Some months, your budget feels less like a plan and more like a polite fiction.

You start the quarter thinking payroll is covered, jobs are moving, patients are scheduled, and overhead is under control. Then a software renewal hits. A supplier invoice lands early. Overtime climbs. One project slows down or a few appointments cancel, and suddenly the numbers you approved a few weeks ago no longer match real life.

That is where a lot of small business owners get stuck.

They do have a budget. It sits in QuickBooks, Excel, or a spreadsheet someone updates once a month. But it does not help them decide anything. It does not answer simple questions like these:

- What can we cut without hurting service

- What should we spend more on because it drives profit

- Which costs are just leftovers from last year

- How do we budget when revenue is uneven

If that sounds familiar, you are not bad with money. You are probably using a budgeting method that was built for convenience, not clarity.

That is why more owners start asking what is zero based budgeting when the old way stops working. Zero-based budgeting is not fancy finance language for slashing costs. It means you stop assuming last year’s spending deserves a place in this year’s budget.

You wipe the page clean. Then you rebuild the budget based on what the business needs now.

For small and midsize businesses, especially ones with uneven cash flow, that shift can be a relief. Instead of arguing with a stale spreadsheet, you can build a budget around jobs in progress, patient volume, staffing needs, software usage, and the goals you are trying to reach.

That Feeling When Your Budget Is Just a Guess

A contractor finishes a strong quarter and assumes the next one will look similar. So the budget carries over. Office overhead stays the same. Subcontractor assumptions stay the same. Software stays in the plan because it was there before.

Then weather delays work. A bid gets pushed. Cash comes in later than expected. The budget did not fail because someone made a dumb mistake. It failed because it was built on memory.

A medical practice runs into a different version of the same problem. The owner expects patient volume to stay steady, so staffing and admin costs roll forward with only minor edits. But schedules shift, overtime creeps up, and a few recurring expenses nobody questions keep draining cash in the background.

Why this happens

Most small business budgets are built with one assumption. Last year’s spending must have been mostly right.

That sounds harmless. It is not.

When you build this year’s budget by tweaking old numbers, you also keep old habits. You keep subscriptions no one uses much. You keep processes that are slower than they should be. You keep costs that once made sense but no longer support the business you are running today.

What owners usually feel

The stress is not just about overspending. It is about not knowing.

You may recognize some of these thoughts:

- “We are busy, so why does cash still feel tight?”

- “I know we spend too much somewhere. I just can’t see where.”

- “I don’t want to cut the wrong thing and create a bigger problem.”

- “Our revenue moves around too much for a rigid budget.”

A budget should help you make decisions. If it only records what already happened, it is not doing enough.

Zero-based budgeting gives you another path. Instead of asking, “What did we spend last time?” you ask, “What do we need now, and why?” That sounds simple because it is simple. The work is in providing honest answers.

What Zero-Based Budgeting Really Means

Zero-based budgeting means you start each budgeting cycle from zero and justify every expense before you put it in the plan.

Not some expenses. Every expense.

That is the basic answer to what is zero based budgeting. You do not begin with last year’s numbers and make small adjustments. You begin with a blank page and build from there.

Packing a suitcase provides a good analogy

Traditional budgeting is like packing for a trip by grabbing last year’s suitcase and stuffing in a few extra things. You assume what was packed before still belongs there.

Zero-based budgeting is different. You empty the suitcase onto the bed. Then you ask about each item.

Do I need this?

Does it help?

Is there a cheaper option?

Is there a better option?

Should this be left behind completely?

That is the mindset.

It was built to challenge autopilot spending

Zero-based budgeting was developed in the 1970s by Pete Pyhrr at Texas Instruments to help organizations reduce costs. Unlike traditional methods, it requires every line item to be justified from scratch each cycle. Research from Bain & Company, cited by Oracle, says clients using this method consistently achieve 15–25% cost reductions by identifying waste that builds up under older budgeting systems (Oracle on zero-based budgeting).

For a small business owner, that does not mean you need a giant finance department. It means you stop giving automatic approval to old spending.

What you are really asking

A zero-based budget forces better questions than a normal budget does.

Good ZBB questions

- Is this expense necessary now

- What job does it do

- Does it support revenue, service, compliance, or operations

- What happens if we reduce it

- What happens if we remove it

- Can we buy the same result in a simpler way

That last question matters a lot for service businesses. Owners often focus on total cost, but the better question is whether the expense earns its place.

A software subscription is a good example. If the tool saves time, improves billing, helps scheduling, or supports job costing, keep it. If nobody can clearly explain why you still pay for it, it belongs under review.

This is not just cost cutting

People hear “justify every dollar” and think layoffs, cuts, and panic. That is not the main point.

A good zero-based budget helps you move money with purpose. You might cut a weak expense so you can protect a stronger one. You might reduce clutter in the budget so you can hire the right person, support a new service line, or invest in a system that pays off.

Zero-based budgeting is not about spending less at all costs. It is about spending on purpose.

That is why the method works. It replaces habit with choice.

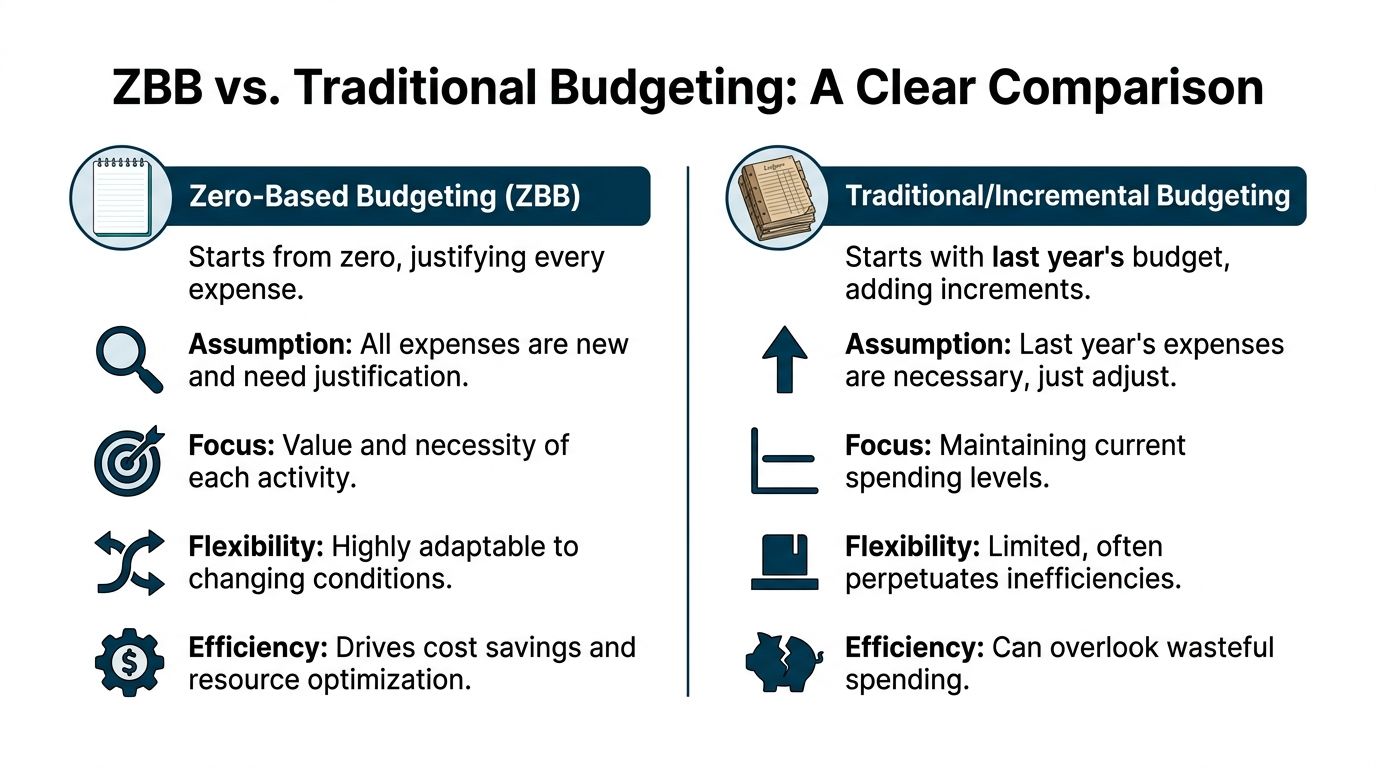

How ZBB Differs From Your Current Budget

The biggest difference is simple. Traditional budgeting protects the past. ZBB tests the present.

If your current budget starts with last year’s actual spending, then adds or subtracts a bit, you are using some form of incremental budgeting. That method is common because it is fast. It is also why so many budgets carry dead weight.

The short version

Traditional budgeting asks, “What changed?”

Zero-based budgeting asks, “Why does this belong in the budget at all?”

That one shift changes everything.

Traditional budgeting vs. zero-based budgeting

| Aspect | Traditional (Incremental) Budgeting | Zero-Based Budgeting (ZBB) |

|---|---|---|

| Starting point | Last year’s budget | Zero |

| Basic assumption | Existing spending is mostly valid | No spending is automatic |

| Review level | Changes get attention | Every line gets justified |

| Main focus | Continuity | Necessity and value |

| Speed | Faster | Slower at first |

| Flexibility | Lower | Higher |

| Waste risk | Higher, because old costs can stay hidden | Lower, because each cost must earn approval |

| Best use | Stable operations with few changes | Businesses that need sharper control and better choices |

What traditional budgeting misses

Say your firm spent money on three admin tools last year. One is used every day. One overlaps with another system. One was useful during a temporary workflow change that no longer exists.

In a traditional budget, all three often stay. Maybe each gets a small price increase. Nobody reviews the reason for the spend because the conversation stays focused on the change, not the baseline.

That is how cost creep happens.

Signs you are running an incremental budget

- You start planning by opening last year’s spreadsheet

- Most line items roll over automatically

- Team leaders defend increases but not the base spend

- You know certain costs feel wrong, but they remain in the budget

- Your budget becomes less useful when conditions change

What ZBB changes in day-to-day management

An evidence-based summary from EBSCO describes traditional budgeting as repetitive and cost-accounting oriented, while ZBB is decision-oriented and requires justification at every stage (EBSCO overview of zero-based budgeting).

That matches what happens in practice. The budget becomes less of an accounting file and more of a management tool.

For example:

- In construction, instead of carrying forward overhead because “that is what office support costs,” you tie spending to active jobs, expected field activity, and the support each project needs.

- In healthcare, you stop treating staffing or admin tools as fixed assumptions and start linking them to patient flow, scheduling pressure, and overtime risk.

- In professional services, you ask whether subscriptions, contractors, and support roles help delivery and margin right now.

If your business changes month to month, this approach pairs well with regular reforecasting. A rolling forecast can help you adjust the plan as conditions change instead of waiting for the next annual budget cycle.

The trade-off nobody should hide

Zero-based budgeting is better at surfacing waste. It is also more work.

You will spend more time discussing expenses. Managers may feel challenged. Some people will say, “We have always done it this way.”

They are not wrong about the effort. They are wrong if they think the old method is free. Incremental budgeting saves time upfront, then costs you money later.

Why Zero-Based Budgeting Works for Small Businesses

A lot of owners assume zero-based budgeting is only for giant companies with huge finance teams. That is one of the reasons the method gets ignored when it could be most useful.

Small businesses usually feel waste faster than large ones do. A big company can hide a bad expense inside a massive budget. A smaller company feels it in cash flow, margin, and owner stress.

It matches the way SMBs operate

Deloitte’s analysis says ZBB allocates funding based solely on efficiency and necessity, and organizations using it have achieved 10–25% operating expense reductions in the first year (Deloitte on zero-based budgeting).

For a small business, that principle matters more than the headline number. You do not have room to fund things “just because.” Every recurring payment competes with payroll, hiring, owner compensation, and growth.

Three SMB examples

Professional services

A law firm, agency, or IT consultancy often collects software over time. Proposal tools, CRMs, project apps, file storage, e-signature platforms, time tracking, reporting tools. One by one, each choice can make sense. Taken together, they can become a mess.

Zero-based budgeting forces a clean review.

- Which tools are required for delivery

- Which ones reduce labor

- Which ones overlap

- Which ones are nice to have, but not worth the cost

That creates room for stronger spending. Maybe you keep the tool that improves billing speed and cut the one nobody opens.

Healthcare practices

A clinic cannot budget the same way a retail shop might. Staffing, scheduling, billing support, and overtime all move with patient demand.

A useful ZBB approach asks whether each admin and staffing cost supports care delivery, compliance, and scheduling efficiency. It also helps owners look past habit. If a piece of software only deserves a place because “we have always had it,” that is not enough.

Construction and trades

Construction businesses deal with timing problems all time. Jobs shift. Materials move. Bids are uneven. Collections lag. That makes last year’s overhead a weak guide for this year’s budget.

ZBB works well here because it can be tied to project activity. Instead of dumping everything into one broad overhead bucket, you look at subcontractor fees, office support, software, vehicles, and field costs in the context of current work.

It helps with strategic choices

A small business budget should help answer real questions:

- Can we afford a hire

- Should we open a new location

- Do we need that software

- Can we survive a slow quarter without panic cuts

- Where should extra cash go first

If you want more ways to review cost pressure without cutting blindly, this guide on how to reduce business expenses gives a practical next step.

It gives owners a calmer way to lead

Owners are often carrying financial stress alone. They know spending needs tighter control, but they do not want to create fear inside the business.

That is another reason ZBB fits smaller companies. It makes spending conversations more objective.

Instead of saying, “We need to cut because things feel tight,” you can say, “We are reviewing every cost against what the business needs now.”

That is a healthier conversation. It gives people a standard. And when the standard is clear, decisions get easier.

Small businesses do not need a more complicated budget. They need a more honest one.

A Practical Guide to Implementing ZBB in Your Business

Most owners make zero-based budgeting harder than it needs to be. They think it requires a massive annual finance project. It does not.

For a small or midsize business, the practical version is simpler. You build from zero for the period ahead, justify the key expenses, and tie spending to what the business expects to produce.

A key challenge for SMBs is variable cash flow. In businesses like construction or healthcare, revenue can fluctuate 30–50% quarterly, and a more flexible business-focused ZBB model can help owners capture 15–20% profitability gains seen in advisory benchmarks when they justify spending against job profitability KPIs instead of forcing a rigid monthly model (Citizens on zero-based budgeting for variable cash flow).

Start with goals, not expenses

Do not open the expense list first. Start with what the business needs to do.

For the next period, define a few concrete targets:

- Protect payroll stability

- Improve cash flow visibility

- Hit a job profitability target

- Support patient volume without waste

- Fund a key hire

- Reduce unnecessary overhead

If you skip this step, you end up debating costs in isolation. A budget should serve goals, not the other way around.

Group costs into decision packages

You do not need to justify every paper clip one by one. Group related expenses into useful buckets.

For example:

| Business type | Useful decision package examples |

|---|---|

| Professional services | Client delivery software, admin support, business development, contractor support |

| Healthcare | Front desk staffing, scheduling tools, billing support, clinical support software |

| Construction | Field labor support, subcontractor coordination, project management tools, office overhead tied to active jobs |

This helps you ask a better question: what does this activity cost, and what value does it create?

Justify each package in plain language

Each package needs a short business case.

Questions to ask

- What does this support

- Is it necessary, useful, or optional

- What happens if we reduce it

- What happens if we cut it

- Is there a lower-cost way to get the same result

Keep the answers short. If a manager cannot explain a cost clearly, that usually tells you something.

A lot of owners find it helpful to review bank and card activity while doing this work. If you want a simple companion guide on expense tracking habits, Smart Receipts has a practical article on how to manage business expenses.

Build for uneven revenue

This is the part most generic ZBB advice misses.

If your cash flow moves around, your budget cannot act like income is smooth when it is not. A contractor might budget by project stage. A clinic might budget around expected patient volume and staffing pressure. A consulting firm might budget around active client load and delivery capacity.

What works better than a rigid monthly model

- Construction firms can justify spending against expected gross profit by job, not just office totals.

- Healthcare practices can tie admin and staffing support to scheduling demand and billing workload.

- Professional service firms can budget around current retainers, pipeline quality, and labor needed for delivery.

That is still zero-based budgeting. You are still starting fresh. You are just building the budget around business drivers instead of pretending revenue arrives in a straight line.

Leave room for the unexpected

A small business budget that leaves no breathing room tends to break fast.

Zero-based budgeting does not mean pretending surprises will never happen. It means choosing your priorities first, then making room for normal uncertainty. Delays, repairs, billing slowdowns, and timing issues are part of business life.

A useful budget is not the one with the prettiest spreadsheet. It is the one that still works when the month gets messy.

Review it often enough to matter

A budget built from zero loses value if you write it once and ignore it.

Use a simple review rhythm. Monthly works for many firms. Some businesses with choppy revenue need more frequent check-ins. Compare actual spending against the purpose each expense was meant to serve, not just against a number.

For owners who want help building a cleaner process, a resource on how to create a business budget can provide a good framework. Some businesses also use outside support from bookkeeping teams, FP&A tools, or advisory firms such as MyOfficeOps to maintain the structure and review cycle.

Common Pitfalls and How to Sidestep Them

Zero-based budgeting is simple to explain and harder to run well. Most problems show up in the same places. The good news is they are manageable if you know where the process tends to wobble.

Pitfall one. Trying to review everything at once

This is the fastest way to overwhelm your team.

If you try to rebuild the entire budget in full detail on the first pass, people get tired, rushed, and sloppy. Then they blame the method.

Better approach

- Start with the biggest spending categories

- Review the cost areas that feel least clear

- Pilot the process in one department or one expense group

- Build a repeatable template before expanding

A smaller, cleaner review beats a giant messy one.

Pitfall two. Turning it into a fear exercise

When owners say “every dollar must be justified,” teams sometimes hear, “Cuts are coming.”

That reaction is normal. It also makes people defensive. They start protecting budgets instead of discussing value openly.

Better approach

Talk about the purpose early.

- Explain what the business is trying to protect

- Show how spending links to goals

- Ask managers for options, not just defenses

- Keep the conversation tied to business value, not personal territory

You want people to think like owners, not like survivors.

Pitfall three. Treating all costs as fixed forever

One reason ZBB works is that it pushes leaders to tie more spending to activity levels instead of treating everything as locked in.

Abacum notes that in mature ZBB adopters, 48% of costs become variable compared with 20% in traditional models, and this level of detail can uncover hidden leaks and free up 10–20% of cash for strategic goals. The same source gives a useful practical example. A clinic might justify software only if it cuts overtime by 20% (Abacum on zero-based budgeting methods).

That is a useful lesson for SMBs. The more you can connect costs to work volume, service levels, or job activity, the easier it becomes to adjust without panic.

Pitfall four. Weak tracking after the budget is approved

A lot of businesses do the hard part once, then lose the benefit because reporting is too vague.

If your bookkeeping categories are messy, or your reports arrive late, you cannot tell whether an expense still earns its place. That is when the budget slowly turns back into guesswork.

Better approach

Use tools and reports that let you see spending clearly.

- Accounting software like QuickBooks can help organize categories and actuals.

- Expense management tools help track recurring charges and employee spending.

- KPI dashboards can connect costs to labor, utilization, overtime, collections, or job profitability.

- Forecasting tools help you adjust as volume changes.

Pitfall five. Forgetting that the first cycle is supposed to feel awkward

The first ZBB cycle usually feels slower than expected. That does not mean the method failed. It means the business is learning how to talk about spending in a sharper way.

If your first pass feels a little clunky, that is normal. What matters is whether each round makes spending easier to explain and easier to control.

The goal is not perfection. The goal is a budget you can trust.

Let an Expert Guide Your Financial Strategy

By the time most owners start asking what is zero based budgeting, they are not looking for theory. They want relief. They want a budget that reflects the business they are running, not a leftover version from last year.

That is the true value of this approach. It moves you from automatic spending to intentional spending. It helps you see which costs support service, growth, and margin, and which ones are just hanging around.

The hard part is time.

A business owner already has enough to manage. Rebuilding budget assumptions, cleaning up categories, reviewing recurring costs, tying expenses to operations, and then tracking the results takes attention most owners do not have to spare.

That is where outside financial support can make the process more practical. If you are comparing the types of professionals who help with budgeting, forecasting, and cost analysis, this overview of Financial Analysts gives useful context on what that role typically covers.

The right advisor does more than hand you a spreadsheet. They help structure the review, challenge weak assumptions, connect the numbers to business decisions, and turn the budget into something you can use.

If your books are behind, reporting is slow, or your budget never seems to match reality, zero-based budgeting can become frustrating fast. If your books are clean and your decision process is disciplined, it becomes a strong operating tool.

That is the difference. Not the template. The guidance.

If you want help building a budget that fits real cash flow, real overhead, and real business goals, MyOfficeOps works with small and midsize businesses on bookkeeping, forecasting, KPI reporting, and CFO-level advisory so owners can make financial decisions with more clarity and less guesswork.