragile. If you weaken the balance sheet just to dress up ROE, you're playing games.

The goal isn't a prettier formula. The goal is a stronger business that earns more from the capital it needs.

From Measurement to Mastery with a Financial Partner

Once you start looking at return on equity the right way, it stops being a finance term and becomes a management habit.

You use it when you decide whether to raise prices. You use it when you think about a hire. You use it before buying equipment, taking on debt, or leaving a pile of cash untouched because it feels safe. It gives you a better way to ask, “Will this decision help my money work harder?”

That's where a lot of owners get stuck. Not because the idea is too complex, but because the data is messy and the week is already full. If your books are behind, your reports are confusing, and no one is translating numbers into decisions, return on equity stays theoretical.

What mastery actually looks like

Mastery doesn't mean building some giant finance department.

It means you have a clean close every month, a reliable profit and loss, a trustworthy balance sheet, and someone who can say, “Your ROE is moving because labor is up, pricing is flat, and too much cash is tied up in slow-paying accounts.”

That's useful. That changes behavior.

The real win for owners

The biggest payoff isn't the ratio itself. It's the discipline that comes with tracking it.

You stop making gut-only decisions. You stop confusing revenue with value. You stop assuming hard work automatically creates wealth. Instead, you build a business that earns more from the capital already inside it.

And that's what most owners want, even if they don't say it that way. They want a business that works hard for them, not one that constantly asks for more money, more hours, and more patience.

If you want help turning return on equity from a spreadsheet exercise into a real operating tool, MyOfficeOps can help you get there. They clean up the books, give you clear financial reports, and provide CFO-level guidance on pricing, hiring, cash flow, and profitability so you can make smarter decisions with confidence.