So, what is full charge bookkeeping? It’s when one person handles all of your company's financial records from start to finish. Think of them as the manager of your business's money, keeping track of everything from daily sales to creating the big-picture reports that show you how you’re doing.

The Person in Charge of Your Company's Money

Imagine your business's money is an orchestra. You have money coming in (sales), money going out (bills), payroll, and bank accounts. A regular bookkeeper might just handle one part, like entering the sales.

A full charge bookkeeper is like the conductor of the whole orchestra. They don't just play one instrument; they make sure every part works together. They ensure the final sound—your company’s financial health—is clear and correct.

More Than Just Entering Numbers

This job is much more than typing numbers into a computer. A full charge bookkeeper takes full ownership of your company's books. They manage the entire accounting cycle, which is the 8-step process of recording and checking every transaction your company makes. You can learn more about this in our guide to small business bookkeeping basics.

Their job is to make sure the financial story your books tell is complete and true. This includes tasks like:

- Handling Daily Money: Managing bills you need to pay (accounts payable) and money customers owe you (accounts receivable).

- Running Payroll: Making sure your team gets paid the right amount, on time.

- Checking Bank Accounts: Matching your company records to your bank statements to catch any mistakes.

- Creating Financial Reports: Making the key reports, like the profit and loss statement, that show you how your business is really doing.

A full charge bookkeeper is in charge of your main financial record (the general ledger) and gets it ready for review. They are the one person responsible for your company’s financial records, giving you a complete picture without needing a big accounting team.

This role is super common in small to medium-sized businesses. These companies need someone to watch their finances closely but aren't big enough yet to hire a full-time financial controller or CFO. When it's time for an accountant to do your taxes, the full charge bookkeeper gives them a clean, organized set of books. This saves everyone time and saves you money.

A Look Into a Full Charge Bookkeeper's Typical Week

So, what does a full charge bookkeeper really do all week? It’s not just sitting in a corner crunching numbers. Their work is a steady cycle of managing your company's money—past, present, and future.

Let's pretend you run a local coffee shop. On Monday, your bookkeeper starts by checking all the sales from the weekend. They'll sort payments for coffee beans from suppliers, milk deliveries, and all the credit card sales from customers. This isn't just data entry; it's giving every dollar a job.

By the middle of the week, they focus on money that’s moving. They’ll handle accounts payable (paying your suppliers for those coffee beans) and accounts receivable (sending invoices to a local office you supply coffee to and following up if they are late). This keeps cash coming in and your vendors happy.

Keeping the Financial Engine Running Smoothly

Later in the week, the focus is on checking and preparing. This is when they do bank reconciliations—which is just a fancy way of saying they match your company's books to the bank's records. It's like balancing your own checkbook, but for the whole business. It's a must-do step to catch errors, spot weird charges, and make sure your financial picture is accurate.

If it's a payroll week, they'll also be busy making sure every barista is paid correctly. This means calculating hours, taking out the right taxes, and following all the payroll rules. It's a detailed job with no room for mistakes.

Toward the end of the week, it all comes together in reports. Using the information they've organized, they prepare key financial statements. These aren't just papers to file away; they are your business's report card.

The real value of a full charge bookkeeper isn't just recording what happened. It's showing you that information in a way that helps you make smarter decisions.

From Daily Tasks to Smart Decisions

For our coffee shop, this means creating reports that show which drinks are the most profitable. Is it the morning lattes or the afternoon cold brew? The bookkeeper’s reports give you the answer.

This level of responsibility is why the job requires a lot of experience. Managing a whole accounting system is complex, which is why employers usually look for someone with at least five to seven years of experience. Their job includes tasks that are often split between a few people, from paying bills to getting financial statements ready for tax time. You can discover more insights about these experience requirements and what they mean for your business.

By Friday, the bookkeeper has brought order to the week's finances. They've paid bills, collected money, checked accounts, and created a clear summary of how the business is doing. This complete cycle of tasks is what makes full charge bookkeeping so important for any growing business.

Bookkeeper vs. Accountant vs. CPA: What Is the Difference?

It’s easy to mix up these job titles, but they each have very different roles in helping your company succeed. Getting them confused can mean you hire the wrong person for what you need.

Think of it like building a house. You need a crew, and each person has a specific job.

Your full charge bookkeeper is the builder on-site every day. They are the ones doing the hands-on work—laying the foundation and putting up the walls. They handle the daily job of building your financial records, making sure every transaction is recorded correctly.

The accountant is like the architect. They take the solid structure the bookkeeper built and use it to draw up plans for the future. An accountant looks at the big picture, helping you create budgets and plan for growth. They analyze the bookkeeper's work to give you advice.

Who Does What?

This is where the jobs really split. A bookkeeper mainly deals with the past and present—carefully recording what has already happened. An accountant focuses on the future, using that information to help you plan your next move. The role of EOFY Accountants shows this difference, as they focus on year-end analysis and strategy.

Finally, the Certified Public Accountant (CPA) is like the building inspector. A CPA has passed a tough state exam and has the legal power to handle complex tax issues and audits. They check the work of both the builder (bookkeeper) and the architect (accountant) to make sure everything is up to code. They are the ones who sign your tax returns and can legally represent you to the IRS.

While a bookkeeper can get your books "tax-ready," only a CPA can give official tax advice and defend your tax filings. They make sure your business follows all tax laws.

To make it even clearer, here’s a simple table breaking down their jobs.

Bookkeeper vs Accountant vs CPA Role Comparison

This table gives a simple look at what each financial professional does.

| Role | Primary Focus | Key Activities |

|---|---|---|

| Full Charge Bookkeeper | Recording & Organizing | Manages daily transactions, bills, invoices, payroll, and creates financial reports. |

| Accountant | Analyzing & Planning | Looks at financial data, creates budgets, analyzes costs, and provides financial advice. |

| CPA | Compliance & Strategy | Prepares and files complex tax returns, performs audits, and offers high-level tax strategy. |

Understanding these differences is key. You need a bookkeeper for day-to-day money management, an accountant for planning, and a CPA for taxes and compliance. Knowing who to call for what job will save you a lot of time and money.

Signs Your Business Is Ready for a Full Charge Bookkeeper

Figuring out when to get more help with your books can be tough. You probably started by doing it all yourself with a spreadsheet. But as your business grows, the financial side can turn from a small chore into a big headache.

How do you know you’ve reached that point? It’s usually a bunch of small problems that show you've outgrown your current system. If any of these sound familiar, it might be time for a pro.

You Spend More Time on Books Than on Customers

This is the most common sign. Look at your work week. Are you spending hours fighting with QuickBooks, sorting expenses, or chasing payments instead of serving your customers?

Your time is your most valuable resource. If bookkeeping is pulling you away from the work that makes you money, you’re losing out. A full charge bookkeeper takes that entire task off your plate, freeing you up to focus on growing your business.

You Have No Idea What Your Real Profit Margin Is

You just finished a big job, and the payment is in your bank account. It feels good, but was it really profitable? If you can’t answer that question for weeks—or at all—your financial information isn’t helping you.

A full charge bookkeeper gives you that clarity. They don’t just record numbers; they set up your books to track how profitable each job is. This means you can see exactly which services make you the most money, allowing you to make smarter decisions.

The goal isn't just to have numbers; it's to have numbers that tell you a story. A full charge bookkeeper helps you read that story so you can write a better next chapter for your business.

You Are Preparing for Growth or a Loan

Are you thinking about hiring employees, opening another location, or applying for a business loan? These big steps require clean, professional financial records. Banks and investors will want to see detailed financial statements.

A full charge bookkeeper makes sure your books are always accurate, organized, and ready for review. They prepare the exact documents that banks need, making the loan process smoother and increasing your chances of getting approved. For more tips on hiring, check out our guide on how to find a bookkeeper for your business. Their work provides the solid financial base you need to grow.

Hiring In House vs Outsourcing Your Bookkeeping

Okay, so you realize you need a full charge bookkeeper. Great! Now for the next big question: do you hire someone as an employee, or do you partner with an outside company?

This is a big decision with no single right answer. It depends on your business needs, your budget, and how you like to work. Let's look at the pros and cons of each choice.

The In-House Option: The Pros and Cons

Hiring an in-house bookkeeper means adding a new person to your team. They’ll work in your office (or remotely for you) and be part of your daily routine. The biggest benefit is having someone 100% focused on your business. They’re always right there when you need them.

But hiring an employee costs more than just their salary. You also have to pay for:

- Benefits: Health insurance, retirement plans, and paid time off.

- Payroll Taxes: You have to pay your share of Social Security and Medicare taxes.

- Overhead: A desk, a computer, software, and other office supplies.

- Training: You'll need to pay for them to keep their skills up to date.

When you add it all up, the real cost of an employee can be much higher than their paycheck.

The Outsourcing Option: A Different Approach

Outsourcing your bookkeeping means you hire a firm—like MyOfficeOps—to do the work of a full charge bookkeeper. Instead of one person, you get a whole team of experts for a set monthly fee.

The biggest advantage here is saving money. You get expert help without the extra costs of an employee. You don't have to worry about benefits, payroll taxes, or buying more equipment. Plus, outsourced services are flexible. If your business has a slow month, you aren’t stuck paying a full-time salary. As you grow, your service can grow with you. You can learn more about how this works in our guide to outsourced bookkeeping for small business.

For many small and mid-sized businesses, outsourcing gives you expert financial help for less than the cost of hiring one full-time person.

A Look at the Real Numbers

Let's talk about cost, because that's often the deciding factor. A full charge bookkeeper is a skilled professional, and their pay shows it. The average hourly rate is around $25.46, which adds up.

A yearly salary is often between $63,000 to $82,500. And that’s before adding the cost of benefits and taxes, which can add another 20-30% to the total cost.

Outsourcing, on the other hand, gives you that same level of expertise for a flat monthly fee. For many businesses, this means big savings every year. If you're looking at your options, this guide on how to hire a bookkeeper can offer more help.

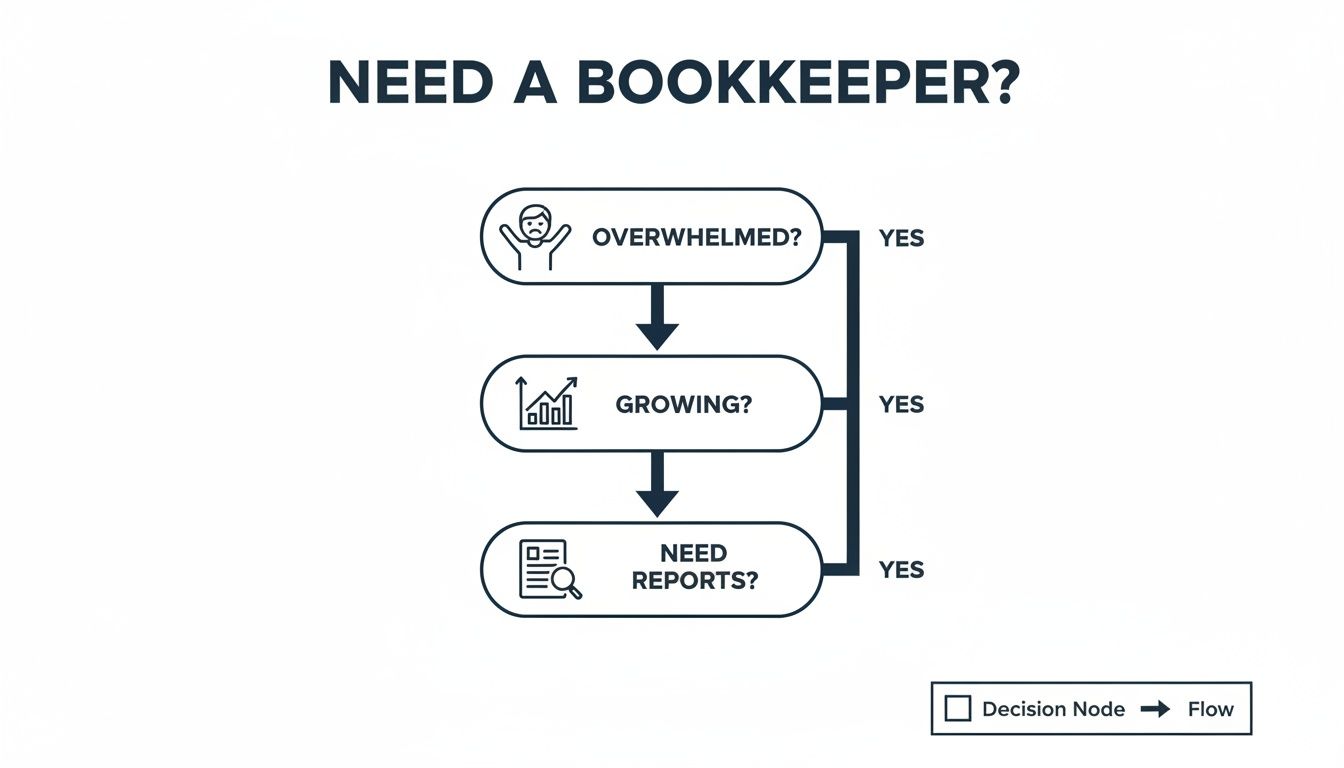

This decision tree can help you see which path might be better if you're starting to feel buried in paperwork.

As the chart shows, if you're feeling overwhelmed, your business is growing, and you need clear reports to make decisions, getting professional help is the next smart step.

Ultimately, whether you hire someone or outsource, the goal is the same: to get the financial clarity you need to run your business with confidence.

Common Questions About Full Charge Bookkeeping

As you think about whether full charge bookkeeping is right for you, a few questions usually pop up. Let's go over the most common ones we hear from business owners.

What Software Should a Good Full Charge Bookkeeper Know?

A great full charge bookkeeper should be an expert with accounting software like QuickBooks Online or Xero. They should also be good with spreadsheets like Microsoft Excel to analyze numbers and create custom reports.

But it doesn't stop there. If you're in a specific industry, like construction, you'll want someone who knows job costing software. A good firm will be comfortable with many different programs, so they can use the tools you already have.

Can a Full Charge Bookkeeper Do My Taxes?

That's a good question. The answer is sometimes. Many experienced bookkeepers can prepare tax returns, and a big part of their job is getting your books "tax-ready."

However, they are not Certified Public Accountants (CPAs). CPAs are licensed to give tax advice and can legally represent you to the IRS. The best setup we see is when a full charge bookkeeper handles your finances all year, then works with a CPA for tax strategy and filing.

How Much Does It Cost to Outsource Full Charge Bookkeeping?

The cost depends on how complex your business is—things like how many transactions you have each month and how many bank accounts you use. Outsourced services offer different price plans to fit businesses of all sizes.

For freelance and outsourced services, you’ll often find different pricing tiers. A solo business owner might pay $150–$300 a month for basic help, while a growing business could pay $800–$1,500+ for a complete package that includes detailed reports and tax-ready books.

When you compare this to hiring a full-time employee—with salary, benefits, and taxes—outsourcing is often cheaper. You get an expert for a set monthly cost that can grow with your business. You can look at bookkeeper salary ranges and service costs to see how the numbers compare.

My Business Is Small. Do I Really Need One?

Even the smallest businesses benefit from this level of financial help. If you're doing the books yourself, think about how many hours that takes you away from serving your clients or growing your business.

A full charge bookkeeper does more than just enter data. They give you the financial clarity you need to make smart decisions about pricing, hiring, and managing your money. Getting a professional involved early builds a strong financial foundation, setting you up for healthy growth. It’s an investment in your company's future.

Ready to gain the financial clarity you need to grow your business with confidence? The team at MyOfficeOps provides expert, full charge bookkeeping and advisory services for businesses in the Philadelphia and West Chester area. Schedule your free discovery call today.