Accounts receivable turnover sounds like a fancy business term, but it’s actually pretty simple. It just measures how fast you collect the money your customers owe you.

Think of it like a report card for turning your invoices—all those "IOUs"—into real cash in your bank account. A higher number is usually a good sign, showing you're good at getting paid for the work you've done.

Breaking Down Accounts Receivable Turnover

Let's imagine you have a lemonade stand. Every time a friend grabs a lemonade and says, "I'll pay you back tomorrow," that promise is an "accounts receivable." It's money you've earned, but you don't have it in your pocket yet. The turnover ratio just counts how many times you successfully collect all those promises over a period of time, like a year.

This number is important because it shows how healthy your cash flow is. If you're slow to collect, you might not have the cash to buy more lemons and sugar, even if you’re selling a ton of lemonade.

What the Ratio Tells You

The accounts receivable turnover ratio shows how well your business handles the credit you give to customers. It answers the question, "How good are we at getting paid?"

For instance, let's say Flo’s Flower Shop made $100,000 in sales on credit last year. At the start of the year, customers owed her $10,000. By the end of the year, they owed her $15,000. Her turnover ratio would be 8. This means she collected her average amount of IOUs about eight times that year. This is a lot like the inventory turnover ratio, which measures how fast you sell your stuff. Both are key pieces of your financial puzzle.

Of course, to get this number right, you need to keep your records organized. This starts with a good system for tracking your money in and out. If you're not sure how, it's a good idea to learn what a chart of accounts is and how it can make your finances clearer.

The big takeaway is that this ratio isn't just a number for your accountant. It shows how much of your cash is tied up with customers instead of being in your bank account to help your business grow.

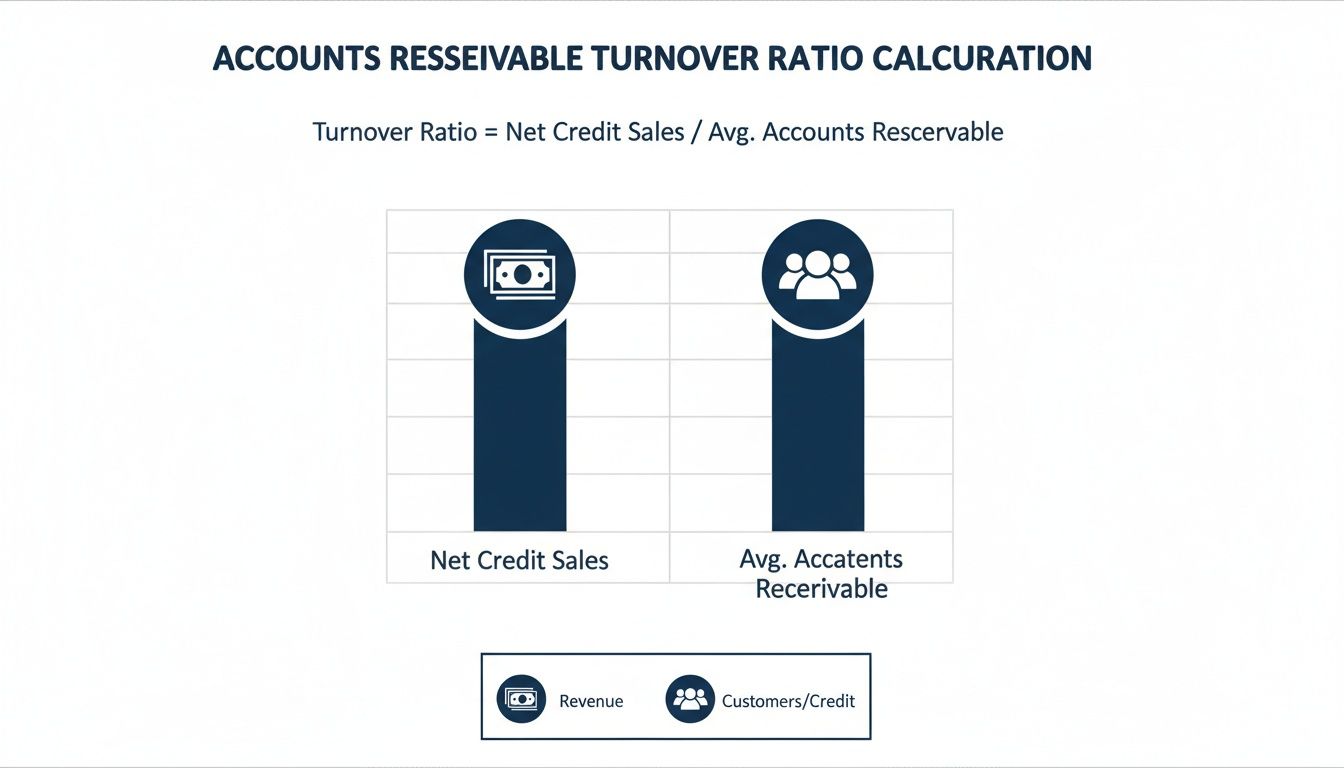

To help you get a handle on this, the table below breaks down the two main parts of the ratio.

Quick Guide to Accounts Receivable Turnover

This simple breakdown shows the two key ingredients in the accounts receivable turnover calculation and what they really mean for your business.

| Component | What It Means | Why It Matters |

|---|---|---|

| Net Credit Sales | The total sales you made to customers who didn't pay you right away. | This is the pile of money you are waiting to collect. |

| Average Accounts Receivable | The average amount of money customers owed you during a specific time. | This shows the typical size of your unpaid invoices. |

Understanding these two parts is the first step. When you track them, you're not just doing bookkeeping; you're learning how to manage your cash flow better.

A Simple Guide to Calculating Your Turnover Ratio

Math doesn't have to be scary, and figuring out your accounts receivable turnover ratio is pretty easy. Think of it like a recipe with just two ingredients. Let's walk through it step-by-step so you can feel good about doing this for your own business.

Here's the formula:

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

Business owners have used this for a long time to understand their cash flow. The only trick is to use the right numbers for each part of the formula. Let's break down where to find them.

Step 1: Find Your Net Credit Sales

First, you need your Net Credit Sales. This is the total amount of sales you made on credit—in other words, any sale where the customer didn't pay you on the spot.

It's important to only use credit sales here. Why? Cash sales don't create an "I owe you." If a customer pays you right away, there's no money to collect later, so we leave those sales out of this calculation.

You also need to subtract any returns or refunds. For example, if a customer returned a product and you gave them their money back, that amount comes off the total. This gives you a more honest number for the sales you actually expect to get paid for.

Step 2: Calculate Your Average Accounts Receivable

Next up is your Average Accounts Receivable. This number gives you a good idea of the typical amount of money customers owed you over a certain period, like a year or a quarter.

To get this, you just need two numbers from your books:

- The amount customers owed you at the start of the period.

- The amount customers owed you at the end of the period.

Once you have those, the math is easy: add them together and divide by two. This gives you a much better average than just picking a number from a single day, which could be unusually high or low. For example, a bike shop might have an average of $83,333 in customer IOUs over a year. Calculating this average smooths out the ups and downs. If you want to dive deeper into how businesses use this, Netsuite.com offers a great overview.

Putting It All Together: A Real-World Example

Let's see how this works for a small graphic design company we'll call "Creative Sparks."

- They had $300,000 in Net Credit Sales for the year.

- Their customers owed them $20,000 at the beginning of the year.

- Their customers owed them $30,000 at the end of the year.

First, let's find their average accounts receivable:

($20,000 + $30,000) / 2 = $25,000

Now, we can put everything into the main formula:

$300,000 (Net Credit Sales) / $25,000 (Average AR) = 12

Creative Sparks has an accounts receivable turnover ratio of 12. This means they collected their average amount of IOUs about 12 times during the year—or, to put it another way, about once a month.

Understanding What a Good Turnover Ratio Looks Like

So, you’ve done the math and have your accounts receivable turnover ratio. Is a 5 good? Is a 10 better? The honest answer is: it depends on your industry.

A contractor building houses over several months will have a very different "good" number than a t-shirt shop that expects payment in 30 days. Comparing the two is like comparing apples and oranges; it just doesn't make sense.

This infographic gives a simple visual of the two main parts that determine your turnover ratio.

As you can see, your ratio is a balancing act between the sales you make on credit and the average amount of money tied up in IOUs at any given time.

What Does Your Ratio Tell You?

Your ratio isn't just a number; it tells a story about your business. It's a clue that helps you understand your cash flow and how your payment rules are working. A healthy ratio suggests you're good at collecting your money.

The key is to see your ratio not as a final grade but as a starting point for asking better questions. Are we collecting money efficiently? Are our payment terms too strict or too loose for our industry?

For example, a high turnover ratio is often a great sign. It usually means you're collecting payments quickly and have good cash flow. But, it could also mean your credit rules are too tight, which might scare off customers who need more time to pay.

On the other hand, a low turnover ratio is a clear warning sign. It often means customers are taking a long time to pay you, which can really hurt your cash flow. This might mean your collection process needs a tune-up or your credit rules are too relaxed.

Industry Benchmarks For Context

To give you a starting point, it helps to see what’s typical for different fields. Just remember, these are general guidelines. The real power comes from tracking your own ratio over time to see if you’re improving.

A healthy turnover ratio is a good sign of a healthy business, just like understanding what is a profit and loss statement gives you a clear view of your company's profits.

Here are some general benchmarks to see where you might stand.

Accounts Receivable Turnover Ratios by Industry

A look at typical accounts receivable turnover ratio ranges across different industries to help you benchmark your business.

| Industry | Typical Turnover Ratio (Annual) | Average Collection Period (Days) |

|---|---|---|

| Retail | 8 – 12 | 30 – 45 days |

| Manufacturing | 6 – 9 | 40 – 60 days |

| Professional Services | 7 – 10 | 36 – 52 days |

| Construction | 4 – 6 | 60 – 90 days |

Looking at these numbers, you can see how much payment times can differ. A construction company waiting for a project to hit certain stages will naturally have a lower ratio than a busy retail store. Your goal isn't to hit a specific number but to be healthy for your industry.

How Turnover Directly Impacts Your Cash Flow

Your accounts receivable turnover ratio isn't just a number to show your accountant. It's a direct measure of the cash you have on hand to run your business every day. Think of your unpaid invoices as a bucket of water you use to keep your company running.

A high turnover ratio means you're emptying and refilling that bucket quickly. This is good! It means you always have enough water (cash) for important things like paying your employees, buying supplies, or paying rent. You get paid fast, and that cash is ready to be used again.

On the other hand, a low ratio means the bucket is filling up very slowly. The water is just sitting there, out of reach. Even if you've made a lot of sales, you're left waiting for the cash you need to pay your own bills. That can be a very stressful and risky situation for your business.

From Turnover Ratio to Collection Days

To make this even more practical, you can flip the turnover ratio to figure out something called Days Sales Outstanding (DSO). This number is a bit more direct and answers a simple question: "On average, how many days does it take us to get paid after we make a sale?"

Calculating it is easy:

DSO = 365 / Accounts Receivable Turnover Ratio

Let's go back to our design company, Creative Sparks. We figured out they had a turnover ratio of 12.

Their DSO would be: 365 / 12 = 30.4 days

This tells them that, on average, it takes about 30 days to collect payment from a client. This number is super useful because you can compare it to your payment terms. If you ask customers to pay in 30 days ("Net 30"), a DSO of 30.4 days is great—it means your collection process is working perfectly.

Seeing your turnover ratio as a measure of time (DSO) makes the cash flow connection crystal clear. Every extra day you wait for payment is a day you can't use that money to grow your business.

The Real Cost of Slow Collections

When your turnover is low (and your DSO is high), you feel the pain right away. You might have to delay paying your own bills, which can hurt your relationships with suppliers. You could even be forced to get a loan just to cover normal costs, which adds interest payments to your budget.

This is why managing your turnover ratio is a key part of running a business well. It’s not just about nagging people for late payments; it’s about building a steady and predictable cash flow. Knowing when money will come in is key for smart planning and using good cash flow forecasting techniques.

When you know how fast you collect money, you can make much better decisions about hiring, expanding, and investing in your business.

Practical Ways to Improve Your Turnover Ratio

So, your accounts receivable turnover ratio isn't where you'd like it to be. Don't worry. You don’t need a complicated plan to fix it. Getting paid faster often comes down to a few simple, practical steps anyone can take to get cash flowing again.

The real goal here is to make paying you as clear, easy, and regular as possible for your customers. A few small changes can make a huge difference in how quickly that cash lands in your bank, giving you more control over your business's health.

Review Your Invoicing Process

Your invoice is the first—and most important—step in getting paid. If it’s confusing, wrong, or sent late, it slows everything down. As soon as the work is done, that invoice should be on its way.

Make sure every invoice clearly lists:

- A unique invoice number to keep track of it.

- A clear due date in bold, easy-to-see text.

- Good descriptions of the products or services.

- Simple instructions on how to pay.

This kind of clarity removes any confusion for your client and shows you're a professional. It's a small change that tells people you’re organized and serious about getting paid on time.

Establish Clear Credit Policies Upfront

Before you even start working with a new client, your payment rules should be crystal clear. You don't need a long, legal document. You just need to explain your expectations from the start.

This is also your chance to run credit checks on new clients, especially for bigger jobs. It’s much better to know about payment risks beforehand than to be surprised by a huge unpaid bill later. Setting these rules protects your business and avoids awkward talks down the road.

A strong credit policy isn't about being mean; it's about making sure everyone is on the same page. When everyone knows the rules from day one, there are fewer problems later.

This proactive approach is key to managing your cash flow and keeping your business healthy.

Make Paying as Easy as Possible

Put yourself in your customer’s shoes. If paying you is a pain, they’re going to put it off. The easier you make it, the faster you’ll get your money. That means offering different ways to pay, like credit cards, bank transfers, or online payment sites.

If you really want to speed things up, look for ways to automate invoice processing. Automation can send out invoices and payment reminders without you having to do anything, freeing you up to focus on running your business.

A simple nudge can also work wonders. Think about offering a small discount—even just 1-2%—for customers who pay early. This little reward can encourage clients to pay your bill first, which directly speeds up your collections and boosts your turnover ratio.

Common Mistakes to Avoid With Your Turnover Ratio

The accounts receivable turnover ratio is a great tool, but it's easy to misunderstand if you’re not careful. Like any tool, using it the wrong way can cause problems.

Let’s look at a few common mistakes I see business owners make. Knowing about these will help you use this number as a helpful guide, not a source of stress.

Comparing Your Business to the Wrong Industry

One of the biggest traps is comparing your ratio to a totally different kind of business. A construction company with long projects will naturally have a much lower turnover ratio than a coffee shop that gets paid right away.

Judging your number against an unrelated business is a recipe for needless worry. Always stick to benchmarks for your specific industry to get a realistic picture of how you're doing.

Focusing on a Single Number

Another common mistake is treating your turnover ratio like a one-time grade on a test. A ratio of 8.5 today doesn't tell you much by itself. The real story comes from watching the trend over time.

Is your ratio climbing from 7 to 8 to 9 over a few quarters? Great! That shows your collection efforts are working. Is it slowly dropping? That’s a clear signal to figure out what's causing the slowdown. The context is what matters most.

Your turnover ratio is more like a speedometer than a finish line. It tells you your current speed and whether you’re speeding up or slowing down, helping you make changes as you go.

Chasing a High Ratio at All Costs

Finally, don't try to get the highest ratio possible no matter what. It's easy to think a super-high number is always best, but it can backfire.

If you make your payment rules too strict—like demanding payment in 10 days—you might improve your ratio but lose good customers to competitors who are more flexible. The goal is to find a healthy balance that keeps cash flowing without losing sales.

Frequently Asked Questions About Accounts Receivable Turnover

Even if you understand the basics, you might still have a few questions about what this all means for your business. Let's break down some of the most common ones I hear.

Can My Turnover Ratio Be Too High?

Believe it or not, yes. While a high number is usually a sign of good collections, an extremely high ratio can be a red flag. It might mean your credit rules are way too strict.

If you’re demanding payment in 10 days or hardly ever let customers pay later, you could be turning away business. Good customers who just need a little flexibility might go somewhere else. It’s all about finding that sweet spot—getting your cash quickly without making it so hard that you scare off potential customers.

What Is the Difference Between Accounts Receivable and Inventory Turnover?

This is a great question because both are “turnover” ratios, but they measure two completely different parts of your business.

- Accounts Receivable Turnover is about how fast you collect cash from sales you’ve already made on credit. It’s a measure of your collections process.

- Inventory Turnover measures how fast you sell the products you have on your shelves. This one is all about how well you manage your sales and stock.

Here’s a simple way to think about it: inventory turnover is about turning products into invoices. Accounts receivable turnover is about turning those invoices into actual cash.

How Often Should I Calculate My Turnover Ratio?

There isn’t one perfect answer, but being consistent is key. For most businesses, calculating your accounts receivable turnover quarterly is a good rhythm. It’s often enough to help you spot trends before they become big problems, but not so often that you get lost in small changes that don't mean much.

However, if cash flow is really tight or you're changing your credit rules, checking it monthly can give you faster feedback. An annual calculation is great for year-end reviews and looking at the big picture, but it’s too slow to help you manage problems as they happen.

Managing your accounts receivable turnover is a critical piece of your financial health puzzle. If you’re struggling to find the time or expertise to stay on top of it, MyOfficeOps can help. Our team provides the bookkeeping and advisory support you need to turn your financial data into clear, actionable insights for growth. Learn more at https://myofficeops.com.