If you run an agency, law firm, consulting practice, or IT services company, you probably know this feeling. Revenue looks decent. The team is busy. Clients are asking for more work. But when you open your financial reports, you still can't answer basic questions with confidence.

Are your biggest clients profitable? Which projects make money and which ones just keep everyone occupied? Why does cash feel tight when sales look fine?

That confusion usually isn't a bookkeeping problem alone. It's a mismatch between generic accounting and the way service firms operate. Accounting for professional services firms has to do more than keep the books clean for tax time. It has to show you how time, pricing, staffing, billing, and collections affect profit in real life.

A product business can count units on a shelf. Your firm can't do that. Your inventory walks in every morning, logs into Slack, joins client calls, and tracks time. That's why owners of service firms need numbers that connect operations to money, not just a standard profit and loss statement.

Why Your Service Firm's Accounting Is Different

A retail business buys inventory, sells inventory, and tracks margin on each item sold. A service firm sells expertise. That's a different animal.

If you're running a creative agency, you don't buy a pallet of logos and ship them out. If you own a law practice, you don't manufacture legal advice. If you lead an IT consulting firm, you aren't storing implementation work in a warehouse. You earn revenue by turning your team's time, judgment, and specialized skill into client outcomes.

Your team is the inventory

That one difference changes almost everything.

Professional services firms operate under different financial constraints than product businesses. Profitability depends on metrics like utilization rates, effective billing rates, and project margins, not inventory management. Firms in this model also put a heavy focus on recurring revenue for stability, with established firms targeting 40-60% recurring revenue and mature firms reaching 60-80%, according to professional services growth benchmarks from Rework.

When owners use a basic bookkeeping setup built for a shop or contractor, they often get reports that are technically correct but operationally useless. The books may tell you what happened last month. They often won't tell you why.

Practical rule: If your accounting system can't show profit by client, project, or service line, it can't help you make pricing and staffing decisions.

The pain usually shows up in three places

Most owners first feel the problem in daily operations, not in the general ledger.

- Project pricing gets fuzzy: You quote based on what feels fair, then hope the work comes in close to budget.

- Cash flow gets lumpy: A good month of invoices doesn't always mean a good month in the bank.

- Busy gets confused with profitable: Teams work hard, calendars stay full, and margins still shrink.

Here's a simple example. A branding agency may have two clients paying the same monthly retainer. One client gives fast feedback, stays inside scope, and uses one account manager. The other drags projects out, adds revisions, and pulls in senior staff repeatedly. On paper, both clients look equal. In practice, one may be carrying the other.

Why standard reports miss the real story

A normal P&L groups expenses into broad buckets like payroll, software, rent, and contractors. That's useful, but it's not enough. Service firms need to know where those costs are being consumed.

That means accounting for professional services firms has to connect financial data to delivery data. Not just revenue and expense. Time by person. Costs by project. Billing by client. Collections by invoice. Write-offs by engagement type.

Once you start looking at the firm that way, the chaos starts to make sense. The issue usually isn't that the business is impossible to understand. It's that the reporting was built for the wrong business model.

Setting Up Your Financial Foundation

Before you can get good answers, you need the right structure. Most firms skip this part because it sounds boring. Then they spend years fighting messy reports.

A solid foundation for accounting for professional services firms has two pieces. First, a chart of accounts that matches how a service business works. Second, revenue recognition that reflects when work is earned, not just when an invoice goes out.

Build a chart of accounts that fits the business

Think of your chart of accounts like folders on a computer. If the folders are vague or messy, you can still save files, but good luck finding anything later.

A service firm's chart of accounts should help you answer questions, not just satisfy your tax preparer. If everything goes into broad buckets like "income" and "expenses," you'll get a report that looks clean and tells you very little. A better setup groups revenue and costs in a way that reflects how you sell and deliver work.

A simple service-firm chart might look like this:

| Account area | Examples |

|---|---|

| Revenue | Retainer revenue, hourly service revenue, fixed-fee project revenue, reimbursable income |

| Direct delivery costs | Direct labor, contractor costs by service line, project software, reimbursable expenses |

| Operating expenses | Admin payroll, rent, insurance, general software, marketing |

| Balance sheet items | Accounts receivable, deferred revenue, work in progress, payroll liabilities |

If you want a plain-English overview of how these account buckets work, this guide on what a chart of accounts is is a useful starting point.

Revenue isn't earned when cash hits the bank

Many firms get tripped up by this.

If a client pays you upfront for a long engagement, it feels natural to call that revenue right away. But you haven't earned it all on day one. You earn it as you deliver the work.

Under ASC 606, accrual-based accounting is the standard for professional services firms. Revenue is recognized as services are delivered. In one example from NetSuite, a $500K, 6-month contract is recognized proportionally over time based on hours or milestones. The same source notes that non-compliant firms can see 20-25% profit margin volatility, while proper adoption can increase margins by 10-15% because the books reflect the actual economics of the work rather than invoicing timing, as explained in NetSuite's guide to accounting for professional services.

A cash-basis report can make one month look fantastic and the next month look terrible, even when delivery was steady in both.

What a good foundation looks like in practice

Good structure is usually simple, not fancy.

- Separate revenue by type: Keep hourly, project, retainer, and reimbursable revenue in different buckets.

- Split direct delivery costs from overhead: That makes project margin easier to see later.

- Track deferred revenue and work in progress properly: Especially when billing timing doesn't match service delivery.

- Use classes, locations, tags, or projects consistently: QuickBooks Online, Xero, and similar systems can all support this if the setup is thoughtful.

What doesn't work is bolting project reporting onto a bad accounting structure after the fact. If the foundation is off, every dashboard built on top of it will be shaky.

How to Track Your Real Profitability

Most firms know their total revenue. Far fewer understand which work produces healthy margin.

That's the gap that causes bad pricing, overloaded teams, and clients that seem important but undermine the business. A common issue in accounting for professional services firms is that the books are compliant enough for year-end reporting, but they don't break profit down in a way management can use.

A key blind spot is project-level profitability visibility. Many firms still don't have systems that allocate costs well by project, client, or department. That makes it hard to explain shrinking margins or make smart pricing and staffing decisions, especially when the firm handles a mix of hourly, fixed-fee, and retainer work, as noted in this discussion of accounting challenges for professional services.

Start with the path from time to invoice

Real profitability tracking starts with one rule. Every hour of work should connect to a client and a project, even if that project is non-billable internal work.

That sounds obvious, but many firms still let people dump time into broad categories like "client work" or skip time tracking altogether on fixed-fee jobs. That's how profit disappears. If you don't know where labor went, you can't know what the work cost.

The clean workflow looks like this:

Team members track time to the right project

Not just to the client. The project matters because a retainer client may have multiple workstreams with different margins.

Payroll and contractor cost get mapped back to delivery

Salaries don't need to be billed by the hour to be costed by the hour. You still need a way to assign labor cost to the work performed.

Invoices follow the same structure

Whether you bill hourly, by milestone, or by retainer, the invoice should map back to the same project records.

Reports compare revenue against fully loaded project cost

That's where you find out if the engagement is healthy.

What should be assigned to projects

Many owners stop at labor. That's a start, but it isn't enough.

A real project view usually includes a mix of direct and indirect cost inputs:

- Labor cost: Salaries, payroll taxes, and benefits tied to delivery staff

- Contractor cost: Freelancers, specialists, and outsourced support

- Project software: Tools used for client work, such as design, legal, or PM platforms

- Reimbursables and pass-throughs: Travel, filing fees, media spend handling, and other client-specific costs

- Write-offs and discounts: These tell you where scope, billing, or collection problems are hitting margin

If a fixed-fee project always looks profitable before labor is assigned, that isn't a win. It's a reporting error.

Questions your reports should answer every month

Once project costing is set up, the conversation changes. You stop arguing about whether the team feels busy and start looking at evidence.

A useful profitability review should answer questions like:

| Question | Why it matters |

|---|---|

| Which clients generate the strongest margin? | Helps you protect and expand the right relationships |

| Which service lines lose money most often? | Shows where pricing or delivery is off |

| Where does non-billable time pile up? | Reveals management drag, scope creep, or poor internal process |

| Which fixed-fee projects run long? | Helps you redesign proposals and staffing |

Owners are often surprised by what this uncovers. The largest client isn't always the best client. The most prestigious project may be the least profitable. The underpriced retainer that "keeps everyone busy" may be draining senior capacity that could go to better work.

That's why operational reporting matters. Compliance accounting keeps you out of trouble. Profitability accounting helps you run the firm.

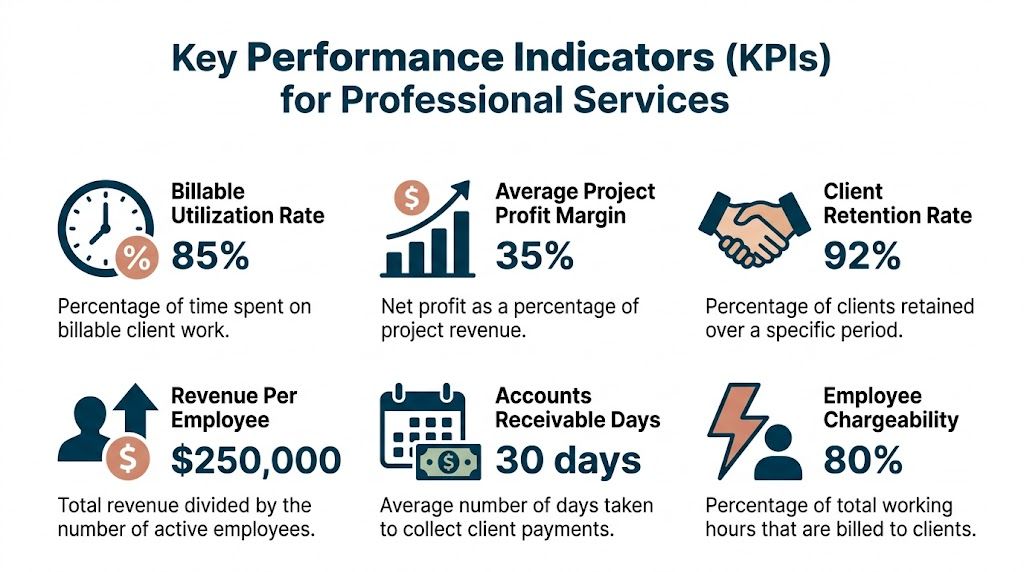

Your Dashboard of Key Performance Indicators

A busy owner doesn't need more reports. They need a short list of numbers that answer, "Are we running this firm well?"

That's what a good dashboard does. It turns accounting for professional services firms into a management tool, not a stack of PDFs nobody reads.

The five questions I want owners to answer fast

If you can't answer these without digging through spreadsheets, your reporting is too slow.

The first and most important is utilization. In professional services firms, utilization rate means the percentage of time spent on billable work. Sustainable benchmarks usually target 70-80%, and a 10% increase in firm-wide utilization can raise revenue per employee by 15-20% without additional hiring. The same analysis notes that low utilization correlates with negative project cash flows in 40% of cases, based on this professional services KPI review from Fyle.

That doesn't mean every person should be maxed out. Admin staff, partners doing business development, and managers handling internal work won't all land in the same spot. It does mean you should know whether low margin is caused by pricing or by too much paid time sitting outside client work.

Track a mix of efficiency and cash metrics

A practical dashboard usually includes:

- Utilization rate: How much paid delivery time is billable.

- Project profit margin: Whether the work is priced and staffed properly.

- Revenue per employee: A quick read on how well the firm turns headcount into revenue.

- Accounts receivable days: How long it takes to collect after invoicing.

- Client concentration: Whether too much revenue depends on one relationship.

- Retention by client type: Whether your best-fit clients stay.

For a more general small business dashboard framework, this overview of key performance indicators for small business can help you shape the reporting cadence.

Don't ignore collection speed

A service firm can look profitable on paper and still struggle because cash arrives too slowly. That's why I like to pair margin metrics with receivables metrics.

If you want a practical breakdown of how to calculate and monitor that number, this guide to mastering the accounts receivable days calculation is useful. It gives owners a simple way to understand whether billing and collections are supporting the business or slowing it down.

Strong dashboards don't try to measure everything. They highlight the few numbers that change decisions.

Common Bookkeeping Mistakes That Silently Kill Profit

Most profit leaks don't come from one dramatic mistake. They come from small habits that repeat every week.

A missed reimbursable expense here. A late invoice there. Time entered to the wrong client. Revenue booked when billed instead of when earned. Each issue looks minor on its own. Together, they can distort your reports and drain cash.

Sloppy invoicing is expensive

This one shows up constantly in service firms. Work gets done. Someone means to invoice it. The invoice goes out late, with the wrong detail, or with missing support. Then collections slow down, the client pushes back, and the staff has to fix paperwork instead of moving on.

That isn't just annoying. It's costly. In the professional services sector, 25% of surveyed companies needed to reissue over 3% of their invoices annually because of billing errors and collection issues, according to this Kinspeed report on professional services finance.

Three habits that hurt margin quietly

Here are the mistakes I see most often.

- Using cash-basis reports to run the business: Cash-basis accounting can be useful for some tax situations, but it often gives owners a false sense of performance during active projects. A prepaid engagement can make one month look rich while hiding future delivery cost.

- Failing to capture reimbursable costs: Filing fees, software passes, travel, subcontractor expenses, and client-specific purchases often slip through when teams don't have a tight expense process.

- Treating write-offs like random bad luck: Repeated write-downs usually point to a pricing problem, a scope problem, or weak approval controls.

Watch the handoff points

The biggest errors often happen where one process touches another.

A project manager approves work but doesn't close the billing milestone. A team member tracks time but uses the wrong code. The controller sends the invoice, but the client contact changed and nobody updated the record. That's how good work turns into collection friction.

A simple monthly review helps catch these issues before they pile up:

| Review item | What to look for |

|---|---|

| Unbilled time | Time entered but not invoiced |

| Aged receivables | Old invoices that need follow-up |

| Write-offs | Patterns by client, service, or PM |

| Reissued invoices | Repeat billing errors by team or process |

Billing problems usually aren't caused by one bad invoice. They're caused by a weak process that keeps producing bad invoices.

Good bookkeeping isn't just about clean records. In a service business, it's part of margin control.

Building Your Smart Accounting Tech Stack

Most firms don't need more software. They need fewer disconnected tools.

The right stack for accounting for professional services firms should do one thing well above all else. It should let data move cleanly from work performed to billable amount to financial reporting. If your time tracker says one thing, your project tool says another, and your accounting system says a third, you're going to spend hours reconciling noise.

Core accounting software is only the base layer

QuickBooks Online and Xero are common starting points for small and midsize service firms because they handle the general ledger, bank feeds, payables, receivables, and standard reporting well. But they don't solve operational accounting by themselves.

You usually need a few connected layers around them:

- Time tracking tools: Harvest, Toggl Track, BigTime, or built-in practice management tools

- Project management tools: Asana, ClickUp, Monday.com, or legal and consulting-specific systems

- Expense capture tools: Dext, Expensify, Ramp, or bill pay platforms

- Payroll systems: Gusto, ADP, Rippling, or the payroll module already in your stack

- Reporting and dashboard tools: Native reports, Fathom, Jirav, or custom management dashboards

Compare stacks by the problem you're solving

A better way to choose tools is to match them to your bottleneck.

If time entry is weak, start there. If invoice accuracy is the issue, focus on the handoff between project data and billing. If month-end takes too long, look at bank rules, expense capture, and payroll integration before buying another dashboard product.

Here's a simple comparison:

| Problem | Better tool priority |

|---|---|

| Missed billable hours | Time tracking tied to projects |

| Billing errors | Practice management or PSA tool with invoice workflows |

| Poor project visibility | Job costing and project reporting features |

| Too much manual entry | Integrated expense, payroll, and bank feed automation |

Integration matters more than feature lists

I've seen firms buy advanced systems and still work from spreadsheets because nobody mapped the workflow. I've also seen simple stacks work well because each tool had a clear job and the integrations were clean.

One practical resource for evaluating software is this roundup of best accounting software options. It helps owners compare categories and think through fit instead of chasing features.

If you need a framework for narrowing choices, this guide on how to choose accounting software is also worth reviewing. For firms that don't want to build and manage the whole system in-house, providers such as MyOfficeOps can handle bookkeeping, reporting, payroll integration, and advisory within one operating model.

What doesn't work is buying software to avoid process discipline. No tool fixes vague scoping, poor time entry, or inconsistent billing rules. Good software amplifies good process. Bad process just moves faster.

Your Path to Financial Clarity and Growth

Most owners don't need a more complicated finance department. They need a reliable way to get clean numbers, understand them, and use them.

That's the goal of accounting for professional services firms. Not prettier reports. Better decisions. You should be able to see which work is worth pursuing, where teams are stretched, when pricing needs to change, and why cash is tight before it becomes a problem.

Two workable paths

There are really two ways to get there.

The first is to build the process internally. That can work well if you have a disciplined team, a manageable level of service complexity, and someone in-house who owns the chart of accounts, project setup, billing rules, close process, and management reporting.

The second is to partner with an outside accounting and advisory team. That route makes sense when the firm is growing, project types are mixed, internal staff are overloaded, or leadership needs more than transaction processing.

Neither option is automatically right. The right choice depends on your capacity and how much decision support you need.

Signs you can keep it in-house

An internal model usually works if most of these are true:

- Your service mix is simple: Maybe you bill mostly one way, such as monthly retainers or straightforward hourly work.

- Your data discipline is already strong: Time entry is current, invoicing is consistent, and month-end closes don't drag.

- Someone owns reporting: Not just bookkeeping. Actual management reporting with follow-up and action.

Signs you need outside help

An external partner usually makes more sense when these show up:

- You can't trust project margin reports: Or you don't have them at all.

- Billing and collections keep creating friction: The same errors repeat, and old invoices pile up.

- Leadership is making pricing or hiring decisions without clear numbers: That's where growth gets expensive.

- Your controller or office manager is buried in transactions: They may be capable, but capacity is the issue.

Clean books are the starting point. Owners usually need someone to translate the books into staffing, pricing, and cash decisions.

A simple decision test

Ask yourself these questions:

| Question | If the answer is no |

|---|---|

| Can we see profitability by client or project? | You need better accounting design, not just better bookkeeping |

| Do invoices go out accurately and on time? | Your cash flow process needs attention |

| Can leadership explain margin changes clearly? | Reporting isn't connected to operations |

| Do we have time to manage systems and reporting internally? | Outside support may be more efficient |

Owners sometimes resist outsourced support because they think it means losing control. Usually the opposite happens. Good support gives you tighter processes, faster reporting, and better visibility. You still make the decisions. You just stop making them in the dark.

The firms that handle growth best usually do one thing well. They treat accounting as part of operations, not as an after-the-fact admin task. Once that shift happens, you stop asking, "What happened?" and start asking better questions, like, "Which work should we do more of?" and "What needs to change before margin slips again?"

If your firm needs cleaner books, clearer reporting, and better visibility into project profitability, MyOfficeOps can help you build the structure behind it. The team supports small and midsize businesses with bookkeeping, payroll integration, financial analytics, and advisory services so owners can move from financial guesswork to practical decision-making.