Working capital management sounds like a fancy term, but it’s really just about making sure your business has enough cash on hand to pay its bills. Think of it as the daily balancing act between the money you have coming in and the money you have going out.

It's like managing your business's piggy bank to make sure it's never empty when you need it.

Understanding Your Daily Cash Flow Game

Let's skip the complicated stuff. Imagine your business is a bucket. The water coming in is the cash you get from customers. The water going out is the money you spend on things like payroll, supplies, and rent. Working capital management is just making sure there's always enough water in that bucket. You don't want it to run dry, but you also don't want so much water sitting there that it's not being used for anything.

This isn’t just for accountants; it’s a vital, everyday job for any business owner. I've seen profitable companies go out of business simply because they ran out of cash to pay their team on Friday. It's a common and painful trap.

The Two Sides of the Coin

At its heart, managing working capital is about looking at two things: what you own that can quickly become cash, and what you have to pay soon. Keeping these in balance is the whole point. It helps you answer questions like:

- Can we afford to buy that new piece of equipment?

- Do we have enough money to get through a slow month?

- Should we pay our supplier early to get a discount?

Good management gives you the confidence to make these decisions. It turns confusing financial reports into a simple tool to help you grow.

The goal isn't just to scrape by each month. It's about building a strong business that can handle surprises and grab opportunities without constantly worrying about cash.

To make it super clear, let's break down the two main parts of working capital.

Working Capital At a Glance

This table makes the two main parts of working capital easy to understand.

| Component | What It Means in Plain English | Real-World Examples |

|---|---|---|

| Current Assets | Stuff you own that you can turn into cash within a year. | Cash in the bank, customer invoices you're waiting on, and products or materials you have in stock. |

| Current Liabilities | The bills you have to pay within a year. | Money you owe suppliers, your next payroll, short-term loan payments, and your rent. |

Working capital is just the difference between these two. It's the money you have left to run the business after you've set aside what you need to pay your immediate bills.

The Two Sides of Your Working Capital

To really get how working capital management works, you need to understand its two basic pieces. Think of it like a seesaw. On one side is everything your business owns that can quickly be turned into cash. On the other side is everything your business owes in the near future.

Keeping this seesaw balanced is the key. This isn't just numbers on a page—it's the real story of your business's health today.

What You Own (Current Assets)

Current assets are all the things your company owns that you expect to turn into cash within the next year. It’s the stuff that keeps your business going.

Here’s what that usually includes:

- Cash: This one's easy—it's the money sitting in your bank account.

- Accounts Receivable: This is the money your customers owe you for work you've already done. Getting this money collected quickly is a big deal for cash flow. You can learn how to measure this with the accounts receivable turnover ratio.

- Inventory: This is any raw materials, unfinished work, or finished products you have on hand, ready to sell.

Think of current assets as the fuel in your tank for the short term.

What You Owe (Current Liabilities)

On the other side of the seesaw, you have current liabilities. These are all the bills and debts your business has to pay off within the next year.

This side includes things like:

- Accounts Payable: The money you owe to your suppliers and vendors.

- Short-Term Loans: Any loan payments that are due within the next 12 months.

- Accrued Expenses: Bills you know are coming up, like your next payroll, taxes, and rent.

These are your immediate responsibilities. Now, let’s put it all together.

The simple formula is:

Current Assets – Current Liabilities = Working Capital

A positive number means you have enough to cover your upcoming bills. A negative number is a warning sign that you might have trouble paying your bills on time.

Let’s look at a local bakery. They have $10,000 in the bank, $5,000 in unpaid invoices from catering jobs, and $3,000 worth of flour and sugar. Their total current assets are $18,000.

They also owe $4,000 to their flour supplier, have a $6,000 payroll coming up, and a $1,000 rent payment due. Their total current liabilities are $11,000.

Using the formula: $18,000 (Assets) – $11,000 (Liabilities) = $7,000 (Working Capital).

This positive $7,000 shows they are in a good spot. They have a cushion to cover their bills and handle any surprises, like a broken oven, without panicking.

Why Working Capital Can Make or Break Your Business

Now that we've looked at the numbers, let’s talk about why they matter so much for your business's survival. Managing working capital isn't just about math; it's what separates a business that grows from one that stalls. I've seen it many times: a company can be making a profit but still fail because it runs out of cash.

Think of it like this: profit is your score at the end of the game, but working capital is your energy to keep playing. If you run out of energy, the game's over, no matter how many points are on the board.

From Survival to Growth

Imagine two local landscaping companies. Both do great work and are profitable.

Company A pays close attention to its working capital. They send invoices right after a job is done, follow up on payments, and don't overbuy supplies. When they get a chance to buy a used truck at a great price, they have the cash ready. They buy it, take on more jobs, and grow.

Company B is always waiting for customers to pay. Their cash is tied up in late invoices and extra mulch sitting in their yard. When the same truck is for sale, they can't afford it. They're stuck, unable to grow, while Company A gets ahead.

This is what working capital management looks like in the real world. It’s not just about paying bills; it’s about building a company that can invest in itself.

Good working capital management gives you the breathing room to think about the future, not just how you'll survive the next week.

This is a big deal for smaller businesses, which often have to wait longer to get paid. A study by PwC found that for small companies, the average time to get paid jumped from about 65 days to 75 days. That puts a huge strain on cash. The report shows that better management helps you plan better and frees up cash for growth. You can see the full study on PwC's Working Capital insights.

Building a More Valuable Business

In the end, strong working capital management does more than keep the lights on. It makes your business healthier and more valuable.

Trust me, banks and potential buyers look at these numbers very carefully. They show how well a business is run. A company that manages its cash well is seen as a safer bet and is worth more. It proves you're in control, ready for whatever comes next.

Your Business's Financial Pulse: The Cash Conversion Cycle

Okay, so you know what working capital is and why it's important. But how do you measure how well you're managing it? The best tool for this is the Cash Conversion Cycle (CCC).

It sounds complex, but it's really just a stopwatch for your money.

The CCC measures how long it takes for a dollar you spend on supplies to make its way through your business and come back to you as cash from a sale. It’s like your business's pulse—a shorter cycle is healthier. A long cycle means your cash is tied up for too long, which can be stressful.

To figure out your CCC, you just need to look at three things.

The Three Levers of Your Cash Flow

Each part of the cycle tells you something different about where your money is and for how long.

Days Sales Outstanding (DSO): This is how long it takes, on average, for customers to pay you after you send them a bill. If you're a plumber and it takes people 45 days to pay your invoices, your DSO is 45. You want this number to be as low as possible.

Days Inventory Outstanding (DIO): This measures how long your stuff sits on the shelf before you sell it. If you're a service business, think of this as your "unbilled work." For a web designer, it's the time from starting a project until you can send the invoice. A lower DIO is better because it means you're turning your work into cash faster.

Days Payables Outstanding (DPO): This is how long you take to pay your own suppliers. If a supplier gives you 30 days to pay, and you pay them on day 29, you're managing your DPO well. You generally want this number to be higher (without being late, of course) because it means you get to hold onto your cash longer.

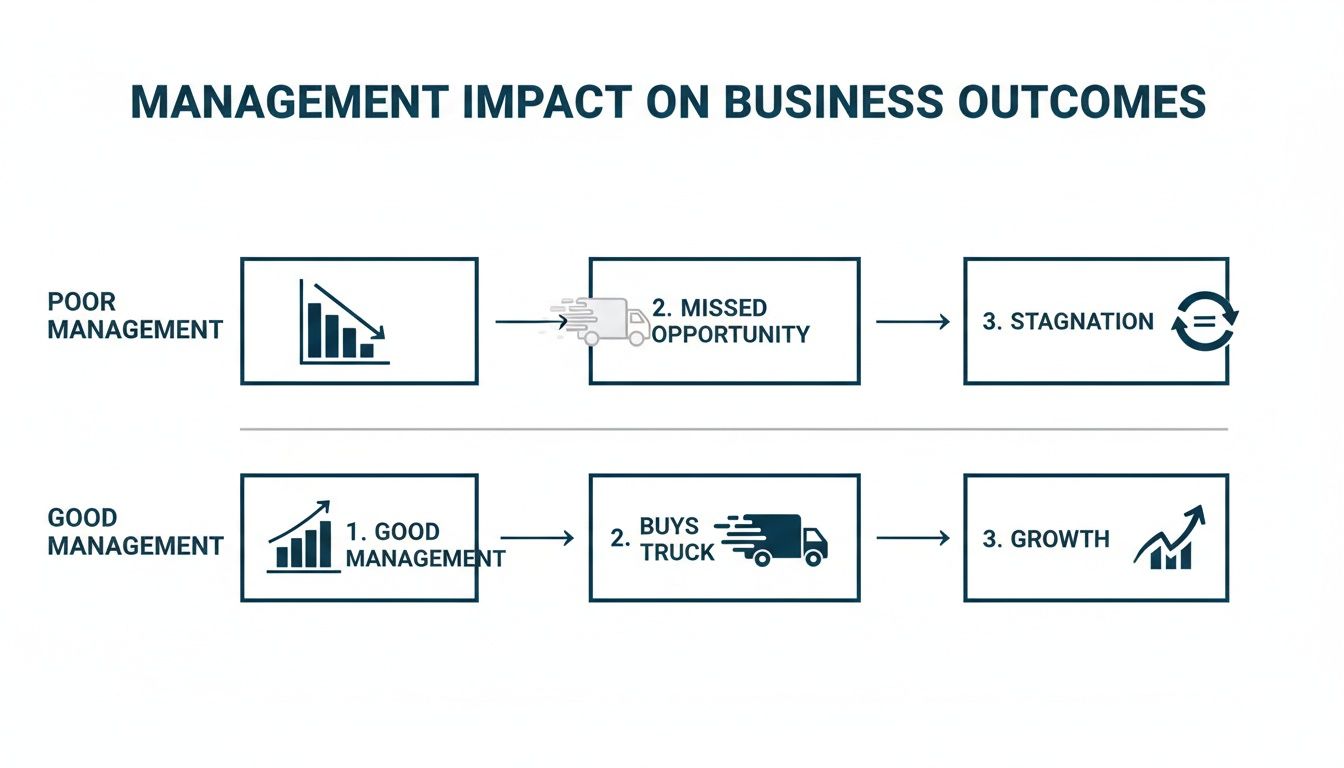

This picture shows how managing these things well—or poorly—affects your business.

As you can see, good management leads to growth, while poor management leads to getting stuck.

Why These Numbers Matter

It's easy to think of these as just numbers, but they have a huge impact. When your DSO and DIO are too long, they trap cash that your business needs to grow, hire new people, or just have a safety net.

A report from J.P. Morgan found that big companies had $707 billion in cash trapped because of these issues. For most of them, the time it took to get paid got longer, and their inventory sat around for longer too. You can read more in the J.P. Morgan working capital findings.

The formula for your Cash Conversion Cycle is:

CCC = DIO + DSO – DPO

By tracking these numbers, you can see exactly where your cash is getting stuck. Is it slow-paying customers? Or are you paying your own bills the minute they arrive? Knowing the answer helps you make better decisions.

Our cash flow forecasting template is a great tool to help you start tracking where your money is going.

Your Cash Flow Scorecard: Key Metrics Explained

Think of these three numbers as your cash flow scorecard. Understanding them is the first step to making them better. Here's a quick look at what each one tells you.

| Metric | What It Measures | What's the Goal? |

|---|---|---|

| DSO (Days Sales Outstanding) | How quickly your customers pay you. | Lower is better. You want your cash as fast as possible. |

| DIO (Days Inventory Outstanding) | How quickly you sell what you have or bill for your work. | Lower is better. Turn your stuff into cash quickly. |

| DPO (Days Payables Outstanding) | How quickly you pay your own bills. | Higher is better (but still pay on time). Hold onto your cash longer. |

Getting these three things right gives you direct control over your company's financial health. It’s the difference between worrying about payroll and feeling confident enough to invest in your next big idea.

Alright, that’s the theory. But what can you actually do today to improve your cash flow? It’s not about some huge, complicated project. It's about making small, smart changes in three key areas.

Think of it like a tune-up for your car. A few small adjustments can make your business run much more smoothly.

Get Paid Faster to Lower Your DSO

The longer your money is stuck in unpaid invoices, the less cash you have. The goal is simple: shorten the time you have to wait to get paid—your Days Sales Outstanding (DSO).

Here are a few simple ways to do that:

- Invoice Right Away: Don't wait. As soon as a job is done, send the invoice. The sooner they have it, the sooner you get paid.

- Offer a Small Discount for Paying Early: A “2/10, net 30” term is a classic. It means customers get a 2% discount if they pay within 10 days. Many will take the deal, and you get your money much faster.

- Make It Easy to Pay You: Let people pay online, with credit cards, or through bank transfers. The less work it is for them, the faster you'll get the money.

- Follow Up on Late Invoices: Have a simple process for reminders. A friendly email often does the trick. Using an accounts receivable aging report helps you see at a glance who is late, so you know who to call.

Manage Your Inventory to Reduce DIO

For many businesses, a lot of cash is just sitting on a shelf as inventory. By reducing your Days Inventory Outstanding (DIO), you free up that cash for other things.

The trick is to have what you need, right when you need it—and not too much extra. This means finding the balance between having enough supplies and not having a storeroom full of stuff that isn't selling. For example, looking into strategies to reduce labor costs and boost profit can also free up cash that might be tied up elsewhere.

A common mistake is buying in bulk just to get a discount. That discount doesn't help if the cash you spent is now stuck in inventory for six months.

Check regularly to see what's selling and what's not, and change your ordering habits.

Pay Your Bills Smarter to Manage DPO

Finally, let's look at how you pay your own bills—your Days Payables Outstanding (DPO). The goal isn't to pay late. It's to use the payment terms your vendors give you as a tool.

If a supplier gives you 30 days to pay, there's no reward for paying on day one. By paying closer to the due date, you keep cash in your bank account longer, where you can use it for other things. Even the biggest companies do this.

A recent study by The Hackett Group found that top U.S. companies freed up huge amounts of cash partly by extending their DPO by just 3%. This simple change helped them free up a piece of the $1.7 trillion in extra working capital they were holding. You can learn more about these corporate working capital survey findings.

Talk to your suppliers. Many are willing to be flexible on payment terms, especially if you're a good customer. A good relationship can give you the breathing room you need to manage your cash flow well.

Getting Help to Manage Your Working Capital

Reading about all this is one thing. Finding the time to actually track it while you're busy running your business is another story. This is where having a financial partner can make a world of difference.

Instead of staying up late with spreadsheets, a good partner sets up systems to track your numbers for you. They give you the simple, clear information you need to see what's really going on with your cash.

From Data to Decisions

But a great partner does more than just give you reports. They help you understand the numbers and make smarter choices. It's like having an expert who can spot cash flow problems months ahead of time, before they become an emergency.

This lets you focus on what you're best at—serving your customers and growing your business.

This isn't just another business expense; it's an investment in your company's health and your own peace of mind. A partner helps you stop reacting to financial surprises and start building a stronger company. That support turns managing your finances from a chore into a powerful tool for growth.

Your Top Working Capital Questions Answered

Even after you get the hang of it, a few questions always seem to come up. Let me clear up some of the most common things I hear from business owners.

Can a Profitable Business Still Go Broke?

Yes, absolutely. This is one of the biggest and most dangerous traps for a business owner. You can have a great sales month and look profitable, but if your customers take 60 or 90 days to pay you, you might not have enough cash to make payroll next week.

Profit is what you earn over time, but cash is what you can spend right now. That gap is exactly why managing working capital is something you can't afford to ignore.

What’s a “Good” Number for the Cash Conversion Cycle?

There's no single magic number. It's different for every industry. A coffee shop that gets paid instantly will have a much shorter cycle than a construction company that takes six months to build a house.

The real goal isn't to hit a specific number. It's to know what's normal for your industry and then work to make your own cycle shorter and better over time.

A shorter cycle is almost always a sign of a healthier business because your cash isn't just sitting around waiting. It's working for you.

How Often Should I Be Looking at My Working Capital?

You should check in on your working capital at least once a month. This helps you spot problems—like customers paying you more slowly—before they get out of hand.

However, if your business is growing fast or cash feels tight, checking in weekly is even better. The most important thing is to make it a regular habit, just like checking the gas gauge in your car before a long trip.

Running a business is tough enough without getting buried in financial reports. The MyOfficeOps team gives you the clear data and expert advice you need to make smart decisions about your cash, profits, and growth. Stop guessing and start knowing where your business stands. Schedule a discovery call with us today.